The easiest way to control someone’s money is to wait for them to look away.

That’s how financial companies make a good amount of money purely off your procrastination.

Two economists, Richard Thaler and Shlomo Benartzi, figured out years ago that convincing people is a waste of time. Instead of trying too hard on winning arguments; you change people’s behaviour by rigging what happens when a human does precisely nothing. “opt-out” link is apparently a tough one to press on.

When companies make people manually fill out a form to save for retirement, barely half do it. Flip the default so they have to manually opt out, and participation instantly clears 90%. It’s the same story with subscriptions. Over 50% of people paying for auto-renewing apps don’t even use them. The subscription I took last week to watch FIFA WC, which I am completely sure I will forget forever, after the game.

The catch in this system is that a default only works when the person whose money it is and the person who picks the fund are two different people. Your employer picks the 401(k) menu, and you just land in it.

On June 18, Franklin Templeton filed for two ETFs designed to wire that default into bitcoin

In the grand scheme of things, the “capital flow moat” is tiny.

Deciding to buy Bitcoin is one of the big barriers to adoption. We almost overcome it when Trump says hi at Bitcoin conferences, but the barrier still stays after all.

Somebody has to choose to hold it, defend that choice to a client or a compliance desk, and eat the downside when it cracks in half. For an advisor who is career risk, most of them route around it and never put it in front of you.

An advisor builds a model portfolio. They pick the funds, and the client holds whatever got slotted in. The client opens the statement, sees “US large-cap equity, 40%,” and doesn’t bother with the holdings underneath. If the advisor used the DRIP version, that client now owns Bitcoin. The client inherited the choice without noticing one had been made.

But they aren’t trying to trick you, the retail buyer, into being lazy. They know you actively look at your portfolio. Instead, they built this infrastructure for your financial advisor.

That is the trick, and it is the same one that built the $4 trillion target-date pile. The default becomes the product, and the product wins by being the thing you get when you do nothing. The DIY buyer who typed the ticker is the one person this doesn’t describe, and Franklin doesn’t need them. The money these funds want sits downstream of someone else’s click.

A dividend reinvestment plan is the most set-and-forget thing in all of investing. Your stock pays you a dividend, and instead of the cash coming into your account, it buys you more of the same stock. You compound deeper into what you already hold and hardly think about it. That is a DRIP.

Franklin just flipped it. The two funds, the Franklin US Equity Bitcoin DRIP Index ETF and the Franklin US Innovation Bitcoin DRIP Index ETF, take the dividends your stocks pay and use them to buy Bitcoin (not more stock).

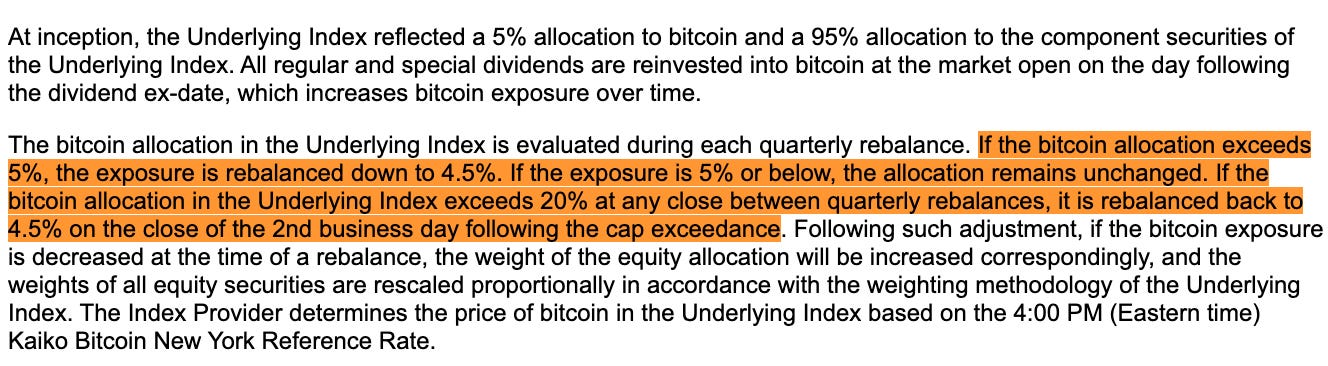

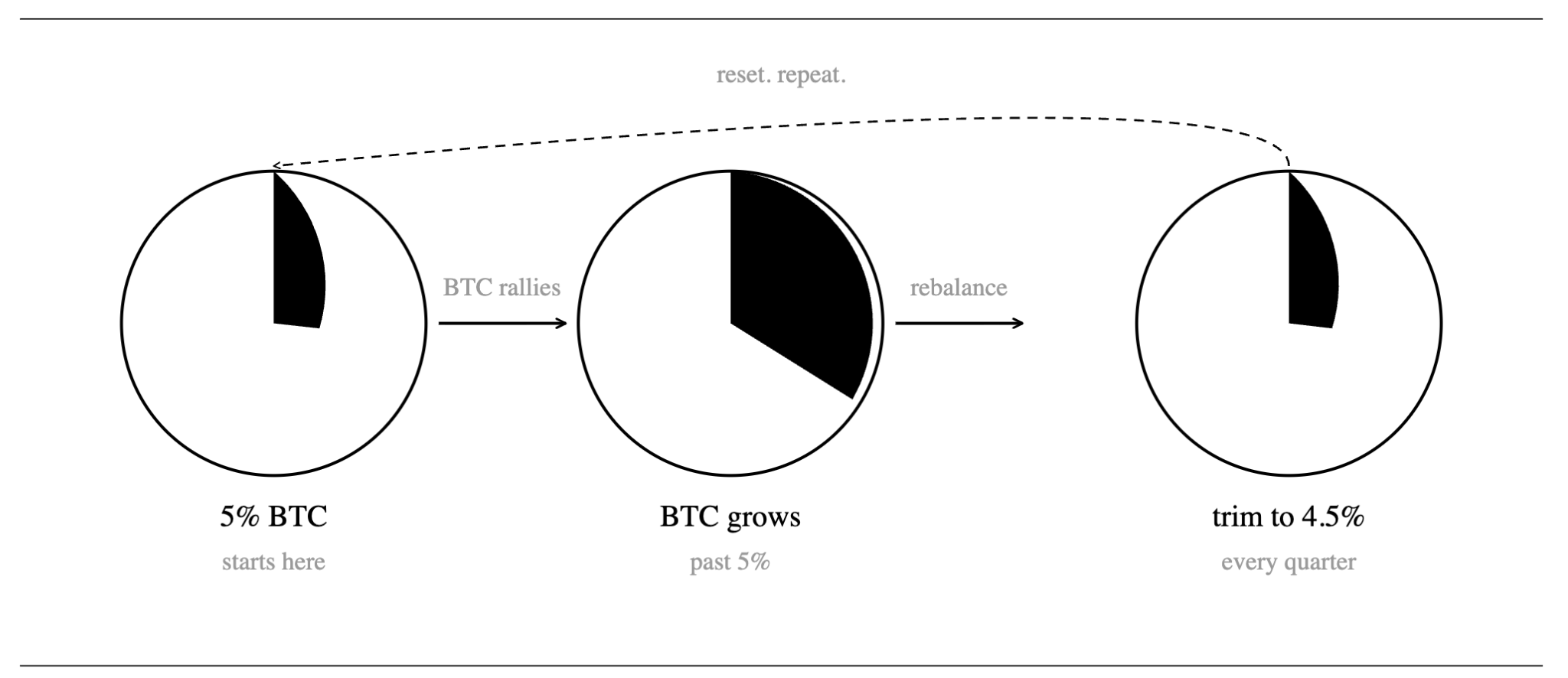

For the Bitcoin allocation itself, the funds plan to use spot Bitcoin ETFs, futures, and options. Franklin built in a quarterly rebalancing mechanism with asymmetric rules. If Bitcoin rallies hard and its weighting drifts above the 5% target, the fund trims it back to 4.5% at the next quarterly rebalance. There’s also a hard cap at 20% Bitcoin allocation.

So the Bitcoin portion starts at 5%. Every quarter, dividends flow in and are used to buy more Bitcoin. If the Bitcoin price goes up and Bitcoin becomes a bigger percentage of the fund, they trim it back down to 4.5% at rebalancing. The excess goes back to the equity side.

The maximum Bitcoin can ever be is 20% of the fund. Even if Bitcoin goes completely parabolic between rebalancing dates.

To bypass a bunch of regulatory red tape, the actual coins are tucked away in a Cayman Islands subsidiary that Franklin owns, which buys a mix of spot crypto, futures, or options.

The whole thing tracks specialised indexes built by a firm called VettaFi, and Franklin is aiming to launch them on September 1. We don’t know how expensive they’ll be yet, because they left the fee section blank on the paperwork.

Now I stop selling you the dream. A new buyer, hardcoded into Wall Street’s plumbing, sounds enormous.

Run the real numbers, and the bid turns into a drip.

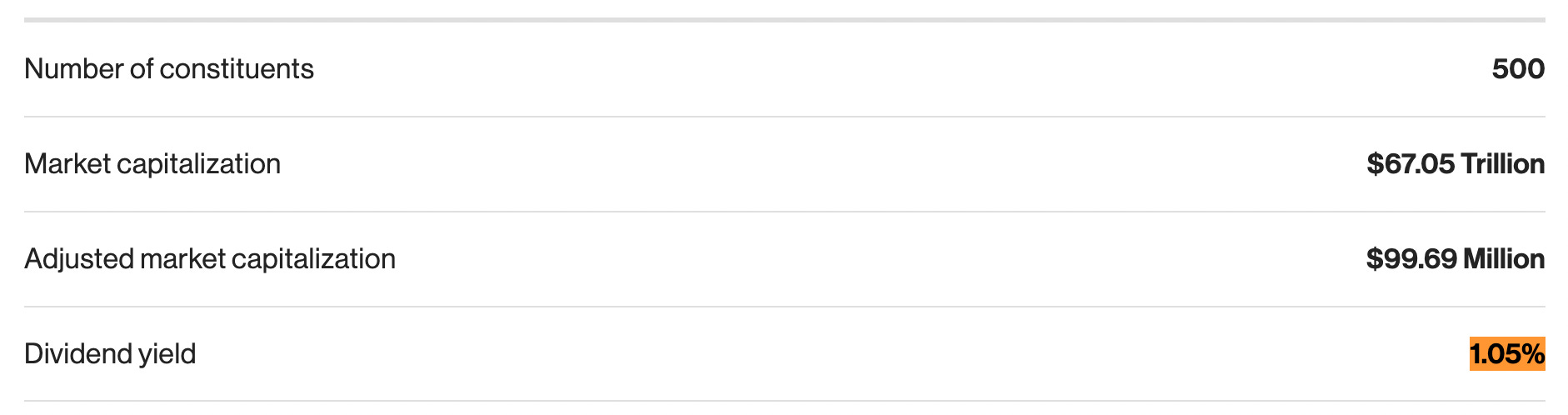

The broad fund tracks an index yielding 1.05% a year. The innovation fund tracks one yielding 0.52%. Both start at 95% stocks and 5% bitcoin, and only the dividends from that stock sleeve get turned into bitcoin. So the broad fund converts about 1% of its assets into bitcoin a year. The innovation one around half a per cent.

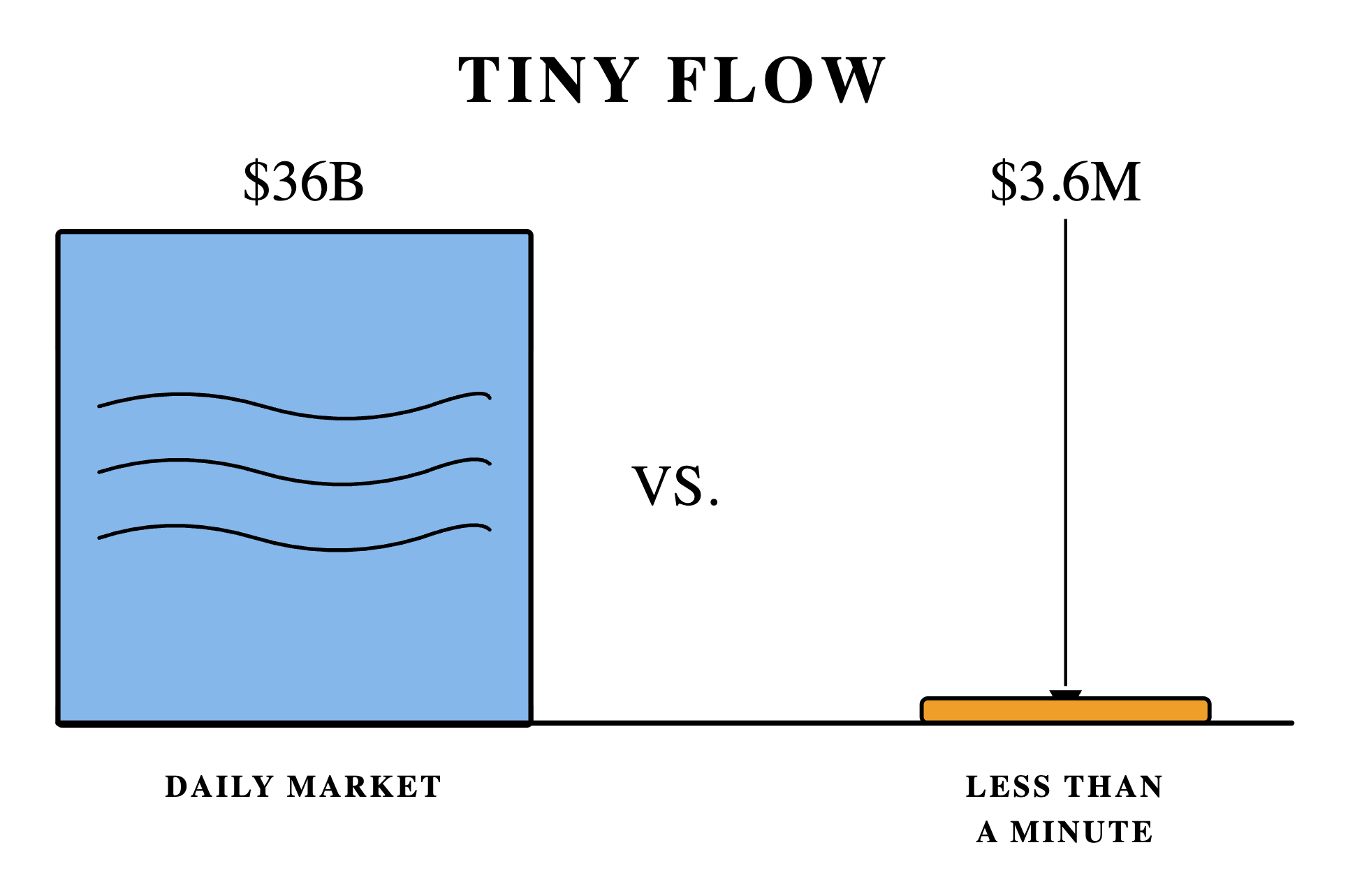

These funds haven’t launched, so use Franklin’s existing bitcoin ETF as the yardstick. It holds about $359 million. One per cent of that is ~$3.6 million of bitcoin buying spread across a whole year. Bitcoin trades tens of billions of dollars a day, around $36 billion. At that rate, the market chews through a full year of this fund’s buying in under a minute.

The innovation fund is the joke inside the joke. Its largest holdings are Nvidia, Apple, and Microsoft, names that pay tiny dividends or none at all. Since the fund relies on those dividends to buy bitcoin, it has almost no fuel to work with. Then the rebalance turns the engine backwards. Bitcoin gets trimmed back to 4.5% every time it grows past 5% at the quarterly reset. So the better Bitcoin does, the more the fund sells. In a real market rally, that constant selling will easily wipe out any gains the tiny trickle of buying managed to create. It is built to keep you from ever actually holding onto a winner.

On a good day for Bitcoin, this fund turns into a forced seller.

How? Index funds have been forced on buyers. Traders make a fortune front-running them because everyone knows exactly what stocks the index has to buy and when. Franklin’s new funds create the opposite problem of a forced, automated seller. Because the fund must buy bitcoin the morning after a dividend and sell it at every quarterly rebalance, any fast trader can step in front of the fund and squeeze it for a profit on both ends.

One fund this size is a mosquito; a whole category of them is weather. Get enough of this capital in one place, and you create a ceiling that presses down on bitcoin every time it rallies.

Apart from the default trick, the filing leaves a few smaller ones open, too.

The mandate dodge - An advisor whose rulebook bans crypto can still drop a client into a fund labelled US large-cap equity.

The offshore wrapper - The bitcoin sits in a wholly owned Cayman Islands subsidiary, the standard rig for holding a commodity-type asset inside a regular fund without breaking its tax status. Legal, and common.

And the tax wrinkle- If a dividend turns into bitcoin before it ever reaches you, you owe the money, but the fund already locked it up in crypto. To pay the tax bill, you are forced to dig into your own pocket and find outside cash to cover a dividend you did not hold.

For all of this to work, A fund like this has to become a default, or sit right next to one. In 2006, the Pension Protection Act gave employers legal cover to enrol workers automatically and have them in a default fund.

Back then, only 5% of 401(k) plans offered a target-date fund. Today, 96% do, and total assets exploded from $100 billion to $4 trillion.

In August 2025, an executive order was issued by Trump that formally opened the way for cryptocurrencies to be used in 401 (k) s. Then, in March 2026, the Department of Labour published an administrative proposal giving fiduciary services liability protection for putting alternative assets such as cryptocurrencies on their plan menus.

The period for submitting comments on this proposal was closed as of June 1, which means that if a final administrative rule is to be issued prior to calendar year-end, it must be done before then. Creating a default alternative investment (target-type funds) is more difficult than creating alternative investments for participants with funds in which they have something invested; thus, regardless of the content of this new administrative rule, corporate attorneys believe that most employers will continue to “wait and see” until a court allows them to proceed under the proposed safe harbour.

None of this runs on convincing anyone. Human attention is the scarcest resource on earth, and whatever automates the friction of thinking wins.

The system just needs your inertia.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.