The history of infrastructure is, in a sense, a history of people who built things that became too important to own. The engineers who designed TCP/IP, the protocol that made the internet run, did not become billionaires. The people who laid undersea telegraph cables in the 1860s lost most of their money. Linux runs an estimated 96% of the world’s servers. Linus Torvalds is worth approximately $50 million. Jensen Huang, who makes the chips that run on Linux, is worth $120 billion. The relationship between building something essential and capturing the value of that essential thing is not what economic intuition suggests it should be. There is a trap that infrastructure builders fall into: the more indispensable their work becomes, the harder it is to charge for it, because charging starts to look like charging for air. Nobody becomes the owner of gravity.

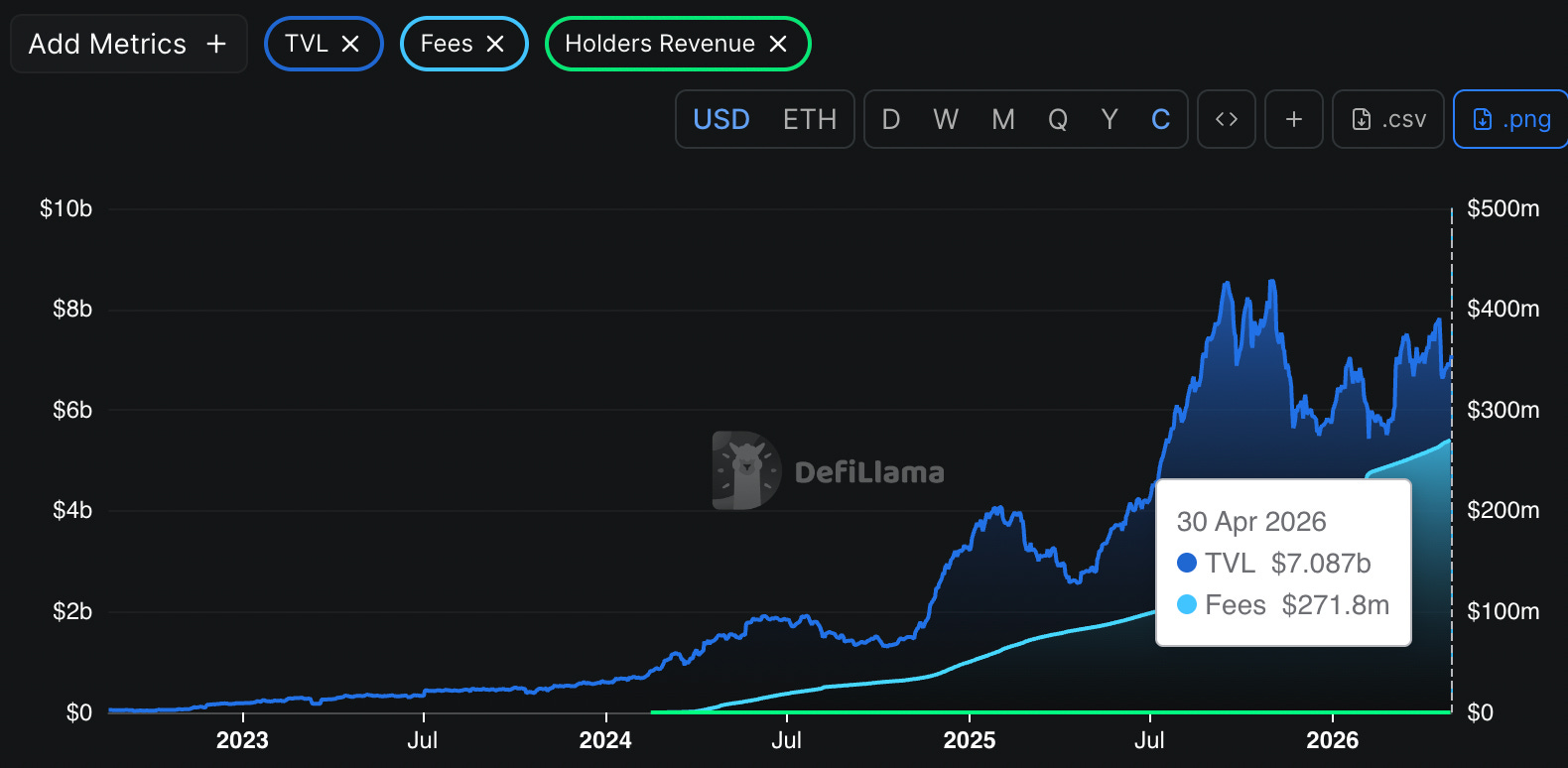

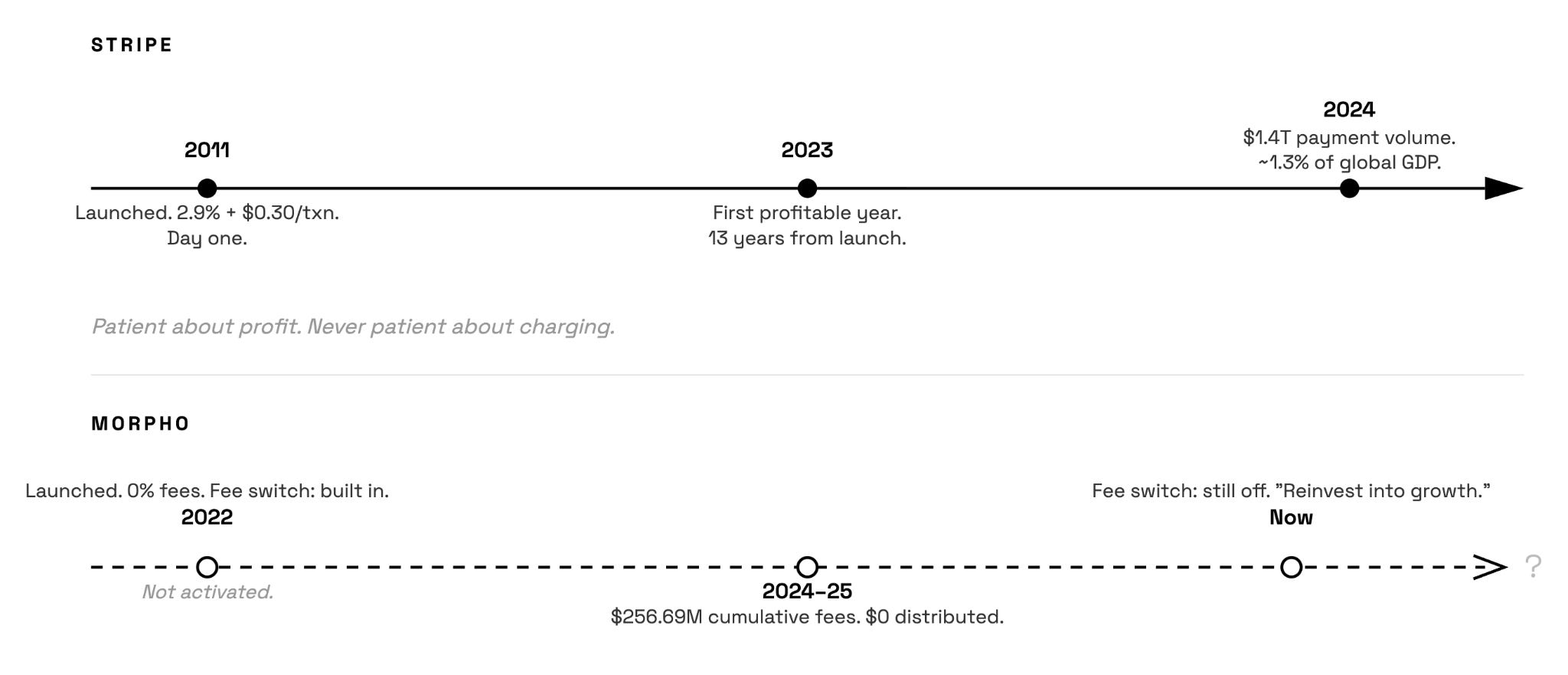

Morpho has generated $256.69 million in cumulative protocol fees. Token holders have received zero of it. The protocol takes no revenue. There is a fee switch built into the contract, capped at 25% of borrower interest, that governance could theoretically activate. In June 2025, Morpho’s founder, Paul Frambot, said publicly that the association advocates reinvesting protocol fees rather than distributing them and that all revenue should go back into growth. But a February 2025 governance proposal was more specific about what was holding things up: the legal and tax work around fee switch activation was not yet complete. The switch is not off because the paperwork is not finished.

Morpho currently has $7 billion in total value locked, with Coinbase running its entire lending product on top of it, Apollo Global Management buying 90 million tokens on a 48-month schedule, and Société Générale deploying on its infrastructure. France’s first DeFi unicorn has decided, for now, that it does not want to be paid.

At this point, you have to ask whether this is an elaborate proof of concept for running a charity on an institutional scale.

Stripe launched in September 2011. 2.9% plus 30 cents per transaction; no setup fees, monthly fees, or charges for failed payments. Patrick Collison said explicitly in 2012, “We only make money if you do.” Legacy processors charged merchants through opaque surcharges, PCI compliance costs, and approval processes that took thirty to ninety days. Stripe lets developers integrate payments in seven lines of code. By 2013, they were processing billions of dollars annually for companies ranging from Lyft to the Museum of Modern Art, with 83 employees and a $1.75 billion valuation.

They did not turn a profit for thirteen years. The 2023 annual letter was the first confirmation of being “robustly cash flow positive.” The 2024 letter called it straightforwardly profitable, with expectations that it would remain so. For six consecutive years during that stretch, Stripe spent more on R&D as a percentage of revenue than any comparable company. They processed $1.4 trillion in payment volume in 2024, which is roughly 1.3% of global GDP. The patience required in infrastructure is a kind of institutional patience that most companies cannot sustain. The Collisons maintained it for over a decade.

Morpho has been called the DeFi Mullet. Fintech in the front, DeFi in the back. When Coinbase launched its crypto-backed USDC lending product, it built the entire user experience itself. Morpho handled the collateral, the matching, the interest calculations, and the liquidation mechanics. Over $2.17 billion in USDC has been originated through this product in the U.S. alone, now expanded to the UK. The strategic value to Coinbase was speed. They deployed a sophisticated, institutional-grade lending stack without building it from scratch. The strategic cost to Morpho was zero revenue from the arrangement. Every dollar Coinbase made on that product flowed through Morpho’s contracts and past Morpho’s empty wallet.

Stripe always charged. The zero-revenue years were about reinvestment, not the absence of a business model. Morpho’s zero-revenue model is a deliberate choice not to charge, with a fee switch in place but explicitly deprioritised by its founder. Stripe was building toward pricing power by deepening its distribution. Morpho’s path to pricing power is less clear, and token holders are the ones bearing the cost of finding out.

The MORPHO token does one thing, it governs. Holders can vote on cross-chain deployments, reward extensions, and, in theory, the fee switch. In practice, the governance actors with the most influence have voted almost exclusively on proposals that expand Morpho's coverage rather than compress the yields that attract deposits in the first place. Because compressing yields reduces TVL, and reduced TVL weakens the argument for turning on the fee switch. The logic is circular in a way that is not obviously resolvable. None of the fees it generated has moved to token holders. The token's all-time high was $4.17 in January 2025. It trades around $2 on April 30th. The circulating supply has expanded from roughly 75 million tokens in early 2025 to over 550 million by April 2026. That is a 7x increase in supply over 12 months, against a price down more than 50% from its peak. Token holders are funding the protocol's growth. The protocol's growth is benefiting Coinbase, Bitwise, Fireblocks, Anchorage, Apollo, and Société Générale. This is the stated strategy.

Apollo, a firm managing $938 billion in assets, agreed to buy up to 90 million MORPHO tokens, 9% of the total supply, over 48 months. When a firm of that scale commits to a 48-month accumulation schedule on a DeFi protocol, it is not speculating on the token price. They are making a judgment about the protocol’s permanence. Infrastructure that survives long enough becomes unchallengeable, and the switching costs eventually exceed any benefit of moving. Replacing Morpho at this point would mean rebuilding the smart contracts, migrating $7 billion in liquidity, convincing Coinbase and Apollo to move their integrations, and restarting the trust-building process from scratch. Apollo is betting that Morpho is approaching that threshold.

Stripe’s moat was never the payment technology. Look instead at the integration depth. Every developer who built on Stripe, every merchant who embedded it into their checkout, every platform running on Stripe Connect represented a switching cost that compounded over the years. By the time Stripe’s competitors understood this, Stripe had already won.

Morpho’s is aiming at the same moat. Coinbase cannot easily rebuild that lending stack from scratch. Steakhouse Financial’s vault curation is optimised for Morpho’s architecture. The integrations are accumulating faster than any competitor is building. Aave’s loan-to-deposit ratio sits at 39%. Morpho’s is 41%. The efficiency gap is widening, and in institutional lending, 200 basis points is no silly game.

When Morpho’s first concrete commercial revenue arrived, a low seven-figure licensing fee from Berachain for the right to use Morpho Blue’s code, governance voted to send it to the Morpho Association, a French nonprofit, rather than the DAO treasury. The explanation was that the legal work around direct DAO fee receipt was not yet complete. The same legal work is blocking the fee switch. So the protocol is generating commercial revenue. It is being routed around the people who own the governance token, with a promise that the routing will change once the paperwork is done. Stripe’s shareholders got rich when Stripe got rich. Morpho’s token holders are awaiting a governance proposal that has not yet been drafted.

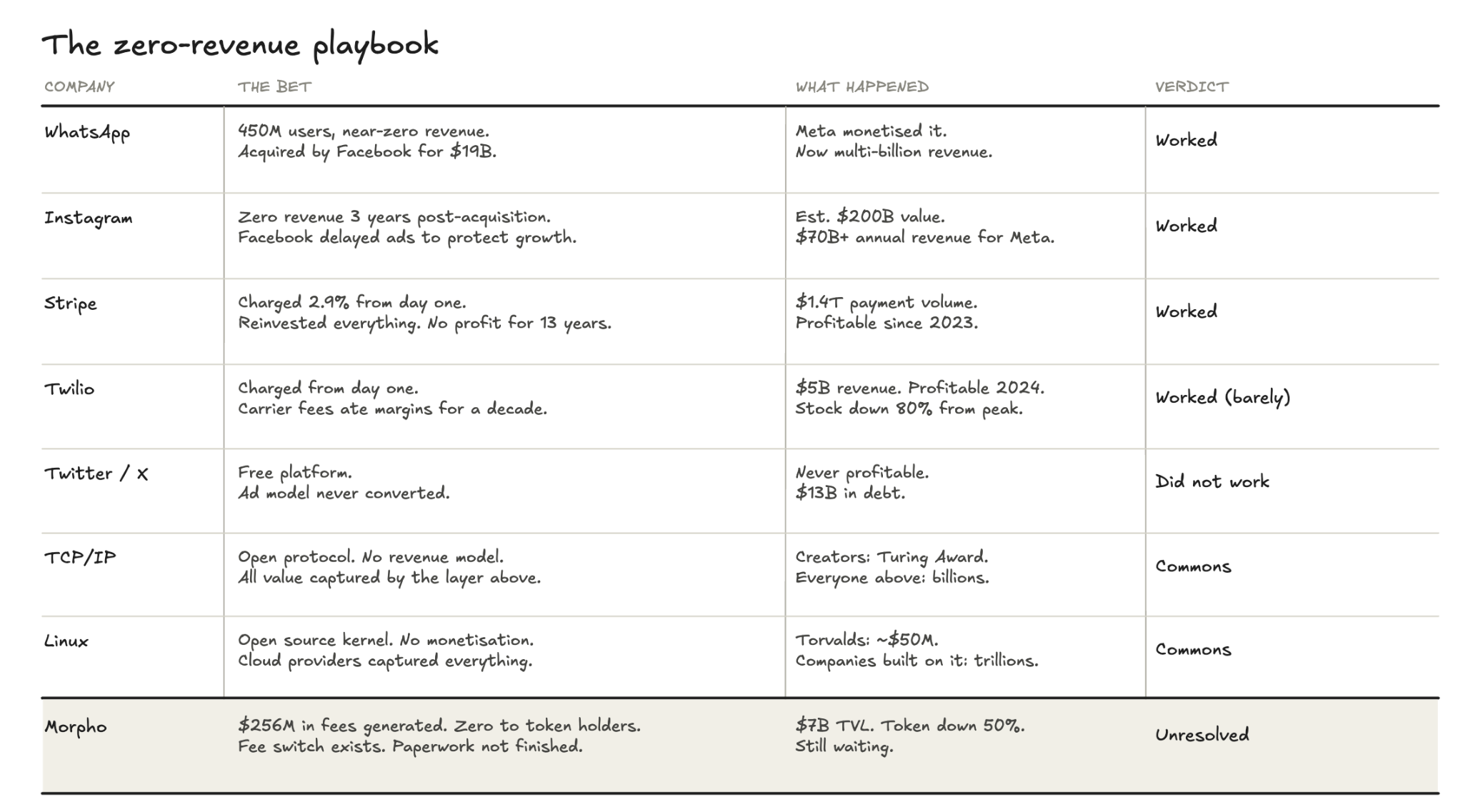

The history of companies that delayed monetisation to win distribution first is more instructive than the Stripe comparison alone. There are really only three outcomes in that playbook, and Morpho fits uncomfortably into all three at once.

The first outcome is acquisition. WhatsApp had near-zero revenue when Facebook bought it for $19 billion in 2014. Instagram generated exactly zero dollars for the three years after its $1 billion acquisition in 2012. In both cases, the zero-revenue period was sustainable because someone else, like Facebook, absorbed the cost and eventually found the monetisation. Neither company’s founders had to answer to token holders during the years of building. The people who gave up something of value during that period, the users, were not promised financial returns. They were just using a free app.

Morpho’s token holders are not users. They are investors who have been told, implicitly, that the protocol will eventually generate value for them.

The second outcome is what Stripe and Twilio actually did, which is to charge from day one and reinvest the revenue rather than profit from it. Twilio has charged per message and per API call since it launched in 2008. It had revenue; what it lacked for over a decade was profit, because carrier fees ate into margins faster than volume could offset them. It took years of grinding to get there, but it was always charging. Morpho is not charging.

The third outcome is the commons: TCP/IP, Linux, the open-source stack. These are zero-revenue infrastructure stories where the people who built the primitive layer never expected or received financial returns, and the value was captured entirely by the layer above. This is actually the cleanest analogy to Morpho’s current architecture, which is why this is a problem. The TCP/IP engineers did not have token holders.

Morpho built open-source-style infrastructure and then attached a token to it that implies someone will eventually get paid. Those two things have not been reconciled. The reconciliation has been deferred to a governance proposal that does not yet exist.

Morpho Blue’s core code is 650 lines. It is immutable, meaning nobody can change it. Not Frambot, Apollo, a governance vote, or a court order. Coinbase generated $2.17 billion in loan originations on top of that because the rules cannot change beneath it. Apollo is committed to a 48-month accumulation schedule because the protocol will work the same way in 2028 as it does today. Every major institution that built on Morpho did so precisely because nobody is in charge.

When Morpho eventually tries to charge, when the legal paperwork is finished, when the fee switch governance proposal is finally written, it will be asking institutions that built on the premise that nobody controls this protocol to accept that somebody now does. The fee switch is a renegotiation of the terms under which every institution currently trusts the protocol. And the institutions with the most to lose from that renegotiation are the same ones whose presence makes Morpho worth charging for in the first place.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.