Hello,

Somewhere on Crypto Twitter right now, a trader is looking at a token that’s up 1,400% in a week. A classic pump, as always, but the project has almost no real users, and most of the tokens in circulation are sitting in a few wallets that never move. He’s seen this movie before, and he knows how it ends.

So he does what anyone would do. He opens a short, figuring the price could crash at any moment, and goes to bed. But when he wakes up in the morning, his shorts are liquidated.

Now, here’s the interesting part: his thesis wasn’t wrong. That pump really was fake. He just didn’t know what he was actually betting against.

This isn’t some made-up story. It’s what actually happened with a token called MYX in September 2025. In one week, MYX shot up from $1.30 to $18.42, even though there were no major announcements or updates behind the product. There were no new users or new activity reported. And the people who figured out the rally was fake and shorted it? They lost $89.51 million doing it.

These are called crime coins. The team behind the token locks up most of the supply, partners with a trading firm to push the price around, and traps anyone who tries to bet on either side. In this piece, we’ll break down how these operations are built, who controls the supply, and why the industry keeps letting it happen.

The Setup

Every crime coin starts with a written agreement between two parties.

On one side is the team launching the token. On the other hand, there is a market maker, a trading firm that quotes prices on exchanges so the token can be traded. This part is the same across all of crypto; what’s not is what’s inside the contract.

The contract usually runs on a 70/30 split. Meaning, for every dollar of trading profit the token generates, 70 cents goes to the market maker and 30 cents to the project. And the contract doesn’t stop at dividing the money. It also spells out, in writing, the market maker’s job to “manage the price” of the token once it lists.

The industry calls this price guidance. What it actually means is the market maker is being paid to push the price in whichever direction the two parties want that week. Across MYX and thousands of tokens launched from the same playbook, this arrangement has reportedly paid out over $30 million per cycle.

What matters more is how the market maker actually gets the tokens: they’re not buying them; they always borrow them as a loan.

The arrangement is called a loan-option model, and it’s the standard way market makers and projects work together on paper. At launch, the project lends the market maker a large number of tokens, usually worth tens of millions of dollars. The market maker then has 12 months to either return them or buy them back at a higher price agreed in advance. That is what the paperwork says, but what usually happens is very different. The market maker sells the borrowed tokens on day one, flooding the market with supply and crashing the price. Once the price is low, they buy the same amount back cheaply, return it to the project, and pocket the difference.

Crime coins use this same loan-option model. The only twist they added is a second revenue stream on top of it. Beyond dumping the loaned tokens, crime coin operators have also figured out how to pull money from the retail traders who spot the manipulation and try to short the crash. (More on how that works in the next section.)

Now, technically, for this to work, the team and the market maker need near-total control over the token’s supply. And on most crime coin launches, they have it. Over 90% of tokens typically sit in wallets that all trace back to a single operator. On a block explorer, these wallets appear as a long list of unrelated addresses, which makes the token seem to have a broad base of holders. But on-chain analysis almost always shows they’re controlled by the same people, just split up to look organic.

In MYX’s case, the concentration was extreme. At the peak of the rally, only about 20% of the supply was outside the control of the team and its allies. The other 80% sat in two places. Some of it was locked in vesting contracts, which meant it literally could not be sold yet. The rest was in wallets belonging to core contributors and early investors, who technically could sell but chose not to. Either way, those tokens were not going to hit the market.

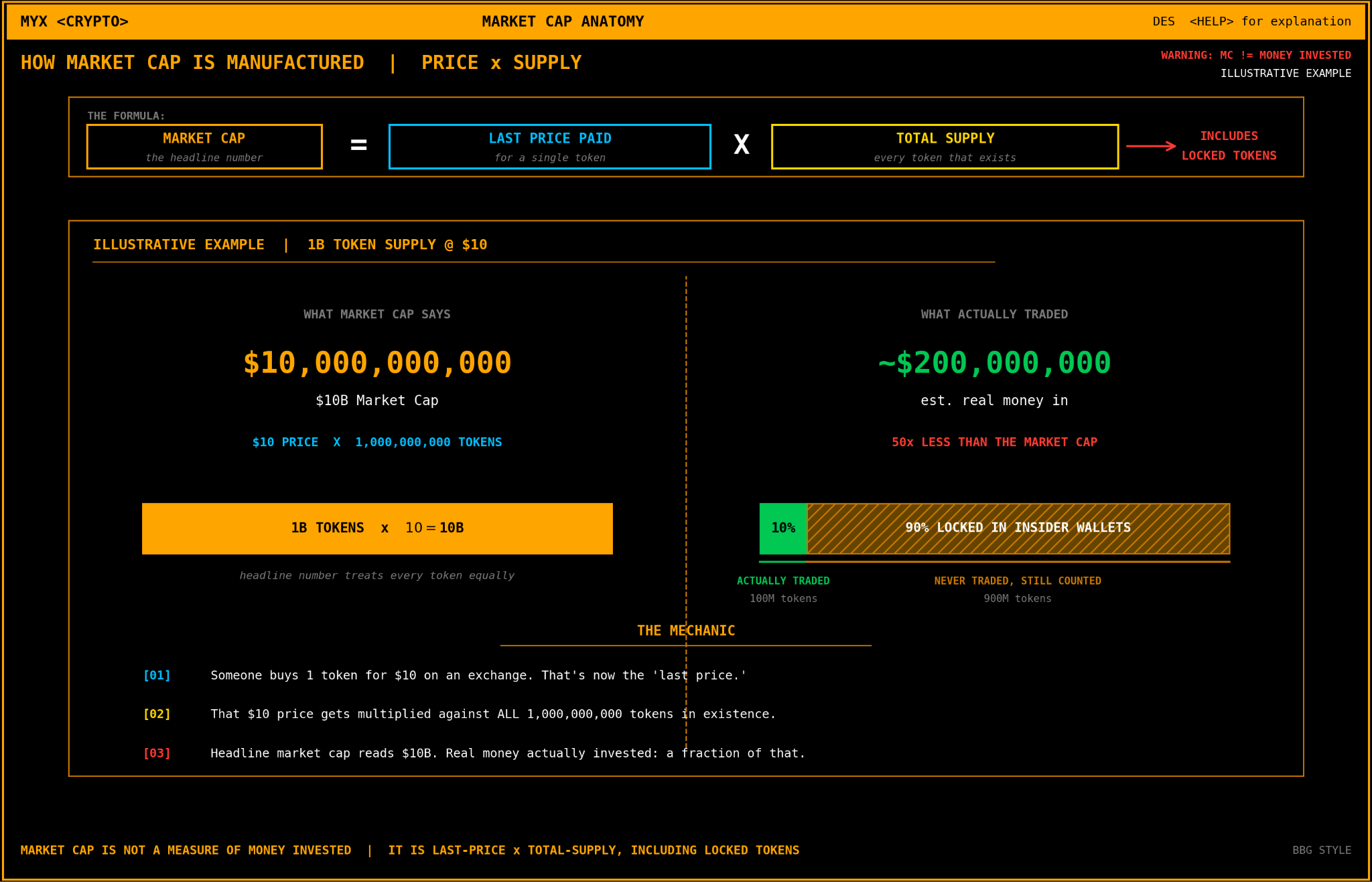

Normally, this is the difference you see between a token’s fully diluted valuation and its market cap. Fully diluted valuation counts every token that will ever exist. Market cap only counts the ones in circulation. On a crime coin, even that distinction breaks down, because the supply that counts as circulating isn’t really free to trade either.

That is how MYX’s market cap could go from $200 million to $3.35 billion in a week without a single new user signing up or any new money being deposited into the protocol. The small slice of MYX actually trading on exchanges was setting the implied price for the much bigger pile that wasn’t trading at all.

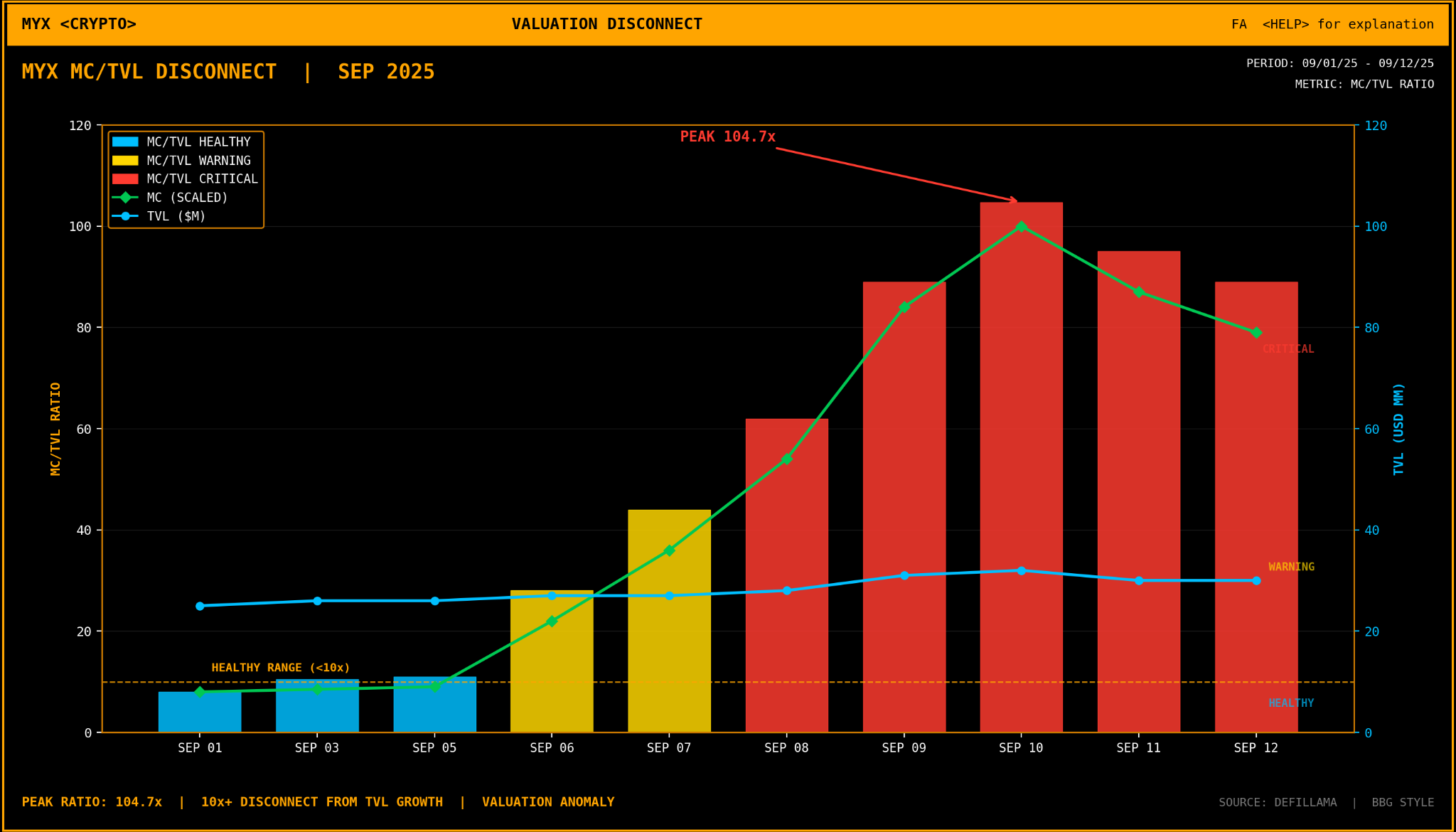

This gap between MYX’s price and its actual business was obvious to anyone who checked. There is a standard DeFi metric for this called TVL, short for total value locked, which is just the amount of money users have deposited into the protocol to use its product. MYX’s TVL stayed between $25 million and $32 million throughout the week as its market cap climbed to $3.35 billion. The market cap-to-TVL ratio is roughly 100. Even the largest DeFi protocols, like Uniswap and Aave, are between 1 and 4. And underneath all of this, MYX, as a business, was generating about $5 million a year in revenue, which the market valued at $17.7 billion. That makes P/S multiple of ~3500x.

All of this setup was running long before the public ever saw MYX trending. Months before the rally started, the operator was running wash trades across multiple exchanges, including PancakeSwap, Bitget, and Binance.

A wash trade is when the same party sits on both sides of a transaction, essentially buying from themselves to engineer high volume. This is because larger exchanges rely heavily on trading volume when deciding which tokens to list and promote, and manufactured volume on one exchange often leads to a token being listed on the next. When investigators were looking back at MYX’s trading history, they traced dozens of small buy orders across different exchanges, all of which eventually converged into a single centralised wallet. A single operator artificially inflated demand by executing numerous small transactions with themselves, creating the illusion of a genuine market

The Four Stages of Extraction

The whole operation usually unfolds in four stages, each exploiting how retail traders typically behave.

The first stage is attracting shorts. The market maker starts pushing the token’s price up on very little actual volume. This is easy to pull off because supply is mostly locked up, and order books on smaller exchanges like Bitget and Gate are already thin. When an order book is thin, it takes very little volume to move the price by 5 or 10%. Take RAVE, another crime coin, for example. Even after it had been run up and was doing billions in daily volume, it still only took $172,000 of one-sided flow on Gate to move the price by 1%. A 10% move costs under $2 million.

The early rally is not about making money on the long side. The money the operator is actually after is on the short side. The whole point of this first stage is to make the pump look so obviously unsustainable that sceptical traders show up to bet against it.

This is counterintuitive because the more fake the pump looks, the better it is for the operator. A normal market maker would want a rally that looks organic and natural. A crime coin operator wants a move that visibly screams manipulation, because that is exactly what pulls in the traders who will short it.

The second stage is setting the hook. Once enough shorts are piled in, the operators start closing some of the long positions they were using to drive the pump, unwinding part of their hedge, and engineering a visible dip alongside a sharp drop in open interest. When open interest falls while price dips, it looks exactly like a local top forming on the chart. This convinces the sceptical traders still on the sidelines that the pump has finally rolled over, and they short into the retracement.

The third stage is the squeeze. This is where the traders who took those shorts start to actually lose money. Most trading on crime coins doesn’t happen through people buying and holding the token. It happens through perps. To keep the longs and shorts balanced, the exchange charges a fee called the funding rate. Every few hours, traders on one side of the market pay a fee to traders on the other side. Which side pays depends on whether the perp is trading above or below the spot price. If the perp is trading higher, longs pay shorts. If it is trading lower, shorts pay longs. In a normal market, this fee runs a fraction of a per cent per day

But on a crime coin in squeeze mode, the funding rate on the short side runs around -2% every 4 hours. That works out to 12% of your collateral per day, drained just for keeping the short open. Hold it for a week, and 84% of your money is gone before the price has resolved anything.

On top of the funding rate, there is leverage. Most shorts on crime coins are opened with 20x, 50x, or sometimes 125x leverage. At 50x, a 2% move in the wrong direction wipes the whole position out, and the exchange liquidates you.

Once enough shorts get liquidated, it creates a domino effect. Every liquidated short forces a buy. Every forced buy pushes the price higher. The higher price then liquidates the next row of shorts above it, forcing more buying. The traders who correctly called the pump fake end up as the biggest source of buying pressure, keeping it going.

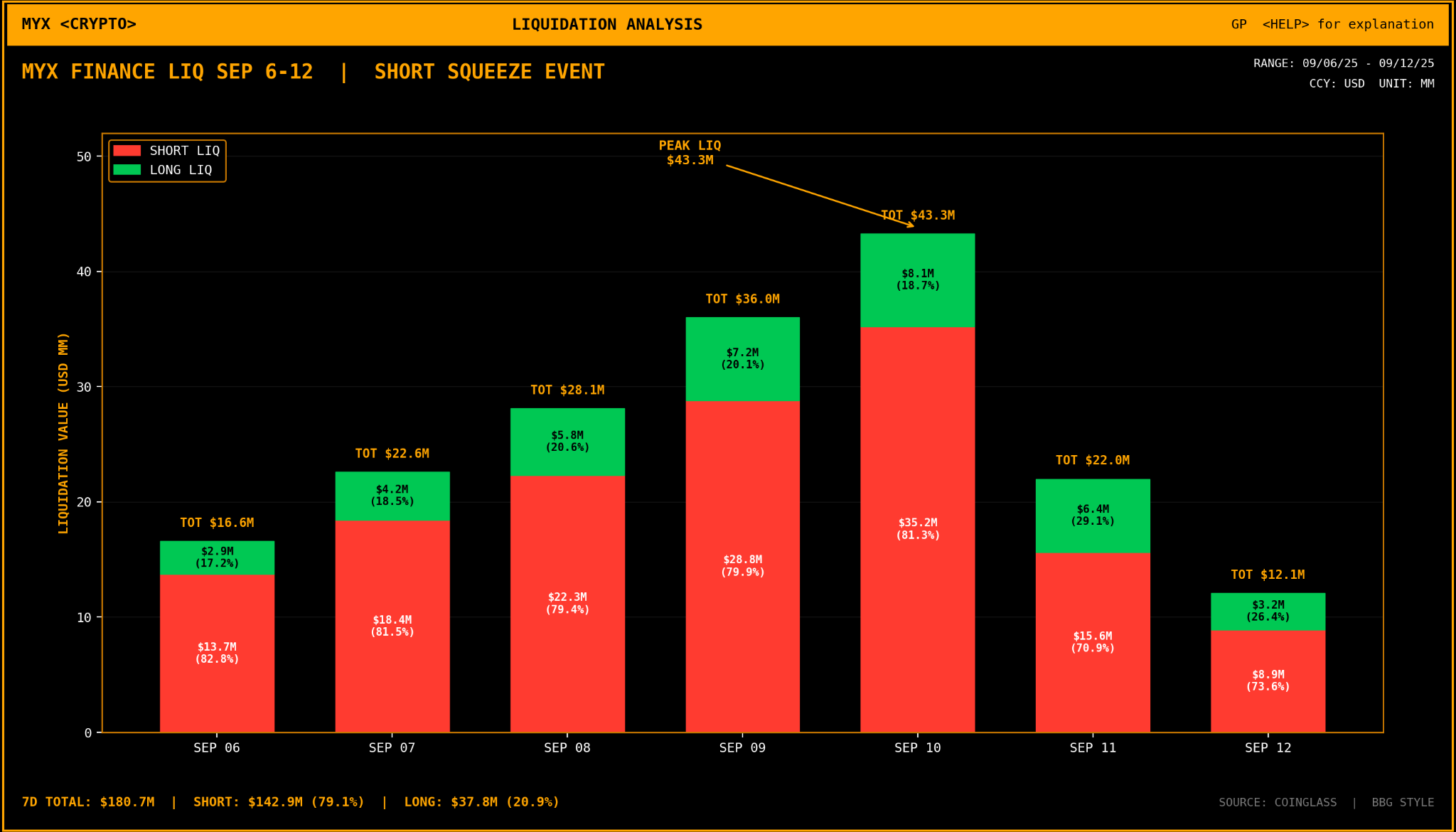

MYX showed us how far this can go. On September 8, 2025, $16.53 million in MYX positions were liquidated in a single day, and $13.68 million of that came from shorts being force-closed. To put that in context, total open interest on MYX that day was around $262 million. In other words, more than 6% of all outstanding leverage on the token was wiped out in 24 hours, almost entirely on the short side. Across the full run, $89.51 million in shorts were wiped out against $23.45 million in longs. Roughly four shorts were destroyed for every long.

The fourth stage is distribution. Once the shorts are cleared and the price is at its peak, the operator reverses the position. They open shorts of their own, close their longs, and begin moving their locked-up tokens toward centralised exchanges. This is where many experienced on-chain traders get caught. When tokens start flowing from known operator wallets onto an exchange, the obvious read is that a dump is coming, and the right move is to short. But these deposits can be deceptive. In crime coin cycles, they are often used as bait to draw in another wave of shorts before the real distribution begins.

What makes all of this possible is how narrow the other side of the trade actually is. A real market has participants with different beliefs, timeframes, and information sets. A crime coin market doesn’t. Every trade, long or short, ends up against the same operator running the same playbook.

Who Owns the Supply Owns the Market

Everything in a crime coin operation traces back to one fact: the team and their allies control nearly all of the supply. That ownership is what lets one operator run spot and perps on the same token at the same time, decide when the rally pauses, and decide when shorts get squeezed. Nobody else holds enough tokens to stop any of it.

On MYX, it was up, with open interest above market cap, two-thirds of the volume on Bitget, and short-side funding that stayed punishing for days. The traders who tried to fade the run read the chart correctly, but had no idea it was being manipulated.

And none of these is hidden. The wallet clusters are on-chain, the volume share is on Coinglass, and the market makers are named in these projects’ funding decks. The industry doesn’t act because the industry gets paid for it. Market makers take a cut of the trading. Projects book treasury valuations off tokens they control the float of. Exchanges collect fees whether the trade is real or manufactured. Retail is the only participant that loses.

That’s all for today.

Until then, stay curious.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.