Hello,

In the 1970s, Bruce Bent and Henry Brown created the first-ever Money Market Fund. The idea was stupidly simple. Banks in America were capped at a 4.5% interest rate on savings due to a depression-era rule. While Treasuries were paying over 9%, you needed a minimum investment of $10,000 to buy them. So Bent and Brown decided to pool small deposits, buy Treasuries at scale, and pass the yield back. Today, money market funds are roughly an $8 trillion product.

Stablecoins have been running a similar play, except that the asset this time is private credit, a $2 trillion market where you need at least a million dollars just to get through the door. Yield-bearing stablecoins are being used to pool small deposits and channel them into credit.

Today, I will dig into how this happened and how Goldfinch, the first-ever attempt to do this with real-world money, just shut down, leaving $56 million in depositor funds stuck in Kenyan motorbike loans.

")

How Stablecoins Became the MMF of Private Credit

Banks in America used to provide roughly half of all debt capital to businesses and consumers in the 1990s, but today that number is roughly 20%. This was because, after 2008, new capital rules came into effect, making it too expensive for banks to hold leveraged loans on their balance sheets. Due to this, they withdrew from mid-market lending altogether, and private credit funds took over.

Apollo, Blackstone, and KKR raised capital from pension funds and insurance companies to start lending to companies that banks had walked away from, charging a steep premium because these borrowers had no other option.

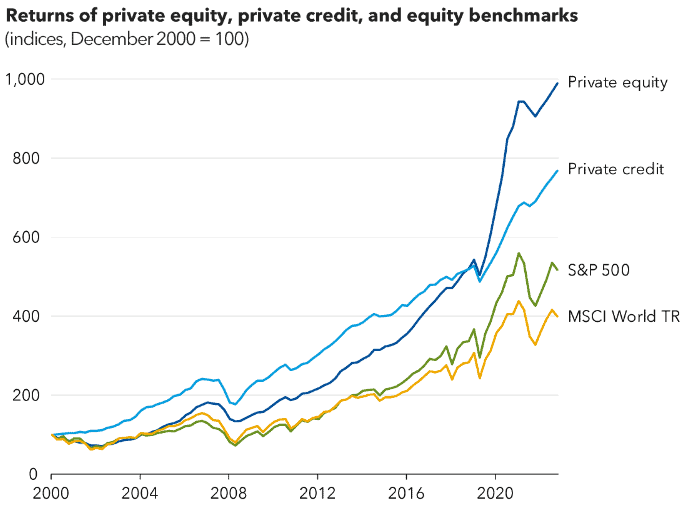

The market has grown from under $200 billion in 2008 to over $2 trillion today, and almost all of that capital has come from institutional investors writing checks of $5 million or more.

One of the biggest reasons why there is a million-dollar minimum for access to private credit loans is that they are hard to manage. Every deal needs due diligence, restructuring, and years of monitoring. Running a fund with ten institutional LPs who each put in $50 million is far more manageable than one with retail investors, each putting $500, and often even the economics don’t work at scale. That’s why, for the last decade, only pension funds and insurance companies had access to this type of yield, earning anywhere between 8% and 12%.

This is when yield-bearing stablecoins changed the game, much like when Bent and Brown opened Treasury access in the 1970s. The paperwork still happens at an institutional scale, with funds like Apollo underwriting and managing risk, but now a tokenised feeder fund can accept deposits of any size and channel them into the institutional strategy without needing to manage thousands of individual investors.

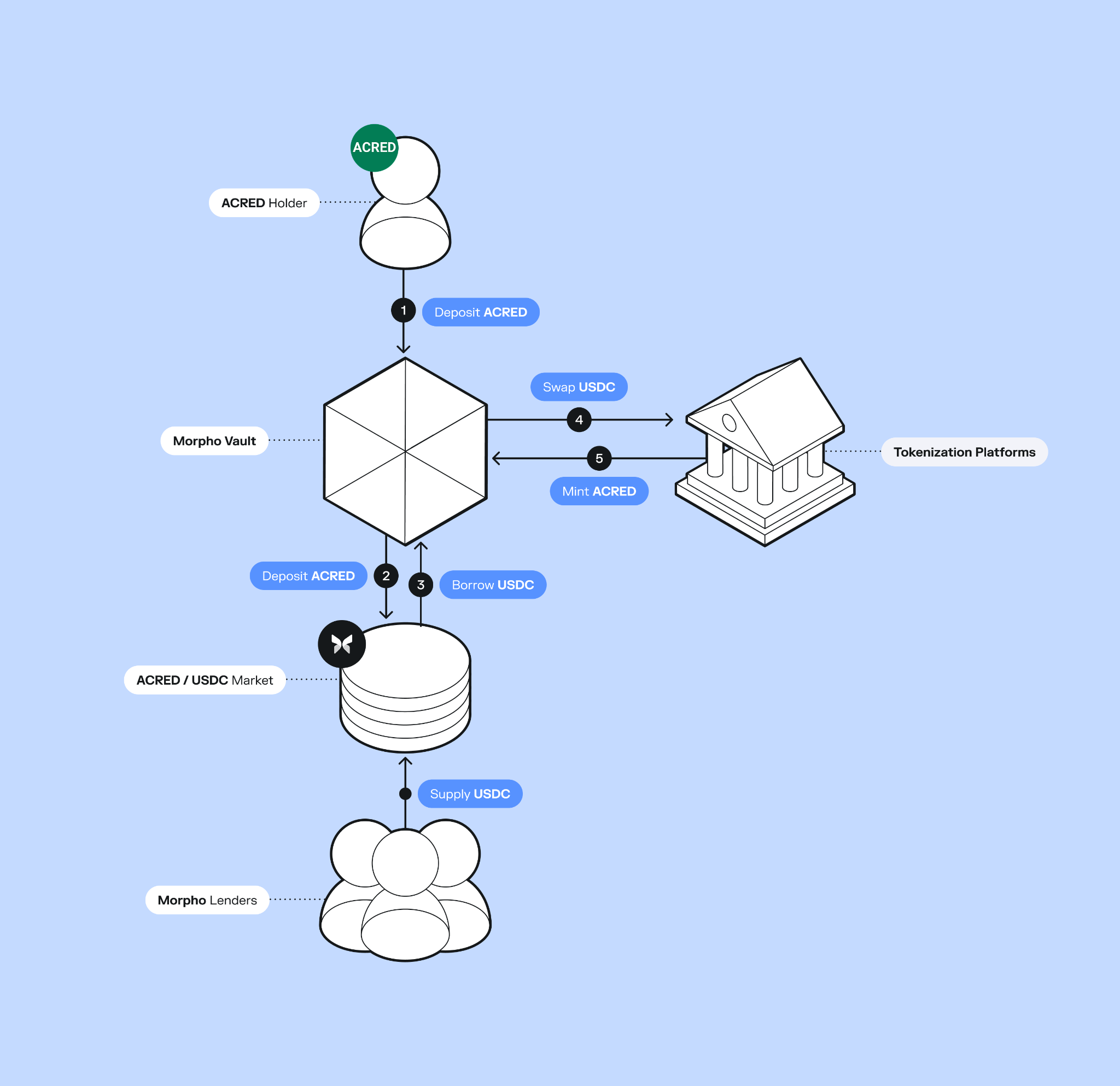

Apollo recently launched a tokenised fund, ACRED, and has already seen $109 million flow into its diversified Credit Fund. Investors can even deposit it as collateral on Morpho to borrow against and loop for leveraged yield.

Figure has built an entire on-chain lending stack that has originated $21 billion in loans, secured a Nasdaq listing, and launched YLDS, a yield-bearing stablecoin with $376 million in circulation. Other protocols like Pyse and Glow went even more granular, tokenising solar energy projects so that investors can invest a few hundred dollars to fund installations in developing markets and earn APYs paid from monthly electricity bills.

This does not mean minimums have disappeared from the funds themselves. ACRED still requires $5 million for direct entry. But once the fund is tokenised, the token trades on secondary markets with no minimum, and it works with DeFi in ways traditional fund shares never could.

In traditional private credit, your capital is locked for years with quarterly redemptions capped at 5%. But on-chain, it’s composable and liquid around the clock. And for firms like Apollo and Figure, this gives them access to $315 billion in stablecoin capital actively chasing yield, and tokenising their funds provides direct access to that pool as a new distribution channel without having to build retail infrastructure from scratch.

A year ago, total on-chain private credit was just $400 million; today it’s $5.87B, a 15x jump in twelve months, which is still just 0.30% of the $2T global private credit market with half of all the new stablecoin supply in Q1 2026 being from yield-bearing, which means the bulk of new stablecoin capital is now chasing active yield instead of just a dollar-denominated peg.

And because every dollar of on-chain credit can be used as collateral and looped through DeFi protocols, the effective financial activity it generates is multiples of the dollar amount.

Take ACRED, for example. An investor deposits $10,000 on Morpho, borrows $7,000 in USDC against it, buys more ACRED with that USDC, and deposits it as collateral again. That one deposit will now be generating over $17,000 in credit exposure. Compare that to traditional private credit: the same $10,000 will just sit in the fund for 5 years with nothing. But on-chain, it compounds across multiple layers simultaneously, which is why the market can scale faster than its raw dollar size suggests. But it also means that when a loan underneath goes bad, the losses can ripple through every layer of the loop.

Tokenising doesn’t mean the underlying risks are also mitigated. Often, these risks go unnoticed as new money keeps coming in, and these fresh deposits fund any redemptions. But as inflows slow, the differences between token promises and what the loan can deliver start to show up. Investors try to exit, but liquidity is lacking, or the token’s price disconnects from its underlying value.

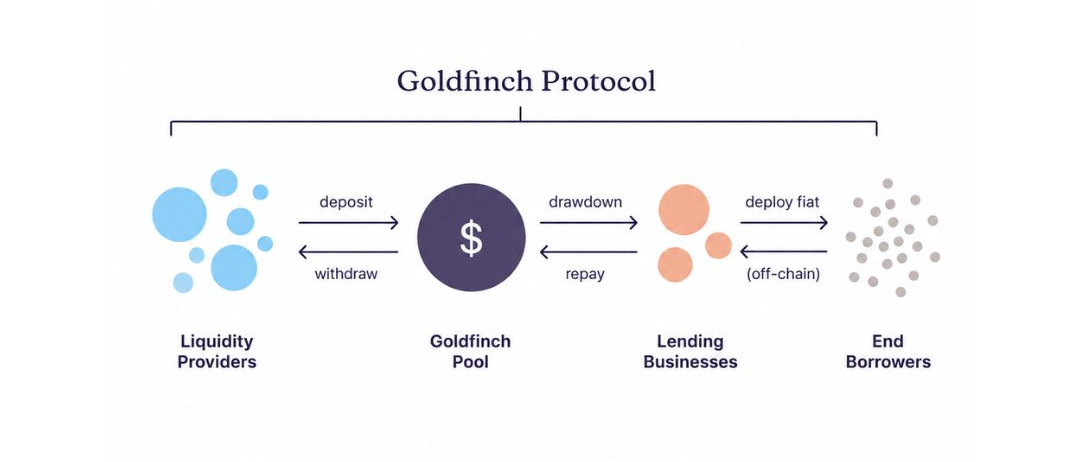

Something like this happened with Goldfinch; it was one of the first protocols launched in 2021 to put private credit on-chain, and it recently had to shut down after $56 million in depositor funds was trapped across Kenya and Nigeria.

What Goldfinch Got Wrong

Goldfinch raised $25 million from a16z in 2021 to route capital from crypto, which was earning barely 2 to 3% in DeFi lending pools at the time, into businesses across Africa and Southeast Asia whose borrowers were paying 15 to 25% on loans because their local banks wouldn’t serve them.

The idea was to let anyone with USDC deposit into a Goldfinch pool, and the smart contract would then route it into a borrower tranche within seconds. But underwriting a loan to a motorcycle-financing company in Nairobi means someone has to understand Kenyan transport economics and verify the borrower’s books in person. They also might have to physically show up at their office if repayments stop.

But these things are not possible on a blockchain. Once USDC was converted into Kenyan shillings and deployed in the lending book, depositors had no way of knowing how their money was being used, whether the borrower was financially healthy, or whether the loan terms were even being honoured. All the information that mattered for the loan’s performance was off the chain and held by borrowers in countries most depositors had never visited.

Which is why it took months for anyone to notice that Tugende Kenya moved $1.9 million from its $5 million facility to Tugende Uganda in 2022 without authorisation. Nearly 40% of the loan had been redirected to a different legal entity in a different country. At the same time, depositors continued earning what they believed was 10 to 12% interest, completely unaware that the capital backing their returns had gone somewhere the loan agreement never covered.

A traditional private credit lender finding a covenant breach this severe would call the loan and force restructuring within days, but Goldfinch depositors found out through a governance forum post, and their only option was to vote on a proposal that had no legal authority to seize assets or audit what was left.

By 2023, Tugende had defaulted in full and gone completely dark. Of the 24 pools that Goldfinch originated over its $113.3 million lifetime, only 13 ever fully repaid. The remaining 8 held $53.82 million in outstanding loans, and not a single one was performing on its original terms. Most were in restructuring and paying less than $51,000 per pool per month, which means that recovering the full $53.82 million at that rate would take between 8 and 15 years.

Goldfinch had absorbed all the risks of currency volatility and limited credit histories in emerging markets, while having almost none of the infrastructure that traditional lenders spend decades building and managing to mitigate those risks. For example, a bank lending in Kenya has local offices and regulatory relationships that give it leverage when deals go sideways.

But Goldfinch had routed capital from anonymous wallets across the globe into the same category of borrowers without any of that scaffolding, widening the information gap between lender and borrower beyond that in a conventional deal and leaving depositors with close to zero ability to intervene when things fell apart.

Moving money on-chain accounts for only about 10% of what lending requires. The other 90% is underwriting and capital recovery, which is hyper-local and expensive to build. Underwriters in this category need to build the credibility floor for an entire asset class that is still earning its right to exist. Every dollar lost to weak underwriting makes the next institutional partner harder to bring on-chain and the entire asset class less credible. And the hard part of credit has nothing to do with what happens on-chain, and anyone building in this space who doesn’t understand that is building the next Goldfinch.

That’s all for today!

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.