Aave’s Extraction

What it costs, who collects it, and why users will still accept the deal

The most expensive thing you can put in front of a person is a decision. Fees are cheap compared to that. People pay for convenience and ease, that’s it.

That’s how the platforms extracted, taking the decision away. Couch lock – one of my favourite words from Tim Wu’s Age of Extraction.

Can’t pick stock, sure, index funds, S&P…

Not sure about lending. Call it a savings account, be proud.

They all just charge you for removal. Removal of decision-making, also sometimes the removal of the best benefits. People didn’t care.

What DeFi did was add. Which chain, which pool, what rate, when to move, where’s the bridge, is this even the real app or made with Claude Fable before July 12? Aave has 2.5 million users and six years of history. Revolut has 65 million users. Is it fair if we say Aave has to be the smarter one here?

Between January and July, the rate on Aave’s USDC pool wandered between roughly 2% and 9%.

Bouncing around is normal in DeFi. You watch the rate go up and down, and you move your money whenever it makes sense.

But that structure is unsellable everywhere else. Neobanks can’t explain to a user that the rate is set by borrowing demand and could collapse to 2% when it clearly advertises a savings account. People don’t put money in chaos. That is why people never start using crypto apps, let alone crypto savings apps, every day.

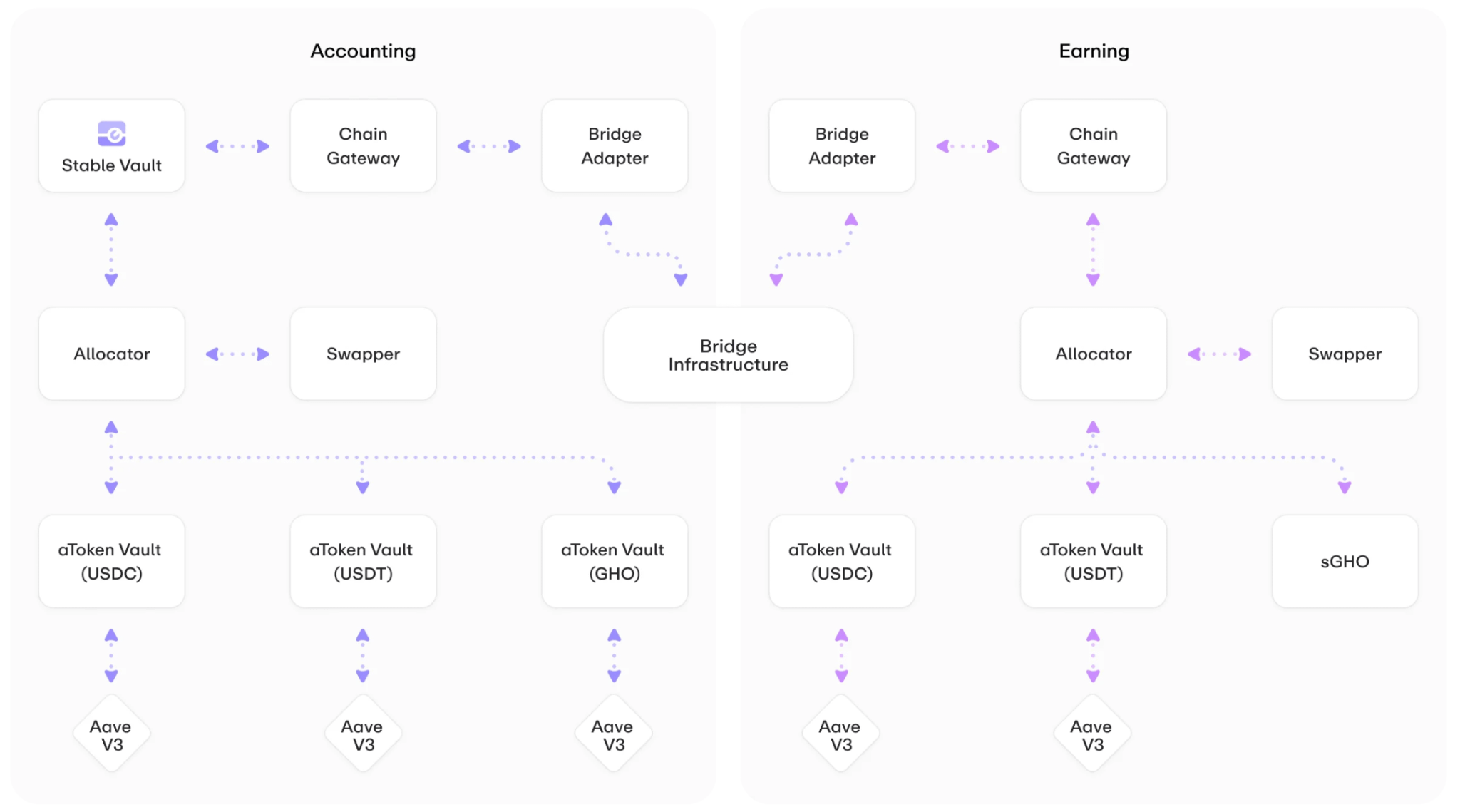

On July 9, Aave Labs found a workaround called Stable Vault. Today, I want to show you how it works, who is making money off it, and why I think regular people are going to use it anyway.

Stable Vaults lets any business plug in once and start offering a savings account. A neobank, a wallet, a payroll processor. Deposits route into Aave’s lending markets. The user sees the rate in the app they use every day; if it seems like a good deal, they’re in.

The rate is fixed. I know it’s a tough thing to say in crypto.

Aave’s market pays whatever borrowers are paying that week. Stable Vaults sits on top and hands the operator a dial. The app types in a number. 4 per cent, say. From then on, the vault pays four per cent per second, no matter what Aave is doing underneath. That is the app’s problem, not yours. Anything the strategy earns above that number goes to the operator.

POV: the person putting money in

They get rated insurance. When Aave’s USDC pool paid 2% this spring, a vault promising 4% still paid 4%, and the operator covered the difference.

Handing off risk has a price everywhere else, and it has one here. Look at a fixed-rate mortgage. It costs 50 to 100 basis points more than a floating one, and that premium is the borrower paying for a fixed number.

The person doesn’t have to create a wallet, keep the seed phrase, bridge, or choose a chain. They get a support line, account recovery, Face ID, and a company with an address if something breaks. Aave’s own app runs SOC 2 certification and 2FA and markets both, because those are what the customer is buying.

The top of the range is what the user loses. When the pool paid 9%, they got 4%. When it paid 6%, they got 4%. It’s a fixed rate fixed by the app, based on what tier the user is. A moving rate is a live measurement you can actively check; an unmoving rate completely hides the middleman’s cut.

The user also picked up a second counterparty. By using this setup, they add two new failure modes to their balance sheet. The financial health of the fintech company running the app, and the code quality of a hidden, private script that shuffles their capital around behind the scenes. In plain DeFi, your only risk is the core protocol code. Here, if the middleman company goes bankrupt, or if their private backend script crashes and misplaces the funds, their money is just as gone, even if Aave itself works perfectly.

In a real swap market, the fixed rate is driven down to something close to fair value because both sides can shop. Here, the operator sets the number alone, and the customer has nothing to compare it against. User isn’t comparing 4% to Aave’s 6%. They are comparing it to their bank. Aave’s app page puts its own rate next to the FDIC national savings average of 0.40%, and against that, anything looks generous.

POV: The Operator

Take a neobank with $200 million of idle user stablecoins. It already has the money and users. It paid to acquire them. It wires in one integration, advertises 4%, and if the strategy returns 6%, it books $4 million a year on a balance sheet item that was previously a cost. Low effort 2%, not bad.

Rise is a payroll company. It pays contractors across 190 countries and has processed over $1.5 billion. When a company pre-funds payroll a week early, that USDC used to sit dead, so Rise built Rise Earn to park it in Aave’s USDC pool on Arbitrum until payday.

Rise takes 1% of the interest earned and nothing else. On a 6% yield, that’s six basis points. The worker gets 5.94%, and they just see Aave’s live rate.

A Stable Vault operator on the same money takes 200. The middleman’s cut went up thirty-three times.

POV: Aave and Stable Vault

Aave sells the vault’s ability to set per-user rates for loyalty, campaigns, or tiers, so think that a premium subscriber gets 5% and everyone else gets 3.5% from the same pool of borrower interest. A fintech issuing its own stablecoin can register it as a deposit asset and run a closed loop. And a balance that earns doesn’t leave, which means the yield is also a retention line.

Is the operator getting this for free? No. It’s short the spread in both directions. When Aave paid 2% this spring, every vault promising more than that had to write a cheque.

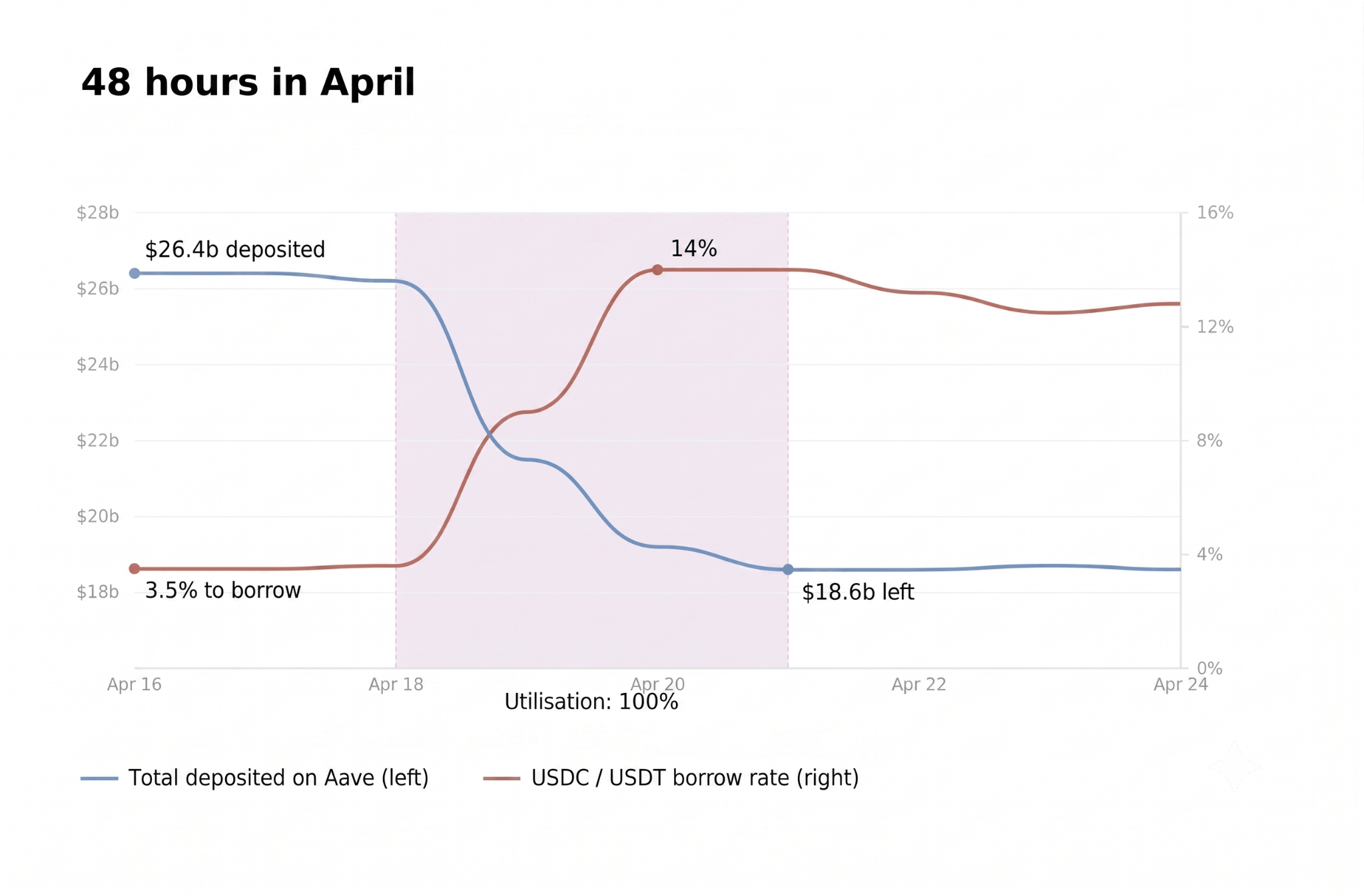

Which brings us to April 18, when the Kelp DAO bridge exploit on April 18 triggered a massive run on Aave, pool utilisation hit 100%, completely freezing all withdrawals and trapping both the operator’s paper profits and the user’s money in the same locked queue.

When utilisation hits the ceiling, nothing comes out for anyone, including the vault. The surplus stacks up on paper next to the user’s principal.

If liquidity returns, the operator sweeps a surplus that piled up during the days the user couldn’t leave. That surplus is the fee the market was paying for illiquidity. The person supplying the illiquidity was the user. If liquidity doesn’t return and bad debt hits the pool, the vault is short, and Aave’s docs say an authorised party can top up the system. No reserve behind “can”.

Aave will say its contracts were never exploited, that Kelp’s bridge failed and not Aave’s code, and that rsETH was frozen within hours. All true. They had previously voted to accept the risky collateral at a dangerous 93% loan-to-value ratio right before their risk manager resigned, leaving everyday users to bear the brunt of a broken app.

Now Stable Vaults look like the last piece?

Rise runs payroll floats through Aave. Kraken white-labelled Aave v3 into a protocol called Tydro on its own L2, then pointed its retail Earn product at it, so a Kraken customer tapping earn is an Aave user too. Cap Finance parks stablecoin reserves in it.

Horizon lends against tokenised treasuries with Circle and Franklin Templeton in the room. Aave App goes straight at consumers. Stable Vaults lets everyone else in and calls it diversification.

Aave doesn’t need more deposits. Kulechov told The Block in March that there’s a liquidity surplus in DeFi and that the focus has to shift to the borrowing side. He’s right, and it’s why USDC has been paying 2-3% instead of 8%. What Aave has always faced is that DeFi capital is mercenary and leaves for fifty basis points. Routing them through an app that owns the relationship, like the payroll, turns the flightiest money in finance into something that acts like a deposit base.

Aavenomics 3.0 went live on June 27 and now automatically buys AAVE from revenue. Revenue needs to flow through the pipe whether or not anyone is bullish. In a bear market, sticky deposits are what keep the buyback running. How do you get them? Stable Vaults.

Coinbase pays around 4% on USDC balances. Robinhood opened Earn on July 1 at roughly 7%, with 28 million funded accounts. Both call it savings.

Coinbase runs on Morpho and Ethena. Robinhood runs on Morpho and Maple, with the risk parameters set by a firm called Steakhouse.

Both of them had to build that. Custody deals, curators, risk teams, months of lawyers. Aave’s contribution is to make all of it unnecessary. With one integration, any app on earth can put a number on a screen and keep the distance between that number and whatever borrowers happen to be paying.

A bank gets to use it because a century of law stands behind it. Reserve requirements, examinations, deposit insurance, and a regulator who can walk through the door unannounced. All of that was built because everyone agreed long ago that the bank lends your money out and somebody has to be standing there when the lending goes wrong.

Everything Stable Vaults delivers is available to anyone with 20-30 minutes. But you make a wallet, bridge some USDC. Then supply it to Aave. What you don’t have to face in this case is KYC, an operator, or a rebalancer. And you lose nothing to spread. You get 6% instead of 4%, and you can see the pool the whole time.

I understand that the system thinks much longer term than my logic does. Also, when people don’t do that, I don’t think they are stupid.

Iyengar and Huberman’s work on retirement plans found that as the number of fund options went up, the number of people who enrolled went down. Faced with more choice, people picked nothing. Every consumer finance product since has been built on that result.

Self-custody has been right for fifteen years, and everyone has been told. Most on-chain card spending still routes through custodial platforms anyway. It’s a preference, expressed repeatedly, at scale. And their safety maths is better than ours. For someone with $2,000 and no crypto background, the likeliest way to lose it is by losing a seed phrase or sending it to the wrong address. An app with Face ID and account recovery removes the failure mode that would have got them. They’re paying 200 basis points for insurance against themselves, and that’s a rational purchase.

So Aave did the right move. It’s what a business with liquidity and no loyalty is supposed to do, and every consumer app in crypto is racing to the same place because the same logic is sitting everywhere we go.

In the end, this is an acceptance of human nature. People want safety, predictability, and most importantly, ease. Building a life is hard enough without having to run a personal central bank. They just want to close the app, look at a number that sits perfectly still.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.