How the Internet Happened - 2

Everyone got rich. Then everyone got poor. Then Google showed up.

Part two of three. Last week: Netscape, Bill Gates’s blind spot, and why the browser was the moment everything changed. Today, Amazon builds a bookstore in a garage, eBay teaches strangers to trust each other, and then the whole thing loses its mind.

My favourite thing about the dot-com crash is that Bernie Madoff was one of the voices warning people it had gone too far. In late 1998, he said publicly: “It defies my imagination that so many people with so little sophistication are speculating on these stocks.” Bernie Madoff. Telling people to be careful with their money.

That’s the era we’re in this week. The part of the internet story that the “we’re in the Netscape moment” crowd leaves out. Let’s go.

In the spring of 1994, a twenty-eight-year-old named Jeff Bezos was the youngest-ever senior vice president at a Wall Street hedge fund. One of his jobs was to identify business opportunities on the internet. He came across a data point that stopped him cold: the amount of data transmitted over the web had grown by 205,700% in a single year. As Bezos later said, “Things just don’t grow this fast outside of petri dishes.”

He quit his job. He and his wife, MacKenzie, packed up their car and drove to Seattle, Bezos typing up a business plan on his laptop as they went. The company they founded in the garage of a rented house in Bellevue, Washington, would become Amazon. The original address was 10704 N.E. 28th Street. The domain was registered on November 1, 1994.

Bezos had thought carefully about what to sell first. He considered software, office supplies, and CDs. He landed on books because they were pure commodities: a copy of a book in one store was identical to the same book anywhere else, so buyers always knew what they were getting. There were also three million book titles in print worldwide, but no single store could stock them all. An online store could. “With that huge diversity of products,” Bezos said, “you could build a store online that simply could not exist in any other way.”

Amazon’s full website launched on July 16, 1995. In the first week, it took in $12,438 in orders and managed to ship $846 worth. The rest was a backlog. Early customers sometimes phoned in their credit card numbers rather than enter them online, not trusting the web. Others simply emailed them, “as if that was somehow more secure,” one early employee recalled. Credit card numbers were recorded on one computer, copied to a floppy disc, physically carried to a second computer, and processed in batches. This was known inside Amazon as a sneakernet.

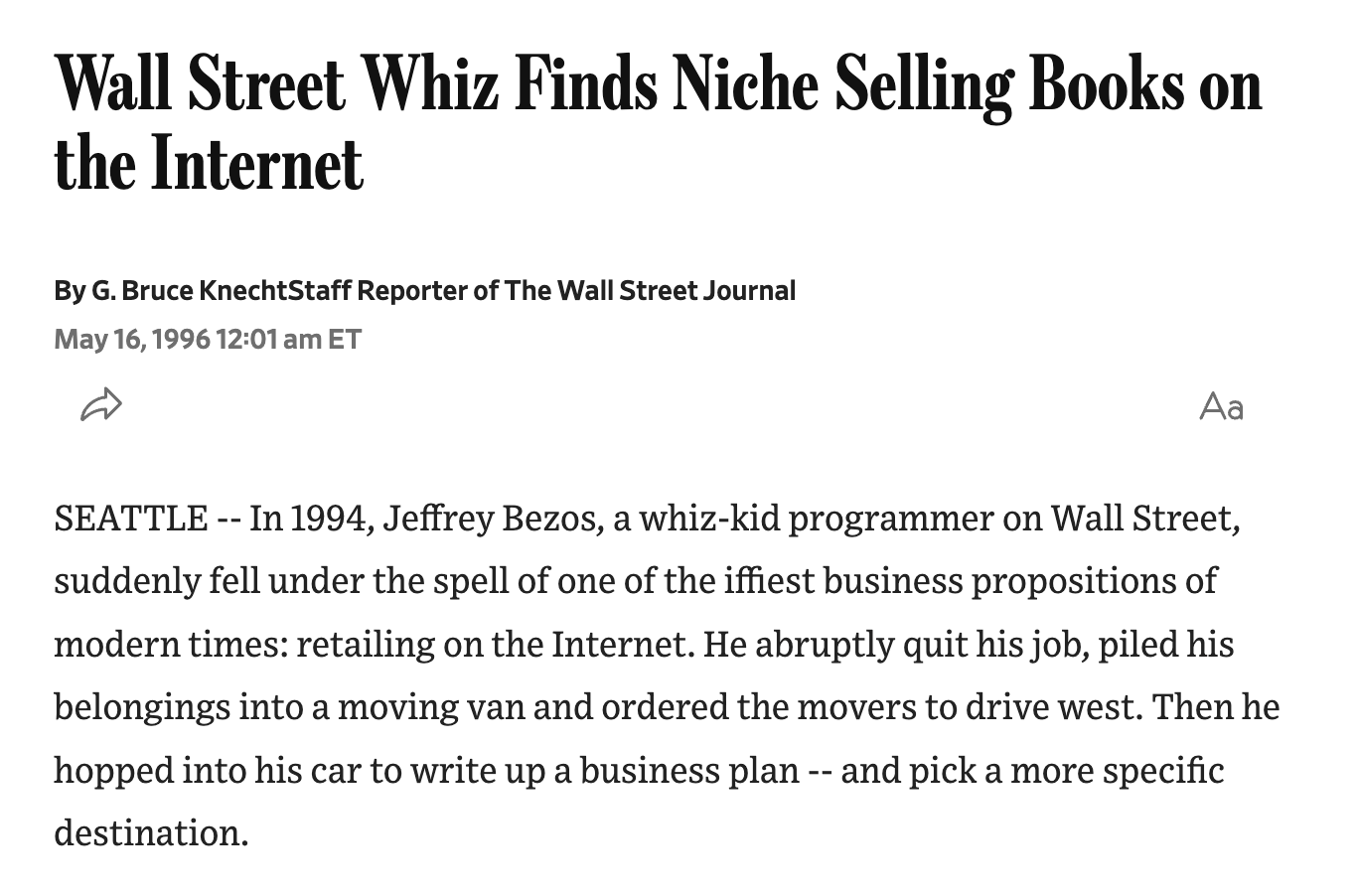

By October, Amazon had its first hundred-order day. By 1996, it was recording 900% revenue growth. And then the Wall Street Journal put Bezos on the front page under the headline “Wall Street Whiz Finds Niche Selling Books on the Internet.” Overnight, Amazon went from experiment to standard-bearer. Kleiner Perkins invested $8 million. John Doerr joined the board.

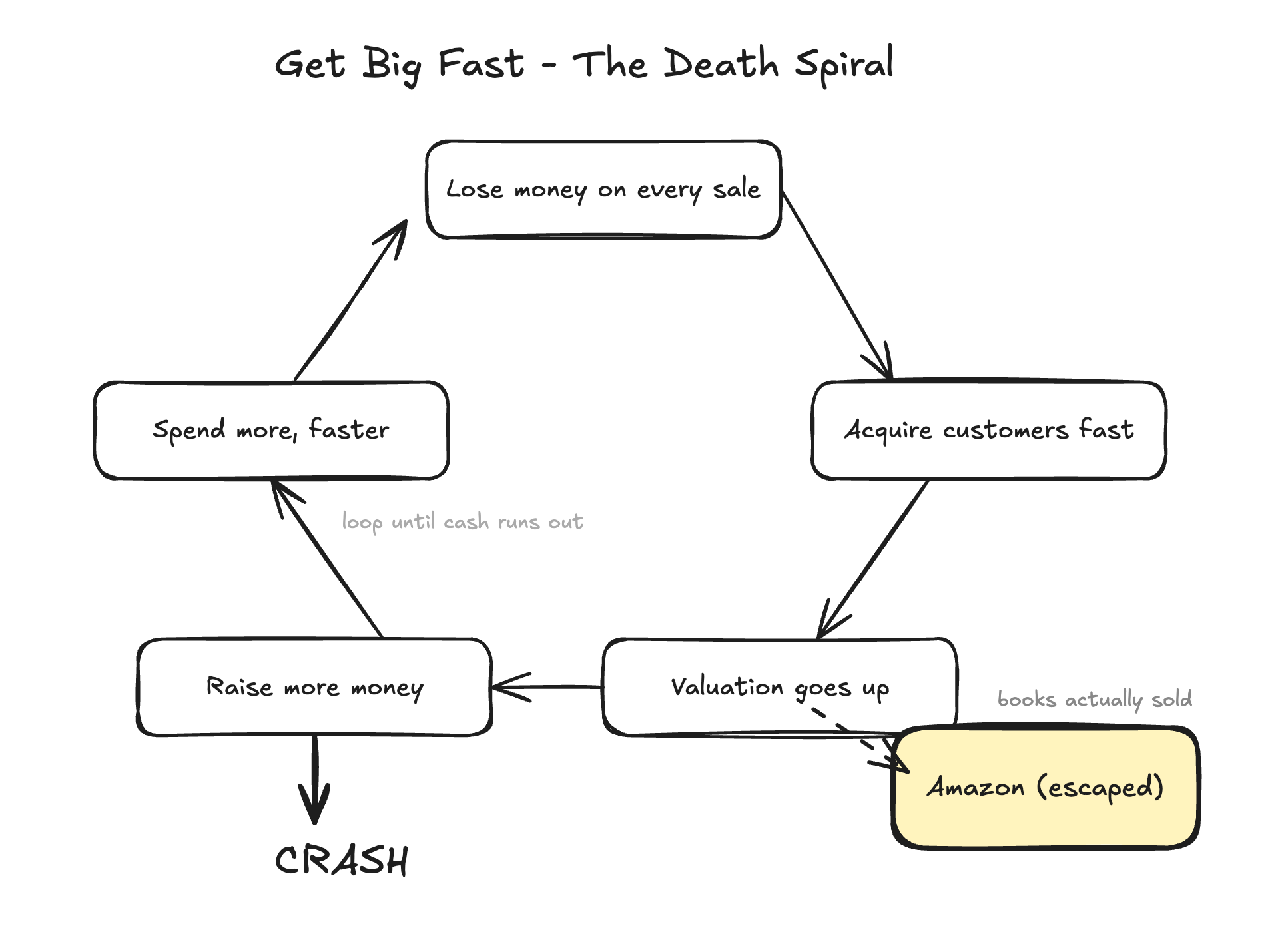

A new motto started circulating inside the company. Netscape had coined the phrase, and Amazon turned it into a religion: Get Big Fast.

If you think about it, every DeFi protocol that launched between 2020 and 2022 was running some version of Get Big Fast. Subsidise users with token rewards, acquire market share, worry about sustainable economics later. Some of those protocols are still here, but a lot of them aren’t. Amazon survived Get Big Fast because Bezos had actually thought about what he was building. People wanted to buy books online. The books were actually worth selling. The thing Bezos was really testing in that garage was whether the internet made something possible that wasn’t possible before. That’s still the only test that matters, in everything you build.

While Bezos was building a bookstore, a French-Iranian programmer named Pierre Omidyar was running a small experiment on the side. He had built an online auction site called AuctionWeb mostly out of curiosity, just to see if the internet could create a decent market for secondhand stuff. He hosted it on his personal webpage, next to his resume. He started charging tiny listing fees because his ISP was threatening to move him to a business account, and he needed to cover the cost.

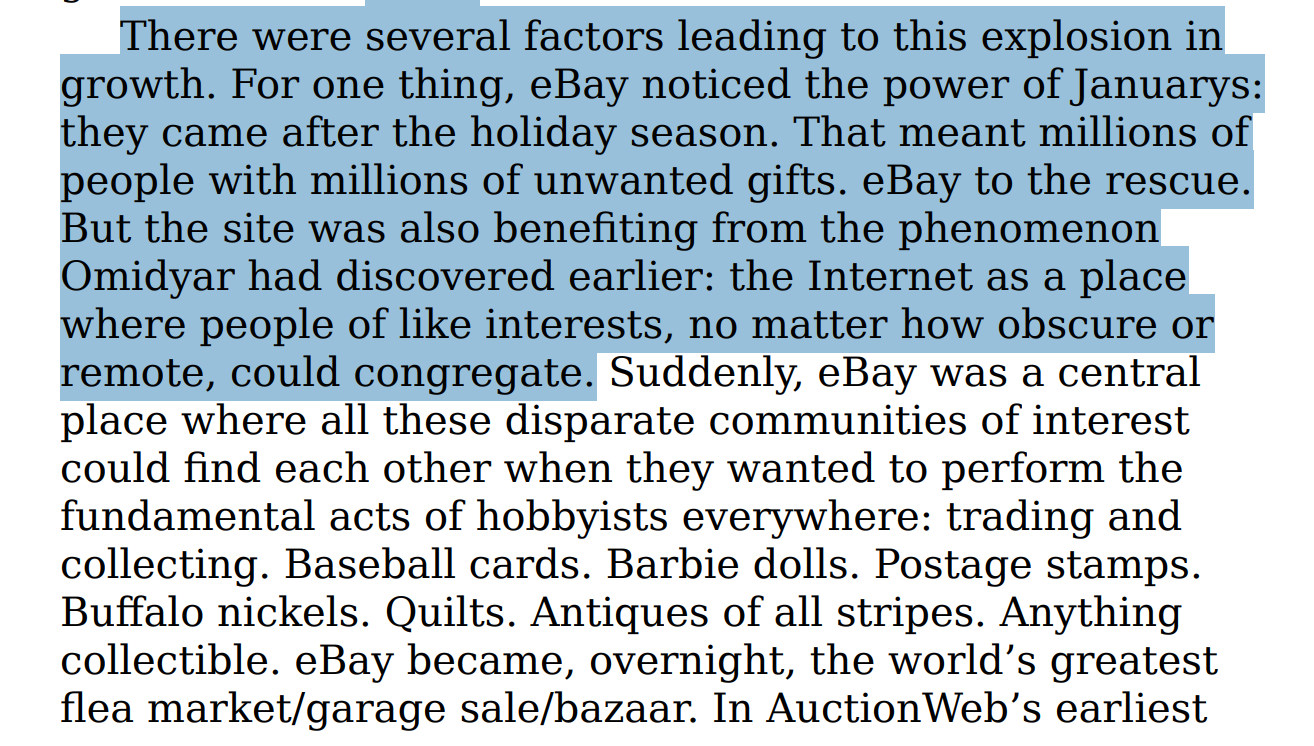

The fees covered the cost. Then they exceeded it. Within a few months, AuctionWeb was making Omidyar more money than his actual job. He eventually renamed it eBay.

What made eBay work? Buying something online from a stranger you would never meet was a deeply weird idea in 1996. What stopped fraud, what kept the whole thing from collapsing into a scam, was a feedback rating system. Buyers rated sellers, sellers rated buyers, and a number accumulated next to your username over time. A seller with a +847 rating had completed 847 transactions that ended with a satisfied buyer. That number became a reputation, and on eBay, reputation was worth more than anything being sold. McCullough is right to linger on this. The feedback rating system is one of the most quietly important inventions of the internet era. Uber, Airbnb, every marketplace that exists today is running a version of Pierre Omidyar’s experiment. The sharing economy is built on the premise that a stranger with a good reputation score is trustworthy enough to get into a car with or sleep in their apartment. That idea did not exist before eBay.

In crypto, the trust problem was solved differently, and it’s not through reputation, but through code. Smart contracts removed the need to trust the counterparty at all. You trusted the protocol, not the person. This is a more radical solution than eBay’s, and in some ways more elegant. But it created its own problem: people trusted the protocol without understanding it, and the protocol, as we’ve seen many times, did exactly what it was coded to do rather than what people thought it was coded to do. The bugs in early eBay could be patched. The bugs in an immutable smart contract on a Tuesday afternoon in 2022 could not.

By 1998, eBay was growing at 1,200% annually. Benchmark Capital had paid $5 million for a 21.5% stake in the company. That $5 million eventually turned into $4 billion.

Now we are in 1998, and something is changing in the atmosphere. It’s hard to describe how irrational things got, but McCullough makes an attempt here. In 1995, seven internet companies held IPOs. In 1996, twenty-seven. In 1999, two hundred and forty-nine. The market was losing its mind about the Internet. The companies being taken public in 1999 were, in many cases, barely companies at all. Pets.com launched in February 1999 and went public in February 2000 (12 months later), having lost more than $61 million on revenues of $5.7 million. The cost of the goods sold was $13.4 million. It was losing 57 cents on every dollar of revenue. It was selling heavy bags of pet food by mail and charging $5 for shipping when the actual shipping cost was closer to $10.

The company’s biggest expense was advertising. Pets.com had a sock puppet. You might remember the sock puppet. The sock puppet was a talking dog-like creature that appeared in a $2 million Super Bowl ad, a Macy’s Thanksgiving Day Parade float, and a spread in Entertainment Weekly. The puppet became a licensed toy. In a single quarter, Pets.com spent $17 million promoting the sock puppet and brought in $8.8 million in total revenue.

Pets.com was valued at hundreds of millions of dollars. It was out of business within a year of its IPO.

Crypto people reading this should be having flashbacks. The 2021 bull run had its own sock puppets, which were celebrity NFT endorsements from people who barely knew what a blockchain was, Super Bowl ads for exchanges, and stadium naming rights. The difference is that some of the crypto technology worked. The crash sorted out which projects had something underneath them and which were running on narrative. That is exactly what 1999 did too.

The mania had a specific structure. Lose money to acquire customers. Acquire customers to justify your valuation. Use your valuation to raise more money. Use that money to lose more, faster, to acquire even more customers. The assumption underneath it all was that once you owned your category, you could flip the switch to profitability. Amazon was doing this. The problem was that most of these companies were not Amazon. They were burning capital to fight for markets that would never be as big as they imagined, selling products at prices that could never be raised high enough to be profitable, and trusting that somehow the switch would flip.

“We’re in an environment where the company doesn’t have to be successful for us to make money,” one Benchmark VC admitted to McCullough.

When your investors are saying that out loud, you are at the top.

The 2021 DeFi and NFT cycle followed the same structure. Protocols subsidised users with token emissions. Lose money on every transaction to acquire liquidity, use liquidity to justify TVL, use TVL to raise the next round. The assumption was that once you owned your category, you could wind down the emissions and keep the users. Most couldn’t. The users were there for the yield, not the product. When the yield stopped, they left. Same switch. Same problem. It never flipped.

The crash, when it came, was not dramatic in the way crashes appear dramatic in retrospect. The Nasdaq peaked in March 2000. It fell 78% from peak to trough. Two and a half trillion dollars in market value evaporated. Pets.com shut down in November 2000, nine months after its IPO. Webvan, the grocery delivery startup that had raised $400 million and built 330,000-square-foot warehouses before establishing whether anyone actually wanted the product, filed for bankruptcy in 2001. Kozmo.com, the instant-delivery service that sent bike couriers to bring you a pint of Ben & Jerry’s at below cost, was gone. EToys. Furniture.com, which had learned too late that you cannot ship a couch by UPS. The tech press started calling it the nuclear winter.

AOL and Time Warner announced the largest merger in corporate history in January 2000, valuing the combined company at $350 billion. It was, in hindsight, the single worst merger of the era. AOL used its inflated stock to buy a real media company weeks before that stock became worthless. The deal that was supposed to represent the internet's conquest of old media instead became a tombstone for both.

Yeah..yeah.. Three arrows, FTX, Luna, leverage on leverage, I remember too, the only problem was why the heck did I not buy BTC at $16k?

But here is what McCullough is building toward, and it is the most important takeaway for us. The nuclear winter killed sock puppets, but it did not kill the internet. While the Nasdaq was falling, venture capital was drying up, and the media was writing the obituary of the dot-com dream, two things were happening. Across a series of server rooms, a search engine built by two Stanford PhD students was improving at an astonishing rate. And a nineteen-year-old college student named Shawn Fanning was about to break the internet open in a completely different way. What the crash did was clear the noise. What was left underneath was Google and Napster.

Part three is where it gets good again. Until then, stay extremely hopeful.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.