Coinbase's Walled Garden🪴

Tokenised equities, sentiment markets, leverage for normies and the cost of leaving.

There’s a pattern that repeats itself across industries, across decades, across every market that’s ever existed. First comes the explosion. A thousand flowers bloom, each claiming to do one specific thing better than anyone else. Specialists proliferate. Niche tools multiply. Consumers are told that choice is freedom, that customisation is power, that the future belongs to those who unbundle the monoliths.

Then, quietly and inevitably, the pendulum swings back.

Not because the specialists were wrong. Not because the monoliths were good. But because fragmentation has a cost that compounds invisibly. Every additional tool is another password to remember, another interface to learn, another point of failure in a system you’re now responsible for maintaining. Autonomy starts to feel like work. Freedom starts to feel like overhead.

The winners in the consolidation phase aren’t the ones who do everything perfectly. They’re the ones who do enough things well enough that the friction of leaving (of rebuilding your entire setup elsewhere) becomes insurmountable. They don’t trap you with contracts or lock-in. They trap you with convenience. With the accumulated weight of small integrations and minor efficiencies that aren’t worth abandoning individually, but collectively form a moat.

We saw this happen with e-commerce. With cloud computing. With streaming. We’re watching it happen now in finance.

Coinbase just made its bet on which side of the cycle we’re entering.

HyperBeat: Your Home Base for Hyperliquid

If you’re trading, building, or just paying attention to Hyperliquid, HyperBeat is where it all comes together. Instead of chasing info across Discords, X threads, and dashboards, HyperBeat gives you a single place to stay on top of what’s happening.

Curated updates and insights around the Hyperliquid ecosystem

Tools, analytics, and resources built for real users

Community-first, signal > noise

Made for traders who actually care about execution and edge

If Hyperliquid is on your radar, HyperBeat should be too.

Let me back up.

For most of its life, Coinbase was legible. It was the place Americans went to buy Bitcoin without feeling like they were doing something vaguely criminal. It had regulatory licenses. It had a clean interface. It had customer support that, while often terrible, at least theoretically existed. The company went public in 2021 at a $65 billion valuation on the thesis that it was the on-ramp to crypto, and for a while, that thesis held.

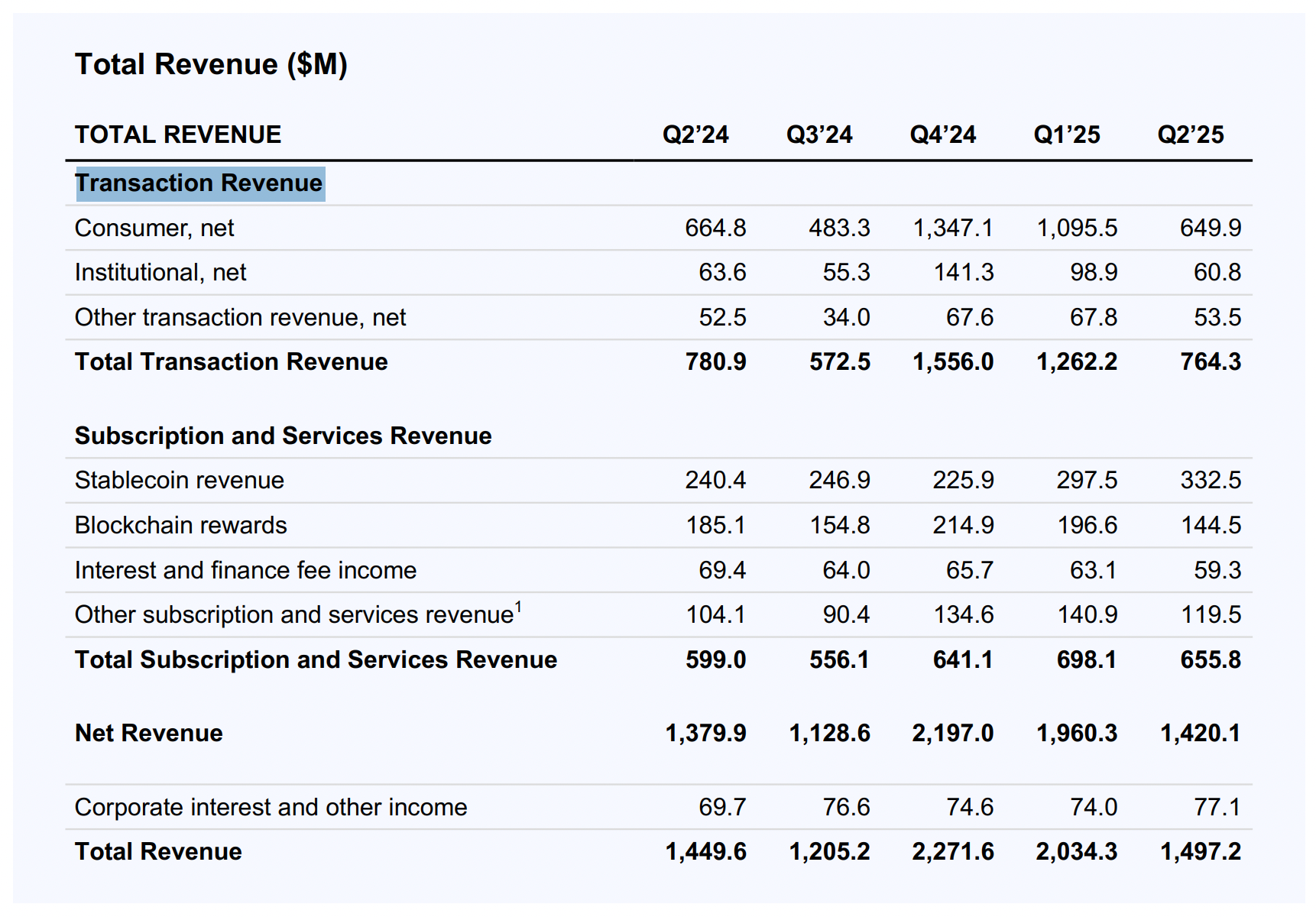

But by 2025, being “the on-ramp to crypto” started to look like a bad business. Spot trading fees were compressing. Retail trading volume was wildly cyclical, spiking during bull runs and collapsing during bear markets. Bitcoin maxis were increasingly comfortable using self-custody wallets. Regulators were still suing the company. And Robinhood, which started as a stock trading app and crept into crypto, was suddenly worth $105 billion, nearly twice Coinbase’s market cap. Coinbase’s revenue in 2021 was over 90% transaction-based. By Q2 2025, that number had fallen below 55%.

So Coinbase did what you do when your core product is under pressure: it tried to become everything else.

The “Everything Exchange” thesis, as they’re calling it, is a bet that aggregation beats specialisation.

Stock trading means users can now react to Apple earnings at midnight using USDC without leaving the app. Prediction markets mean they’re checking prices on “Will the Fed cut rates?” during lunch. Perpetual futures mean they can lever up their Tesla position by 50x on a Sunday. Each new surface is another reason to open the app, another opportunity to capture a spread, a fee, or some stablecoin interest on idle balances.

The strategy is “let’s be Robinhood” or “let’s make sure our users never need Robinhood?”

There’s an old idea in fintech that users want specialised apps. One app for investing, one for banking, one for payments, one for crypto. Coinbase is betting the opposite: that once you’ve done KYC once and linked your bank account once, you don’t want to do it nine more times elsewhere.

This is the “aggregation beats specialisation” thesis. And it makes sense in a world where the underlying assets are increasingly just tokens on a blockchain anyway. If a stock is a token and a prediction market contract is a token and a memecoin is a token, why shouldn’t they all trade in the same venue?

The mechanical logic is that you deposit dollars (or USDC), you trade everything, you withdraw dollars (or USDC). No bridging between platforms. No multiple account minimums. Just one pool of capital flows between asset classes.

The more Coinbase resembles a traditional brokerage, the more it has to compete on traditional brokerage terms. And Robinhood has 27 million funded accounts. Coinbase has about 9 million monthly transacting users. The differentiator can’t just be “we also have stocks now.” It has to be the rails.

Read: $COIN v/s $HOOD: The $160 Billion Battle 💥

The promise is 24/7 liquidity for everything. No market hours. No settlement delays. No waiting for your broker to approve your margin request while the trade moves against you.

Does this matter to most users? Probably not yet. Most people don’t need to trade Apple stock at 3 a.m. on a Saturday. But some do. And if you’re the venue that lets them do it, you get their flow. Once you have their flow, you get their data. Once you have their data, you can build better products. Once you have better products, you get more flow.

It’s a flywheel, assuming the flywheel starts spinning.

The prediction market play

Prediction markets are the most unusual part of this bundle, and perhaps the most important. They’re not really “trading” in the traditional sense. Instead, they’re structured bets on binary outcomes. Will Trump win? Will the Fed hike? Will the Lakers make the playoffs?

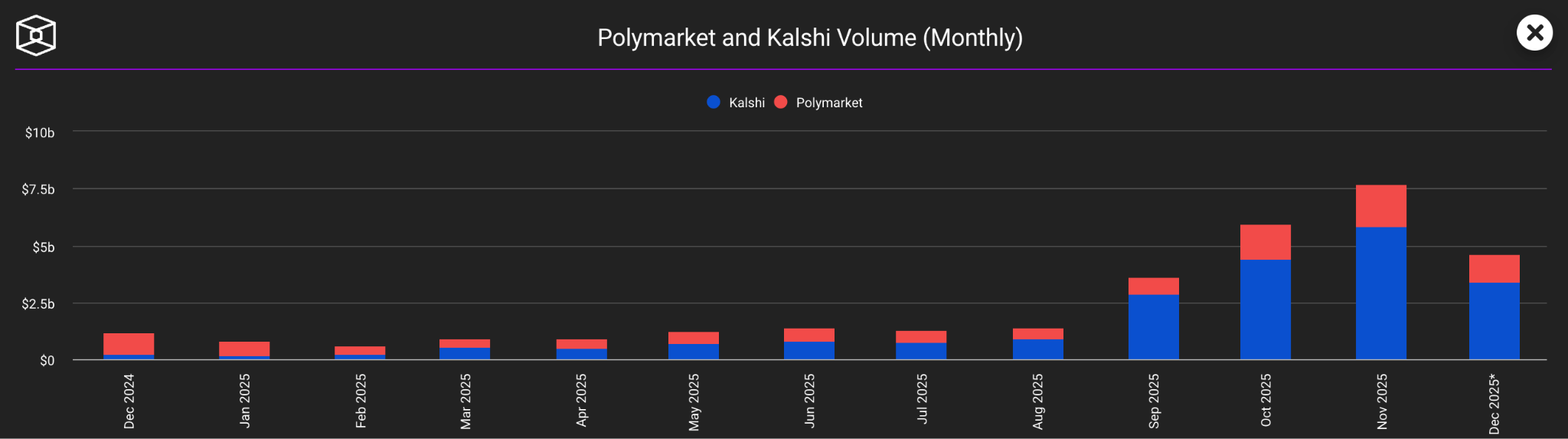

The contracts disappear after they settle, so there’s no long-term holder base. The liquidity is event-driven, which means it’s spiky and unpredictable. And yet platforms like Kalshi and Polymarket saw monthly volumes spike to more than $7 billion in November.

Why? Because prediction markets are social tools. They’re a way to have an opinion with stakes attached. They’re a reason to check your phone during the fourth quarter of a game or during election night.

For Coinbase, prediction markets solve a specific problem: engagement. Crypto can be boring when prices are flat. Stocks can be boring when your portfolio is just sitting there. But there’s always some event happening somewhere that people care about. Integrating Kalshi gives users a reason to stay in the app even when their Bitcoin isn’t moving.

The bet is that users who come for the election markets stay for the stock trading, or vice versa. The bet is that more surfaces equals more stickiness.

The business model is margin

Strip away the innovation narrative and what you’re really looking at is a company trying to monetise the same user in more ways. Transaction fees on stock trades. Spreads on DEX swaps. Interest on stablecoin balances. Borrowing fees on crypto-backed loans. Subscription revenue from Coinbase One. Infrastructure fees from developers using the Base blockchain.

I’m not criticising. This is just how exchanges work. The best exchanges aren’t the ones with the lowest fees. They’re the ones users can’t leave because leaving means rebuilding their entire setup elsewhere.

Coinbase is building a walled garden, but the walls are made of convenience instead of lock-in. You can still withdraw your crypto. You can still move your stocks to Fidelity. You just probably won’t, because why would you?

Coinbase’s advantage is supposed to be that it’s on-chain. That it can offer tokenised stocks and instant settlement and programmable money. But for now, its stock trading looks a lot like Robinhood’s stock trading, just with extended hours. Its prediction markets look a lot like Kalshi, just embedded in a different app.

The real differentiation has to come from Base, the Layer 2 blockchain that Coinbase built and controls. If stocks actually move on-chain, if payments actually use stablecoins, if AI agents actually start transacting autonomously using the x402 protocol, then Coinbase has built something Robinhood can’t easily copy.

But that’s a long-term story. In the short term, the competition is about who has the stickiest app. And adding more features doesn’t automatically make an app stickier. It can also make it more cluttered, more confusing, and more overwhelming for new users who just want to buy some Bitcoin.

There’s a segment of crypto users who are going to hate this. The true believers. The people who wanted Coinbase to be the onramp to decentralised finance, not a centralised superapp that also happens to have some DeFi features buried in a submenu.

Coinbase has clearly chosen scale over purity. It wants a billion users, not a million purists. It wants to be the default financial venue for the general public, not the preferred exchange for people who run their own nodes.

This is probably the right business decision. The mass market doesn’t care about decentralisation. The mass market prioritises convenience, speed, and avoiding financial loss. If Coinbase can deliver that, the philosophy doesn’t matter.

But it does create a strange tension. Coinbase is trying to be both the infrastructure for an on-chain world and a centralised exchange that competes with Schwab. It’s trying to be both the champion of crypto and the company that makes crypto invisible. It’s trying to be both rebellious and regulated.

Maybe that’s possible. Maybe the future is a regulated on-chain exchange that feels like using Venmo. Or maybe trying to be everything for everyone means you end up being nothing special to anyone.

This is the Amazon strategy. Amazon isn’t the best at any one thing. It’s not the best bookstore or the best grocery store or the best streaming service. But it’s good enough at all of them that most people don’t bother going anywhere else.

However, many companies have tried to build the everything app, and most of them just built a cluttered app.

If Coinbase can own the full loop of earn, trade, hedge, borrow, pay, repeat, it doesn’t matter if individual features are slightly worse than specialised competitors. The switching cost and the hassle of managing multiple accounts will keep users inside the ecosystem.

That’s all about Coinbase’s everything exchange.

See you with another thought next week.

Until then, DYOR.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.