Meet Me at the Agorá

Why megabanks are double-dipping on public blockchains

The original agora was a public square in Athens, several thousand years ago. Anyone could show up, and anyone could trade. The agora had no membership requirements or jurisdictional controls. It was permissionless by design, and that’s where the word comes from.

The BIS chose the name intentionally, or maybe not. It’s hard to tell.

Project Agorá, the experiment the Bank for International Settlements just completed with seven central banks and over 40 private institutions, is almost the opposite of what the word suggests.

A system where money knows which country it belongs to before it moves. Smart contracts enforce AML checks and sanctions screening at the token level. Each central bank keeps full control over its own reserves, and no cross-border movement happens without passing through the compliance layer embedded in the token itself.

Programmable money that asks permission first.

The seven central banks are: the Federal Reserve Bank of New York, the Bank of England, the Bank of Japan, the Bank of Korea, the Bank of Mexico, the Swiss National Bank, and the Banque de France, representing the Eurozone. The Bank of Canada just joined four days ago.

The project includes major financial giants such as JPMorgan, HSBC, Deutsche Bank, UBS, Mastercard, Visa, and SWIFT, as well as more than 40 other firms.

It’s a massive amount of institutional firepower for a single project, and that’s why I decided to sit with it.

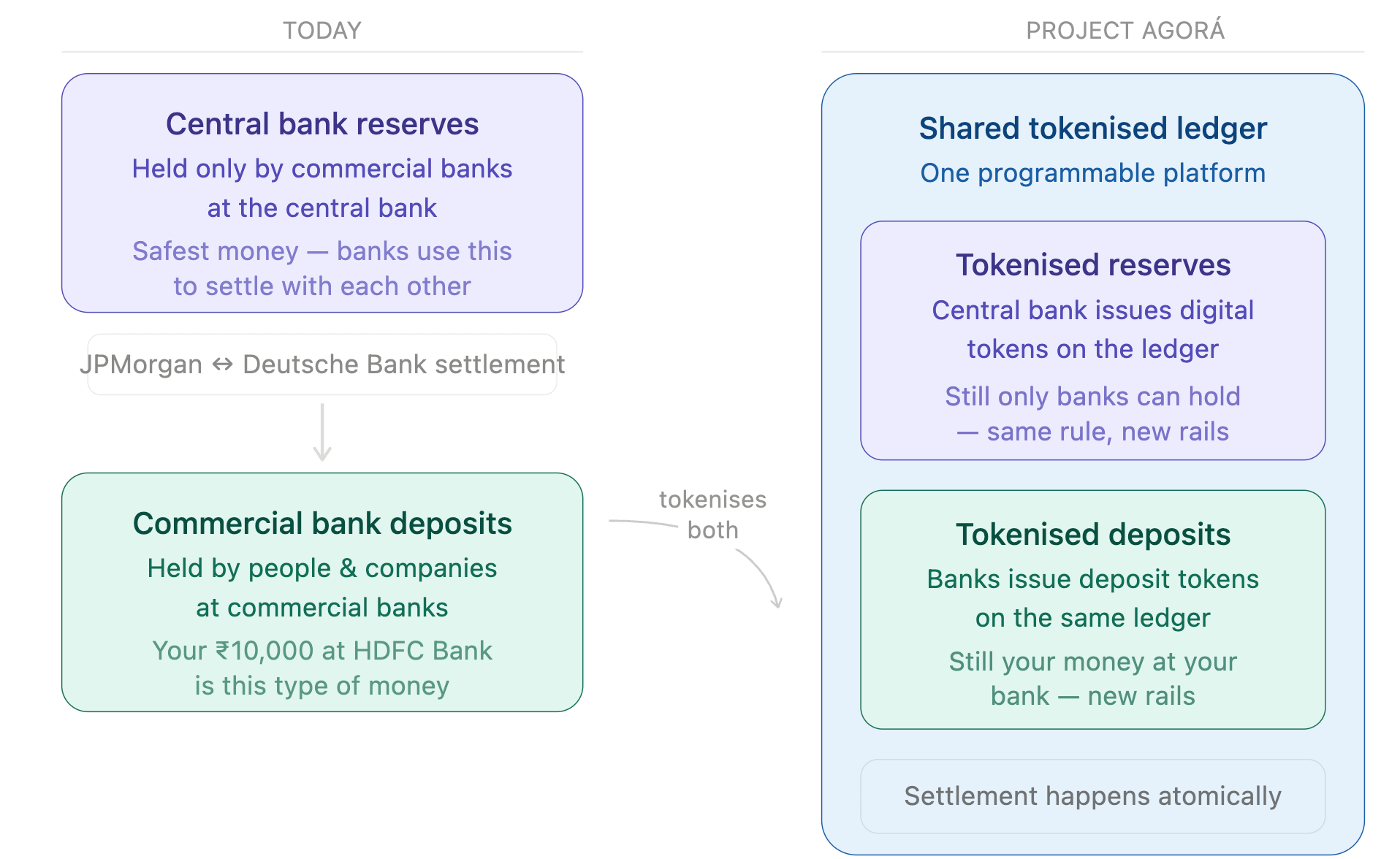

The architecture relies on a basic two-layer split. One layer is controlled entirely by the central banks to handle the core money, while the other is run by commercial banks to handle daily customer transactions.

Tokenised commercial deposits are held on a shared platform, where multiple private institutions manage cross-currency coordination.

At the same time, central bank reserves are stored on separate local ledgers, each controlled entirely by one of the seven domestic central banks.

By combining commercial banking into a single ledger and linking sovereign reserves to domestic control, the BIS aims to create a smooth state monopoly. They are racing to build a compliant, regulated system before independent stablecoins like Tether completely separate global commerce from traditional banking.

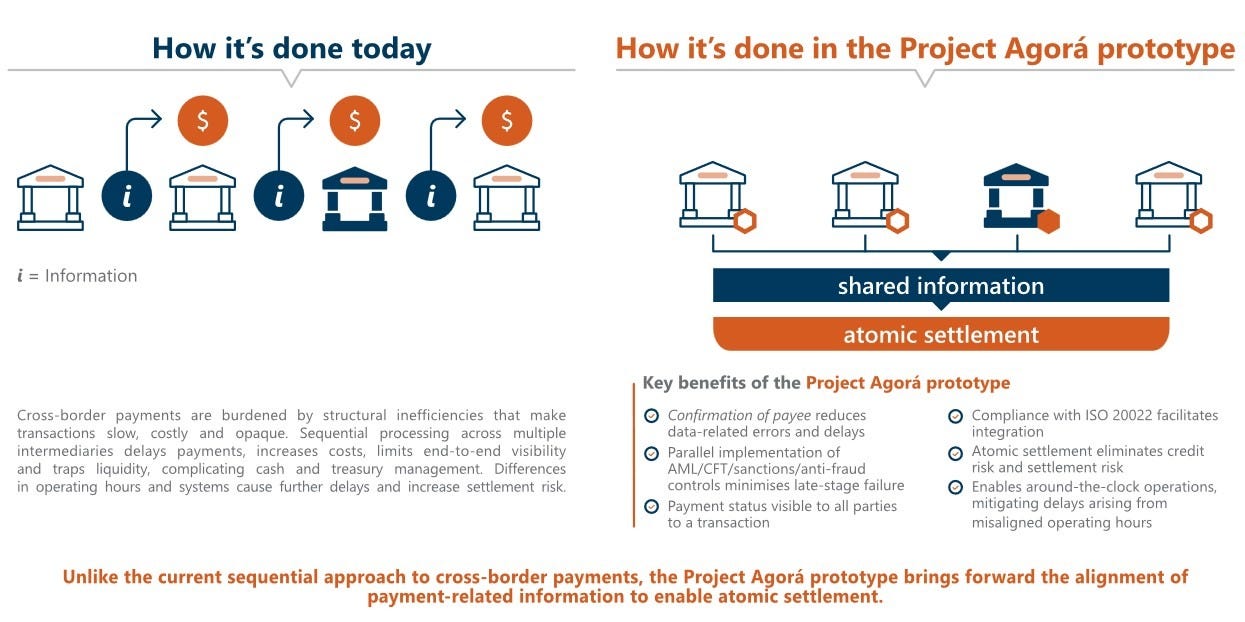

This removes the slow friction of global banking. Currently, international payments operate like a disjointed relay race, with messaging, manual compliance checks, and ledger settlements running on separate corporate systems at varying speeds. Project Agorá simplifies this multi-day coordination challenge into a single, immediate network action. The BIS completed this prototype phase on May 27, 2026, with the Bank of Canada joining right after.

While the organisers stress that this is still a trial to assess the infrastructure rather than an immediate rollout plan, the next phase will focus on real-value testing. There is no official timeline for production.

Project Agora marks a change from typical central bank research papers. Seven major monetary authorities spent two years building and testing instant cross-currency settlement. The code works as intended. The remaining obstacles are focusing on how these different governments will regulate and oversee a shared network. Those administrative challenges are substantial, but the main technical debate is settled.

SWIFT, the messaging system that currently runs international banking, moved at the same time, one layer below.

On March 30, 2026, SWIFT completed the design phase of its blockchain-based shared ledger and entered MVP development, aiming to launch live transactions before the end of 2026. The ledger runs on Hyperledger Besu, an EVM-compatible platform. Settlement stays off-chain through existing RTGS systems.

But SWIFT is not really competing with Agorá. While SWIFT’s ledger synchronises tokenised deposits among commercial banks, Agorá handles the heavy-duty final settlement layer for sovereign central bank reserves. The BIS built Agorá to be explicitly compatible with SWIFT standards. This is the legacy system converting global correspondent banking into a programmable matrix in two perfectly coordinated phases.

Look at the overlapping rosters. Deutsche Bank is a core participant in Project Agorá. It is also part of the global consortium (nine-bank coalition) alongside Goldman Sachs, Bank of America, Barclays, and Santander, exploring a joint 1:1 reserve-backed token on public blockchains. UBS and Citi are on both lists too. JPMorgan is inside Agorá, handles JPM Coin, and just used the public XRP Ledger for a settlement pilot.

This level of overlap is uncommon. Typically, companies allocate serious engineering resources to a single standard and wait. Sending top developer teams to work on competing structures at the same time shows that the leadership is divided. The people with the best data and the most financial stakes cannot predict which governance model will prevail. They understand the technology, but they are uncertain about the politics.

Ripple spent ten years claiming that blockchain-based atomic settlement was the right approach for cross-border payments. Atomic means all or nothing. Either the entire transaction completes or nothing happens. The BIS agreed and created what Ripple described, using tokenised central bank reserves instead of XRP as the settlement asset. This undermines the idea that XRP’s role as a bridge asset is essential for institutional settlement.

The XRP Ledger is still making its way into institutional systems. On May 6, JPMorgan’s Kinexys, Mastercard, Ripple, and Ondo Finance completed the first cross-border redemption of tokenised US Treasuries on XRPL, settling in under five seconds.

Ripple’s dollar stablecoin, RLUSD, reached a market cap of $1.4 billion. The XRPL surpassed $2 billion in tokenised assets in January 2026.

Société Générale launched its euro stablecoin on XRPL in February. Ripple even received conditional approval for a national trust bank charter from the OCC in December 2025.

Ripple’s argument about the architecture was sound, but their claim about the necessity of a specific asset was less compelling. Still, XRPL is being integrated into institutional settlement systems, which is a bigger deal for the long-term outlook than the debate over XRP versus central bank reserves.

Let’s skip the usual marketing points. On the XRPL, transaction fees are very low and are permanently removed rather than going to node operators. Higher institutional volume doesn’t generate cash flow for validator nodes or token holders, unlike gas fees on Ethereum. It just slightly reduces the existing XRP supply. Also, if a bank like JPMorgan transfers a tokenised asset to another institution on the XRPL, it uses its own private capital pools. They do not rely on public XRP liquidity pools to carry out those transactions. The network just provides speed and cryptographic security, not the money itself.

The benefit here is ecosystem lock-in. If institutions trust the network to manage tokenised fiat or stablecoins, the technology becomes embedded in the global financial system. This drives the development of bank-grade node infrastructure and makes the ledger a trusted, permanent financial tool. In the long run, integrating your code into the core of global banking is much more important.

All of this lands on stablecoins with real weight. Tether easily clears $40 billion to $50 billion on an average day. The total stablecoin market is $320 billion. Agorá is moving toward real-value testing, but there is no production timeline. SpaceX didn’t wait for Agorá to finalise cross-border treasury operations in stablecoins. Western Union didn’t wait for Agorá to launch on Solana. It’s the competitive dynamic that counts.

Agorá aims for wholesale institutional cross-border settlement. If it launches and grows, it will address a problem that stablecoins currently handle for institutions moving money between countries.

That market is huge, but it’s not the entire stablecoin market. When the Central Bank of Brazil issued Resolution 561 to prevent local fintechs from using stablecoins for cross-border payments, it didn’t stop millions of ordinary Brazilians from holding digital dollars as a simple savings tool. Likewise, a Turkish retail investor buying USDT on a phone app to avoid lira inflation is not the type of user Agorá is designed for. Those everyday use cases remain unchanged whether Agorá launches or not.

Stablecoins and Agorá are currently more complementary than competitive, but they may collide in the medium term, depending on unresolved factors.

For now, they hardly intersect. Agorá functions as a closed wholesale system. To use it, you must be a central bank or a bank approved by a central bank. A Brazilian holding USDT to safeguard savings from the real, or a fintech managing remittances through Solana, would not fall within Agorá’s reach. Public stablecoins cannot provide the finality that a central bank requires. Agorá cannot keep up with the onboarding speed of a public network. They don’t compete because they do not operate in the same space.

The medium term is more complicated. Corporate treasury teams now use USDC and USDT for cross-border transactions because correspondent banking takes days and is more expensive.

If Agorá launches with real liquidity, which is uncertain, some of that volume could shift. CFOs prefer to avoid non-sovereign counterparty risk on the balance sheet if a regulated alternative operates at the same speed.

For Agora, getting seven sovereign central banks to agree on shared governance is a complex issue, and that’s where these projects have historically stalled. Meanwhile, corporate treasury teams already have established USDC integrations, risk frameworks, and workflows. These will not be discarded simply because a theoretically better option exists.

The segmentation outcome will be Agorá taking institutional corridors, and public networks keeping retail margins. Sounds like a draw. It isn’t. If that’s how it plays out, it means sovereign infrastructure successfully contained public networks to the parts of the market that don’t threaten the existing intermediary model. Remittances, retail savings, and emerging market payments. These are large, but they’re not where the leverage in global finance sits.

We are about to see this theory tested in real time. The EU’s Pontes framework will connect distributed ledger platforms directly to Europe’s main TARGET settlement infrastructure in September 2026. That’s just three months away. If this integration works as planned, it will give tokenised institutional payments in Europe direct access to central bank money. This will mark the official start of the battle between state-controlled pipelines and the open web.

The agora in Athens only failed when people stopped showing up. That’s the ultimate baseline for any network.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.