All About Crypto Exchanges

Cryptocurrency exchanges have come a long way since the launch of Bitcoin in 2009. Exchanges have played, and continue to play, a vital role in the acceptance of cryptocurrency by governments, businesses, and institutions worldwide.

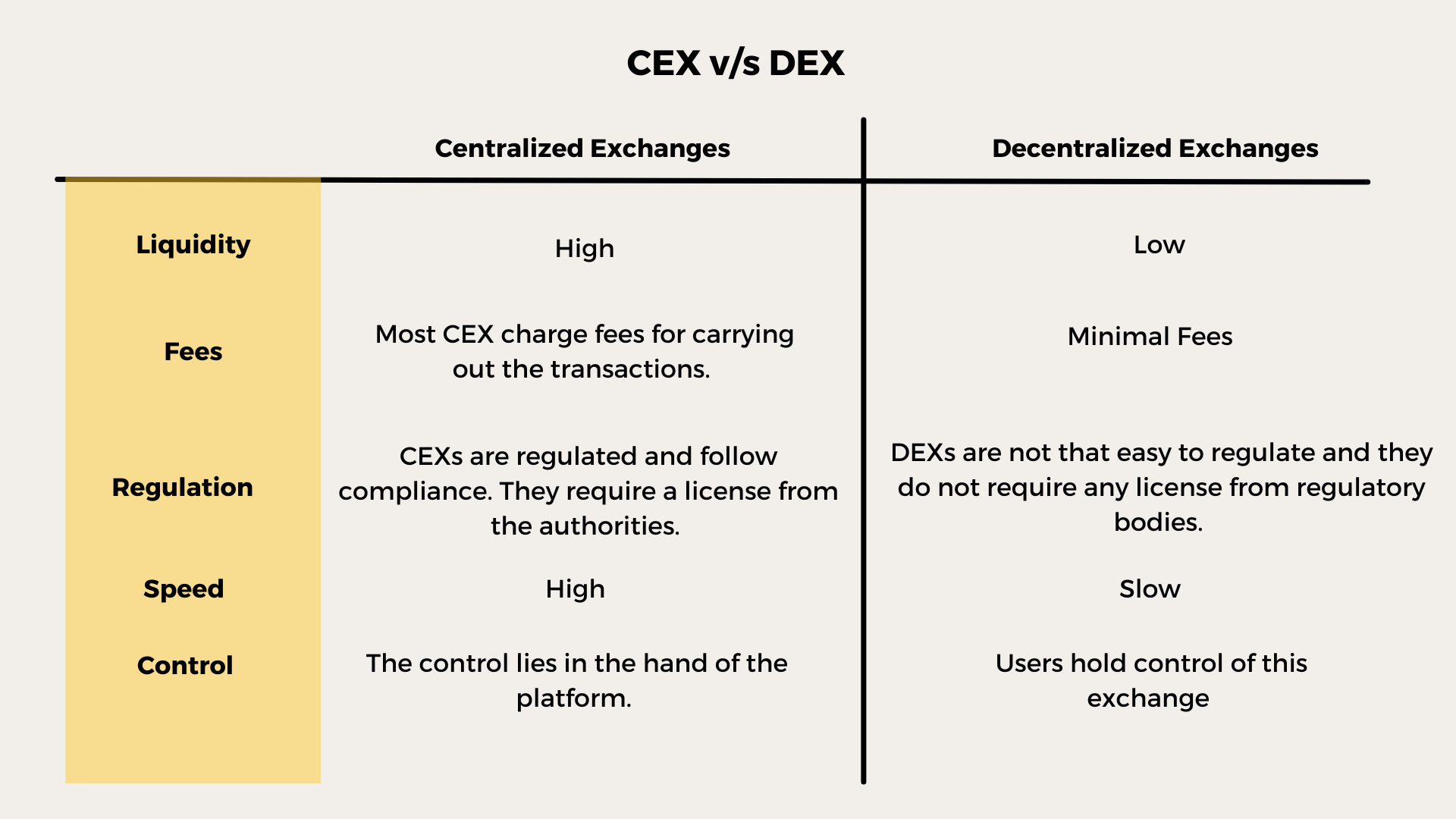

While majorly there are two types of exchange - Centralised and Decentralised - how they operate are very different, and their usage also tells about adoption, education and innovation in crypto.

Centralised Exchange (CEXs)

A platform where you can buy and sell digital assets such as cryptocurrency. In these types of exchanges, a third-party monitors and secures the transactions on behalf of the user. The blockchain system does not track these deals.

The centralised cryptocurrency exchanges require their users to verify their personal information before using their tools. If the user is an organisation, then it must provide some corporate information for verification. The verified users on these exchanges get to a higher withdrawal quota and other customer support in case of any technical error. The centralised cryptocurrency exchanges are quite popular among crypto enthusiasts since they are easy to use and follow all the compliance for their users' secured and easy crypto journey.

Every country has a few popular exchanges which follow domestic compliances and are registered under the jurisdiction of the land. For example, homegrown exchanges like CoinSwitch Kuber, CoinDCX, and WazirX have caught some attention in India, similar to Coinbase and BlockFi in the US and several other regions.

The core need for such exchanges is the ease of use, making exchanges one of the most lucrative businesses in the space, with the ambition of onboarding the subsequent billion users who are new to the crypto landscape.

Characteristic of Centralised Exchanges

Custodial Nature: Custodial Exchanges are the ones who are in possession of the crypto one buys on the platform. They are the custodians of the private keys. Trading is done off-chain, i.e., trading is tracked on their balance sheet instead of being verified by the blockchain. This allows transactions to be done quickly and cheaply but leads to a lack of transparency.

Transactions Via Fiat Currency: Centralised exchanges support buying and selling crypto assets through fiat currency. One can sell the cryptocurrency they are holding and withdraw the amount in fiat and vice versa. This makes a case for custodial exchanges robust among people who have just started exploring the space.

Security: Centralised exchanges offer an extra layer of security and reliability for transactions and trading. By facilitating the transaction through a developed, centralised platform, these exchanges offer higher comfort levels.

Regulatory Compliance: Centralised exchanges are subject to the regulations of the jurisdictions in which they operate, though these can vary considerably. In some countries, a single financial regulator has oversight of cryptocurrency businesses. For example, in the United States, regulation is more fragmented; some issues, such as licensing, are managed on a state-by-state basis, while other aspects of exchange policy, like KYC data collection and AML issues, are mandated by federal law.

Token Listing: Which tokens or cryptocurrency should be made available for trading is decided by the company running the exchange. There is not any say of the community except for expressing the demand. Also, most of these centralised exchanges have been accused of charging very high listing fees from project owners and also the allocation of a particular portion of the total supply to the exchange, which on most days might not be in favour of these projects as the same would be asked by other exchanges and very little would be left in the hands of the community.

Major Centralised Exchanges

Binance: Founded in 2017 by Changpeng Zhao, Binance is the world's biggest centralised cryptocurrency exchange. It alone facilitates transactions worth $40bn daily, which is more than the combined volume processed by its four most significant competitors.

As per a recent report by Bloomberg, Zhao, who is popularly known as CZ among cryptophiles has amassed a fortune of $96 bn, which is just below that of Oracle founder Larry Ellison and surpasses that of Mukesh Ambani, the Indian tycoon. Zhao's fortune could be significantly larger, as the wealth estimate does not consider his personal crypto holdings, including Bitcoin and his firm's own token - Binance Coin, now called BNB.

Coinbase: Coinbase is an app that lets one buy and sell all sorts of cryptocurrencies, like bitcoin, Ethereum, Litecoin and about 50 others. One can also use Coinbase to convert one cryptocurrency to another or send and receive cryptocurrency to and from other people.

Founded in 2012, Coinbase is the first major cryptocurrency exchange to go public in the United States. Many big-time influencers in the crypto space have been associated with Coinbase, including its co-founders - Brian Armstrong and Fred Ehrsam. Brian serves as the CEO of Coinbase while Fred moved on to establish a well known crypto-native investment and venture fund, Paradigm. Former a16z partner Balaji Srinivasan also served as the CTO at Coinbase as their company Earn.com was acquired.

FTX: Co-founded by one of the most exciting and influential founders, Sam Bankman-Fried, more popularly known as SBF, FTX is also one of the most unique and feature-rich exchanges for traders. Registered in the Bahamas, it is a sister company of popular quantitative cryptocurrency trading and investment firm Alameda Research which was also co-founded by the same bunch of founders - SBF and Gary Wang.

FTX's feature suite includes Spot and Future trading, Leverage of up to 20x, Volatility Tokens, Prediction Markets and even Tokenized Stocks - making it paradise for degens and full-time traders.

Kraken: Kraken is regulated by FinCEN in the US, FINTRAC in Canada, and the FCA in the UK – highlighting how safe and credible the platform is. Users can buy crypto using the 'Instant Buy' feature or Kraken Pro, the latter of which is a pure crypto exchange offering. Instant buys will have a 1.5% fee (plus an additional fee depending on your payment method), whilst Kraken Pro uses a maker/taker pricing structure.

Kraken has over 80 cryptocurrencies to trade and offers free crypto deposits on the most supported coins in terms of assets. Also, Kraken's staking feature is one of the best on the market, allowing users to earn rewards in just a few clicks and receive their payments twice per week!

Apart from these are multiple centralised crypto exchanges like Huobi, BitFinex, BitStamp, Bakkt, and others, and they are pretty significant in quite a few geographies and trading volumes.

Decentralised Exchanges

Simply put, a decentralised exchange (DEX) is a cryptocurrency exchange that operates without the need for a centralised authority. DEXs were created to remove the requirement for any authority to oversee and authorise trades performed within a specific exchange.

Decentralised exchanges are operated by code and allow peer-to-peer trading of cryptocurrencies. Peer-to-peer refers to a marketplace that links buyers and sellers of cryptocurrencies.

What if there are not enough coins to buy? This is where market players come into the picture.

Decentralised exchanges work with market makers, which are entities that facilitate trading and are always willing to buy and sell a particular asset, and by doing this, they provide liquidity. This helps users trade, and they do not have to wait for the other party to show up.

Characteristics of Decentralised Exchanges

Non-Custodial: Users of decentralised exchanges do not need to transfer their assets to a third party. Users get to keep control of their wallet's private keys. A private key is advanced encryption that enables users to access their cryptocurrencies. Users can immediately access their crypto balances after logging into the DEX with their private key. Therefore, there is no risk of a company or organisation being hacked, and users have assured more excellent safety from hacking and theft.

Anonymity: Decentralised exchanges do not ask users to enter private information, such as social security numbers or addresses, that centralised exchanges are compelled to require as part of banking and financial regulations. Thus far, because DEXs do not take control of assets, they have fallen outside such regulations.

Community Driven: Centralised exchanges work kind of like banks. However, there is no single actor on the other end in a truly decentralised exchange. While there might be a founder who initiated the idea and developed the platform, over time, the community and the developers run the platform through repeated iterations and governance voting.

Unvetted token listings: Anyone can list a new token on a decentralised exchange and provide liquidity by pairing it with other coins. This is usually done through a community vote, and while some exchanges do not charge for listing tokens there might be some other agreements that the players might deem fit.

Types of Decentralised Exchanges

DEXs operate on Smart Contracts, eliminating intermediaries. This setup allows users to create marketplaces operating on various mechanisms, and each mechanism has its own set of supporters. All mechanisms ideally focus on providing the best prices in exchange for the tokens and enabling cheap, fast, and reliable transactions.

Automated Market Maker(AMM)

Automated Market Makers (AMMs) are decentralised exchange (DEX) protocols for trading digital assets using algorithms instead of order books. Also, AMMs facilitate permissionless token swaps without intermediaries. Instead, AMMs use smart contracts, oracles, liquidity providers (LPs), and liquidity pools.

The AMM model uses liquidity pools or collections of crypto tokens to make trading possible via an algorithm that sets the token prices based on the changing ratio of tokens supplied. Liquidity providers (LPs) or market makers supply liquidity to pools in the form of digital assets. In return, they are rewarded with trading fees proportional to how much liquidity was initially contributed.

Essentially, AMMs remove counter-parties and introduce algorithms to set the price, letting you trade X tokens for Y tokens regardless of whether someone is on the other end of the trade.

On several occasions, AMMs are also called Swap Exchanges. This might not hold for all cases, but UniSwap, SushiSwap, PancakeSwap are all AMMs in nature.

As explained in our article on DeFi, Liquidity Pools is a collection of funds locked in a smart contract on a decentralised finance (DeFi) platform where anyone can deposit their crypto assets and receive rewards in exchange for liquidity to the platform.

When working with Liquidity Pools, the volatile nature of crypto comes into play, and there are specific terms that one needs to know to stay ahead of their trade and take precise decisions. Some of them are:

Slippage: Slippage is the difference between the expected and actual cost paid for an order of cryptocurrency. Slippage can be positive and negative as it occurs when the actual price of the order is higher or lower than expected.

Supposedly, the current ask for BTC is $10000, and you are planning to buy BTC worth $50000. This means that when placing the order, you are expecting 5 BTC against the $50000, but between the time you place the order and the broker receives the order, the price of Bitcoin rises. By the time your order goes through, your $50,000 was enough only to purchase 4.7 bitcoin instead of the expected 5. This is a negative spillage, and if the prices fall and you get more BTC against what you paid, it is positive.

Crypto slippage occurs primarily because of wild swings in price that render a trading order executed at a different price than the trader may have expected. Another reason slippage occurs in cryptocurrency is due to a lack of liquidity. Cryptocurrencies that are not traded very often, either because they are new or due to their lack of popularity, have a significant difference between the lowest ask and the highest bid, which can cause dramatic changes in the price as an order is being entered and executed.

While slippage may be inevitable, there are ways to minimise its impact. Luckily, most crypto brokers and exchanges have a slippage tolerance control. This means that one can "set" the level of slippage they are willing to tolerate, and the broker will not fill orders outside this threshold. For reference, a typical level of tolerance is less than 0.10%.

Impermanent Loss: Impermanent loss happens when one provides liquidity to a liquidity pool, and the price of the deposited assets changes compared to when they were deposited. The more significant this change is, the more exposed to impermanent loss. In this case, the loss means less dollar value at the time of withdrawal than at the time of deposit. It is called impermanent loss because the losses only become realised once they withdraw the coins from the liquidity pool.

Market Depths: A market depth, or depth of market, is a measure of supply and demand for liquid assets, such as cryptocurrencies, based on the number of available buys and sell orders. The use of "market depths" significantly improves the protocol's previous version. With different market depths serving as bridges between source and destination tokens, the new algorithm offers a more sophisticated approach than just splitting a swap across different protocols.

Order Book DEXs

Similar to centralised exchanges, order books on DEXs maintain records of all the open orders for purchasing and selling assets for specific pairs of assets. The buy orders imply a trader's interest in purchasing or bidding for an asset at a particular price. On the other hand, sell orders show that the trader is prepared for selling or asking for a specific price for the concerned asset. The discrepancy between the prices is responsible for determining the depth of the order book alongside the asset's market price.

One could discover two distinct order book DEX crypto exchange types: on-chain and off-chain order books. The DEXs that store their open order information on the chain are on-chain order book DEXs. On-chain order book DEXs could help traders leverage their positions by using funds from lenders on their platform.

On the other hand, off-chain order book DEX or decentralised exchange platforms store the order books of the blockchain networks. The off-chain order book DEXs only enable transaction settlement on the blockchain, thereby offering the value of centralised crypto exchanges.

Another critical aspect of an order book decentralised exchange or DEX platform is the risk of liquidity issues. Order book DEXs compete with centralised exchanges and impose additional fees for on-chain transactions. On the other hand, off-chain order book DEXs can reduce the costs, albeit with smart contract-related risks.

Although the concept of the order book is long-running, implementing the mechanism for DEX is a recent innovation that is still being tested. The advantage comes with the functionality of - 'Pending Order'. It allows users to give play to their observations and take preemptive measures to pend orders at a designated price. At the same time, the fixed price also means that the common problems of slippage and front-running characterised by AMM will be significantly alleviated.

DEX Aggregators

Decentralised exchange aggregators are also emerging as one of the top additions in a decentralised exchange list for obvious reasons. They are trading protocols that work by sourcing and routing liquidity throughout multiple DEXs according to specified requirements.

The idea behind such aggregators is that to receive the best and most efficient price for a token swap, one must check for the best price across all the DEXs. Manually checking is inefficient and does not enable complex trading routes and paths. Thus, sophisticated DEX aggregator algorithms are vital for saving money on swaps.

Major Decentralised Exchanges

Uniswap: One of the most widely used automated market maker platforms is Uniswap. Built on Ethereum, the Uniswap decentralised exchange (DEX) has catalysed the AMM space attracting colossal amounts of liquidity. Also, many consider Uniswap to be the flagship Ethereum-based AMM. Since launching, numerous clones and forks of the Uniswap protocol have emerged. The protocol uses open-source code, which makes copying and cloning relatively simple.

SushiSwap: SushiSwap was initially a fork of Uniswap. The SushiSwap team launched what is known as a "vampire attack", whereby a protocol attempts to steal LPs from a competitor by offering better rates and rewards. SushiSwap managed to lure Uniswap LPs to the new SushiSwap protocol by offering SUSHI token rewards on top of attractive trading fees.

Balancer: The Balancer AMM uses a Constant Mean Market Maker (CMMM) model, enabling liquidity pools to hold up to eight assets. There are three types of Balancer liquidity pools. Firstly, Private Pools require only a sole LP to operate.

Secondly, Shared Pools allow anybody to provide liquidity and use the Balancer Pool Token (BPT) to track the ownership of the pool. Then, there are Smart Pools. Smart Pools also use the BPT token and can accept liquidity from any LP. However, Smart Pools can readjust the weighting and balances of assets, as well as trading fees.

Serum: Serum, at its core, is a fully on-chain order book built on Solana. The protocol's first-of-its-kind central limit order book (CLOB) is the technology that enables users to trade with each other in an efficient, trustless, and non-custodial way. The protocol is also asset-agnostic, which means any crypto-assets (spot, derivatives, synthetics, and so on) can be traded on the order book. An upcoming upgrade called Serum Core will make the order book capable of order-matching any financial asset, not just SPL (Solana Protocol's ERC-20 equivalent) tokens.

Founded by SBF, Serum is related to Alameda Research and FTX and supported by Solana Foundation.

1inch: The leading DEX Aggregator is 1inch. It features a similar UI to the popular Uniswap and PancakeSwap and automatically routes swaps via the optimal route. 1inch claims to offer users access to over 50 liquidity sources on Ethereum, 20 on Binance Smart Chain, and eight on Polygon. The list of DEXs it draws on includes the likes of Uniswap, 0x and Balancer, as well as 1inch's own liquidity protocol, formerly known as Mooniswap.

Sergej Kunz and Anton Bukov founded 1inch in 2019 during ETHNewYork's hackathon. As of June 2021, 1inch's exchange trades about $250 million a day. 1inch also has its own governance token, and the primary way to earn 1INCH tokens is by providing liquidity to its liquidity platform.

As said earlier, most of the innovation kickstarted with Ethereum, and that is the base protocol for a lot of these products, but with every passing day, innovation and the thriving community is taking a multi-chain approach, i.e., DEXs that have done well on one protocol are also being built on other protocols. A prime example of this is UniSwap being built on Polygon(previously, Matic), an L2 Ethereum scaling protocol.

Even centralised exchanges like Binance have a DEX deployed on an L1 layer developed by the Binance Smart Chain team.

Why DEXs Haven't Scaled

Education: The biggest problem for DEXs is that users are not aware of the benefits and use cases of decentralised exchanges. Also, even if users are aware, many of them are not very comfortable dealing with private key wallets and thus avoid using DEXs.

User Experience: DEXs are not user-friendly enough for their UI/UX as they are generally optimised for the technical aspect of things. There is no customer support and handholding, which makes it very difficult for newcomers on the platform to get the hang of it. Also, the lack of doing transactions via fiat currency is a bummer. While it is to note that this is not the reason behind this is backed by the core fundamentals of enabling liquidity pools, it just makes it difficult to convince people to carry out transactions.

Economics: Since transactions are happening on-chain and keeping exchanges based on Ethereum in mind, they take more time, but they are also expensive due to gas fees. Also, there is this imminent problem of not having enough liquidity pools. This is a classic chicken and egg problem as traders do not join because traders are not already on the platform to match their orders; getting liquidity through a significant adoption by the ecosystem is a long process.

Though most decentralised exchanges can be classified as either an AMM or order book-based platform, an increasing number of platforms are beginning to blur the lines between the two or offer something else entirely.

With regulations coming around, more mechanisms would come into existence, but it would not be an overstatement to say that exchanges are the way to onboard millions and let them into the world of crypto, where broader concepts await further exploration.

Stay informed in just 5 minutes

Get a daily email that makes reading crypto news informative. Have fun keeping up and getting smarter.

The dispatch is sent in time zones at 8:30 am. Choose your preferenceEastern Time Zone (UTC-05:00)USTISTGMTSST

Subscribe