There is a category of companies that profit when the world gets worse. Defence contractors. Oil majors. Gold miners. These are the obvious ones, the companies whose business models assumes instability and prices it in.

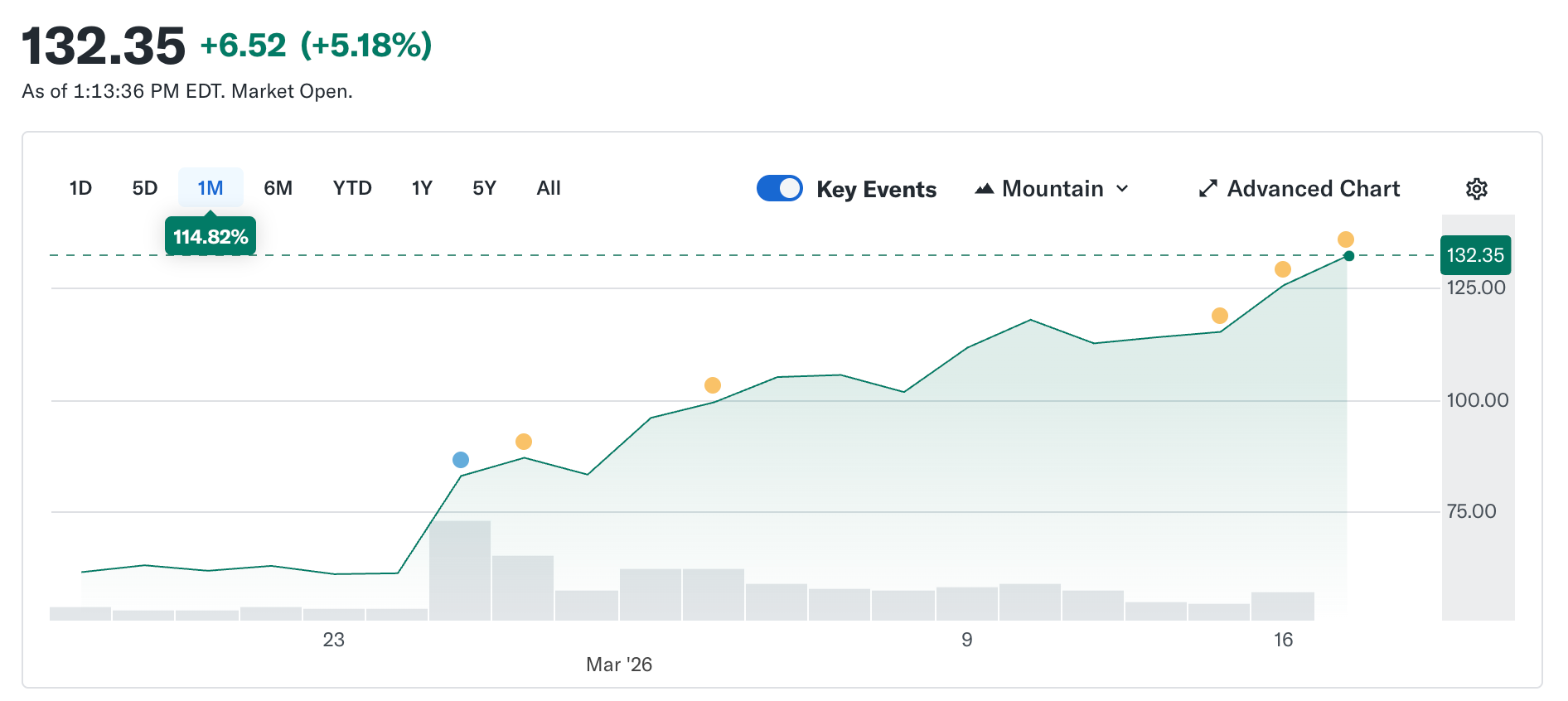

Circle is not supposed to be in that category. Its token worth exactly one dollar, always, by design. Stability is the entire product. And yet Circle’s stock has gone from $49.90 on February 5 to roughly $123 today, more than doubling in five weeks. Meanwhile, the broader crypto market remains 44% below its peak in October.

A company whose product is designed for price stability became the hottest trade in the market because the world got more unstable.

I want to explain how that works, why it’s more interesting than it looks, and what it tells us about what Circle actually is versus what the market is currently paying for.

What circle is (of course, we are going back to that)

Strip away the branding, the payments narrative, and the infrastructure pitch, and you’re left with this: Circle holds U.S. Treasury bonds. Every dollar of USDC in circulation is backed by a dollar parked in short-term government debt. The interest on that debt goes to Circle. That’s roughly 90% of the company’s revenue in any given quarter. The business model is not complicated once you see it: Circle is a money market fund that issues a stablecoin.

The implication is that Circle’s revenue has one input that matters, which is the federal funds rate. When rates are high, Treasuries yield more, and Circle earns more for every USDC in circulation. When rates fall, the revenue compresses. Everything else is commentary.

So here is the chain of events that produced a 150% rally from the February low.

The Iran conflict pushed oil prices up by roughly 35% since February 28. Oil prices above $100 means inflation concerns, and inflation concerns mean the Fed can’t cut without looking reckless. The March 18 hold was never really in question. CME FedWatch was already showing 90%+ probability of no change long before the war began. What the war actually moved was the full-year picture. Before the conflict, markets priced in two 25 basis point cuts in 2026. Afterwards, that number dropped to one, pushed out past September at the earliest. The probability of no cuts at all in 2026 roughly doubled. With rates staying higher for longer, Circle’s Treasury reserves kept yielding. More yield means more revenue. More revenue means a higher stock price. War broke out, and a stablecoin issuer was the beneficiary. That sentence was not in anyone’s model.

For context, the bear case that had Circle’s stock at $49 in February was essentially a bet on rate cuts. The market was pricing in multiple Fed cuts through 2026, which would have directly compressed Circle’s reserve income. As a rough estimate: at current USDC supply levels of $79B, each 25 basis point cut costs Circle somewhere in the range of $40-$60 million in annualised revenue. Two cuts wipes close to $100 million from the top line before year end. The war made that calculation disappear overnight. Not because Circle changed, but because the macro backdrop that was supposed to undermine the thesis stopped being the macro backdrop.

How the squeeze started

While the rate story kept the stock elevated, the initial explosion came from positioning.

Going into Q4 earnings on February 25, about 17.8% of Circle’s shares outstanding were sold short. Hedge funds had built serious bearish exposure. The thesis was that rates will eventually fall, reserve income will compress, the business has no revenue floor that isn’t rate-dependent. Hard to argue with on the fundamentals. Then Circle reported earnings of $0.43 per share against a consensus of $0.16. Revenue came in at $770M versus $749 million expected. On-chain USDC transaction volume hit nearly $12 trillion in the quarter, up 247% year over year. Shorts covered. The stock jumped 35% in a single session. According to 10x Research, hedge funds lost an estimated $500 million in a single day on their short positions. The war then picked up what the earnings started.

The coinbase problem

Here is the part that doesn’t make it into the rally narrative.

Circle’s net income for 2025 was a $70 million loss. Not a profit. The Q4 quarter was excellent. The year was not. To understand why, you need to understand the Coinbase arrangement, which is the most important and most underappreciated fact about Circle’s business.

When USDC was originally launched in 2018, Circle and Coinbase formed a joint consortium to govern it. The consortium dissolved in 2023, with Circle taking full control over USDC issuance. However, Coinbase kept a revenue share.

Coinbase takes 100% of the reserve income from USDC held on its platform and splits everything else 50/50 with Circle. In 2024, that arrangement sent $908 million of Circle’s $1.01 billion in total distribution costs straight to Coinbase. Roughly 54 cents of every dollar Circle earned went to a company that doesn’t issue the token and doesn’t touch the reserves. By early 2025, Coinbase held 22% of the total USDC supply, up from 5% in 2022. The more USDC grows on Coinbase’s platform, the more Circle pays out.

The arrangement auto-renews on a three-year cycle, and Circle cannot exit it unilaterally. Whatever comes out of the next renegotiation will directly impact Circle’s margin. In Q4 2025, distribution costs alone were $461 million, up 52% increase year over year. The $70 million net loss for the full year was partly due to $424 million in one-time stock-based compensation from IPO vesting, which made the headline number worse than the underlying business. But the underlying business still faces a structural cost issue that no rate environment fully resolves.

The market is pricing Circle as infrastructure. The P&L says it’s a rates trade with expensive distribution costs. Both perspectives can be true simultaneously. They just price differently, and right now the market is paying for the best version of both at once.

What makes this more than a macro trade

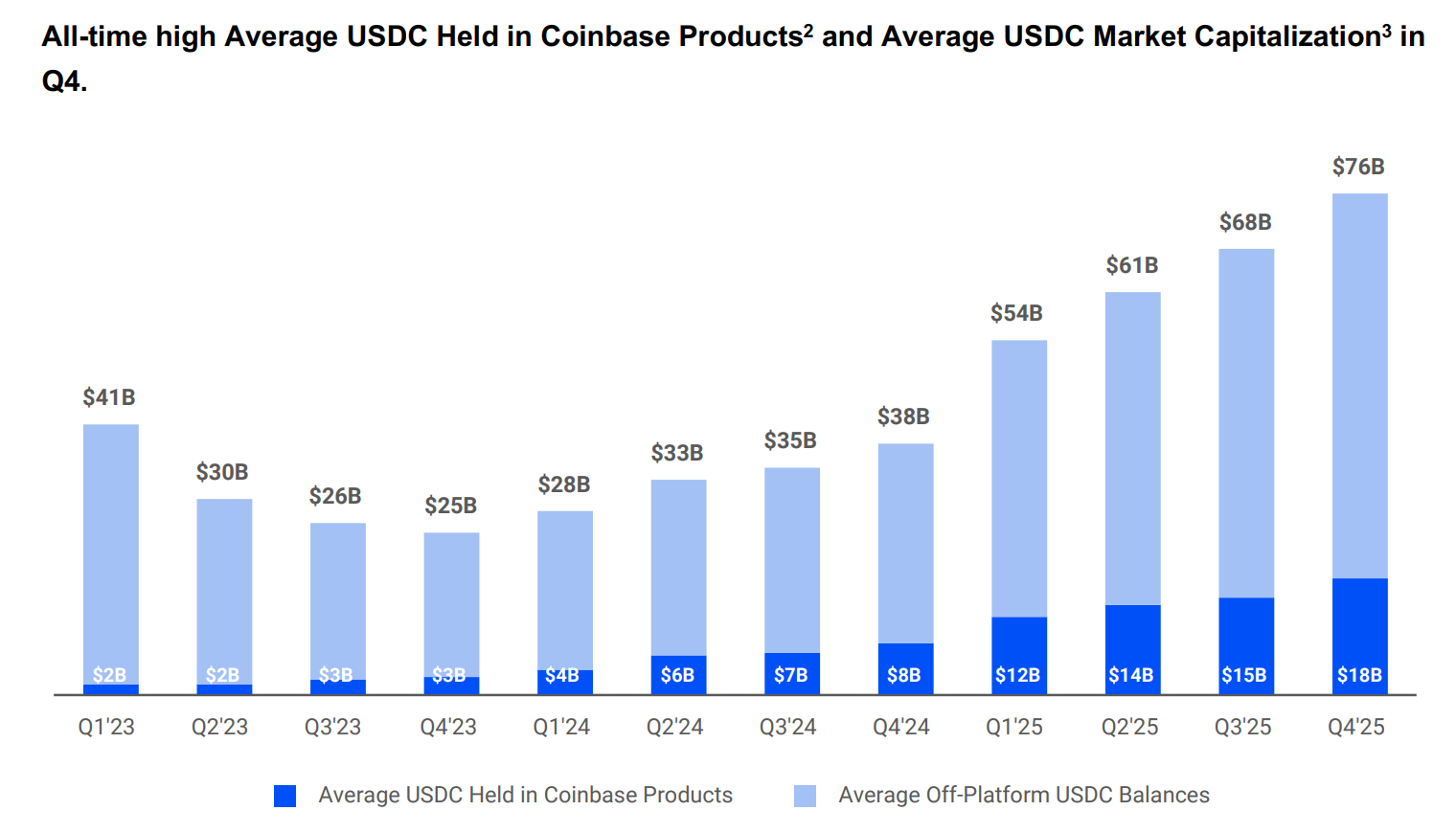

USDC supply recently hit $79 billion, a new all-time high, while the broader crypto market is down 44% from its October peak. That divergence is worth pausing on. Speculative assets go down when markets go down. USDC kept growing because people were using it to move money, not hold it as a bet. During the Iran conflict, demand for USDC in the Middle East spiked specifically because traditional banking became unreliable. People used it for remittances and cross-border transfers when the normal rails were disrupted. That’s what payment infrastructure does under stress. It gets used more, not less.

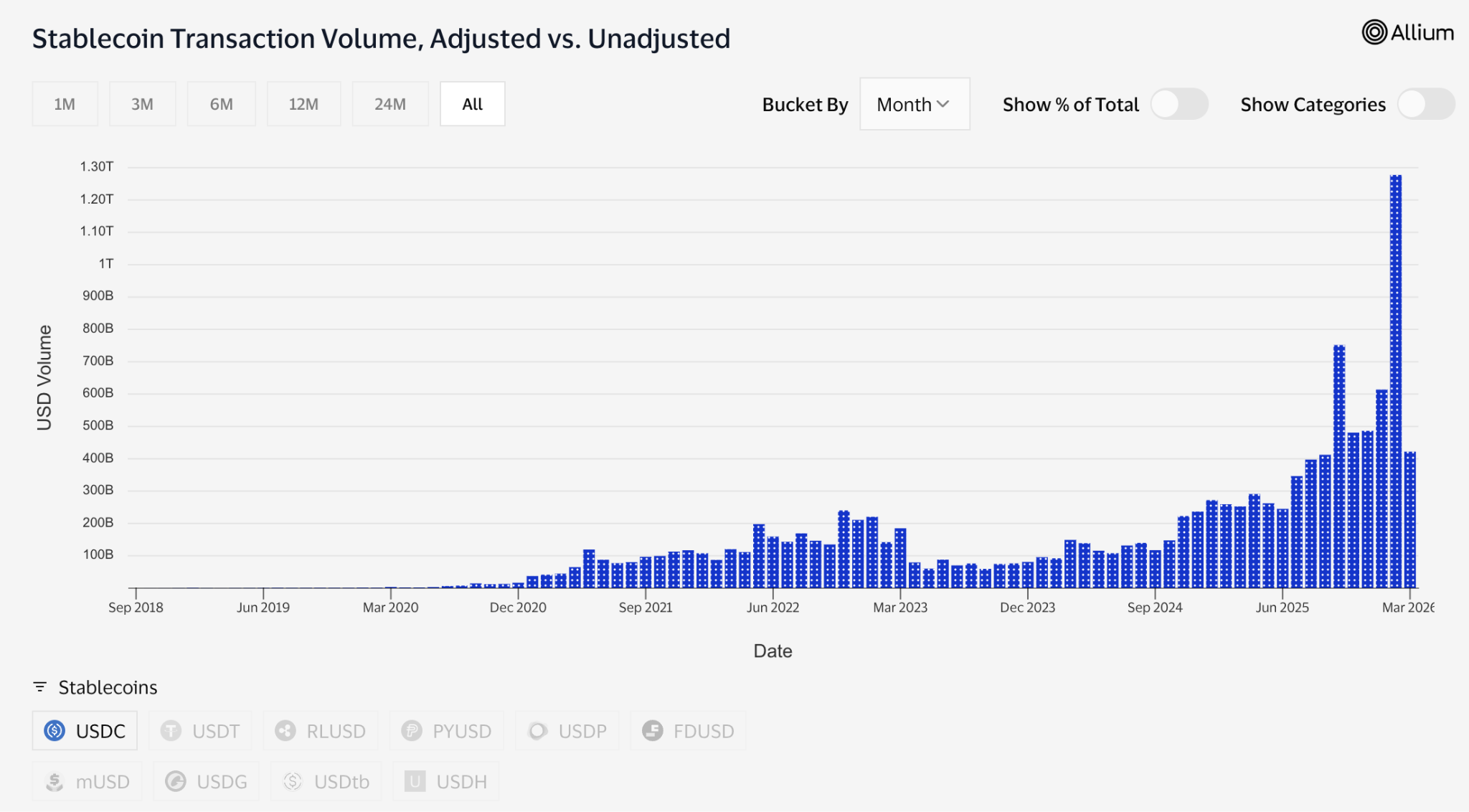

The transaction data backs this up. In February alone, USDC processed roughly $1.26 trillion in adjusted transfer volume, against USDT’s $514 billion for the same period. Tether still holds a $184 billion market cap against USDC’s $79 billion. By total supply, it isn’t close. But USDC is now moving more money than USDT.

Dormant supply and active settlement are distinct concepts. One indicates where people park their dollars. The other shows which dollar people use when they need to move value.

Druckenmiller said something relevant this week. In a Morgan Stanley interview recorded January 30 and released Thursday, he said he assumes global payment systems will run on stablecoins within 10 to 15 years, then said crypto is “a solution looking for a problem.” The most credible macro investor alive just split the space cleanly in two. Stablecoins are inevitable infrastructure, everything else is still searching for a reason to exist. That framing is the intellectual permission structure for the bull case.

The infrastructure bet

Tokenised assets have grown from about $1.5 billion in early 2023 to roughly $26.5 billion today. Many of these products, including BlackRock’s tokenised Treasury fund, BUIDL, which now holds over $2 billion in assets, rely on USDC for processing subscriptions, redemptions, and settlements. Prediction markets processed more than $22 billion in trading volume in 2025, largely settled in USDC. Polymarket alone. Visa now supports over 130 stablecoin-linked cards across 50 countries, processing roughly $4.6 billion in annualised settlement volume.

Circle is also building the infrastructure beneath all of this. The Circle Payments Network connects 55 financial institutions and is running at $5.7 billion in annualised volume, allowing banks and payment providers to move USDC across borders and convert directly into local currencies. Arc, Circle’s own Layer-1 blockchain, is designed to support institutional layer entirely. Settlement infrastructure that doesn’t depend on Ethereum or Solana. While neither Ethereum nor Solana is large enough to impact revenue today. Both are strategic bets for the future, should rates ever fall.

The AI layer is smaller in dollar terms but structurally interesting. Circle’s own data, released by its global head of marketing in March, shows that over the past nine months AI agents completed 140 million payments totalling $43 million. 98.6% of those were settled in USDC, averaging $0.31 per transaction. There are now over 400,000 AI agents with purchasing power. The dollar amounts are still small, but not the direction. If AI agents need to pay each other for compute, data access, and API calls at high frequency and sub-cent amounts, they need something that settles instantly and costs nothing to send. Circle just launched Nanopayments specifically for this. Gasless USDC transfers as small as $0.000001, bundled off-chain and settled in batches. The testnet already supports 12 chains including Arbitrum, Base, and Ethereum.

This is the version of Circle the market is paying $123 a share for. A company at the center of tokenised finance, AI-agent commerce, cross-border payments, and prediction markets, with a regulatory tailwind from the GENIUS Act and a probable CLARITY Act passage before summer. Bernstein has a $190 target. Clear Street has $136. Seaport Global, the most bullish on the street, has $280.

The tension that doesn’t go away

Here is where I want to be honest about something the bull case tends to skip over.

Circle’s earnings depend on interest rates staying high. That is not a forever condition. The Fed will cut rates at some point. When it does, the yield on Treasury reserves backing USDC will compress, and so will Circle’s interest income.

Circle knows this. It has been expanding its transaction fees, enterprise services, the Payments Network, Arc. The stuff that doesn’t need a rate environment to work. But right now that revenue is small. Reserve income is still the whole game.

So you have these two sitting at the same stock price, and they are not the same bet.

The infrastructure thesis says USDC is becoming genuine payment plumbing. Regulated, transparent, increasingly embedded in traditional finance in ways that are sticky regardless of rates. That thesis is supported by the data. The volume numbers, the institutional integrations, Druckenmiller’s framing, Macquarie calling stablecoins a foundational layer of global financial infrastructure. If this thesis is right, Circle looks cheap at any rate environment because the addressable market is the entire global payments system.

The rates trade thesis says Circle is a levered bet on higher-for-longer, and the stock has priced in a scenario where the Fed never meaningfully cuts again. If that thesis is what is driving the price, then every point the Fed eventually cuts by is a headwind, and the stock is running ahead of what the fundamentals actually justify at normalised rates.

Both perspectives are priced in. The war has made it hard to tell which one the market is buying.

That is probably the most useful thing to understand about CRCL right now. Not whether it goes to $190. But whether you are buying infrastructure or whether you are buying a Treasury yield proxy that has learned to tell a better story about itself. One of those is a long-term position. The other unwinds the moment Jerome Powell changes his mind.

For now, the war is keeping both alive. The oil price is doing the heavy lifting and somewhere in the gap between these two scenarios lies the true value of a company that figured out how to make dollar-denominated internet money, but now has to figure out how to survive the moment when the dollar stops yielding 5%.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.

? Bitmain

What's good