Hello,

I came across this guy, Robert, on Reddit a while back. He is 49, works at a construction company in Houston, and sends $300 every two weeks to his parents in Puebla. They spend it on groceries and rent. Every other Friday, he walks into a Western Union, fills out the form, pays cash, and sends the money. He’s been doing this for nine years, and he doesn’t even know what a stablecoin is.

LATAM’s remittance market hit $174 billion in 2025. And the biggest finding from Bybit’s six-month, five-country on-the-ground research was that most fintechs chasing this market are building for the wrong corridor, the wrong user, and the wrong product entirely.

So I went deep into the corridor data and the on-the-ground research, and the picture looks very different.

Building for the Wrong Corridor

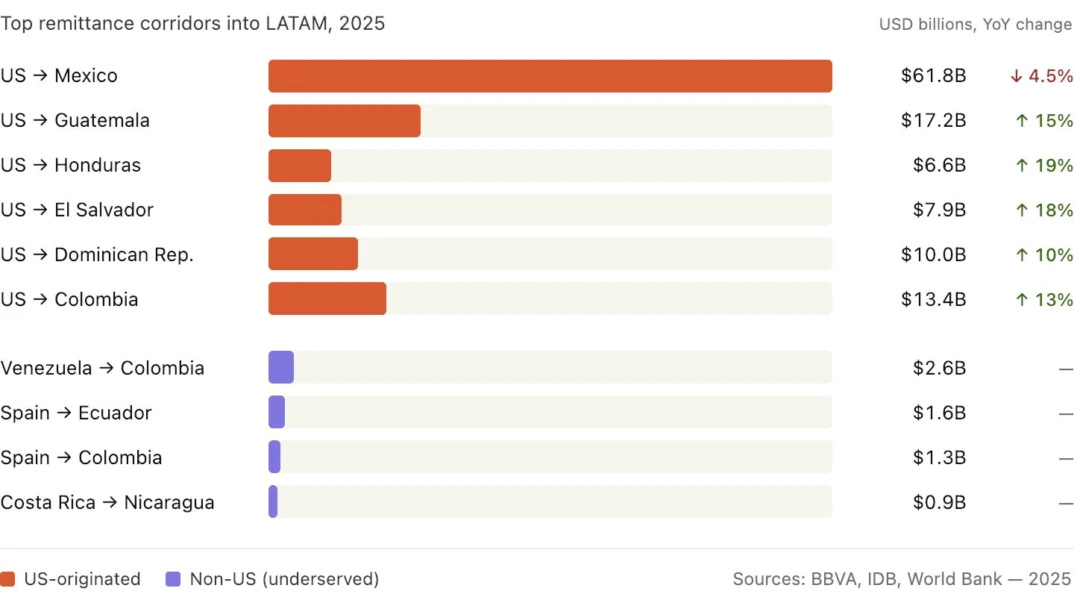

The first thing every fintech gets wrong about LATAM is treating it as one market. It’s not. It can look like one in a pitch deck, because fintech startups can throw a $174B TAM number on a slide and just circle all of Latin America. But on the ground, it’s three completely different remittance markets that operate in distinct ways.

Mexico is the most mature corridor and the entry gate: $62 billion a year, the biggest single flow in the Western Hemisphere. Mexico has SPEI, one of the best instant bank transfer systems anywhere in the world. It has a 37-million-strong diaspora in the US, many of whom have been there for decades, and it has the cleanest regulatory environment, the deepest data, and the most partnerships. So naturally, this is where every fintech and crypto startup builds first.

It’s also the corridor that just started shrinking for the first time in 11 years.

Everyone’s blaming Trump for this, but the decline started in November 2023, 20 months before any crackdowns. The guys like Robert who’ve been sending money for a decade are aging out; their kids grew up in Houston and don’t have the same connection to Puebla; and new Mexican migration has slowed to a trickle, even as 3.5 million people have come from everywhere else in LATAM. Every mature diaspora goes through this. The Italians did, the Irish did, the Greeks did. Mexico is entering that same phase now.

By contrast, Central America is growing fast. Honduras: up 25.3%; Guatemala: 18.7%; El Salvador: 17.9% YoY. But look at what’s driving it. Migrants from these countries are afraid of deportation, so they’re sending 27% more money per transfer than last year. Women are picking up extra shifts, men are taking second jobs, families are pulling from savings, and pushing as much money across the border as they can while they still can.

These are also countries where remittances make up 30% of GDP in Honduras, 27% in El Salvador, and 21% in Guatemala. These countries have built their entire consumer economy around the assumption that this money will keep flowing in, from local prices and labor markets to spending patterns. Think of it like the Gulf states and oil revenue. When inflows swing 20% in a single year, it rewires everything downstream.

And the infrastructure here is almost nonexistent compared to Mexico. No SPEI equivalent, very few digital payment rails, and 45% of senders still pay cash. Even in Mexico, where 99% of remittances move electronically, 51% of recipients still receive the money in cash. The sending side went digital years ago. The families collecting the money on the other end are still walking to a cash window.

South America is a completely different game. Argentina, Colombia, Venezuela. I’ll get into these in the next section because they’re more about access to dollars than remittances.

All these non-Mexico corridors add up to roughly $112 billion a year. Venezuela-to-Colombia alone is an estimated $2.6 billion. That corridor has been running on P2P stablecoin swaps over WhatsApp for years now because when the banking system completely collapsed, people just built their own rails. Fintechs spent the last five years piling into Mexico’s $62 billion corridor right as it started to plateau, while $112 billion in actively growing corridors have almost no one seriously building for them.

The Product Isn’t The Transfer

The second thing fintechs get wrong is their understanding of the actual product. Every crypto pitch for LATAM remittances is about making the transfer better: faster, cheaper, and on stablecoin rails instead of SWIFT. But the transfer is the least interesting part of the whole chain. Robert doesn’t use Western Union because the transfer is good. He picked it because he walked past one on the way home from work nine years ago, and it worked, so he kept going back. The product decision is happening at the edges. How the sender initiates the transfer and what the receiver does with the money once it arrives, and almost nobody is building for those two moments.

Felix Pago is a good case study for the sending side. They processed over $1 billion last year, serving 300,000 migrants, entirely through WhatsApp, without an app, wallet, or onboarding. All you do is text a number; a chatbot responds in the kind of Spanish your tío actually speaks; you pay through a link; and in under 60 seconds, the money lands in a bank account in Mexico.

Under the hood, it runs on USDC through Stellar and Bitso, but the sender never sees any of that. Felix cut fees from $4.98 to $2.99. And it still made more revenue per transaction at the lower price because stablecoin settlement killed the pre-funded correspondent bank accounts that companies like Western Union burn millions maintaining. The users who adopted the fastest were millennial women and older men who live on WhatsApp. Felix won by meeting users where they already were, not by building better rails.

Then there’s the receiving side, where the much bigger product lives, and it has nothing to do with remittances. The biggest takeaway from Bybit’s six months on the ground was that LATAM users don’t want to use stablecoins to move money. They want to hold dollars. The balance is the product, not the transactions.

In Argentina, the peso has lost 97% of its value against the dollar since 2018, inflation hit 211%, and the government capped official dollar purchases at $200 a month. So people started buying USDT through WhatsApp groups at a 30% premium just to get their savings out of pesos. Over 70% of all crypto purchases in Argentina are USDC and USDT, with Bitcoin at just 8%, because people there primarily want to hold onto the value of their paychecks.

Lemon Cash capitalised on this and grew from under 10,000 users to over 2 million in two years by letting people convert their paycheck into USDC the second they get paid, hold it there, and only convert back to pesos when they swipe their Visa card at the grocery store. By providing a functional dollar savings account that the domestic banking system lacks, stablecoin circulation in Argentina has grown to $11 billion, representing more than 27% of the nation’s M1 money supply.

Similarly, in Colombia, banks require a $5,000 minimum to open a USD account, which the average Colombian worker will never have. Stablecoins are the only way most Colombians can hold dollars, and 52% of all crypto bought in the country now goes into stablecoins because the banking system has priced them out of the one financial product they actually need.

Brazil has a completely different problem. The real is stable enough that Brazilians don’t need access to dollars the way Argentines and Colombians do, and PIX already processed $4.5 trillion in 2024, making it one of the world’s most advanced instant payment systems. But what Brazil actually wants from stablecoins is better settlement infrastructure on top of their own currency. BRLA, a real-backed stablecoin plugged directly into PIX, went from near zero to $400 million a month in volume by early 2026, and Brazil’s central bank says 90% of all crypto volume in the country is stablecoin-related.

Argentina needs dollar savings. Colombia needs dollar access. Brazil needs settlement infrastructure. The product that wins in one country would fail in the other two, and building for all three at once is how you build for none of them.

Who Actually Wins This

If fintechs are chasing the wrong corridor and building the wrong product, the obvious question is: who wins in LATAM remittances? And the honest answer is that nobody has it figured out yet, but you can already see which pieces matter and who has them.

Western Union lost almost half its US-to-LAC market share in four years, dropping from 29% to 16.8%, and responded by buying Intermex for $500 million and rushing to build its own stablecoin, USDP. That’s a company that knows the ground is shifting but is too slow to do anything except copy the people eating its lunch.

Remitly grew from 14% to 22.7% over the same period simply by being a better digital transfer product, but they still don’t have a wallet, a card, or any way for the receiver to hold dollars. Bitso processes 10% of the entire US-Mexico corridor on stablecoin rails. But they’re a crypto exchange, and crypto exchanges don’t have local payment integrations or the kind of UX that works for someone like Robert.

The winner needs to own both sides of the transaction: the sending experience that Felix proved works through WhatsApp, and the dollar balance that Lemon proved people will use as their primary savings account. On top of that, they need local payment rails like SPEI, PIX, and PSE, a card so users can spend without converting, and a yield layer so the dollar balance earns while it sits. All of that needs to work on a $150 Android phone for someone who has never opened a crypto app. That’s an entire financial stack, and the only realistic way to build it is to build it one corridor at a time.

The regulatory landscape matters here, too. Brazil just classified stablecoin transactions as foreign exchange under three new central bank resolutions and set minimum capital requirements between $2 million and $6.9 million for crypto firms. Mexico’s 2018 FinTech Law still confines virtual asset activities to licensed institutions with prior central bank authorization, and approvals remain scarce.

Both are hard markets to crack from day one. Colombia and Argentina are the opposite, with lighter compliance, regulatory sandboxes, and more room to build and iterate. The common mistake is starting with Brazil because it’s the biggest market, but it’s also the hardest to enter. The smarter play is to win Colombia and Argentina first, where the product is dollar savings and dollar access, nail the underlying stack, the card infrastructure, the local payment integrations, and then bring that operational playbook to Brazil, where the product changes to settlement infrastructure but the plumbing underneath stays the same.

The Bigger Picture

Last summer, the US passed the One Big Beautiful Bill Act, which includes a 1% federal tax on cash remittances. About half of all LATAM senders still use cash agents, and digital and crypto transfers are largely exempt from this. So Robert, walking into a Western Union every two weeks, is about to start paying more for doing things the way he always has. At the same time, Felix’s WhatsApp transfers and Mexico’s OXXO SPIN wallets cost him nothing extra.

The average cost to send a remittance to LATAM is still around 6%, and in some corridors, such as Paraguay, it’s nearly 12%. Crypto rails compress that to under 2%. For someone sending $300 every two weeks, that difference amounts to roughly a month’s worth of groceries saved per year for his family back home.

The race in LATAM is about who owns the balance that Robert trusts enough to keep his family’s grocery money in. Whoever owns that balance owns LATAM fintech.

That’s it for today. See you next week.

Until then, stay curious,

Vaidik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.