Historically, finance has evolved alongside the networks that carry it.

Roman trade routes gave birth to insurance, enabling merchants to scale across geographies. Colonial shipping created the need for remittances and foreign exchange. The internet demanded new payment rails for e-commerce to proliferate.

The internet also established a model for how open networks function.

But each of these networks also required trust infrastructure to function. SWIFT works because a network of banks agreed on how to reconcile transactions without physically moving money. The NYSE’s value is in sequencing orders and enforcing integrity at high frequency. In every case, the network’s value lies in delivering trust without friction on every transaction. A financial network without implied trust eventually dies.

The cost of maintaining that trust, however, has always been the bottleneck. Each layer of verification - the auditor, the fund administrator, the custodian, the compliance officer - adds cost, adds time, and adds a permission gate. Consider traditional asset management, it scales headcount with AUM because the verification layer is human-powered.

Blockchains compress that cost. They are networks where transactions, asset positions, and liabilities can be verified by anyone, continuously, at near-zero marginal cost. You don’t need a fund administrator to check allocations quarterly - they’re onchain, visible in real time. You don’t need a custodian to hold assets - the smart contract is the custodian.

When you can verify capital deployments and how yield is generated - without relying on a fund administrator or quarterly report - you can build investment structures that would be difficult to operate on closed rails.

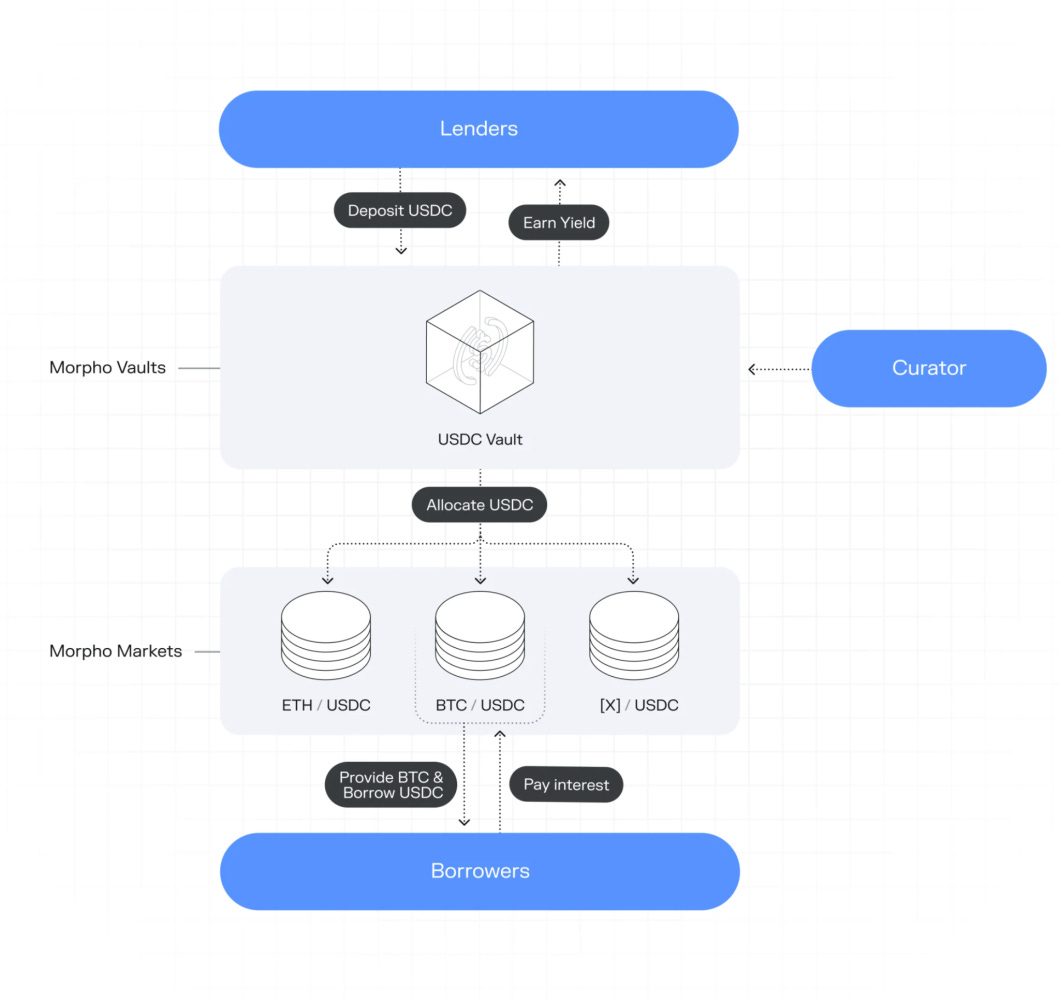

Among the most notable structures are vaults - managed funds executed entirely through smart contracts. At their core, vaults pool capital, programmatically allocate it across decentralised finance (DeFi) yield sources, and continuously route the accrued interest back to depositors.

Vaults have existed in some form since 2020. What has changed over the past eighteen months is the infrastructure surrounding them.

Vault protocols like Morpho now operate as open platforms - any asset manager can build a strategy on top, any risk curator can manage a vault, and any exchange or wallet can distribute it to their users.

This openness has allowed specialised players to plug into the same infrastructure independently, each contributing what they do best. The result is a composable, verifiable financial network that has attracted capital.

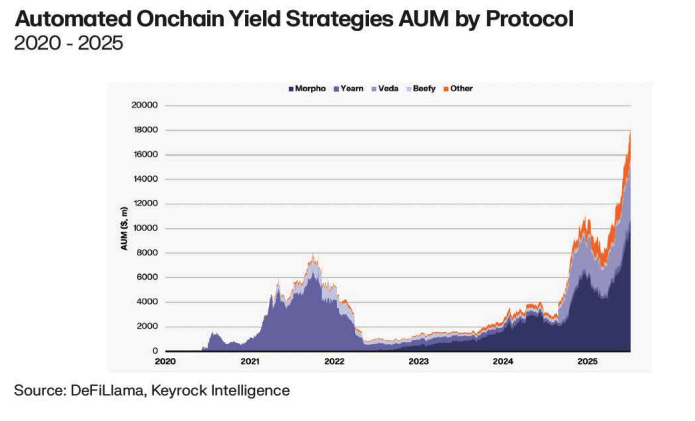

Last year alone, over $6 billion flowed into on-chain vaults. For context, tokenised Treasuries - the undisputed heavyweight of on-chain yield-generating asset classes - grew from $3.3 billion to $6.96 billion in that same timeframe. In sheer growth velocity, vaults effectively matched the most established category in institutional digital finance.

Look specifically at Morpho and Spark, the two dominant vault platforms, and their assets under management (AUM) surged from $2.46 billion to $7.64 billion today.

If you broaden the lens to the entire ecosystem of automated yield strategies, accounting lending, liquid staking, and hybrid approaches, the aggregate AUM now hovers at $17.5 billion, completely eclipsing previous highs from 2021.

How vaults got here

At its core, a vault works like a mutual fund. An investor deposits capital - typically stablecoins - and gets a receipt token showing their share of the pool. A curator then allocates that money across DeFi lending markets based on a specific strategy. As the money earns interest, returns flow back to the depositors. Simple enough.

But what makes vaults different from a normal managed account is how you can use that receipt token. It doesn’t just sit in your wallet.

Through ERC-4626, that token can be plugged into other DeFi apps. It can be used as collateral for a loan on Aave, paired with a liquidity pool on Curve, or stacked into a higher-order yield strategy. ERC-4626 allows the output of one financial product to easily become the input of another.

While composability is part of the reason for the massive scale we see today. The credit also goes to the underlying stack of products that enable the construction and distribution of vaults.

Back in the “DeFi Summer” of 2020, Yearn Finance was the first to pioneer the idea of automated yield. They proved that fund-like structures could run entirely on-chain. Instead of users manually moving capital between Aave, Compound, or Uniswap to chase the highest rates, Yearn vaults encoded these strategies into smart contracts, reallocating funds programmatically.

However, Yearn acted as both the infrastructure provider and the strategy operator - a single entity handling everything from the base smart contracts to capital allocation to user distribution. As the market expanded, this monolithic model hit its limits. Risk management, software engineering, and consumer distribution require entirely different skill sets. Bundling them into one entity created bottlenecks and concentrated risk.

To scale safely, today’s vault ecosystem has unbundled into three distinct layers. When the infrastructure builder, the risk manager, and the retail platform operate independently, each can specialise without being constrained by the others.

We can split financial services apart because the underlying blockchain system is transparent and programmable.

In regular finance, making sure different specialists (like managers and record-keepers) do their jobs requires expensive legal contracts, heavy regulation, and constant audits. But on a blockchain, smart contracts can automatically forces everyone to follow the rules, and anyone can check the work instantly.

Because the code handles the “trust,” it’s much easier to coordinate different experts. Which is why the vault stack can support five intermediaries in a chain without the aggregate overhead making the product uneconomical.

The protocol layer provides the baseline smart contract architecture. Morpho dominates here with roughly $9.6 billion in AUM.

Because of its fully permissionless design, Morpho serves as neutral infrastructure rather than a single product. It attracts a wide range of strategies. Apollo Global Management, with $940 billion in traditional assets, understands the importance of Morpho in enabling on-chain strategies. Resultantly, the company acquired 9% of Morpho’s token supply, signaling where institutional capital sees base-layer value.

The curator layer is where strategy and risk management reside. Curators function like the general partners (GPs) of on-chain finance. They define a vault’s mandate, select eligible assets, set risk limits, and manage daily reallocations.

Curators act as the risk officers of this decentralised ecosystem. Curators encode Loan-to-Value (LTV) ratios to create buffers against market volatility, dictating a threshold where an underwater position should be programmatically liquidated to protect depositors. To prevent a vault from outgrowing the liquidity of its underlying assets, they impose strict supply caps.

Additionally, they design algorithmic interest rate curves based on capital in the pool. When borrowing demand spikes and liquidity tightens, the smart contract automatically drives up the cost of capital, naturally deleveraging the system and attracting new deposits. This helps abstract the underlying complexity and provides a stable and predictable yield for institutions and retailers alike.

By separating them from the protocol layer, curators are forced to compete on performance. Curated Morpho vaults consistently deliver roughly double the APY of vanilla lending markets today, because managers competitively shift capital rather than leaving it stagnant in a pool.

Today, a growing set of specialised curators compete for deposits on these platforms.

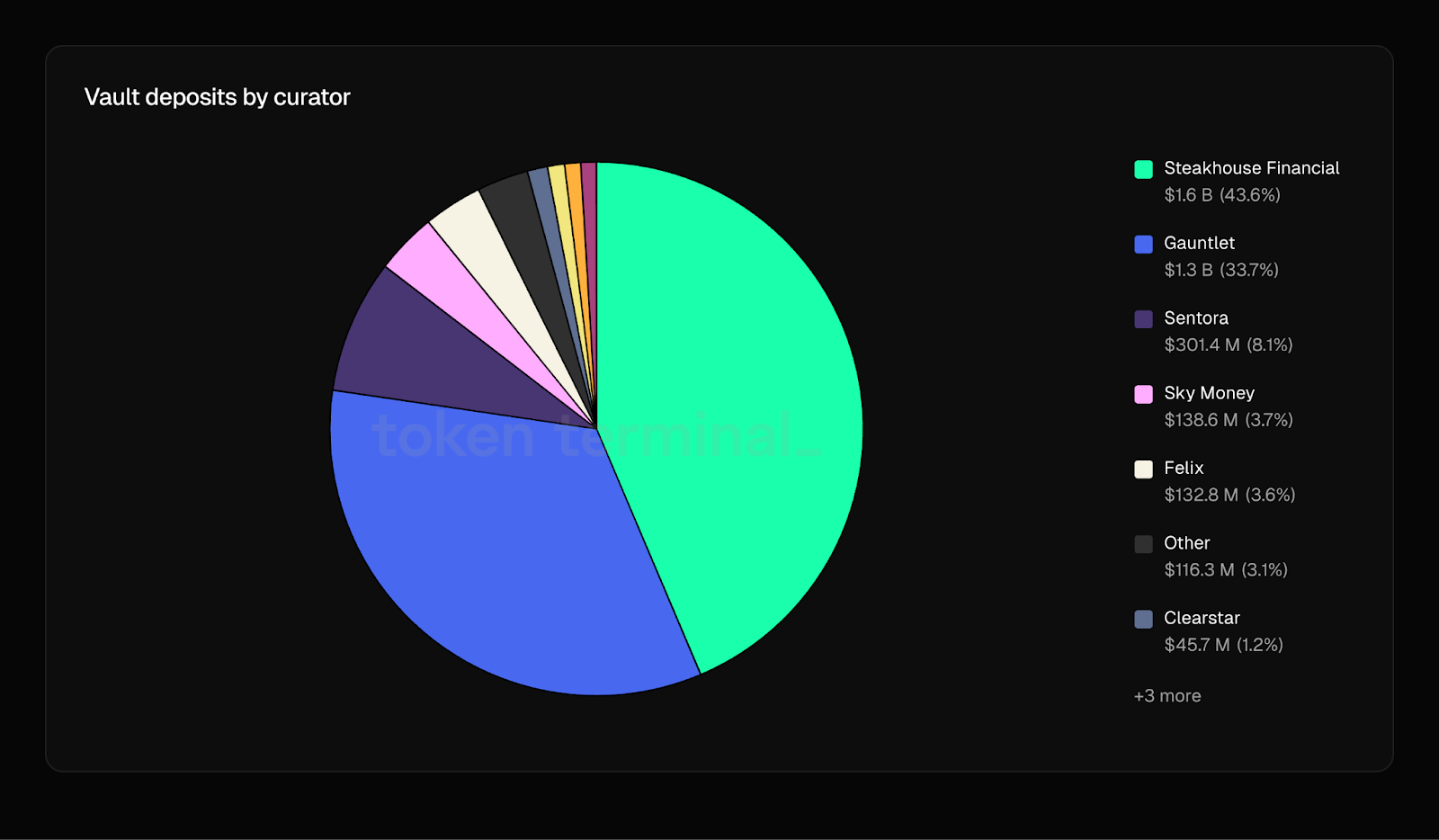

Steakhouse Financial is the largest curator on Morpho, managing over 50 vaults across six chains with roughly $1.5 billion in deposits and the first curator to cross $2 billion in total assets curated on the protocol. Gauntlet runs 70+ vaults with approximately $1.37 billion in AUM.

Steakhouse does it with a team of less than 20 people. This is possible because the underlying network offloads the verification requirements to the blockchain and the system’s openness enables the protocol to rely on companies like Coinbase for distribution and Morpho for code enforcement.

More recently, Bitwise entered as a Morpho curator - a move that matters less for the capital it brings initially and more for what it signals about the stack. Bitwise is a $15 billion off-chain asset manager with existing distribution to institutions. By becoming a curator, it moves vertically through the vault stack, bringing its own capital relationships and compliance credibility to capture value across both curation and distribution layers.

The distribution layer is where this complex plumbing transforms into a consumer product. Platforms with massive reach, like Coinbase, Crypto.com, and Gemini, now route user deposits directly into these curated vaults.

A Coinbase customer depositing USDC into a basic “earn” product is interacting with DeFi infrastructure without realising it. A clean fintech interface in the front, with decentralised infrastructure running in the back.

The capital chains running beneath these simple apps are quite deep.

Consider a retail user on Crypto.com depositing dollars into a yield product. Those dollars flow into a Morpho vault operated by Grove Finance. Grove, in turn, holds $712 million of a tokenised AAA-rated CLO fund brought on-chain by Centrifuge and managed by traditional heavyweight Janus Henderson. The end user earning a 4.82% yield on their stablecoins has no idea their return originates from a Wall Street credit fund.

Every intermediary in that chain adds a specific, necessary layer of specialisation.

Centrifuge handles the legal and technical work of wrapping a traditional credit fund into a token that DeFi protocols can recognize. Grove Finance provides the risk framework and capital allocation strategy, deciding how much exposure to take on a given instrument. Morpho supplies the lending infrastructure - the smart contracts, market parameters, and vault architecture. Crypto.com handles distribution, compliance, and the user interface.

This is a clear example of financial sophistication scaling on open networks, through composable, specialised intermediaries rather than a single institution trying to do everything.

The Demand Source

The three-layer unbundled stack explains how vaults work today. But what led to the $6 billion in inflows last year?

Let’s start with who is actually allocating the capital.

Data suggests that amongst these vault participants, 63% of them are retail users with under $10,000 in their accounts. Notably, these retail users account for just 6 basis points of the actual capital. The real capital comes from whales and institutional players - addresses depositing over $100,000 per transaction - represent 99.2% of the money in automated yield strategies.

These participants include crypto-native funds, DAO treasuries, and family offices. Depositing into the vaults offers them a hands-off, risk-managed way for them to park large cash reserves.

The primary engine behind this institutional capital influx is the massive expansion of stablecoins, and their growing use as savings instruments — therefore generating passive yield.

Over the course of 2025, the stablecoin supply grew from roughly $200 billion to $300 billion. Crucially, regulatory developments like the GENIUS Act are accelerating this growth, but with a specific catch. Under these new frameworks, stablecoin issuers are legally prohibited from paying interest directly to token holders. Since native stablecoins are legally required to yield nothing, that $300 billion is structurally forced to move one layer out into lending protocols to find a return.

Vaults have become the default parking lot for this idle money, which is why over 90% of Morpho and Spark vault AUM (assets under management) is in stablecoins.

Additionally, automated on-chain yield strategies have always been superior in pure yield terms. Today, they deliver an average gross APY of 7.95%, compared to 4.67% for traditional short-duration fixed income and money market funds.

We have sufficient capital that demands yield, and we have enough APY to attract them; the final piece needed was a way of distribution to reach users and institutions who want the returns but won’t interact with DeFi protocols directly.

This is a real barrier. EY’s institutional survey reported that 62% of institutional investors prefer gaining crypto exposure through registered vehicles rather than acquiring assets directly on-chain. Only 24% of surveyed investors currently engage with DeFi at all. The demand for yield exists; the willingness to navigate wallets, smart contracts, and gas fees does not.

On the retail side, another EY report found that 51% of non-DeFi investors cited lack of expertise as their top reason for not participating.

The distribution layer solves this issue by wrapping vault infrastructure inside familiar interfaces. For these users, a Coinbase “earn” button that routes to a Morpho vault in the background removes the barrier entirely.

Coinbase routes USDC deposits through Steakhouse-curated Morpho vaults on Base - the same Steakhouse that now manages over $1.5 billion in deposits. Crypto.com, Gemini, Bitget, Ledger, and Trust Wallet have built similar integrations. For an institution that can’t hold assets in a self-custodial wallet or interact with a smart contract directly, depositing through Coinbase means the compliance, KYC, and custody requirements they need are handled at the interface layer. They get vault yields without vault complexity.

For traditional asset managers, this creates a distribution pipeline to a global audience where the compliance burden sits with the platform and not the protocol.

What stands in the way

While the numbers are compelling, the risks are too.

Smart contract vulnerability remains the most direct threat to this entire ecosystem, and the track record is sobering.

Consider the sheer variety of the wreckage: In 2021, Yearn lost $11 million to a flash loan manipulation. And suffered another $9 million loss in late 2025, from an infinite minting bug. The markets responded accordingly, protocol’s TVL (Total Value Locked) today sits at $250 million, down from its all-time high of $6.3 billion.

A similar fate befell Euler in 2023, where a single missing “health check” in Euler Finance’s code allowed a hacker to drain $197 million across four different asset pools in just fifteen minutes.

The terrifying pattern across these incidents is that almost all of the exploited code had been thoroughly reviewed by top-tier security firms like OpenZeppelin and Trail of Bits. While audits are necessary, they haven’t been sufficient.

Because vaults are composable, every new protocol they plug into creates a new attack vector. The industry has responded by building heavy safeguards - timelocks to delay sudden parameter changes, real-time monitors like Hypernative to spot abnormal flows, automatic circuit breakers, and decentralised veto mechanisms that allow depositors to block suspicious moves.

While these mitigations are meaningful, they are not guarantees. A bug at the protocol layer can wipe out a vault in seconds, regardless of how well the curator allocated the capital.

Other than the security risks of code, there’s another fundamental difference in how the actual financial product behaves differently from traditional fixed income.

DeFi vaults charge meaningfully higher fees - roughly 1.50% compared to the 0.08% you might pay for a Vanguard money market fund.

However, that gap is largely just a reality of scale; a $70 million smart contract cannot amortise operational costs the way a $360 billion Wall Street behemoth can. Yet, even after those higher fees are deducted, on-chain allocators are still taking home roughly 186 basis points more yield than they would in traditional finance (6.45% vs 4.59%).

But as the history of exploits shows, that extra yield is not free alpha; it comes with pre-existing risks. It is the exact, market-priced premium for bearing technical risk. There is no FDIC deposit insurance on-chain. There is no government backstop, and there is no lender of last resort. Allocators demand higher returns precisely to compensate for the very real possibility of an oracle failure or a smart contract bug wiping out their position.

For crypto-native funds, DAO treasuries, and traditional institutions with the right risk appetite, that structural premium remains highly attractive.

How these tensions resolve will shape the next chapter. But the structural advantage that vaults have - the reason they’re scaling faster than any previous onchain financial product -is in the cost of trust.

Traditional asset management adds costs to scale trust between participants. Each layer adds cost that ultimately comes out of investor returns. On verifiable rails, the ledger itself provides that trust layer - continuously, permissionlessly, at near-zero marginal cost.

That’s why Steakhouse can run $1.5 billion with 20 people, why five intermediaries can sit in a single yield chain without eating the return in fees, and why Coinbase can offer vault-powered earn products to 100 million users without building proprietary fund infrastructure.

The risks are real and the regulatory questions are unresolved. But the economics of trust on verifiable networks are structurally different. And if that cost advantage holds, $17.5 billion may turn out to be early.

Until then, stay safe.

Nishil

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.