Meteora’s Margin Story ☄️

Probing the gap between its most visible product and most profitable one

Hello,

DeFi protocols often report on their volume, sharing TVL charts and fee dashboards. What they rarely do is publish a full set of financial statements, including income broken down by segment, cash flow reconciliations, and treasury positions by quarter.

For a Solana liquidity protocol, Meteora’s 53-page annual token holder’s report for 2025 sets a new precedent.

The headline number shows over $182 billion in trading volume facilitated, growing 250% year-on-year (YoY). Meteora generated over a billion dollars in fees and a healthy treasury, earning it a 24-month runway. In a year when SOL lost nearly a third of its market capitalisation, Meteora remained one of the busiest platforms on Solana.

One of the interesting stories in this report is its income statement, which reveals how Meteora’s flagship product and its most profitable products are two different things.

In today’s analysis, we will examine how this model works and explore where the billion dollars in fees flow after each stakeholder takes their share.

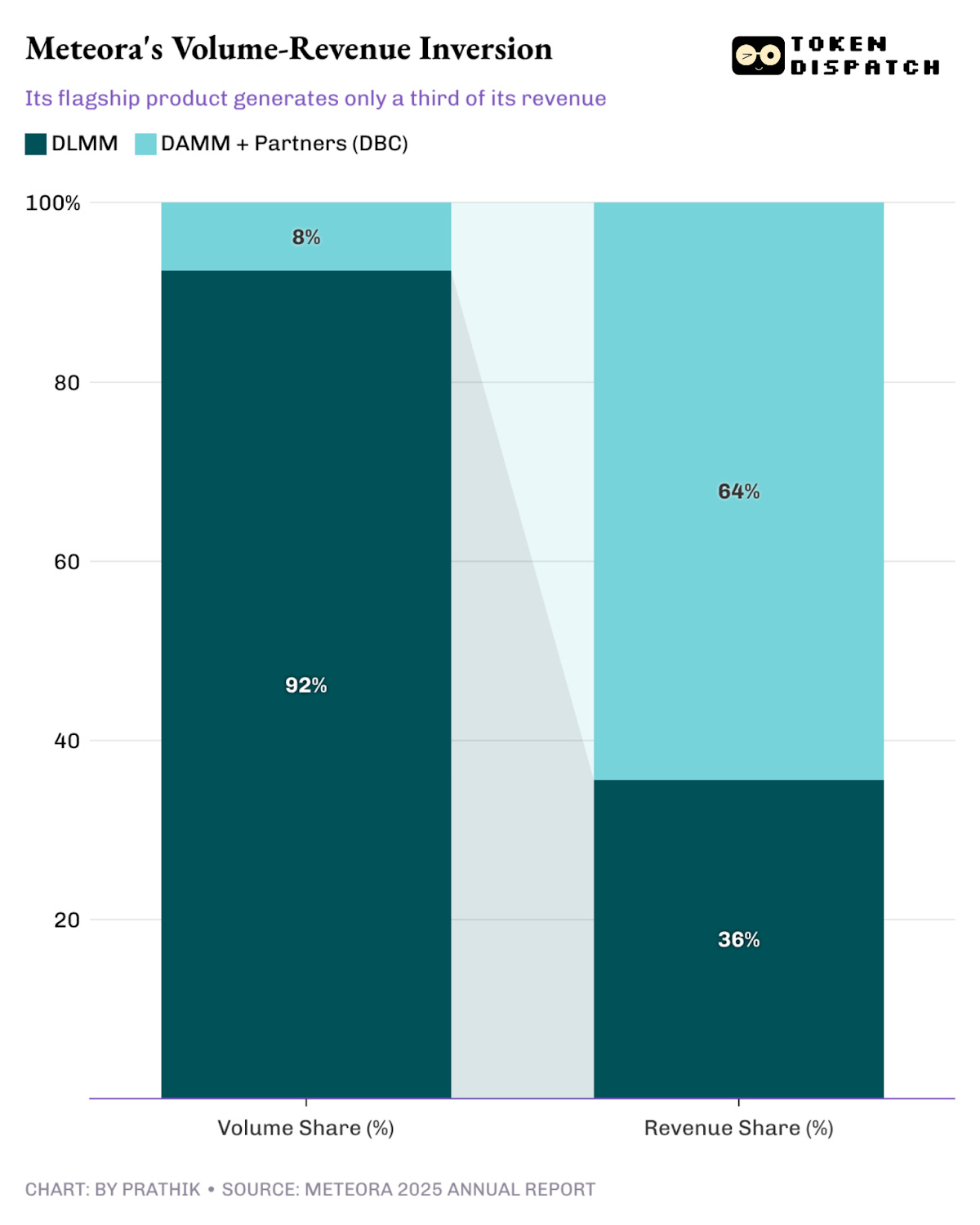

The Volume-Revenue Inversion

Meteora runs four on-chain programmes: DLMM, DAMM v1, DAMM v2, and DBC. The Dynamic Liquidity Market Maker (DLMM) is the protocol’s flagship product, the one the Liquidity Provider (LP) Army rallies around, and the one most people associate with the protocol. DAMM v1 and v2 are constant-product automated market makers (AMMs). Dynamic Bonding Curve (DBC) powers token launches through customisable bonding curves. Each programme collects swap fees from traders and splits them between liquidity providers and the protocol.

In FY2025, DLMM facilitated $168.3 billion in trading volume, while the remaining flowed through DAMM ($11.5 billion) and DBC ($2.4 billion) pools. It’s evident that DLMM is Meteora.

Yet, volume is not revenue.

DLMM generated $43.1 million in protocol revenue, barely a third of total revenue, despite generating 92% of the total volume. However, fees from DAMM pools and the launchpad partner (DBC) together generated $78.0 million, about 64% of Meteora’s total revenue.

This shows that Meteora’s flagship product, with utmost attention, and the major revenue-generating product are not the same. DLMM brings the volume, the brand recognition, and the LP community, while the DAMM and launch infrastructure bring the margin. Both are essential, and the interplay between them is what makes the model work.

But why does its flagship product generate only a third of the protocol’s revenue? To understand that, we need to look at the various kinds of assets that trade on each programme and the fees they generate per dollar of volume.

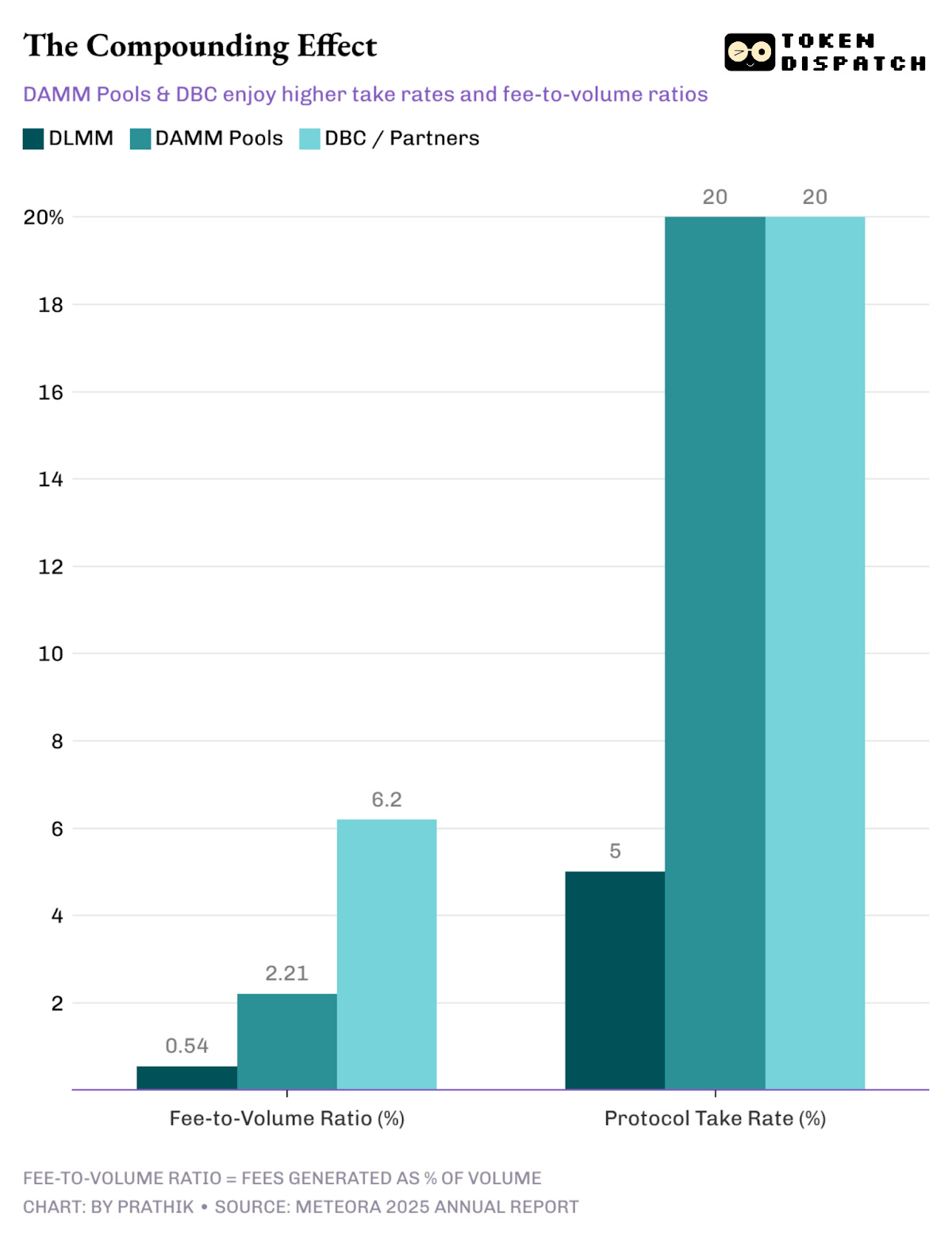

The Compounding Advantage

The gap in contribution is partly explained by the take rate, calculated as a percentage of fees retained by Meteora after paying the LPs. This rate varies across programmes. On DLMM, LPs keep 95%, and Meteora retains 5%. On DAMM and DBC, LPs keep 80%, and Meteora retains 20%. That’s because Meteora charges a premium on the newer programmes for the additional infrastructure they provide, including anti-sniper protections, dynamic fee mechanisms, and composable launch tooling that goes beyond routing swaps.

That’s a 4x differential between the flagship product and the one that contributes the most to its margins. But that explains only part of the gap.

The other part is explained by varying fee intensity, the amount of swap fees generated per dollar of volume.

DLMM primarily routes established trading pairs. SOL-USDC, major tokens, assets with deep order books and tight spreads. These pools compete on execution quality, which means fee tiers are set low to attract aggregator flow. Across FY2025, DLMM pools generated $907.3 million in fees on $168.3 billion in volume, with a fee-to-volume ratio of 0.54%.

The DAMM and DBC pools serve a different market. New token launches, memecoins, long-tail assets, and high-volatility, low-liquidity pairs. Fee tiers on these pools run wider to compensate LPs for the impermanent loss risk that comes with providing liquidity to assets that can move 30% in a day. DAMM pools generated $254.4 million in fees on $11.5 billion in volume, with a fee-to-volume ratio of 2.21%, roughly four times that of DLMM.

This is what compounds the gap between what both products contribute. For every dollar of volume, the DAMM and DBC pools generate approximately 4x as much in fees. Meteora then retains 4x more of those fees as protocol revenue.

This differentiation of how these two programmes work is key to Meteora’s structure. DLMM is built to win on execution and scale, while operating in a tight-fee, high-throughput and aggregator-friendly environment. The launch infrastructure stands out for its unique tooling, configurable economics, and a fee structure that reflects the premium value it provides to token creators. Together, they give Meteora a diversified top line that most single-product DeFi protocols lack.

But diversification only matters if both engines keep running. The quarterly data shows what happens when one of them stalls.

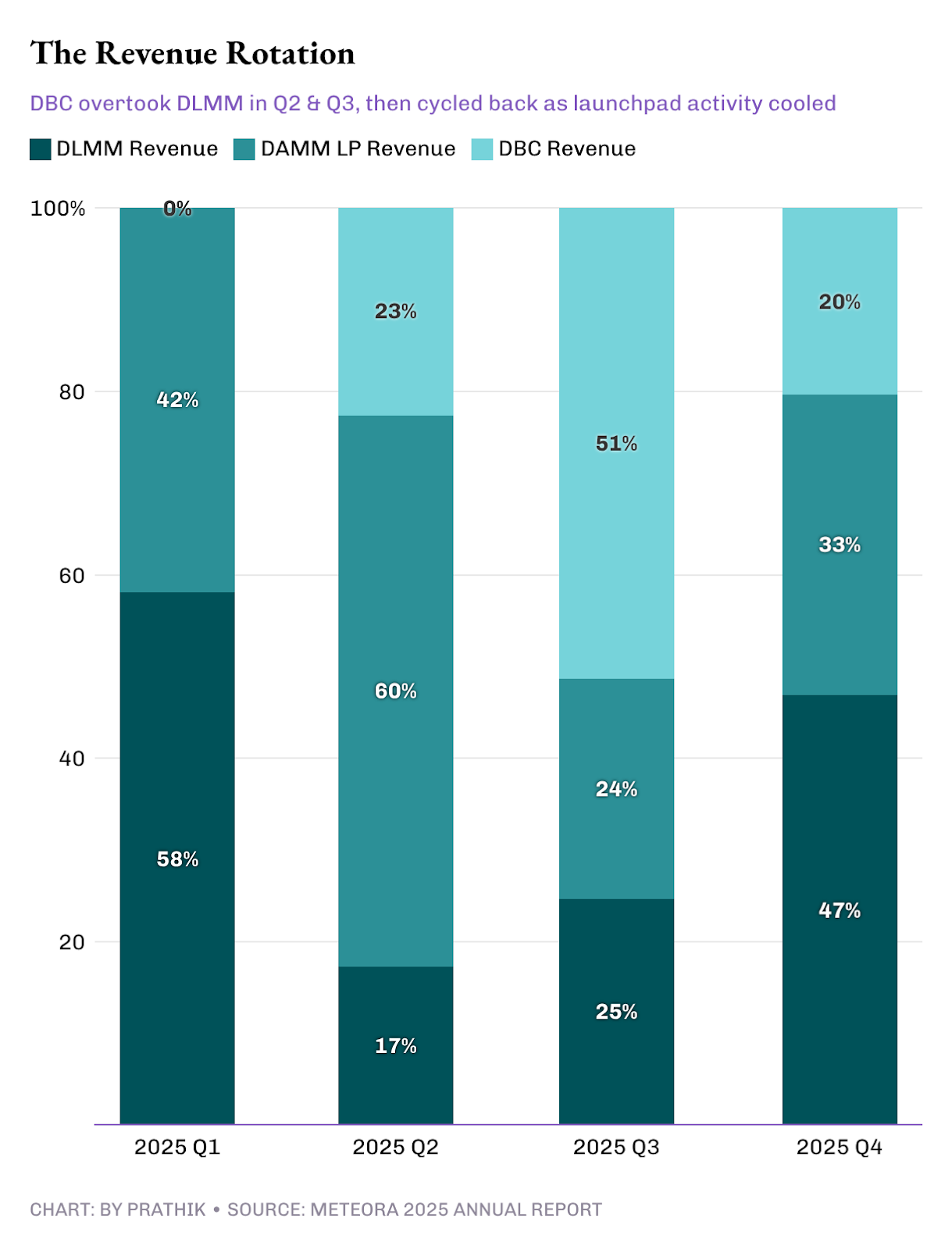

When the Launch Cycle Cools

In Q1, Meteora’s entire $36.5 million in revenue came from LP pools, when the launchpad infrastructure hadn’t shipped yet. DLMM contributed 58% of that quarter’s revenue. By Q2, partner fees first appeared at $8.6 million after Meteora went fully permissionless and launched DBC and DAMM v2. Immediately, DLMM’s share of revenue dropped from 58% to 17%.

Q3 was the launchpad quarter. Believe’s Internet Capital Markets (ICM) trend drove launch volume through Meteora’s bonding curves, and partner fees surged to $15.1 million, more than half the quarter’s total. For the first time, launch infrastructure was contributing more to the top line than both LP pool programmes combined.

Then Q4 arrived. Partner revenue fell 77% to $3.5 million as launchpad activity cooled. DLMM’s share climbed back to 47%.

The quarterly view reveals the trade-off.

The high-margin launch business can dominate revenue in a good quarter, but it’s cyclical. The lower-margin DLMM business doesn’t spike as hard, but it’s not over-reliant on narratives. In Q4, when launchpad revenue hit its lowest point, LP pool revenue from DLMM and DAMM still covered $13.8 million, comfortably above the protocol’s $1.5 million monthly burn rate.

While DLMM holds the fort during testing cycles, the launch infrastructure works as a catalyst during favourable times.

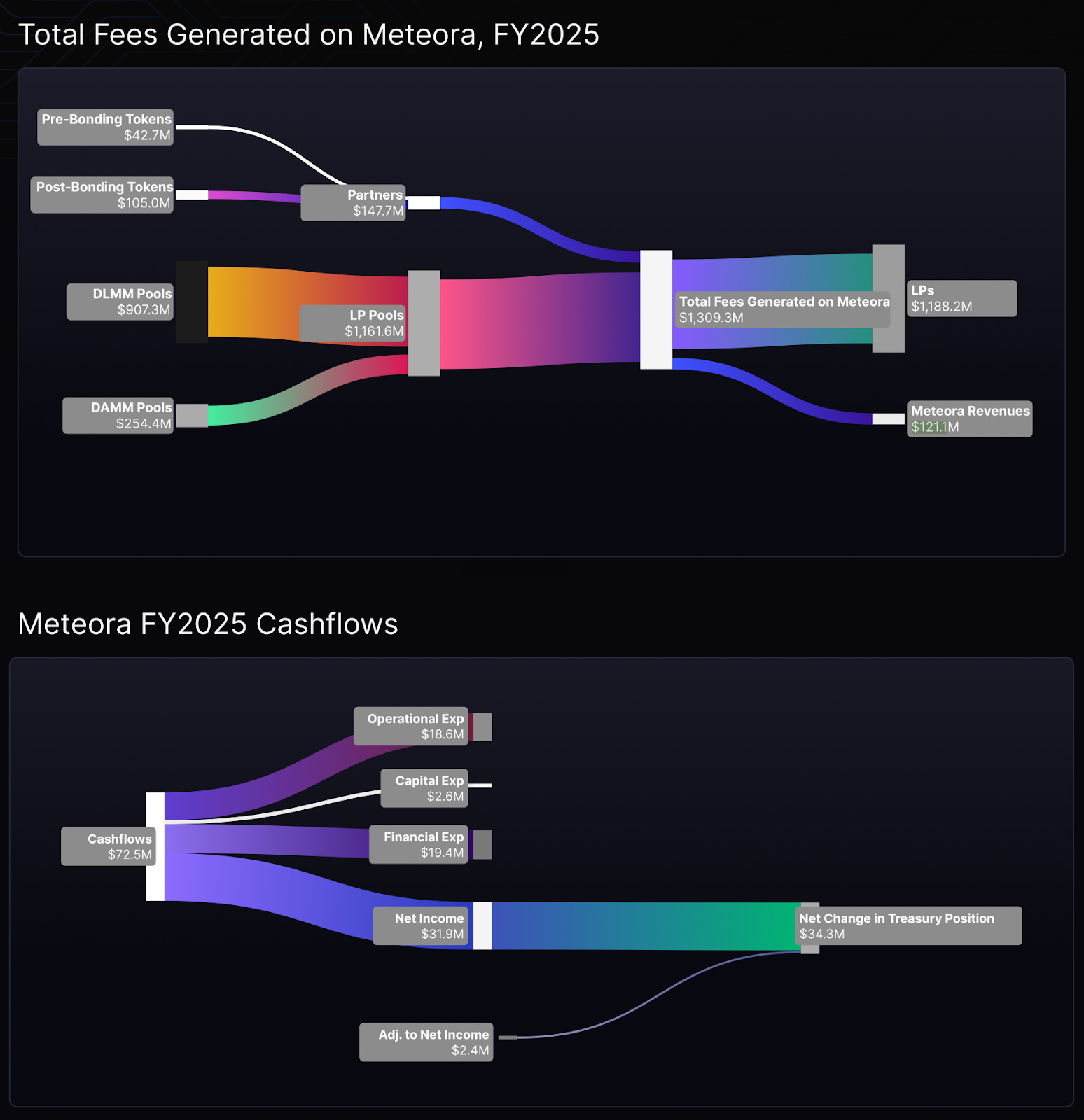

Where the Billion Dollars Go

In FY2025, Meteora generated $1.31 billion in swap fees, of which LPs received $1.19 billion (~90%). After their cut, Meteora retained $121.1 million in protocol revenue.

But Meteora did not receive all the $121.1 million it earned.

Fees are collected in the same tokens being traded. On a SOL-USDC pool, that means fees arrive in SOL and stablecoins. On a memecoin launch pool, fees accrue in the just-launched token, and that token can depreciate by 80% before the protocol converts it into a stable asset. Of the $121.1 million in accrued revenue, only $72.5 million was captured in the treasury as SOL and USDC/USDT. The remaining $48.6 million, roughly 40%, eroded in the gap between earning the fee and liquidating the token.

However, this difference between what is accrued and what is earned is present in every crypto protocol similar to Meteora.

The protocol has since addressed the leakage. Starting January 2026, a programme-level update periodically converts non-stablecoin fees into USDC. If it works as intended, the gap between earned and realised revenue should narrow meaningfully in FY2026.

What This Means

Meteora’s report gives us a complete picture of its economics, something that a DeFi protocol rarely offers.

It offers us a transparent understanding of how a protocol can facilitate $182 billion in trades, generate over a billion in fees, and still see only $72.5 million land in its treasury. But that’s the reality of running liquidity infrastructure, where most of the value rightly accrues to the capital providers who make it work.

What is most compelling is the architecture underneath. Meteora has built a model where a high-volume, lower-margin product sustains the brand and community, while a lower-volume, higher-margin product funds the protocol’s growth.

The 2026 roadmap signals that the team clearly sees this. Their planned convergence of LP and trading tools is an attempt to widen DLMM’s revenue potential by pulling traders, a far larger user base, onto the same platform. Meteora Labs and the Bedrock initiative are bets on expanding the variety and quality of assets launching through its infrastructure, which is where the margin lives.

Both moves point toward strengthening both engines rather than choosing between them.

For the broader DeFi industry, the lesson is not to lean too much into volume as a metric. Revenue composition is what determines whether a protocol can survive a down cycle, fund its own development, and compound over time. Meteora had the confidence to publish the numbers that make this distinction visible. More DeFi protocols should follow suit.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.