Crypto's K-Shaped Thesis

Crypto's biggest wins are making everyone money except crypto investors.

Hello,

There’s this famous Crypto Influencer who goes by the name of ThreadGuy. He rose to prominence in 2021 by teaching people how to trade NFTs. Now he sits in his New York apartment with a barrel of American crude oil behind his desk, trading pharmaceutical stocks and commodities on Hyperliquid. A few weeks ago, he had Cobie on his stream. Cobie has been one of crypto’s longest-running voices since 2012, sold Echo to Coinbase for $375 million, and now works there full-time. When ThreadGuy asked him about the state of crypto, he described something called a “K-shaped” dynamic.

“There’s this weird K-shaped thing happening in crypto,” he said, “where crypto seems to be having phenomenal success stories, much more than any previous year. But it’s just not represented in asset prices that people can buy.”

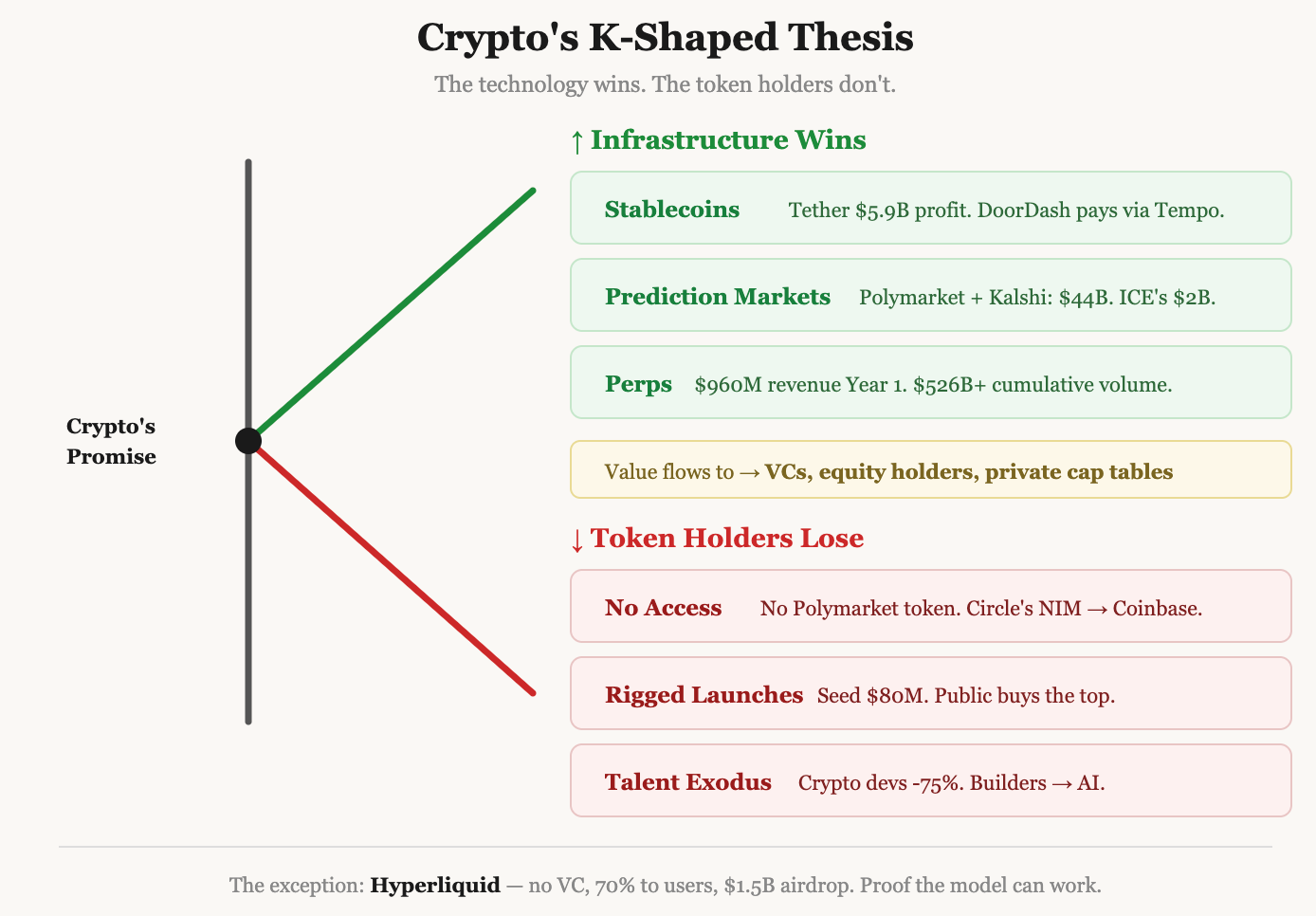

That line has been stuck in my head since. Because he’s right. Polymarket and Kalshi have become a $44 billion prediction market duopoly. Stablecoins are being used to pay gig workers. DoorDash now pays drivers through Tempo. Hyperliquid processes more trading volume than most centralised exchanges, on a chain it built from scratch. Trade XYZ predicts the Monday stock market open within 50 basis points. Crypto was supposed to move money without banks, make markets without brokers, and let anyone trade anything from anywhere at any time. By almost every measure its critics ever threw at it, it’s doing exactly that.

And the people who believed in it earliest, the ones holding tokens, have gotten almost nothing from it. You can’t buy Polymarket equity. You can’t buy Tempo. Circle went public, but half of USDC’s net interest margin goes to Coinbase for distribution rights before shareholders see a cent. The platforms are all winners, but token holders lose every time.

That is the K-shape. And the more I looked into it, the more I realised this isn’t just a crypto problem.

Where Does The Value Go?

Let’s start with stablecoins, because they’re crypto’s true Product-market-Fit. Tether is estimated to have made $10 billion in 2025 and has roughly 100 employees. That is more profit per head than almost any company on earth. Circle went public and has a market cap of $23 billion as of April 28. Stablecoin supply has grown 100x over the past few years from $6.8 billion in 2020 to more than $315 billion today. And it is the US Treasury itself that projects it to grow to $2 trillion by 2028

This is real financial infrastructure being built on crypto rails. And for anyone holding a token, the economic relationship to all of this is zero. Tether’s profits flow to Tether’s shareholders. Circle’s economics flow to Circle’s equity holders and to Coinbase, which effectively takes 50% of USDC’s revenue just for putting it in front of users. DoorDash pays drivers through Tempo, and the value of that transaction accrues to DoorDash, Tempo, and the driver. Not to anyone’s token portfolio.

Prediction markets tell the same story. Polymarket went from a niche crypto experiment to a CNN fixture. The Wall Street Journal now uses its data alongside editorial reporting. Substack built a direct integration with Polymarket so writers can embed live odds in their posts, turning every newsletter into a real-time data terminal. ICE, the company behind the New York Stock Exchange, invested $2 billion at an $8 billion valuation. Kalshi won its CFTC legal battle and expanded into economics, sports, and science. Combined volume across both platforms hit $44 billion in 2025, with $10 billion in a single month.

None of that value went to token holders. Polymarket’s early backers, Founders Fund, General Catalyst, and Blockchain Capital, are sitting on massive unrealised gains. One of crypto’s biggest success stories runs on crypto rails, was built by crypto people, and ended up with a traditional equity cap table where the upside sits with venture capitalists (VCs).

You might argue that Polymarket hasn’t launched a token yet. That’s true, and it might launch one eventually. But even if it does, private investors have already set the valuation at $8 billion. The window where early users could have captured meaningful upside closed before most of them knew it existed. And if it never launches a token at all, then the entire value of the prediction market revolution, the thing crypto people spent years arguing would change how the world processes information, will have been captured entirely by a traditional equity cap table. Funded by VCs, exited to institutions, with zero on-chain ownership for users.

Even in DeFi, the pattern is the same. Crypto spent the better part of a decade building the infrastructure for decentralised finance — from lending protocols, automated market makers, perpetual exchanges, and stablecoin rails, mostly in the open, mostly with tokens, and mostly while regulators were actively trying to kill it. The people who built this stuff took enormous risks. The users who provided liquidity and tested these protocols when a single smart contract bug could drain everything took risks, too.

And now that the technology has proven itself, now that it’s clear that stablecoins, on-chain trading, and tokenised assets work, the companies showing up to capture the value are not the ones who took that risk.

They’re traditional firms with equity structures, private fundraising rounds, and no obligation to distribute anything to the users or communities that made the technology viable in the first place. Stripe is building stablecoin payments. PayPal has launched its own stablecoin. Banks are tokenising assets on private blockchains.

They were all observing from the back seat at what crypto built, and once they confirmed it worked, they are now rebuilding it inside walled gardens where the economics flow to shareholders.

The upside is being privatised. Tokens were supposed to be the mechanism that prevented this, the thing that let early participants share in the value they helped create. Instead, the projects that actually succeeded either never launched a token or launched one so late and at such an inflated valuation that public holders were effectively the exit liquidity for insiders who got in at a fraction of the price.

The K-shaped Capitalism Problem

And this isn’t some crypto-specific failure. This is how wealth creation works now, everywhere, and crypto just inherited the same disease it was supposed to cure.

SpaceX has gone from zero to roughly $1.75 trillion in private valuation. OpenAI is at $852 billion. Anthropic is somewhat in the same territory as $800 billion. These three companies alone represent trillions in value creation. If you were an ordinary person in the 1970s or early 2000s and thought Apple, Amazon, or Google would be important, you could just buy their shares. You could participate in the wealth creation of a company you believed in. That relationship between being right about the future and being rewarded for it, that was the basic social contract of capitalism. It no longer holds.

These generational companies remained private at every stage when the real returns were made. The only people who got access were already in the club, the Silicon Valley networks, the fund-of-funds, the LPs writing $50 million checks into venture vehicles. By the time SpaceX or OpenAI eventually goes public, the price will reflect a decade of compounded private gains that retail investors had zero access to. The number of publicly traded companies in the U.S. has dropped 46% since 1997, from about 7,500 to 4,000.

There are over 1,400 venture-backed unicorns worth a combined $5 trillion, all staying private. Companies used to go public to raise capital. Now they raise billions in private rounds, indefinitely, from the same tight circle of funds. By the time they IPO, price discovery had already happened in rooms that regular people would never be allowed to enter.

The data confirms this isn’t some paranoia. IPO returns from 1970 to 1990 averaged 5% annually, less than half of what you’d have made just by buying public companies of a similar size. Low-float IPOs, the kind SpaceX and OpenAI would likely do, have a 90% historical failure rate. Ten out of eleven low-float IPOs since 1980 underperformed the market by 50% or more within three years. So the deal being offered to normal people is, you don’t get to invest when the company is worth $10 million and growing. You get to invest when it’s worth $1.5 trillion, and the insiders are looking for liquidity to exit.

This is what is called the K-shaped economy, where gains are privatised as they flow through closed circles, and losses are socialised through overpriced IPOs, through index funds forced to buy at the top, through inflation and stagnant wages, which get spread across everyone else.

This is also what’s driving talent out of crypto. Crypto code commits fell 75% since early 2025, from 850,000 weekly to 210,000. Active developers dropped 56% to about 4,600. Where are they going? AI. GitHub now has 4.3 million AI-related repositories. LLM imports grew 178% in a year.

And this makes complete sense if you think about it in terms of the K-shape. Every major crypto onboarding wave, from 2013 altcoins, 2017 ICOs, 2021 DeFi and NFTs, to memecoins, had one thing in common: normal people made money fast. AI has that energy right now. One person, called Peter Steinberger, built OpenClaw and later sold it to OpenAI for billions, all by himself. That is the kind of energy crypto used to have. If you’re a 22-year-old like me and deciding where to spend the next five years of your life, the math isn’t that complicated. Crypto is offering you governance tokens that launch at $16 billion and bleed for two years. AI is offering you the chance to build AI agents with three people that could be worth a billion dollars before your next birthday.

The talent started leaving because, somewhere, crypto stopped distributing the upside it creates. The K-shape pushed the gains upwards, to VCs, to equity holders, to the same insiders the industry wanted to build to displace. Where is Decentralisation Anon?

Okay Enough! What’s the Solution?

So crypto has a problem. The technology is fantastic, but the people who believe in it don’t get to participate in the upside. The same privatisation dynamic that is eating away at traditional markets has infected the industry specifically designed to prevent it. Is there a way out?

Cobie thinks there might be, and I agree with him. The answer is the one thing crypto can do that no other industry can, airdrops.

Airdrops distribute ownership directly to users globally, without intermediaries, at the exact moment when ownership is most valuable. That’s what airdrops were always supposed to be. In practice, most of them have been a joke. But there’s one case that proved it can actually work, and it’s worth understanding.

I am talking about Hyperliquid. Jeff Yan and his team built a perpetual exchange from scratch on its own L1 blockchain, ran it for over a year, grew it to over $4 trillion in cumulative trading volume to date, and, when it came time to distribute ownership, allocated 70% of the total token supply to the community. All of this with no VCs, Advisors, or exchange listing partners. The actual traders who used the platform, moved capital through it, and stress-tested it for months. 94,000 addresses claimed tokens in a $1.5 billion airdrop. Some of them became millionaires overnight.

And here’s the best part. They didn’t dump the tokens. Because the people who received HYPE weren’t mercenaries farming a product they didn’t believe in. They were Hyperliquid’s best users. The most active traders, the people who moved the most capital, the ones who stayed because the product was better than the alternatives. They got ownership proportional to their contribution, and they held. The team mirrored it. After distributing about 20% of their vested tokens in the first two months (likely for taxes), they cut distributions to 1% in the following months. Today, 97% of Hyperliquid’s protocol revenue flows to HYPE buybacks and burns.

Saurabh at DCo broke down the valuation math in detail. Hyperliquid earned $960 million in revenue in 2025 on roughly $3 trillion in volume, but trades at just 10-13x revenue, compared to 25x for CME, 23x for ICE, and 22x for CBOE. It grew to nearly a billion in revenue in its first full year, has no debt, no headcount drag, and a buyback mechanism that returns almost all fees to token holders.

Hyperliquid is proof that this is possible. Distribute to users, not investors. Let actual usage drive value. Align incentives so the people who build the product and the people who use it are on the same side of the trade. But of course, most airdrops are not Hyperliquid.

Most of them are elaborate performance theatres where people pretend to use products they don’t actually care about just to farm tokens they plan to sell the second they unlock them. The projects know this is happening. The users know the projects. But everyone still plays along because admitting that an airdrop is a customer acquisition cost paid in inflated tokens won’t help raise more money on VC pitch decks. Because 90% of these tokens exist just to give VCs an exit, not to align incentives with the users.

The data from Cobie’s own analysis is damning: Ethereum’s ICO allowed retail investors to buy at a $26 million valuation and capture 7,500x returns. By the time you get to projects like Berachain, the seed round is $40 million, and the public launch price is at its peak. Retail holders are underwater, while seed investors are up 138x.

So the question is simple, and I think it matters more than most people in this industry realise: Is Hyperliquid a model or an exception?

If it’s a model, if more teams can build real products, skip the VC extraction machine, and distribute ownership to the people who actually use what they built, then crypto has something genuinely unique. SpaceX can’t airdrop shares to the people who watch its launches. OpenAI can’t distribute equity to everyone using ChatGPT. But crypto can. It has a mechanism. It’s been done at least once, and it was a success.

If it’s an exception, if Hyperliquid was just a one-off with the right team, the right product, and the right timing, then Cobie’s K-shape thesis wins. Token holders keep losing. The smart builders keep leaving for AI. And the only way to participate in crypto’s success is to buy Coinbase or Circle stock. Which is exactly the kind of outcome crypto was supposed to make impossible.

That’s all for today.

Vaidik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.

we noticed this K-shape thesis cropping up across galaxy and red beard's recent issues, the "everyone trades everything" angle is the part that should worry token holders most