Hello,

In 1719, John Law, a Scottish gambler and monetary theorist, convinced the French Regent to allow him to build a system that wrapped illiquid colonial assets into liquid paper instruments. He created the Mississippi Company, which held a monopoly on trade with French Louisiana, a vast territory mostly composed of swampland.

Law wrapped these illiquid colonial claims into company shares redeemable for gold. Ordinary Parisians piled in. A year later, the scheme turned him into the richest man in Europe and the Controller General of Finances. Albeit temporarily.

What happens when you hold stocks redeemable for gold? You wait for a high and then demand the gold. Investors did just that. The redemptions started, and they wanted their gold back. However, there was not enough gold. Law responded by changing the rules. He capped the amount of gold anyone could hold. He devalued the notes by decree and mandated that shares could be sold only through his bank at prices he set. Each intervention bought him a few more weeks, but it destroyed trust. By 1720, the investors’ claim papers became worthless. Law fled France after leading France to the Mississippi Bubble.

Three centuries later, the largest private credit funds in the world are responding similarly to a surge in redemption claims from investors. They are changing the rules of redemption to manage the damage. But is this the solution, or just a band-aid fix? Can on-chain private credit help? In today’s deep dive, I will explore that question. Let’s get started.

From Inception to Redemption

Private credit refers to lending that occurs outside of banks and public markets. A company borrows directly from a specialised fund run by firms such as Blackstone, Apollo, or Blue Owl, rather than from a bank or by issuing bonds. The borrowers are typically mid-sized businesses that can’t yet afford to go public.

This market barely existed two decades ago. Today, it’s over $3 trillion and is expected to touch $5 trillion by 2029. The industry filled the gap created by the 2008 financial crisis, which had made it costly for banks to hold risky loans due to regulations and capital requirements.

Private credit lured investors with higher returns (8-10%) compared to public markets, in exchange for illiquidity. The investor’s money was locked up for years. That was the whole point of the proposition. It offered companies greater flexibility and ease in managing their business than a traditional loan secured through syndicate banking. In return, investors received an illiquidity premium for not being able to access their money for an extended period.

Then, the industry decided to change the rules. They wanted to attract retail investors, either to offer them more attractive returns or to grow the private credit market. In response, the US Congress created business development companies, or BDCs, in 1980 under the Investment Company Act. BDCs remained a niche product for decades, but they gained popularity when firms like Ares, Blackstone and Blue Owl launched non-traded versions specifically designed to tap into retail and high-net-worth capital. These vehicles wrapped illiquid corporate loans, but with quarterly redemption windows to appease retail investors.

Retail investors bought into the deal but overlooked a major structural loophole: the private credit industry promised them liquidity while the underlying loans remained illiquid. If the lending cycle got frothy and retailers flocked to redeem, it would leave the private credit funds issuing these retail wrappers in soup. So they set a 5% cap on redemptions. This seemed to solve the problem for the fund managers. But what happens if the market crumbles, forcing redemption demands to exceed the 5% limit? The inevitable happened at last.

In September 2025, two major collapses shattered retail confidence in private credit.

First, Brands Group, an auto parts supplier, filed for bankruptcy after loan agreements failed to detect and disclose hidden off-balance sheet liabilities. Lenders underwrote the deal, presuming it was a 5x debt-leveraged buyout, while in reality it was closer to 20x. In the case of Tricolor Holdings, a subprime auto lender, the company allegedly pledged the same collateral for multiple loans. When the reality came to light, the demand for redemptions surged.

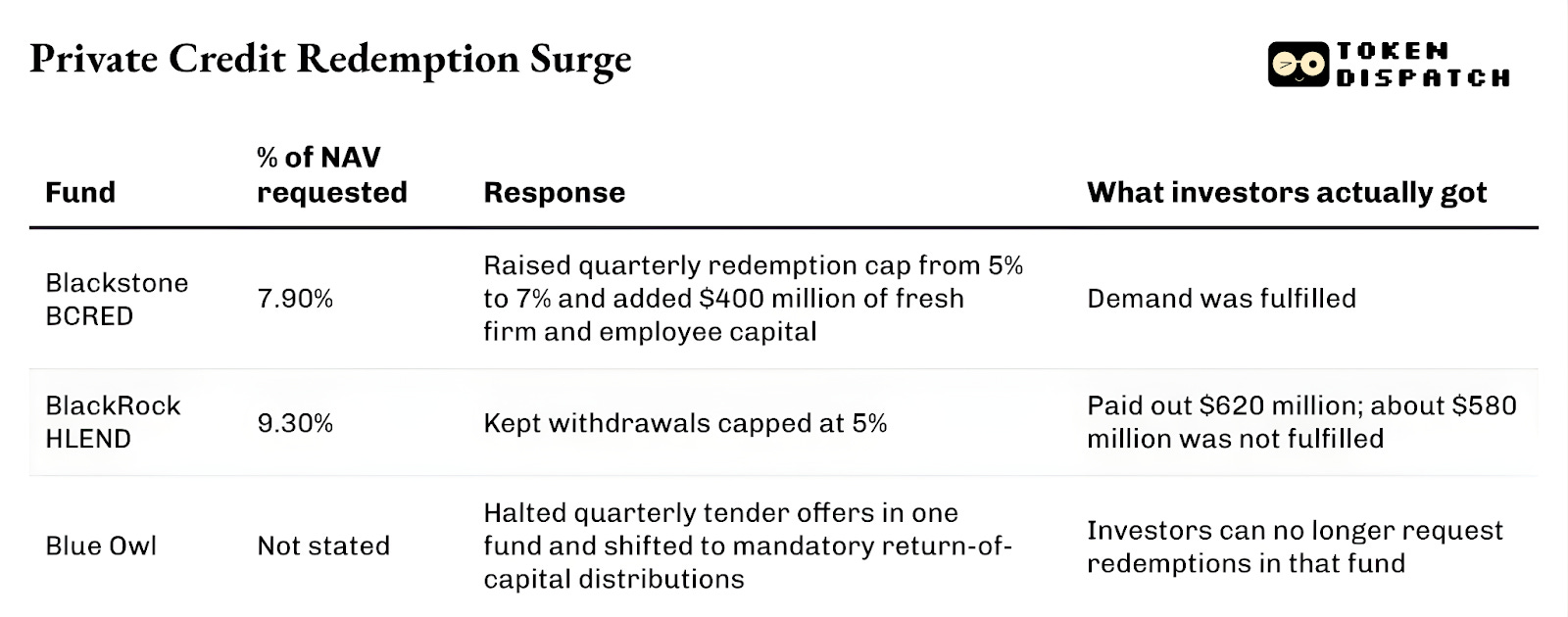

This has led top private credit fund managers to resort to discretionary rule changes or gatekeeping redemptions.

Each of these responses had something John Lawesque about them. Some gatekept redemptions, while others changed the rules when crisis struck.

What concerns me about all of this is that gatekeeping and discretionary rule changes cut both ways. On the investor side, it sends a message that the terms they agreed to are negotiable, and only in one direction. Investors are left at the mercy of fund managers who can tighten redemption limits, or worse, halt them altogether and restructure payouts. What’s also unfair is that these changes are made only after capital has been committed. This undermines the spirit of any contract signed between two parties.

On the fund manager side, they begin playing conservatively. A fund under constant pressure to redeem will not deploy capital confidently. Instead, it starts preserving cash instead of lending it.

Is On-Chain Private Credit a Fix?

There could be a lot of things that people might boast about on-chain private credit. They will show the numbers on tokenisation dashboards and the total value locked in private credit protocols. But most of these are just wrappers for the existing traditional private credit industry. Why do I say this? Here are the facts:

At its core, on-chain private credit’s unique selling point (USP) is its ability to run a smart contract across any financial primitive. This contract can set withdrawal limits, collateral ratios, and distribution rules within the code. While an on-chain private credit fund cannot promise more liquidity than a traditional one, it can ensure that no fund manager can unilaterally alter the terms of the contract once capital is committed. No board vote can upsize a tender offer or switch from quarterly redemptions to return-of-capital distributions, as Blue Owl did.

The code continues to run as is, regardless of the manager’s wishes or market conditions.

A smart contract-powered private credit fund can also address the issue of double-pledging. Tricolor’s collapse involved pledging the same collateral for multiple loans. Tokenised collateral creates a single, auditable record with a single set of tokens for a single set of claims. This makes it structurally harder to double-pledge.

First Brands was marked at par by private credit funds just months before bankruptcy. On-chain, every transaction and repayment is visible in real time. No self-reported valuations can misdirect investors here. Assets cannot be marked at 100 cents if the on-chain market values them at 60.

And if on-chain credit tokens trade on secondary markets, you get better price discovery. It solves the pricing mismatch between the NAV of non-traded BDCs and the underlying loans. We saw this in how hedge funds Saba Capital and Cox Capital tendered an offer to buy Blue Owl shares at a 20-35% discount to NAV.

Protocols are already building this infrastructure. Maple Finance runs institutional credit pools with $3 billion in assets under management. Apollo has launched a tokenised feeder fund with Securitize. WisdomTree brought on-chain NAV data for its private credit fund through Chainlink oracles. The infrastructure is in place.

However, there’s something none of this infrastructure can solve. It cannot evaluate whether a borrower will repay or if a mid-market software company will survive AI disruption.

The underwriting problem that comes with failure of human judgment, as seen in First Brands and Tricolor, can be minimised with on-chain records, but not eliminated altogether. But the other, bigger problem is that most business aspects, including maintaining financial statements and records of supplier contracts, assets and liabilities, exist entirely off-chain. A smart contract cannot inspect borrowers’ books or verify their financial statements. Even if there were a protocol that wanted to bring that data on-chain for verification, businesses wouldn’t agree to exposing their financial and other sensitive business details on a public blockchain. This makes full on-chain underwriting a non-starter with current infrastructure.

Blockchain currently offers a different set of trade-offs. But private credit failing through DeFi can be worse than the traditional private credit industry failing.

Imagine there’s a fund with deteriorating assets and rising withdrawals. For this fund, a DeFi ecosystem hungry for high yield from real-world assets is a perfect target. There’s a high incentive for investors seeking redemptions and fund managers seeking fresh capital to tokenise these loans and sell them into on-chain pools. DeFi can quickly become a dumping ground for illiquid and distressed products from the traditional market.

We saw this happen with Goldfinch, a pioneer in on-chain lending, when a borrower made an unauthorised intercompany transfer that was large enough to threaten the business as a whole. Tokenisation could only expose the aftermath, but couldn’t prevent the fraud.

There is a counterargument to this. On-chain secondary markets can also bring liquidity to distressed assets and help in better pricing. But what separates a market function from becoming an exit liquidity venue is a thin line that could easily collapse.

As long as critical information, such as borrower quality, covenant strength, and financial reporting, remains off-chain, on-chain credit will not solve the problems of the traditional industry. It will only bring a new set of problems.

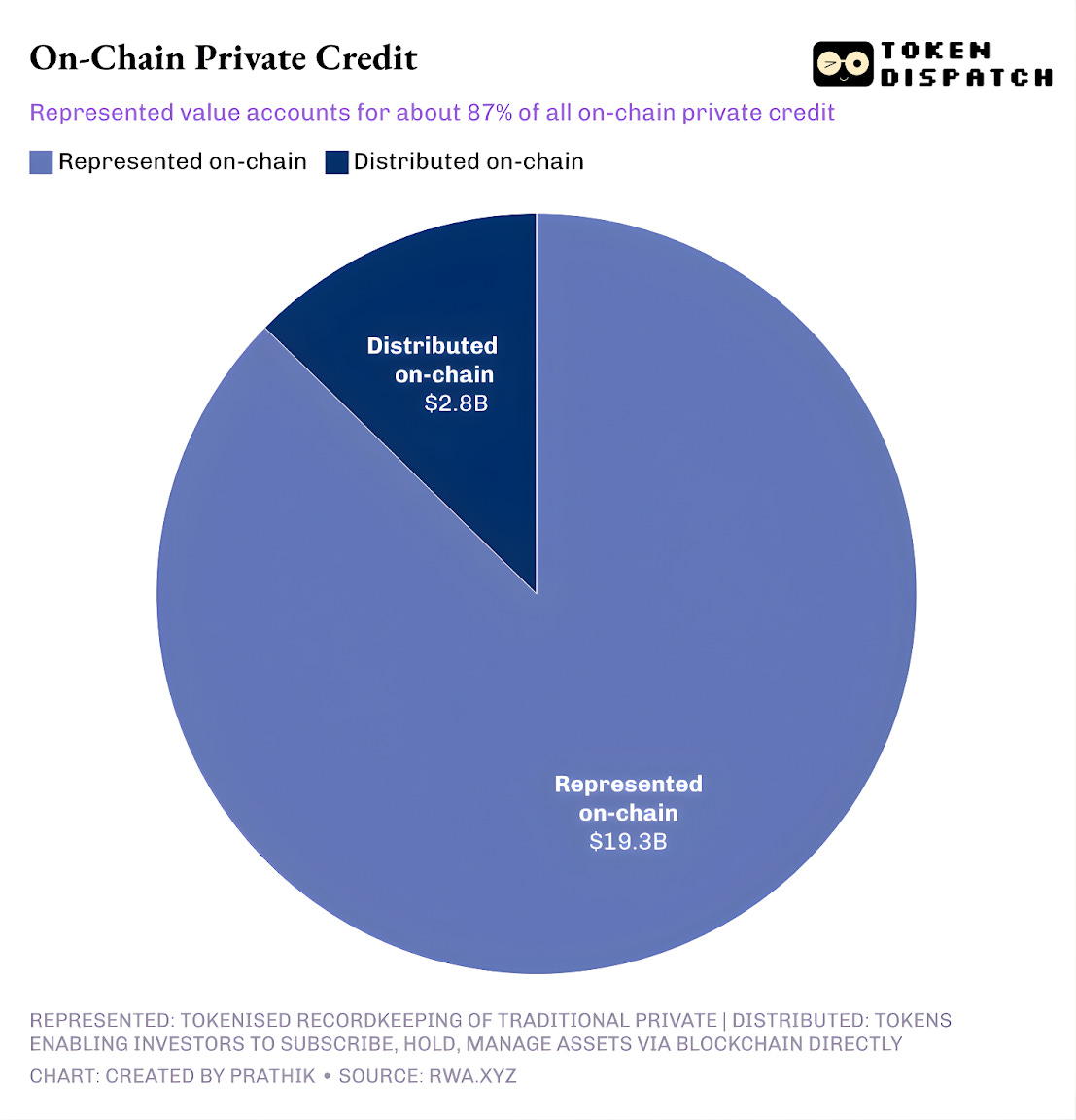

If major on-chain protocols channel hundreds of millions in DeFi deposits into loans that default or have weak underlying assets, then the damage will spill across multiple protocols. On-chain private lending is still nascent. Total active blockchain-native loans across protocols is barely $3 billion, as against the $3-trillion traditional private credit industry. A high-profile default could set back the entire real-world-asset thesis by years.

If on-chain private credit wants to be more than just a shinier wrapper for the traditional private credit industry, it needs to solve for trust before it solves for yield. This includes third-party verification of underlying collateral, instead of relying on a self-reported one by the originator. It could include standardised risk disclosures that translate duration and credit risk into terms that DeFi participants can understand and take cognisance of.

It should even include credit ratings from traditional agencies for on-chain instruments, something Maple Finance CEO Sidney Powell expects to happen by the end of 2026. It should even include frameworks that can detect and block originators from dumping their distressed assets into on-chain pools. Without these measures, the convergence of traditional and decentralised finance risks will become extractive and not additive.

That’s it for today. I will be back with another deep dive.

Until then, stay curious!

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.