When someone tells you not to look at something, you immediately want to look at it. Barbra Streisand once tried to remove a photograph of her house from the internet. Before she filed the lawsuit, 6 people had downloaded it. After she filed, almost half a million people had seen it. This is now called the Streisand Effect, and it is one of the most reliable phenomena in the history of information.

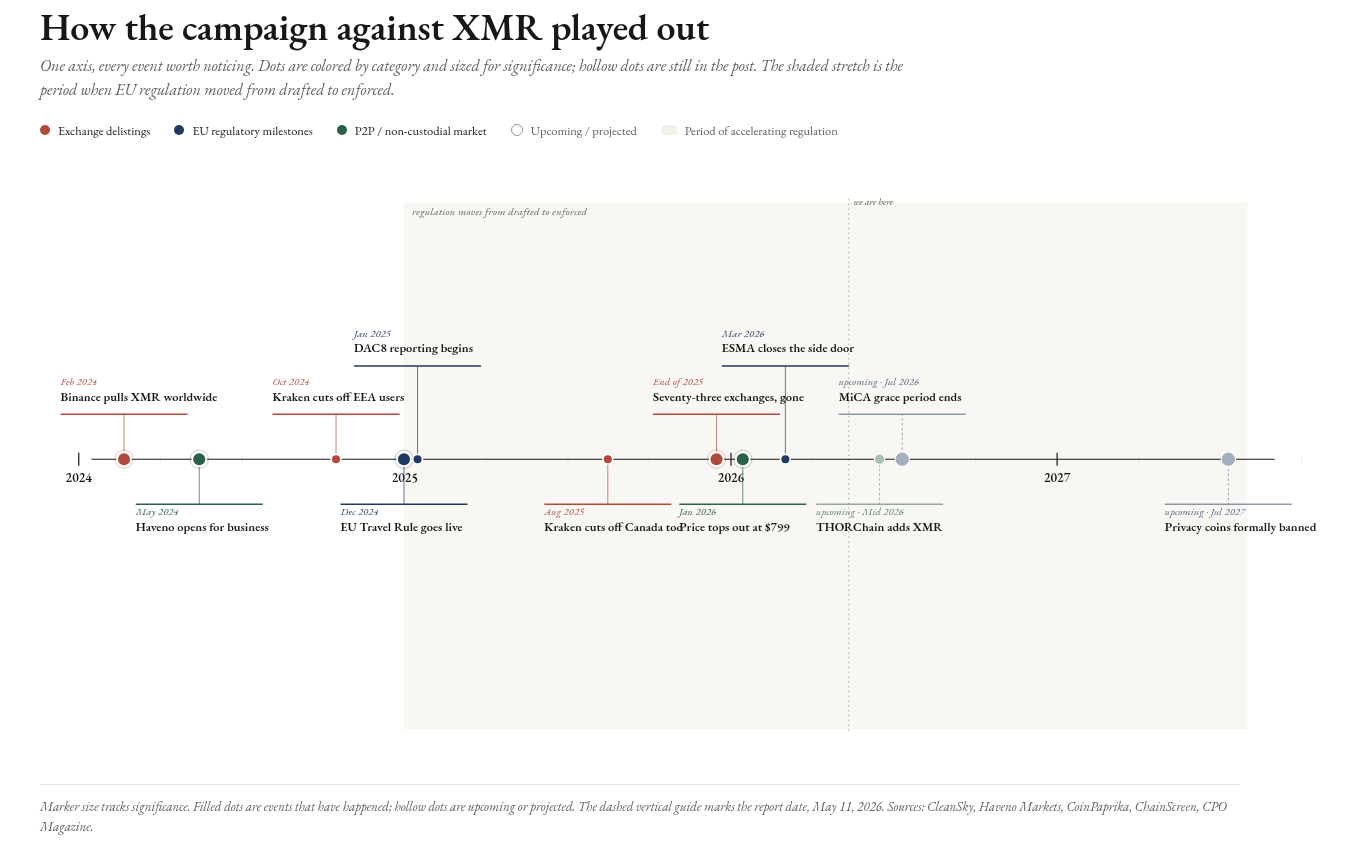

Europe’s regulators spent two years telling exchanges not to list Monero. Seventy-three exchanges complied. In January 2026, Monero hit its highest price in eight years. I did not see this coming either. Nobody who runs a coherent regulatory theory would have predicted this.

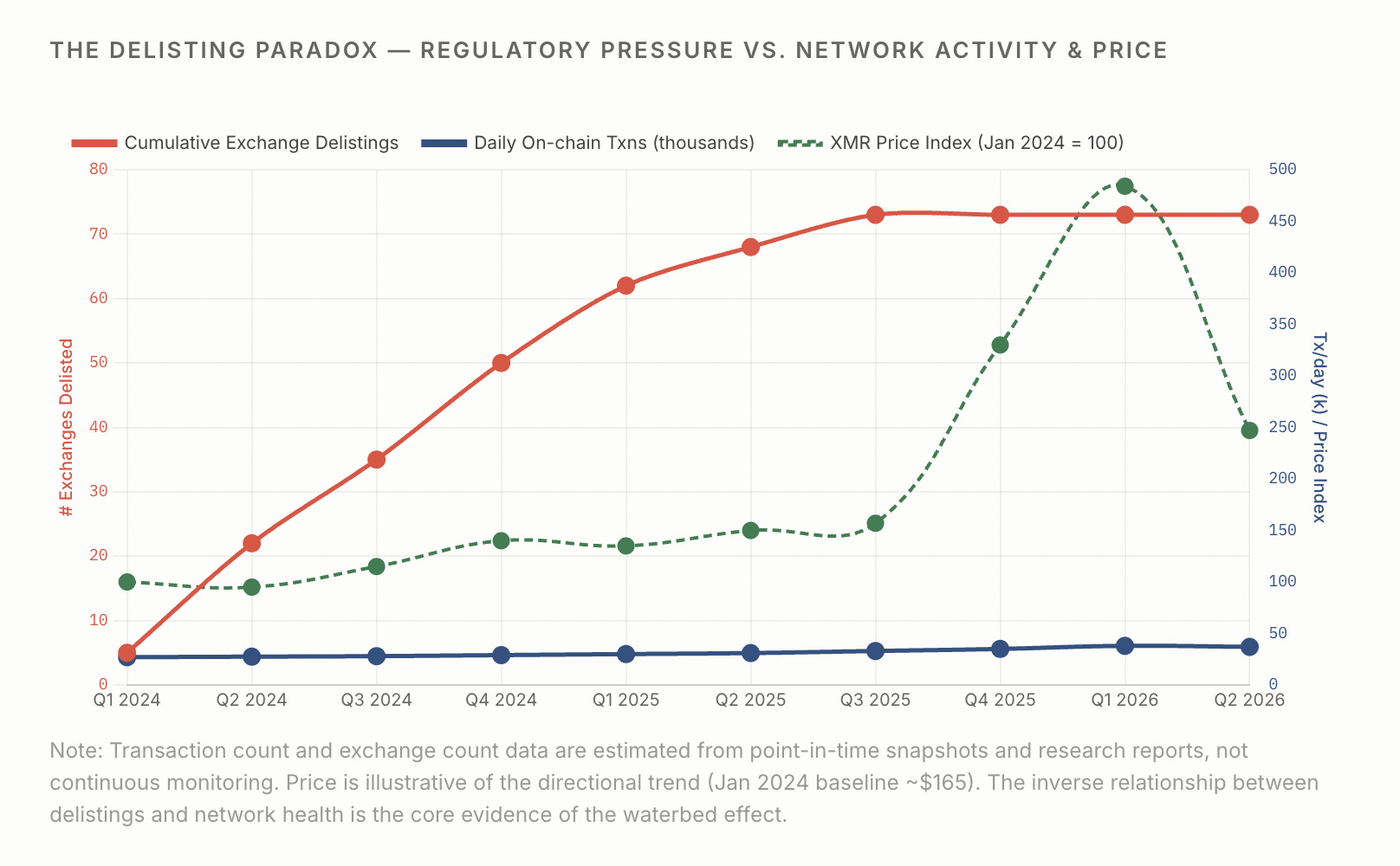

When a cryptocurrency gets delisted from major exchanges, liquidity dries up, and the price falls. The project fades and becomes a footnote in discussions about assets that could not withstand regulation. This pattern is so dependable that exchanges use the threat of delisting to influence governance, and projects worry about it as a result.

On January 14, 2026, Monero hit an all-time high. I am not saying regulators should have read the Wikipedia article. But they really should have read the Wikipedia article.

The EU’s MiCA framework, the Travel Rule, and DAC8 are all designed around this logic. Apply pressure at the custodial exchange interface where crypto meets the traditional financial system, and the underlying asset loses its economic viability. For most assets, this works. But Monero survived.

Start with the basics.

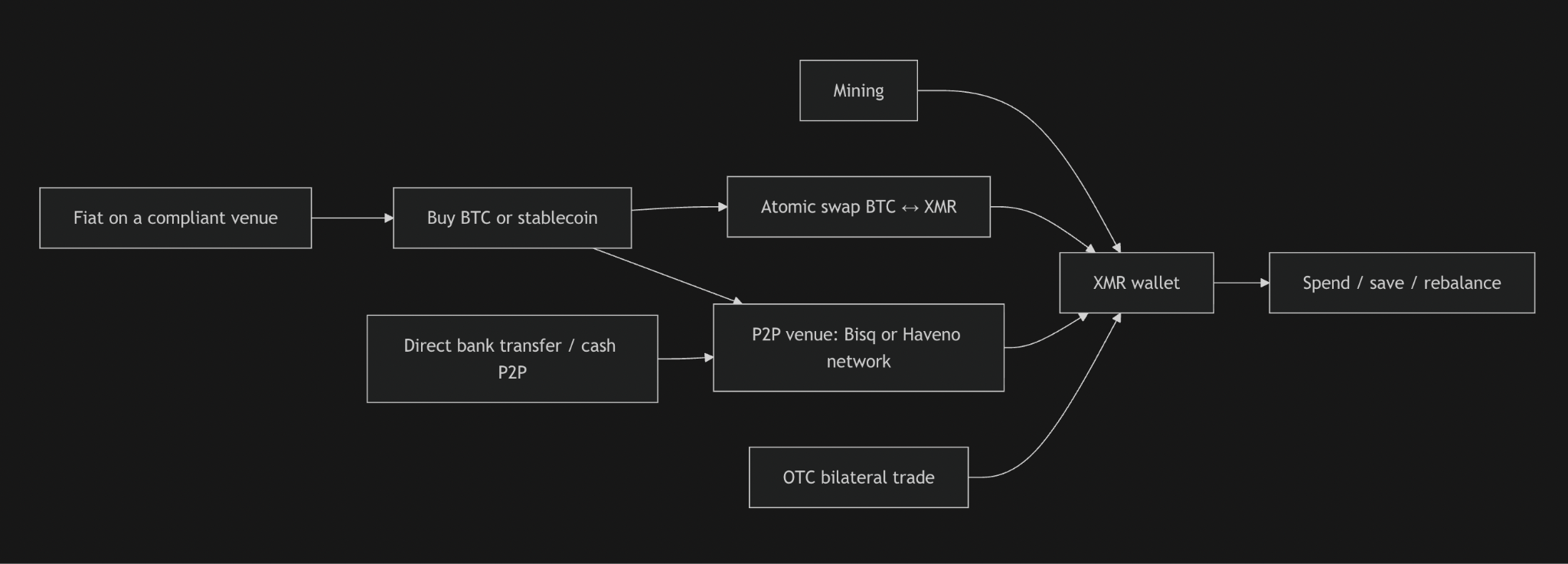

Monero is a cryptocurrency where transactions are private by default. Bitcoin transactions are publicly visible on-chain, which means every address, every amount, every movement is visible. Monero uses ring signatures, stealth addresses, and a mechanism called RingCT to hide both the sender and the amount.

Chainalysis, the blockchain forensics firm that governments hire to trace crypto, has publicly admitted it cannot reliably extract meaningful data from Monero’s privacy. Monero was delisted because regulators cannot track it. The delistings are, in a strange way, a product review. The technology works well enough that governments choose to cut off access instead of trying to monitor it.

Now, let’s examine the outcomes of the delistings.

The Haveno decentralised exchange, a non-custodial, peer-to-peer platform designed for XMR trading, launched in May 2024. From its start until May 2026, it processed 24,018 trades totalling 921,585 XMR, as of May 10, worth about $374 million at average prices. Haveno did not exist before the delistings began. It was created to take advantage of the market that regulated exchanges were leaving. During the delisting period, on-chain transaction counts increased by about 30-35%. Transactions grew from 25,000-30,000 per day in early 2024 to 35,000-40,000 by early 2026.

By early 2026, that totalled roughly 800,000 transactions a month. The network behaved like a healthy asset migrating its settlement layer, not a failing one.

The day after Monero reached its all-time high on January 15, Felix Protocol launched XMR/USDC perpetual swap markets on Hyperliquid without requiring governance votes, exchange approvals, or regulatory permissions. On launch day, total cross-exchange XMR futures open interest peaked at a record $275 million. The price of XMR rose by 6%, and volume increased by 13%.

As of May 2026, Hyperliquid holds $36.37 million in XMR open interest, surpassing Binance (before delisting) and BitMEX to become the largest venue for XMR trading globally. It achieved this as a decentralised exchange that does not require KYC or a regulatory license.

You push down on one spot, and the volume just pops up somewhere else, like a waterbed. The campaign to delist Monero is the ultimate case study. Regulators tried to “turn off” the coin by bullying centralised exchanges, but the market moved house.

By removing custodial access, they accidentally funded the construction of the non-custodial world. Haveno, atomic swaps, and P2P markets reach this scale because they have become a mechanical necessity. The pressure meant to kill Monero’s market ended up building its permanent infrastructure instead. Love a beautiful coincidence.

Before the delisting campaign, regulators had some control. They could monitor the order books on licensed exchanges, rely on fiat on-ramps for KYC, and use exchange data for their analysis. By enforcing the delistings, they lost all those surveillance tools at once. Fiat access switched to P2P networks running over Tor, and price discovery shifted to permissionless DEX infrastructure. Regulators lost their line of sight.

The EU’s AMLR formally bans anonymous crypto-asset accounts under Article 79, effective July 10, 2027. The MiCA transitional deadline arrives in July 2026. Each new enforcement milestone, on current evidence, is likely to accelerate the infrastructure migration rather than reverse it. Every user pushed out of a custodial exchange is another user becoming entrenched in the P2P world. By the time the full ban arrives in 2027, this non-custodial ecosystem will have had three more years to strengthen itself.

A word of honesty about the claim that “Monero doesn’t need exchanges anymore” is that the research behind this article is detailed on this point.

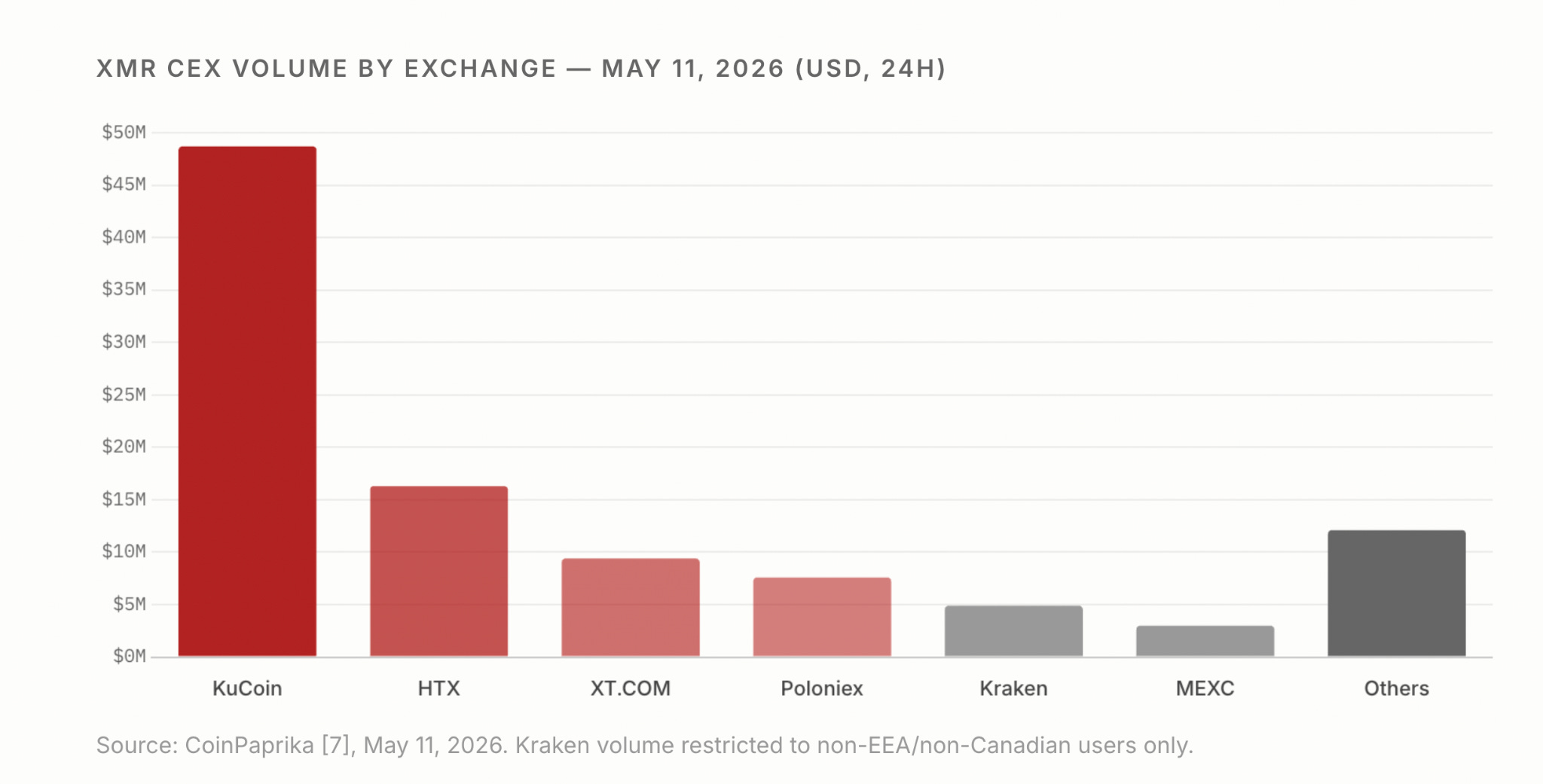

Monero does not need major regulated European spot exchanges. This has been shown. What it still needs are the functions that exchanges provide, such as price discovery, fiat conversion, large-block liquidity, and arbitrage across venues. These functions have moved to Haveno and Bisq for P2P transactions, to atomic swaps for BTC/XMR conversion, to offshore centralised exchanges like KuCoin (which holds 50%+ of CEX XMR volume as of May 2026) for the remaining custodial layer, and to DEX perpetuals for positioning. Monero’s own FAQ still lists exchanges as the most common method for acquisition. The official Monero project page still includes exchanges in its resources.

The more accurate claim is that Monero has shown it can survive and even reach an all-time high without the regulated European venue layer. This does not mean that exchanges have become irrelevant to it. The January 2026 ATH is proof of resilience, not proof that liquidity is unlimited or that all structural risks have disappeared.

Two developments will shape Monero’s next year.

The first is the FCMP++ upgrade, which is currently in its second beta stressnet as of May 2026. A Trail of Bits security audit is scheduled for May 11-22, 2026. Full-Chain Membership Proofs will replace Monero’s current ring signature system. Instead of hiding your transaction among 16 decoys, it will now hide it among 150 million outputs. A clean audit would eliminate the last significant technical objection to Monero’s privacy claims.

The second development is THORChain’s planned integration of XMR, expected in June or July 2026 (pending the second audit). This would allow decentralised, cross-chain swaps of XMR without requiring KYC or custodians. This integration addresses the remaining major weakness: most non-custodial access to XMR still goes through a Bitcoin leg first.

Enabling direct XMR/ETH and XMR/stablecoin swaps on a DEX would remove that dependency and further reduce the exchange layer’s role.

Neither of these changes is guaranteed. Audits can uncover problems. Integrations may be postponed. Hashrate concentration poses a constant risk for any proof-of-work network. The AMLR ban might lead to more delistings from the offshore exchanges where XMR still trades. Liquidity fragmentation across DEX, P2P, and offshore CEX creates wider spreads and greater price impact than a unified order book.

The EU acted as Monero’s most effective, unpaid marketing department, and all they got for it was a loss of visibility and a headache. They should probably send a bill for the consulting work, but they’ll probably just schedule another meeting to discuss a markup for a markup.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.