Hello,

Google is one of the three largest cloud providers on Earth, and right now it’s buying $920 million worth of compute per month from SpaceX. A rocket company.

That is how broken the GPU capacity market is. There is no benchmark for pricing or a way for lenders to hedge the hardware they are financing; everything runs on blind capital allocation. And this is about to change because the CME and ICE have announced they will list futures contracts for GPU compute time.

Compute is being pulled into a full-scale capital market, the same way electricity was in the 1990s, and today I will dig into what this new, liquid forward curve, powered by stablecoin settlement, could unlock for the largest infrastructure buildout since the railroads.

")

Making Compute Tradable

When I say compute is following electricity’s path into a capital market, I mean it very specifically, and understanding it will tell us exactly how this market can be built.

There is a huge distinction in commodity markets between what traders call stock goods and flow goods. Oil, for instance, is a stock good because you can store it in a tanker until there is a buyer. You can stockpile crude when prices are low and sell when prices spike. Compute, on the other hand, is a flow good because you rent a GPU for a period of time and pay for access to its computational power over that window. And any capacity that goes unused during that time is gone permanently.

A GPU sitting idle in a rack is not a “stored compute” any more than a disconnected power plant is “stored electricity” because in both cases the valuable product is the flow - GPU hours or kilowatt-hours and not the physical machine producing it.

This is a critical difference for pricing because stock commodities have a built-in stabiliser in the form of inventories that flow commodities lack. The inventory can be released during periods of high volatility to counter price rallies. Flow commodities don’t have such a buffer; that’s why compute spot prices often swing hard.

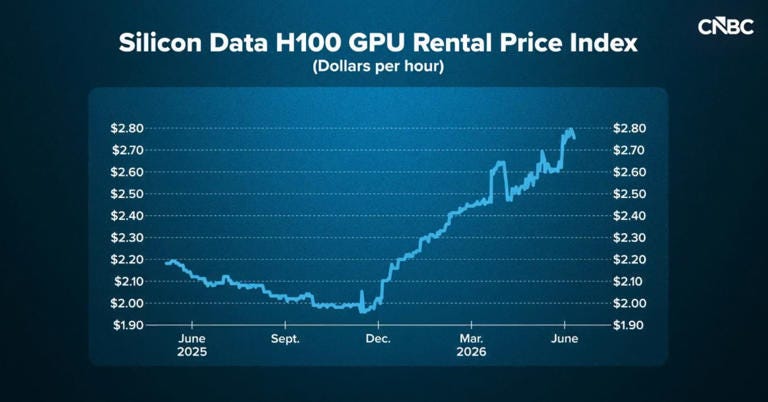

In mid-2025, compute spot prices had collapsed by 70% in 18 months as a lot of new supply flooded the market alongside Nvidia’s next-generation Blackwell chips, making the H100s less desirable. But then they again surged 48% in just four days this year when demand spiked due to HBM manufacturing, and there was no inventory anywhere to absorb it. For AI companies, whose training runs cost tens of millions of dollars, and lenders who have financed over $120 billion in data-centre credits for this hardware, the volatility with no hedging instrument is an existential problem.

And there is a second problem that sits on top of this. A barrel of oil is always identical to every other barrel anywhere in the world, which is exactly what allows it to be traded on an exchange without inspecting the physical product. But an H100 in Virginia is a measurably different product from an H100 in Iceland because the chip, cluster configuration, and the neighbouring workloads will all affect its real-world performance.

Benchmarking data across global GPU providers has shown up to 38% performance variance for nominally identical hardware. Electricity had this same problem in the 1990s: power on the Texas grid was a different product from power in the mid-Atlantic because transmission and local demand created different conditions at every point in the network. The only way for them to solve this was by giving each node its own price, which can be quoted as a spread against a reference benchmark, and that reference benchmark is exactly what the compute market is missing right now.

SF Compute has built a live order book for GPU time, where buyers and sellers trade hours, much like you would trade any commodity on a spot market. The logic is that once you have a liquid spot market, you can use it to derive an index price from trading activity. And that same index price could then be used to build a cash-settled future on top of it.

Once a data centre can sell a futures contract and lock in revenue months ahead, it can approach its lenders and show them that its revenue is hedged, thereby securing lower interest rates and building more capacity. Which, in turn, can bring overall compute prices down for everyone.

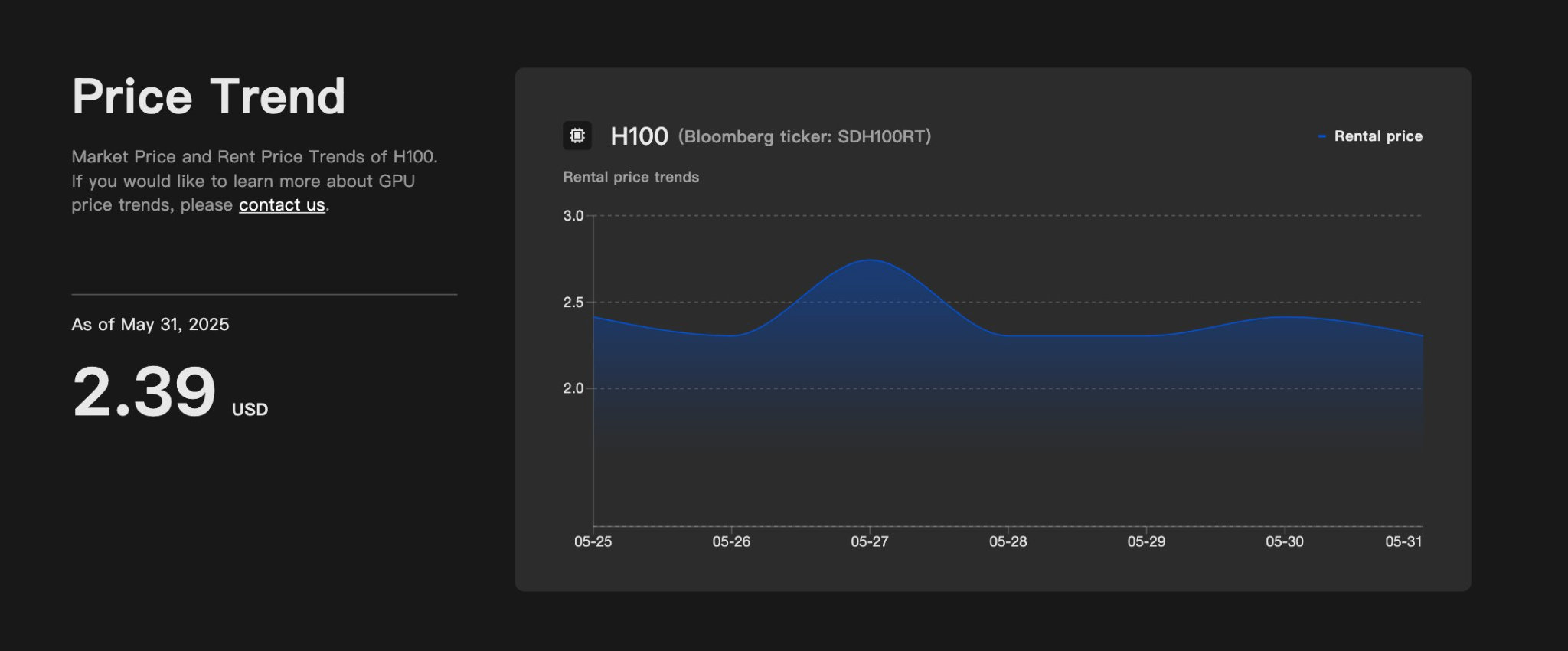

Another company, Silicon Data, has built a daily index called SDH100RT, which has been live on Bloomberg terminals since May last year and has so far aggregated 3.5 million data points from global providers into a single benchmark for the cost of an hour of H100 GPU time. The CME’s newly announced futures contract will settle against its index. There are a few more firms racing to build this now because becoming the reference price allows them to capture a thin layer of every transaction in the market for as long as it exists.

The electricity market went through this exact phase too: when, in 1993, Nord Pool opened the first electricity futures exchange, more than 200 new power marketing firms launched. It took the industry a decade to debate whether electricity was even a commodity in a legal sense, but today it’s a $6 trillion annual market. Compute is following a similar timeline right now.

The Dealer in the Middle

So we have what we can all call the first Compute spot markets with price indices in some form, and the exchanges have announced intent too. But between an index price on a Bloomberg terminal and a functioning capital market, there is another critical layer that makes it all work, and it looks very different from trading.

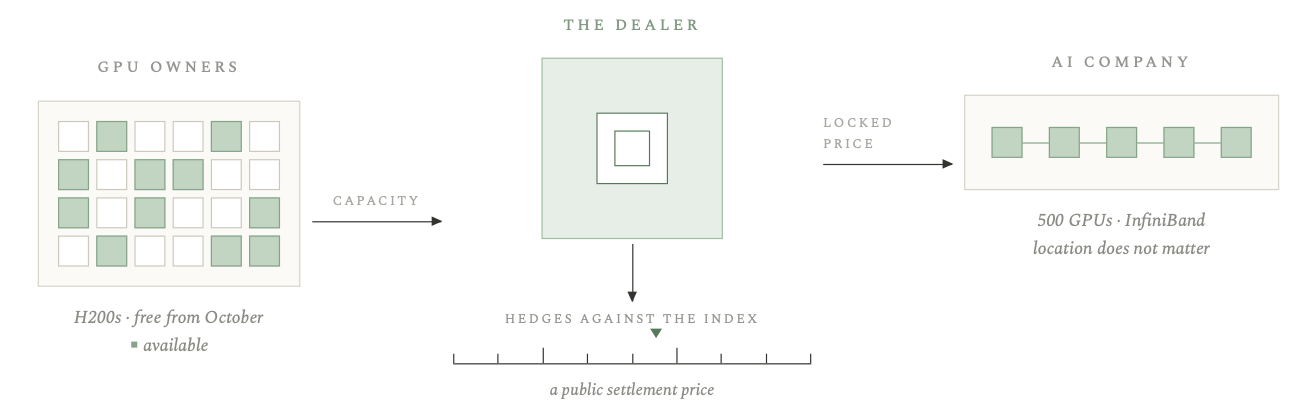

A compute futures market will not function the way a stock exchange does, in which standardised shares change hands between anonymous buyers. It will be driven by dealers who sit between GPU owners wanting to lock in revenue and AI companies wanting to lock in costs.

For example, let’s assume a data centre has plenty of H200s available in the US starting in October. There is a startup that needs 500 GPUs but only cares that the interconnect is InfiniBand (a communication medium for GPUs), not where the machines are located. Now, this is a very specific ask, and someone will need to take the custom order on one side and hedge the exposure against the standardised index on the other.

And it’s not something new; every commodity in the past has needed such a layer, where someone can absorb the messy linkages of the physical product and translate them into fungible units that an exchange can trade. An H100 sitting in a rack is just a bespoke contract that nobody else can price. It generates revenue for only one party under a private agreement, and the rest of the financial system cannot even touch it. But if you can wrap it with an index price and a public settlement layer, it can become a live commodity that a lender can hedge.

In 2023, CoreWeave borrowed $2.3 billion using just Nvidia GPUs as collateral, the first time H100 hardware had ever secured a loan. Its most recent facility got an investment-grade rating from Moody’s, based on Meta’s creditworthiness, not CoreWeave’s, because Meta signed a take-or-pay contract that requires payment whether or not they actually use the compute.

This is also where crypto rails become load-bearing. The buyers and sellers of compute are global, and none of them can open a US commodities exchange account with CFTC approval. But a crypto wallet can settle a stablecoin payment, and any wallet can hold a tokenised compute credit.

GPU export controls already reveal how compute access is geopolitically stratified, as Nvidia has been unable to ship frontier chips to China and dozens of other countries. A compute futures market settled in stablecoins can enable researchers and startups outside the export-controlled tier to access compute pricing and hedge their costs through infrastructure that routes around constrained access, much like stablecoins already do in Argentina and Nigeria.

The Liquid Forward Curve

Right now, building a GPU cluster means borrowing millions of dollars against revenue you cannot lock in, because no instrument in global financial markets exists to do so. But a liquid forward curve allows companies to borrow against hedged revenue at a lower rate than they would against an unhedged position. This means you get a cheaper cost per compute hour. So who is going to build the settlement layer for the forward curve?

The only solution needed right now is a settlement layer in which the collateral is verifiable by anyone and the forward curve is a public good. Currently, there’s no way to verify the condition of the pledged hardware, whether it has been double-collateralised, or its actual utilisation rate. But if the GPU and its revenue stream are tokenised as on-chain assets, every lender can verify the collateral in real time, making the forward curve publicly visible rather than trapped in bilateral negotiations.

And then there is also an upcoming generation where AI agents will buy compute per inference call, and they cannot open bank accounts. Crypto is the only payment gateway that can clear a micro-transaction between an agent in Tokyo and a GPU rack in Virginia in under a second.

Now there are severe counterweights to this, because the GPU supply is brutally concentrated right now. The top hyperscalers in the market control 78% of global IT power. Nvidia holds over 80% of the high-end AI chip market, and its product launch schedule can move the entire market. The standardisation is a bottleneck, but financialising an asset class during a buildout boom can make it more contagious.

More than $120 billion of AI infrastructure debt has been moved off balance sheets into Wall Street-funded SPVs, and much of it into corporate bond funds sitting inside target-date retirement products, where the person whose savings are exposed has absolutely no idea. I believe there’s a high likelihood that the financing models used to build the infrastructure embed assumptions about residual hardware values that available data does not yet support.

The electricity market did not stop at the generator. It went all the way through to the wall socket and into the price of everything that uses power. The compute market has a lot of wiring left to string too!

That’s all for today!

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.