Hello,

The business of moving money has enough problems to be solved. One such problem is a $2.5 trillion gap in global trade finance. That’s just shy of Brazil’s $2.64 trillion annual GDP, which ranks 10th-largest globally.

The trade finance gap has jumped from $1.5 trillion to $2.5 trillion over the past decade. But what is trade finance? That’s the financing gap in global trade caused by rejected or unmet applications for letters of credit, trade loans, and other financial instruments needed to facilitate international commerce.

Humans have made great strides in improving how the physical world moves goods and services. We have containers that one can scan at a port, track in real-time across oceans and use to deliver things across the globe with minimal logistic issues. Yet we have failed to prevent global trade from grinding to a halt because the financial paperwork moves at a snail’s pace.

A supplier may have the goods, manage to prepare the order for delivery, and still be stuck with the shipment because of insufficient paperwork. The order could get stuck between a stack of unsigned invoices, missing payment instructions, a faulty bill of lading, bank rejections, or settlement delays. The problem compounds if the supplier is a small exporter or a company in an emerging market.

This is the elephant in the room of global trade that XDC Network is addressing.

Anatomy of a Trade

Let me walk you through what a typical cross-border deal looks like. Imagine a textile manufacturer in Manila shipping fabric to a fashion retailer in Rotterdam. What could possibly go wrong?

Everything.

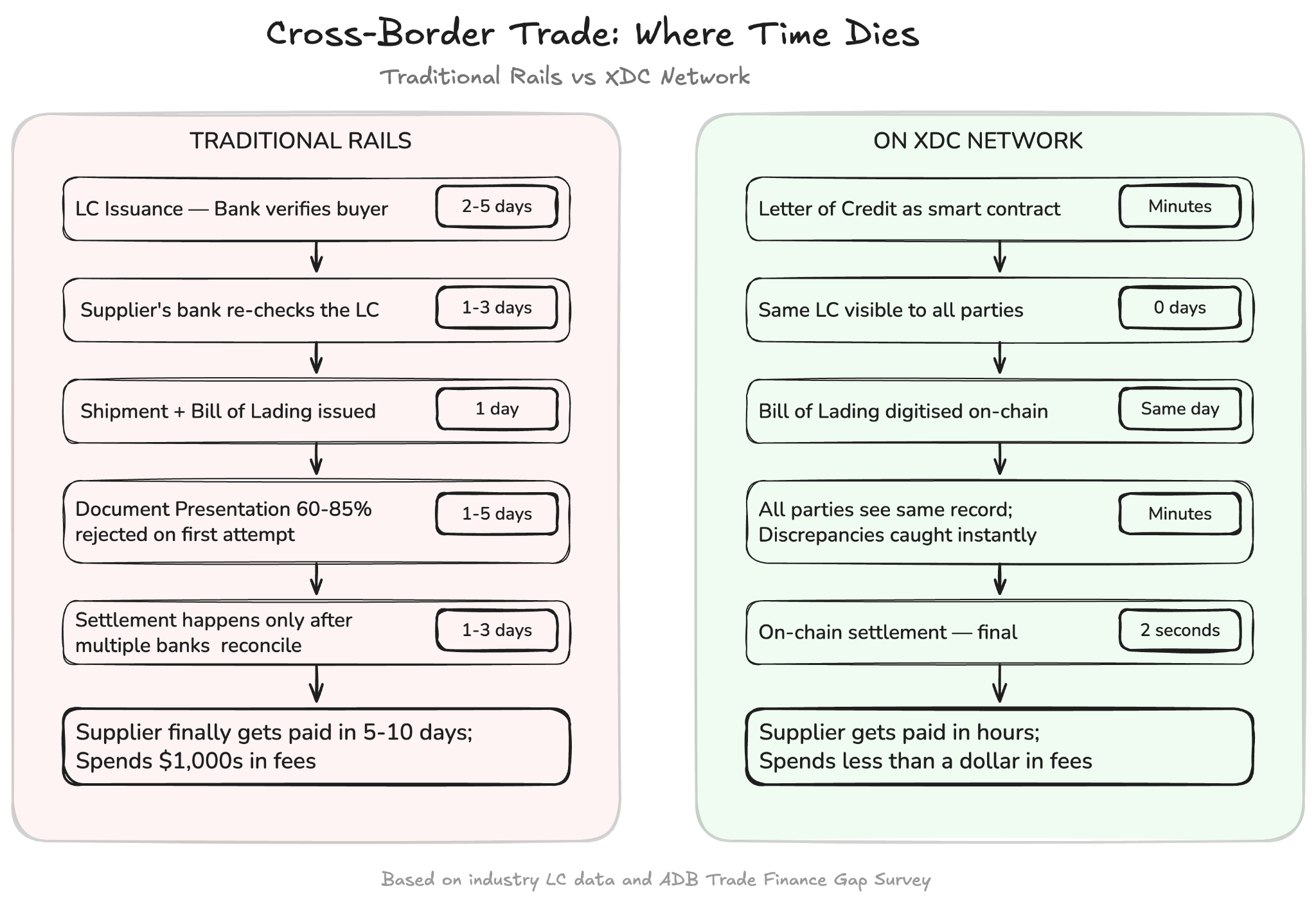

First, there’s the Letter of Credit (LC). The buyer’s bank in Rotterdam must issue an LC, which is a formal guarantee that the buyer can and will pay. Before issuing the LC, the bank verifies the buyer’s creditworthiness, reviews the supplier’s track record, examines the shipping terms, confirms the insurance coverage, and cross-checks the invoice. Documents are prepared, reviewed, signed, and sometimes physically couriered. By the time the LC is opened, two to five days have passed. The fabric hasn’t moved an inch yet.

Next comes the verification of the LC. The LC reaches the supplier’s bank in Manila, which must independently verify the same document. It checks whether the issuing bank in Rotterdam has sufficient credit standing. Are the terms consistent with the underlying trade? More documents, leading to more back-and-forth. Another one to three days gone.

Then the product moves. Finally. The fabric now gets loaded onto a ship. A Bill of Lading (BoL) is issued by the cargo carrier to the supplier, acknowledging receipt of the goods and the conception of a contract of carriage. Now, the supplier’s bank assembles a full document package that includes the invoice, contents of the package, certificate of origin, BoL, and insurance certificate, and presents it to the issuing bank.

Even if a single field doesn’t match, say the invoice says “cotton-polyester blend” and the LC says “cotton blend,” the entire package could get rejected. The supplier has to resubmit. The clock resets. These are not rare incidents. Industry-wide, roughly 60–85% of LC document presentations are rejected on the first attempt because of discrepancies.

Finally comes the settlement. If everything clears, despite or after all the above struggles, the issuing bank releases the payment. So, the settlement could become a painful consequence of four to five separate institutions, each having independently verified the same set of facts through its own siloed systems. The total cycle could range from five to ten days. For an export worth a million dollars, the cost could run into the thousands of dollars (0.5%-2.5%) in correspondent banking charges, SWIFT messaging fees, and FX conversion fees. For a small exporter, these fees alone can eat into the margins of the entire deal.

Now here’s what should make you angry. Nothing in this process failed because of a lack of money, goods, or demand. The buyer wanted the fabric, and the supplier had it packed and ready. Yet, the trade died or got delayed because multiple parties were trying to verify the same facts through separate systems that don’t talk to each other.

That’s a shameful excuse for the human race that has innovated ways to move money with a click in under a couple of seconds.

Multiply this scenario by millions of trades each year across thousands of corridors, and it becomes clear why the gap has only gotten worse over the past decade.

This is where blockchains come in handy. Let’s see how the same trade would move on-chain.

The XDC Bet

XDC Network, an open-source and EVM-compatible Layer 1 blockchain, is built around trade finance, real-world asset (RWA) tokenisation, enterprise applications and cross-border settlement. Ritesh Kakkad and Atul Khekade co-founded XDC Network to simplify trade finance by using a smart contract system. The network tokenises real-world assets like bonds, trade receivables, and trade documents on a low-cost, highly secure, high-speed blockchain. It went live in June 2019 with a 108-validator masternode architecture and has since processed over 1.2 billion on-chain transactions.

On XDC, the letter of credit is tokenised as a smart contract, while the bill of lading is digitised on-chain. Every party, including the buyer’s bank, the supplier’s bank, the shipping company and the insurer, sees the same record at any point in time. When the supplier’s bank in Manila pulls up the LC, it’s the same LC the issuing bank in Rotterdam created. No independent verification is required at either end.

There’s no way a “cotton-polyester blend” discrepancy can creep in. Even if it surfaces, it is rectified within minutes the moment the document is uploaded. There are no three-day review cycles.

Settlement is finalised in 2 seconds, at a cost of 1/1000th of a cent or $0.00001. The textile manufacturer in Manila gets paid within hours rather than waiting weeks in anticipation and hoping. The retailer in Rotterdam gets their shipment on schedule.

You may ask, why XDC? Can’t other generic blockchains do the same?

XDC speaks the language banks understand. It is designed to be compatible with ISO-20022, a messaging standard that banks use to route trillions of cross-border payments through the SWIFT protocol every day. Every letter of credit, payment instruction, and trade document exchanged between a bank and a supplier is ISO 20022-compliant.

Generic chains like Ethereum and Solana carry minimal transaction metadata, which is enough for token swaps or other DeFi activities. Trade finance documents are inherently data-heavy. A letter of credit must include the buyer’s bank, the supplier’s bank, shipping terms, insurance references, port of origin, commodity descriptions, and dozens of other structured fields that a compliance officer must verify before releasing payment. Generic chains are not designed to carry so many metadata fields. Chains like Ripple and Stellar have achieved ISO 20022 compatibility, but through middleware integration. Reliance on external bridges means more points of failure. XDC’s moat is in eliminating the need for a bridge by building the network compliant with the standard from the ground up. This gives them a multi-year head start in terms of architecture.

XDC also acts as a hybrid chain. Through XDC subnets, institutions get the openness and composability of a permissionless network to build and deploy smart contracts and transact freely. But at the same time, XDC mandates that every validator complete KYC with notarised identity documentation visible on-chain.

It’s a hybrid design that no other generic blockchain offers.

Why Trust XDC

Every blockchain has a set of validators who confirm transactions, produce blocks and maintain the ledger. On most chains, these operators are invisible and anonymous wallets. It could even be pseudonymous entities chasing staking yield. If things go south with an exploit on the chain at 2 AM on a Sunday, the only consequence for these validators is loss of a bag of tokens.

In traditional finance, nobody thinks about this. But what if you are a bank or a business evaluating whether to move commercial transactions, including letters of credit and trade receivables worth millions, onto a blockchain? The first thing your compliance team will ask you is for the face that’s backing the new technology.

XDC’s validator lineup is led by SBI Holdings. The Japanese financial giant has joined XDC’s validator ecosystem to expand the latter’s footprint across Asia. German telecom conglomerate Deutsche Telekom is also a validator. Their subsidiary, Telekom MMS, has been running a node on XDC for almost two years.

XDC also has United Overseas Bank (UOB), one of Southeast Asia’s largest banks, as a validator. The bank has deep roots in trade finance across Singapore, Thailand, Malaysia and Indonesia. Do you see the pattern yet? The validator list is not a random aggregation of legacy players. XDC has assembled some of the best players across various domains of expertise that it aims to solve with its blockchain.

It has also backed the legacy line-up of validators with institutions specialising in the digital assets space.

HashKey Group, one of Asia’s largest licensed digital asset managers, is also on the institutional validator list.

What matters more than all the big names is that these businesses are not backing the project for staking reward. The three legacy giants are all regulated entities with balance sheets, boards, compliance departments and reputations that help them stand out far beyond the crypto ecosystem.

The three of them collectively hold close to a trillion dollars in assets on their balance sheets and have a combined market cap of more than $200 billion. It’s a case of deep skin in the game. They back it because they trust the technology to change the way global trade works for the better.

On top of that, XDC has further reinforced the commitment. Every node operator, including the institutions, must lock at least 10 million XDC as collateral, which would be slashed the moment any of them tampers with a transaction or acts against the network’s interests.

So there’s a lot to lose for the validators, given their reputation in the market. But what happens when any of the trade financing documents are falsified on-chain? Let’s go back to the fabric example.

What if the supplier in Manila signs off on inaccurate information on the bill of lading? What if they inflate the shipment quantity, or claim goods were loaded when they weren’t? On-chain, anonymous validators could confirm the falsified document like any other transaction. There’s no recourse beyond the protocol. On XDC, the validators confirming transactions are KYC-verified institutions, like UOB and SBI Holdings. They operate under the same regulatory frameworks as the banks on either side of a traditional cross-border trade.

So, these validators have a lot at stake beyond the 10 million XDC that they have parked as collateral.

For XDC, having this kind of line-up adds to their credibility. The due diligence the early validators conducted before backing XDC serves as de facto business development for the incoming validators.

The traders using tokenised trade finance infrastructure will probably never know XDC exists. They might not even care. But if the institutions and banks they’ve long partnered with are on the validator list, that trust will follow here.

You cannot ask institutions to move real commercial transactions on-chain and then ask them to trust anonymous infrastructure. “The validator set we have built on XDC is our answer to that,” says Atul Khekade, Co-founder, XDC Network

But what has all this institutional backing translated into? Valid ask.

What’s Live on XDC?

In late 2025, XDC’s venture arm acquired Contour Network, a blockchain-based letter-of-credit (LC) platform that was originally backed by HSBC, Citi, Standard Chartered, BNP Paribas, and DBS.

Contour had already proven the concept worked, cutting LC processing times from 5-10 days down to a matter of hours. XDC acquired the platform in 2023, injected capital, and is rebuilding it as an end-to-end digital trade finance platform with stablecoin-based settlement. The acquisition brings a battle-tested LC infrastructure onto XDC’s rails, accelerating its ability to move letters of credit, the documents that guarantee trade deals between banks, on-chain at scale.

In April 2025, Brazilian fintech firm LIQI said it would tokenise $500 million in real-world assets on XDC, including private credit, corporate debt, and receivables, by the end of 2026. In Dubai, ComTech Gold uses XDC Network to issue CGO, a token backed one-to-one by physical gold stored in TransGuard vaults, with a Sharia compliance certification that opens the door to the Islamic finance market.

In February this year, VERT Capital, a leader in the Brazilian structured finance space, tokenised two major Brazilian debentures - Mottu and Banco Pine on XDC Network. They aim to tokenise $1 billion in assets on the network by the end of 2026.

Where Does XDC Go From Here?

The crypto ecosystem originally aimed to remove trust entirely and let code handle everything. But the masses won’t adopt something that’s on the other extreme of the binarised world. Trust still matters to institutions and their customers, who probably would want nothing to do with blockchain or crypto.

XDC lets you see who is running the infrastructure. You can verify the KYC documentation for validators, trace their stake, and check their on-chain uptime. The protocol penalty is just one part of ensuring accountability. But with a line-up like this, the institutions bear accountability through their balance sheets, regulators, and reputations.

The $2.5 trillion trade finance gap has persisted for decades. In fact, it has only gotten worse in the past decade. That’s because the technology to move trade documents as fast and cost-effectively as we moved containers didn’t exist. But now it does. If that textile manufacturer in Manila can get paid in hours and not weeks, then the $2.5 trillion gap begins to close gradually.

That’s it for today. I will be back with another one soon.

Until then, stay curious.

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter is sponsored by XDC Network. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.

The biggest risk to Global Trade, at present is eroding trust. Extensive blockchain roll out will help to shore up a pillar (confidence in the financial payment system).