Jupiter’s Black Box

Rise of private market makers

Once upon a time, all we cared about was typing in SOL, picking USDC, and hitting swap. Good old days. If you got a better price - that’s all that mattered.

Times have changed now; things are getting serious. The market is shifting away from hobby projects toward professional, institutional systems. Wall Street firms are flocking in for the infra, while retail is no longer a big fan. Now, I want to know exactly how we got that better price and who is on the other side of my order?

We need that collective suspicion if we are ever going to build a better or more permanent place for crypto in the fintech world.

You think you are trading in a public market when you buy or sell a stock, but you are really in a private network. Modern retail apps use a controversial routing system that started in the 1980s, when Bernie Madoff, a pioneer in electronic trading, became the first major user. Madoff discovered that if he paid legal kickbacks to retail brokerages, they would provide his private firm with early access to their client orders before those orders reached an open exchange.

This setup let one private company operate between the trader and the public ledger, taking a tiny share of the spread on each transaction.

The original idea behind crypto was to create a system where this kind of centralised middleman cannot exist.

The main rule of decentralised finance was supposed to be transparency, meaning everything happens out in the open. But over the last year, Solana has built a completely different system.

Jupiter is the main hub for trading on Solana. Lately, the engine behind all these trades has changed. It now runs on private, secret trading pools. This piece is about the hidden black box inside the Solana trading market.

Early AMMs were transparent. They were just a pool of two tokens with an open math formula, and anyone could check GitHub to see exactly how their money was handled. If you traded on Raydium or Orca, you were basically using a machine built out of glass.

A prop AMM is not that. Here, the prices come from a server. The server is owned by a private company. The contract on Solana is a completely hollow wrapper. Its only job is to act as a gateway, passing your trade directly to an off-chain server where a private firm’s algorithm handles the execution. “Prop” is short for proprietary, which means they refuse to tell you how they make money.

A year ago, this would have been a strange thing to build. Today, it dominates Solana spot trading.

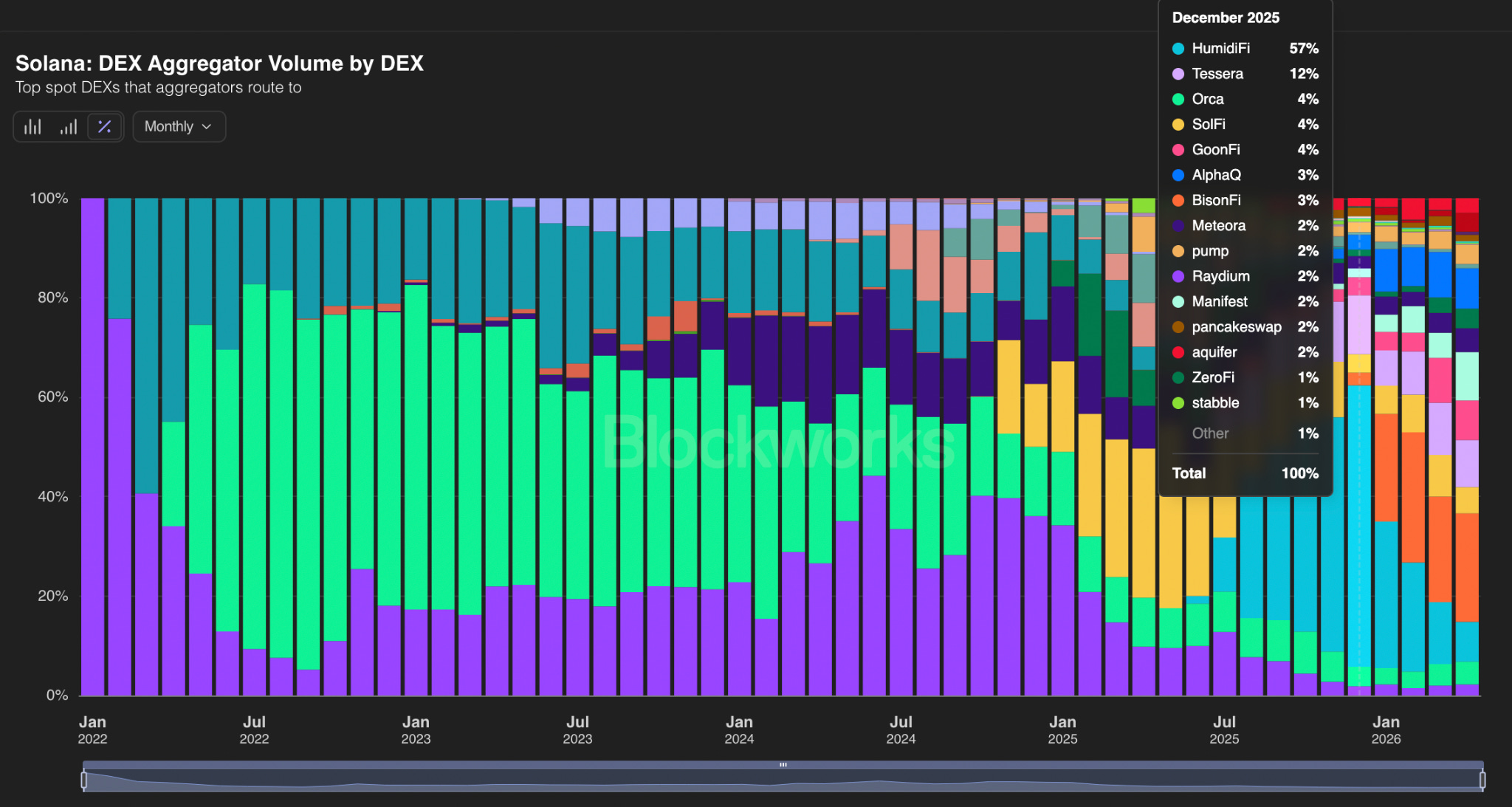

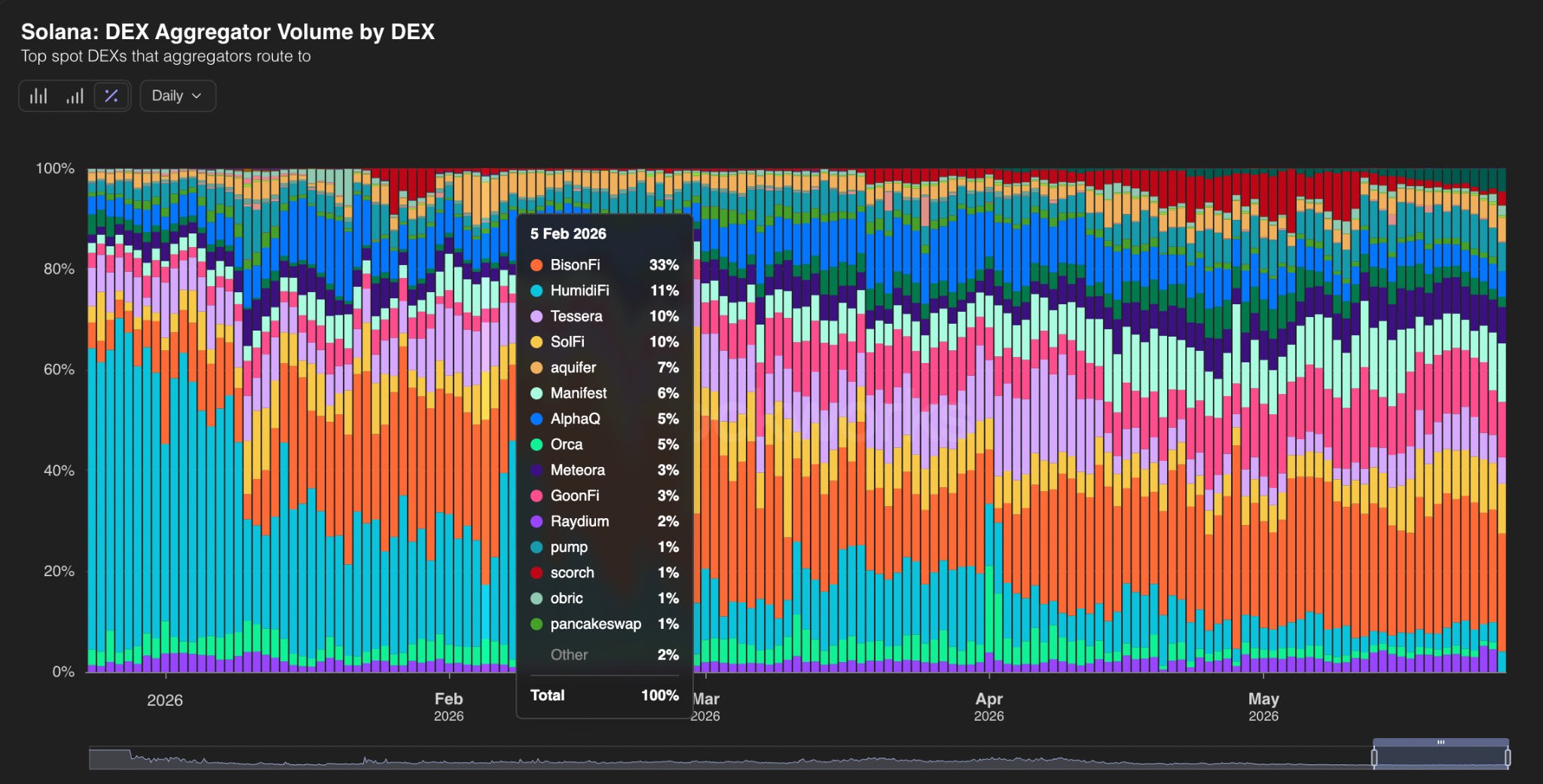

HumidiFi launched in June 2025. By December 2025, HumidiFi alone routed 57% of all Solana aggregator volume. Raydium dropped to 2%. Orca held 5%. Tessera sat at 12%. By late January 2026, the entire prop AMM category accounted for about 92% of Jupiter’s routing.

Jupiter itself processes about 75 - 80% of all Solana aggregator volume, so once the prop AMMs took Jupiter, they had effectively taken Solana spot trading.

The reason is the spread, which is just the hidden fee you pay a market maker to execute your trade. In finance, these costs are measured in basis points, where one basis point is a tiny fraction of a per cent. Even on a standard trade, those fractions add up fast. According to dune, private programs like HumidiFi and Tessera offer very thin spreads.

Using a public pool instead of a private market maker means you pay much more to swap your tokens. The private options are too cheap to ignore. In fact, Jump Research found that most regular trades on these private platforms get a better price than you would find on big exchanges like Binance or Coinbase.

Who is actually running this? TesseraV is Wintermute. The same Wintermute that has made markets across Binance and Coinbase for half a decade.

SolFi is Ellipsis Labs, a Paradigm-backed quant shop. HumidiFi is Temporal, the firm behind a meaningful slice of Solana’s MEV infrastructure. Each one is a professional trading desk, and they have general counsel, compliance, and Bloomberg terminals.

In the venues from which these firms came, they had to register with the SEC. Rules against trading ahead of customer flow. Surveillance for spoofing. Algorithms reviewed. The whole apparatus of the US market structure exists to keep them honest.

Because Citadel pays Robinhood seven hundred million a year, and nobody can prove that’s bad for you, but it sure doesn’t feel good.

On Solana, none of that applies. The same firms run the same trading they always did, with no exchange operator and no securities regulator. The order flow reaches them through an aggregator that handles over 90% of Solana’s aggregator volume.

The anonymous-DeFi framing gets this fact wrong. These are well-known professional trading firms that moved here because there are fewer rules.

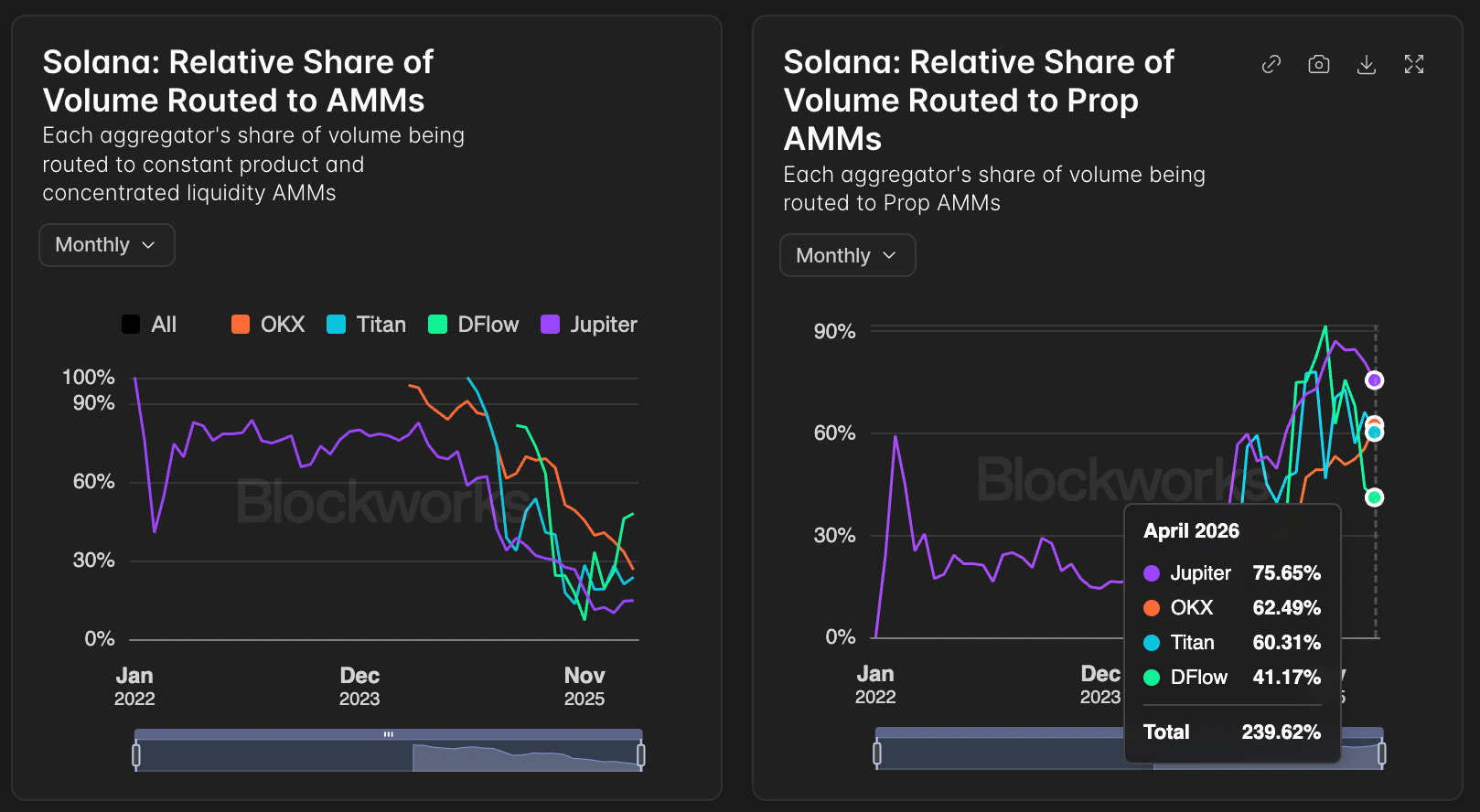

Who Owns the Top Spot?

A market that gives somebody a 68% share in five months and takes most of it back in another thirty days has something strange in its DNA. HumidiFi held 68% of prop AMM volume through December 2025. Thirty days later it was at 26%. The reason was just that a competitor just quoted tighter.

Between January 10 and 13 of 2026, HumidiFi’s daily volume dropped 80% with no public explanation.

BisonFi was already waiting. Within three weeks BisonFi’s daily volume went from around $180 million to $1.43 billion. Its 7-day total hit $11.5 billion.

By early February, BisonFi held 34 to 35% of prop AMM routing while HumidiFi held 26%. The lead ran until today.

The competitor is BisonFi, announced in late 2025 by Forward Industries, the publicly traded company chaired by Multicoin’s Kyle Samani. Then, sometime between the volume takeoff, Forward issued a statement that BisonFi is “not an initiative of theirs.” The website domain is currently listed for sale. Strange how the top spot on Solana’s largest order-flow market is harder to identify than the one it displaced.

Nobody in this market owns anything. Jupiter runs an auction every block, asking who is quoting tightest right now, this millisecond, and sends the trade there. The system rewards getting your quote to the true mid-price faster than others. Maybe two dozen firms worldwide have the setup for that. They will be replaced by another quant shop in a few weeks.

On January 28, DFlow, Solana’s second-largest DEX aggregator, stopped routing to HumidiFi. The founder claimed it was maintenance. HumidiFi’s on-chain contracts kept running. However, there was an impact on volume, and users whose trades had been routed through HumidiFi for months received no notice. Jupiter redirected the flow elsewhere.

Jupiter is a company. It has a treasury, a token, employees, and a P&L. Every swap touching the router pays a fee. Ultra mode pays more. JUP holders get a slice. The aggregator’s value proposition is best execution on Solana, and a huge percentage of aggregator volume comes through it because the proposition holds.

Jupiter has absolutely no incentive to push back on the fact that closed-source private firms fill half of Solana’s spot trades. Pushing back means worse fills, less volume, and less revenue for everyone involved. If you pull the proprietary AMMs out, Jupiter still runs, but it gets clunkier. Your trades take a heavier hit on slippage, split-second prices start to disappear, and the whole ecosystem completely loses its edge.

The risks we are talking about never materialised. People think that it’s proof that they will never. And that’s how every concentration risk in financial history is defended.

Look at the famous collapse of Long-Term Capital Management in 1998. The fund was run by elite Wall Street quants who used top-secret mathematical models to swallow risk and print effortless profits. For years, their private black boxes worked flawlessly, convincing the entire market that the risk had been mathematically eliminated. But the moment an unpredictable global crisis hit, their hidden formulas broke, their private liquidity vanished instantly, and the entire apparatus collapsed in days.

If a pricing bug exists inside a private program in Jupiter, the public only finds out after the capital is gone. When a high-severity flaw was found in Raydium’s open-source code, the patch happened completely in the open. At the same time, a similar flaw inside a proprietary AMM stays entirely in the dark.

Traditional market makers are subject to strict legal rules against trading ahead of customer orders - front-running. On Solana, private desks control their own quote streams and decide when to step away. Because of how Solana orders transactions, one cannot prove these desks are trading against their own users. Outsiders have no way to confirm they aren’t.

Yet, the ecosystem accepts this risk. Why? Open-source math pools work fine for basic crypto tokens, but they break completely if you try to trade real-world assets like US stocks or foreign currencies on-chain. If a smart contract tries to price a tokenised share of Apple stock using only a simple, passive formula, high-frequency traders will exploit the time delays and drain the pool instantly.

Prop AMMs fix this by moving the complicated risk math off-chain. Private servers continuously feed ultra-fast price updates to their custom Solana programs, allowing them to adjust to real-world news and open the door for Wall Street assets to safely move on-chain. But this creates a massive single point of failure. If a private company’s server goes down, bugs out, or feeds incorrect data during a market panic, the liquidity vanishes, and the entire on-chain market for that asset instantly freezes.

We were told the rule of DeFi was that you could read the code.

The interface still says that your trade was routed through TesseraV or SolFi. But that is Wintermute and Ellipsis Labs, pricing your swap.

But they aren’t the only ones playing this game. The architecture is shifting toward an entire ecosystem of private, multi-firm networks. Look at platforms like Bebop, which plugs straight into twelve to fifteen different private market makers to source quotes behind the scenes. Or look at silent protocols like Lifinity, ZeroFi, and Obric — opaque “dark AMMs” that have no public website, no marketing, and no community channels. They exist purely as code snippets plugged into Jupiter to capture your order flow. Traditional trading desks like Wincent are constantly competing in these hidden auctions.

I am not arguing that anyone has been wronged here. In so many ways, Wintermute is a better counterparty than the median memecoin pool. PropAMMs make the broader market healthy by squeezing spreads down to almost zero. Maybe this is how an industry grows up.

The beauty of crypto is that if you are a decentralisation purist who hates the idea of private code, you can easily bypass the aggregators and swap your tokens directly on a public, glass-box pool.

But the massive market share of these private networks proves that most people just want the cheapest possible trade.

We spent years criticising traditional finance for being an opaque, private playground run by Wall Street algorithms. Yet, when given a completely blank slate, the crypto market naturally built the exact same thing because it is faster, cheaper, and more efficient.

Ultimately, you have to choose which fight matters to you.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.