Hello

A lot of crypto conversations still orbit around the speed, cost and finality of infrastructure. They are all important, I agree. But they all rank far lower than something more basic and fundamental when it comes to adoption. Something qualitative and human. I wonder how builders expect a customer to adopt a new technology when they can’t help them understand how the it’s going to improve their life.

Humans evolved as a dominant social animal species because of our superior cooperation and communication skills. Yet, today, we have sidelined the very communication aspect of telling why a new technology matters in the pursuit of seeking better adoption.

Although the crypto landscape has witnessed some of the most useful technologies and products being built, few have focused on building the all-important relationship layer. I am thinking of trust, a user-friendly interface, the regulatory comfort that makes a treasurer or a retail saver actually move their money.

It is true that good infrastructure enables better movement of money, but a robust relationship layer is what can direct and trigger that move.

In today’s guest op-ed, Sebastien Davies, Partner at Primal Capital, writes about how distribution is the mechanism that turns infrastructure into outcomes.

Onto the story,

Prathik

P.S.: This was first published on Interop Markets.

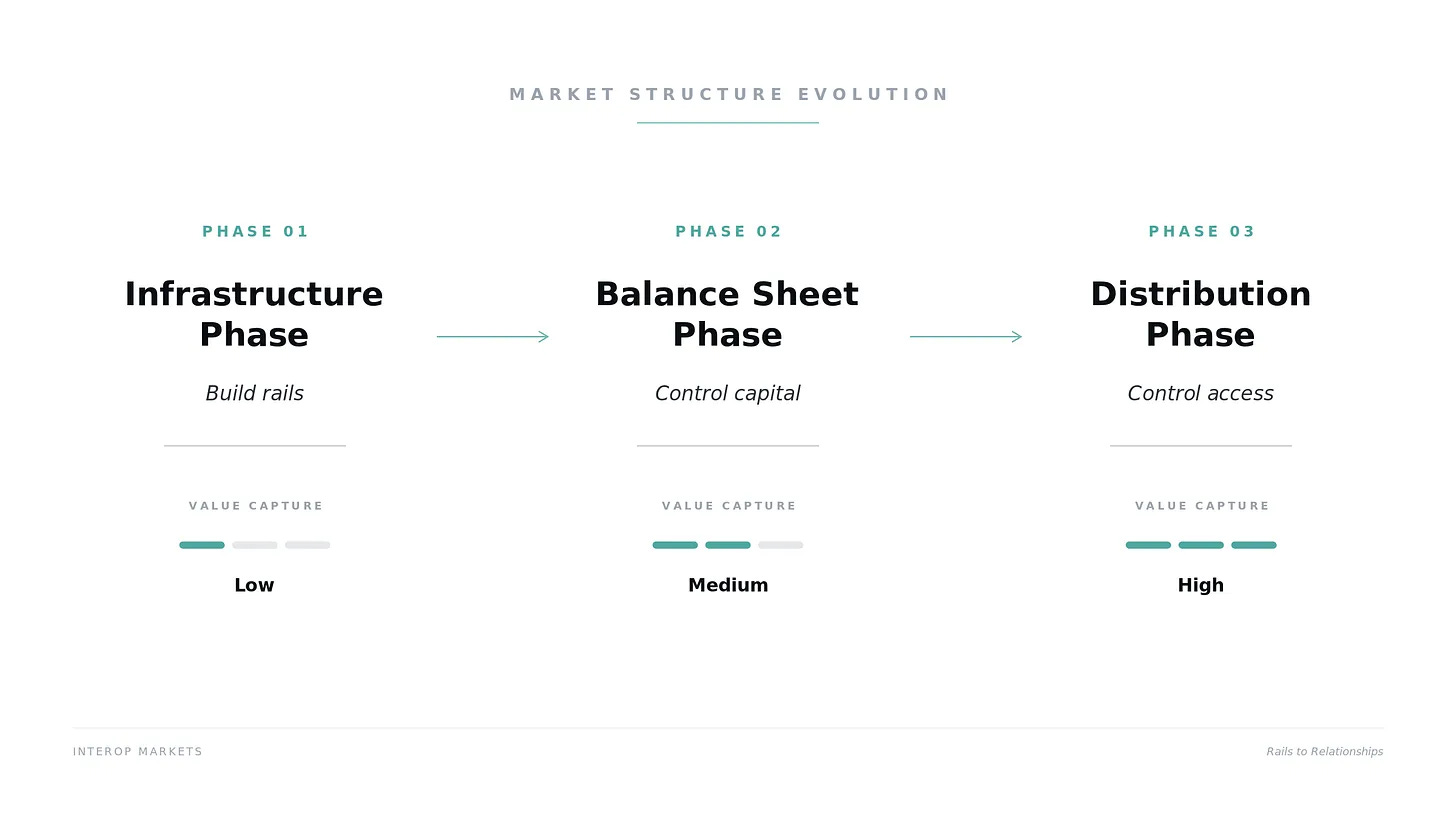

The defining delusion of the last ten years in crypto was the “Field of Dreams” fallacy. Builders and investors operated with the assumption that properly engineered rails would automatically magnetise the world’s capital. This was the Infrastructure Phase, a massively capital-intensive epoch dedicated entirely to building empty containers. Between 2020 and 2024, the fundamental barriers to entry were strict regulatory prohibition and structural impossibility. Fiduciaries lacked the legal mandate to participate, and the baseline plumbing of custody, execution, and reporting simply did not exist at an enterprise-grade level. The industry deployed billions of dollars and dedicated millions of hours to engineering and lobbying solely to overcome these compliance and mechanical realities.

By 2025, the industry reached a quiet consensus. The “Battle for the Rails” had effectively ended in a draw between standardised, institutional-grade multi-party computation (MPC) custody stack and regulated stablecoin frameworks. The mechanical question of how to safely move a billion dollars on-chain has been answered. This technical victory, however, produced a troubling realisation. Infrastructure is fundamentally a commodity. It is a necessary precursor to activity, but it remains entirely agnostic regarding value capture.

In the traditional financial hierarchy, power is rarely held by the entity providing the ledger. It is held by the entity that controls the entry point. We are now witnessing the pivot from the Infrastructure Phase to the Balance Sheet Phase, but the catalyst for this transition is not more technology. It is distribution.

The Friction of the Blank Slate

Infrastructure enables a better system, but it does not account for the “gravity” of legacy balance sheets. A corporate treasurer does not evaluate a new financial rail based on its cryptographic elegance or its sub-second finality. They evaluate it based on the friction required to reach it.

Historically, financial power has accrued to those who minimise this activation energy. In the 1970s, the emergence of Money Market Funds (MMFs) offered higher yields than traditional bank deposits. However, the technology (the ability to pool short-term debt) was not the breakthrough. The breakthrough was distribution through retail brokerages like Merrill Lynch, which placed the “new container” directly into the investor’s existing workflow. The capital moved because the distribution channels made the migration invisible.

In digital finance, we see a similar pattern. The existence of a high-yield, on-chain Real-World Assets (RWA) vault is irrelevant if it sits outside the institutional user’s primary interface. Infrastructure provides the destination, but without distribution, the “audience” never leaves the traditional bank’s lobby.

Distribution Directs Liquidity

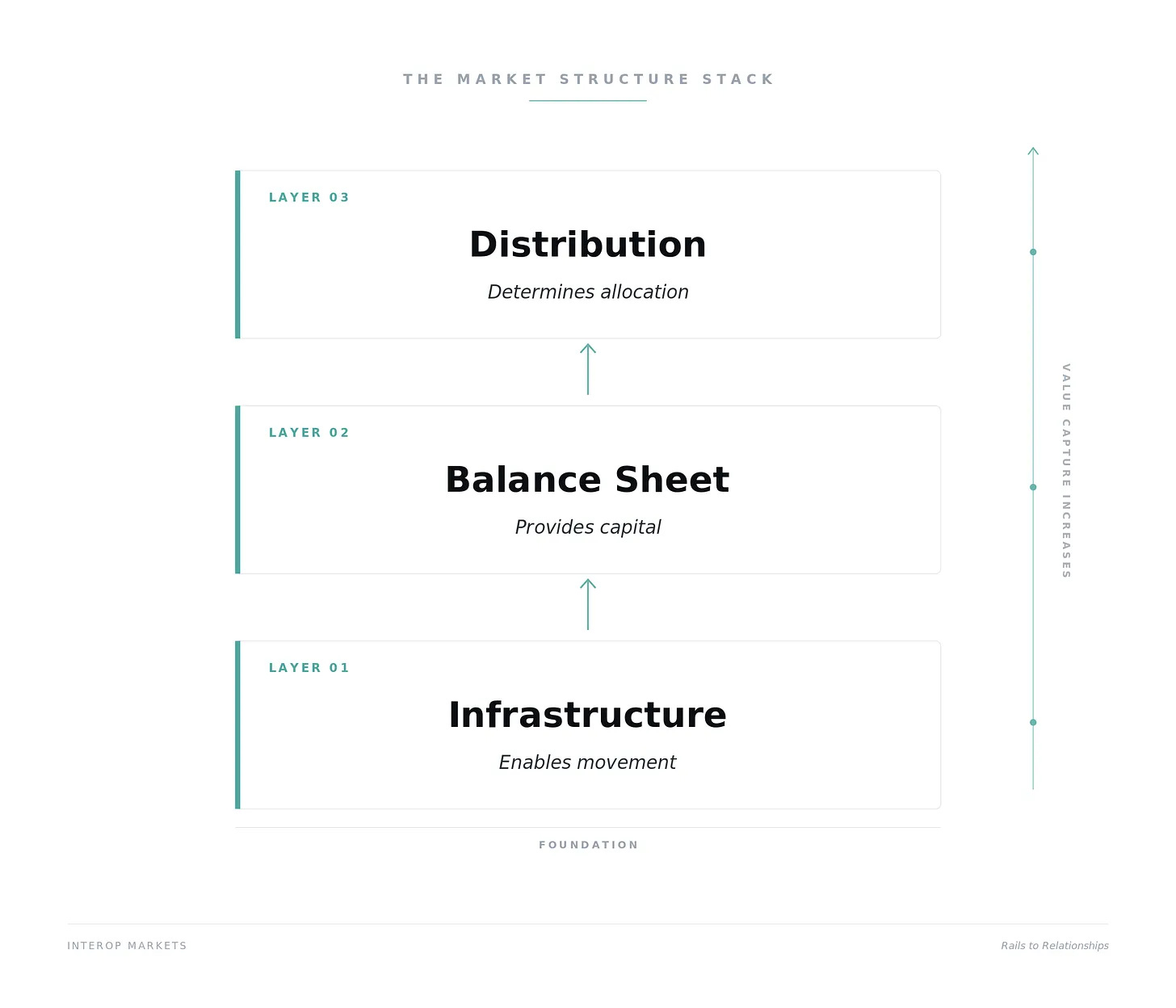

If the balance sheet is the strategic asset that determines the winner of the interest rate spread, distribution is the navigator that directs the flow toward that asset. We must view distribution as the “connective tissue” of market structure. It encompasses the presence, trust, regulatory licenses, and API integrations that allow capital to reside in a specific container.

The current market structure is bifurcated. On one side, we have highly efficient, crypto-native infrastructure capable of managing programmable liquidity with unprecedented precision. On the other, we have $100 trillion in institutional balance sheets sitting in “static” containers (traditional bank accounts and custody systems) where returns are suppressed by layers of intermediation.

Value capture in the coming decade will bypass protocols competing purely on marginal fees or throughput. The economic rents will accrue directly to the “Web2.5“ hybrids that monopolise both the customer interface and the regulatory perimeter. These new gatekeepers serve as the critical bridge, offering the “one-click” migration of a balance sheet from a zero-yield checking account into a 24/7 programmable liquidity pool.

The Shift in Gravitational Centres

We are moving into an era in which the distinction between “crypto” and “finance” is dissolving, with a battle for the front-end relationship. As infrastructure becomes commoditised and invisible, the “Interface War” begins.

When a treasurer can park cash in a tokenised Treasury fund as easily as they can in a commercial bank account, one of the bank’s primary moats (the difficulty of leaving) is challenged. However, this shift occurs only when the digital container is distributed through the treasurer’s existing terminal, auditor, and risk framework.

Infrastructure enables, balance sheets fund, and distribution allocates.

In the “Infrastructure Phase,” we treated liquidity as a stagnant pool that merely needed a better pipe. We assumed that superior efficiency alone would naturally drain it. This fundamentally misunderstands financial physics. Institutional capital operates as a dense bundle of permissions, risk mandates, and operational habits. Distribution is the force that actively reconfigures those bundles.

Distribution dictates the path of capital. In any competitive market, economic power accrues to the entity that owns the customer’s attention, systematically commoditising the underlying providers, who still earn a rent.

The Anatomy of Institutional Distribution

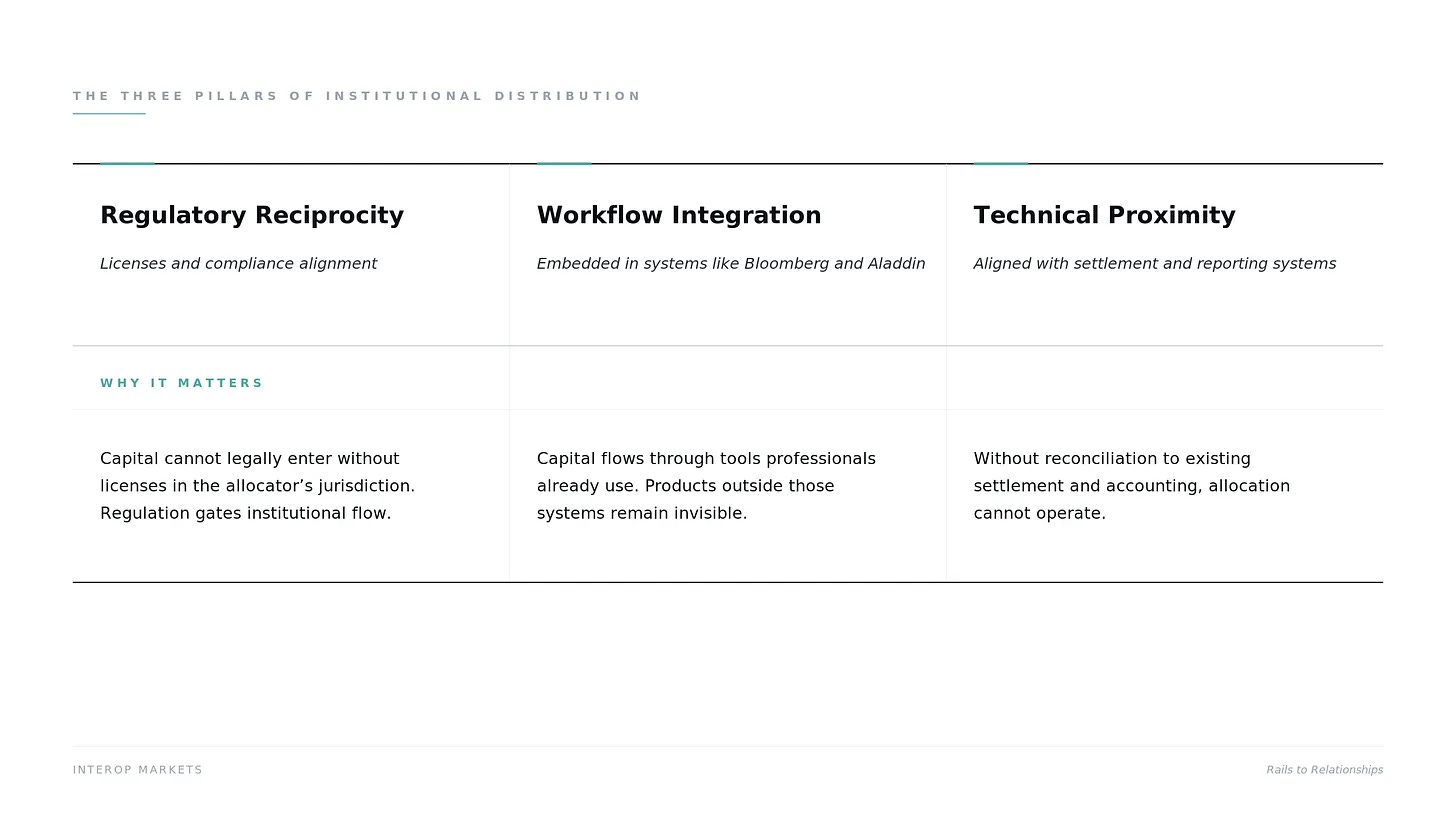

For institutional allocators, distribution represents a formidable, three-dimensional moat:

Regulatory Reciprocity: The access provider must hold licenses in the allocator’s exact jurisdiction and strictly comply with the allocator’s specific fiduciary requirements.

Workflow Integration: The asset has to sit inside existing enterprise command centres, integrated directly into systems like Bloomberg Terminals, BlackRock’s Aladdin, or State Street custodial dashboards.

Technical Proximity: The infrastructure must execute within existing legacy settlement cycles and integrate directly into the accounting software used for reporting.

Without these pillars, even the most attractive digital assets remain peripheral. Distribution turns them into balance-sheet allocations.

The “Default” Advantage

The history of financial infrastructure shows that technical elegance often loses to entrenched distribution. The persistence of the SWIFT network and the ACH system illustrates this dynamic. While both are modernising to improve speed and reduce friction, modern blockchain architectures outpace them in programmability, transparency, and marginal cost. Yet these legacy systems remain deeply embedded in enterprise connectivity. Corporate treasuries, payroll providers, and commercial banks are already wired into them.

The true friction of switching extends far beyond transaction fees. It sits in the operational risk of overhauling an entire corporate stack. As a result, value accrues to the gatekeepers who provide seamless compatibility with existing systems. The defining infrastructure of this cycle will be built by those who can bridge legacy capital into modern digital frameworks.

Distribution as a Filter for Signal

In a world of programmable liquidity, the sheer volume of “containers” (protocols, vaults, and yield strategies) creates a massive discovery problem. An institutional treasurer cannot, and will not, perform due diligence on 50 different DeFi protocols. They require a distributor to act as a curator.

This is where the hybrid model begins to take hold. These entities act as the institutional front end, performing risk assessment and compliance, and distributing structured yield to their clients. The underlying infrastructure provides the yield, and the balance sheet provides the scale, but the trusted orchestrator captures the highest-margin economics by controlling the point of access.

Redirected Flow: We are beginning to see the first signs of this “Distribution Arbitrage.” Neobanks and crypto-first exchanges are no longer just offering Bitcoin trading. They are beginning to introduce tokenised money market funds and stablecoin-based yield products directly alongside traditional savings accounts.

When a user’s primary banking interface offers 5% on a tokenised product and 0.5% on a traditional deposit, and the switch requires no change in workflow, the distribution channel has effectively broken the bank’s hold on that capital. The infrastructure was ready years ago. The balance sheet was always there. It is the distribution and integration into the financial service interface that finally trigger the migration.

Victorious Networks

Financial history is instructive here. The firms that scaled were the ones that made their products accessible to existing pools of capital and integrated them into established systems. Distribution, not just design, is what translated innovation into adoption.

Distribution via Jurisdiction

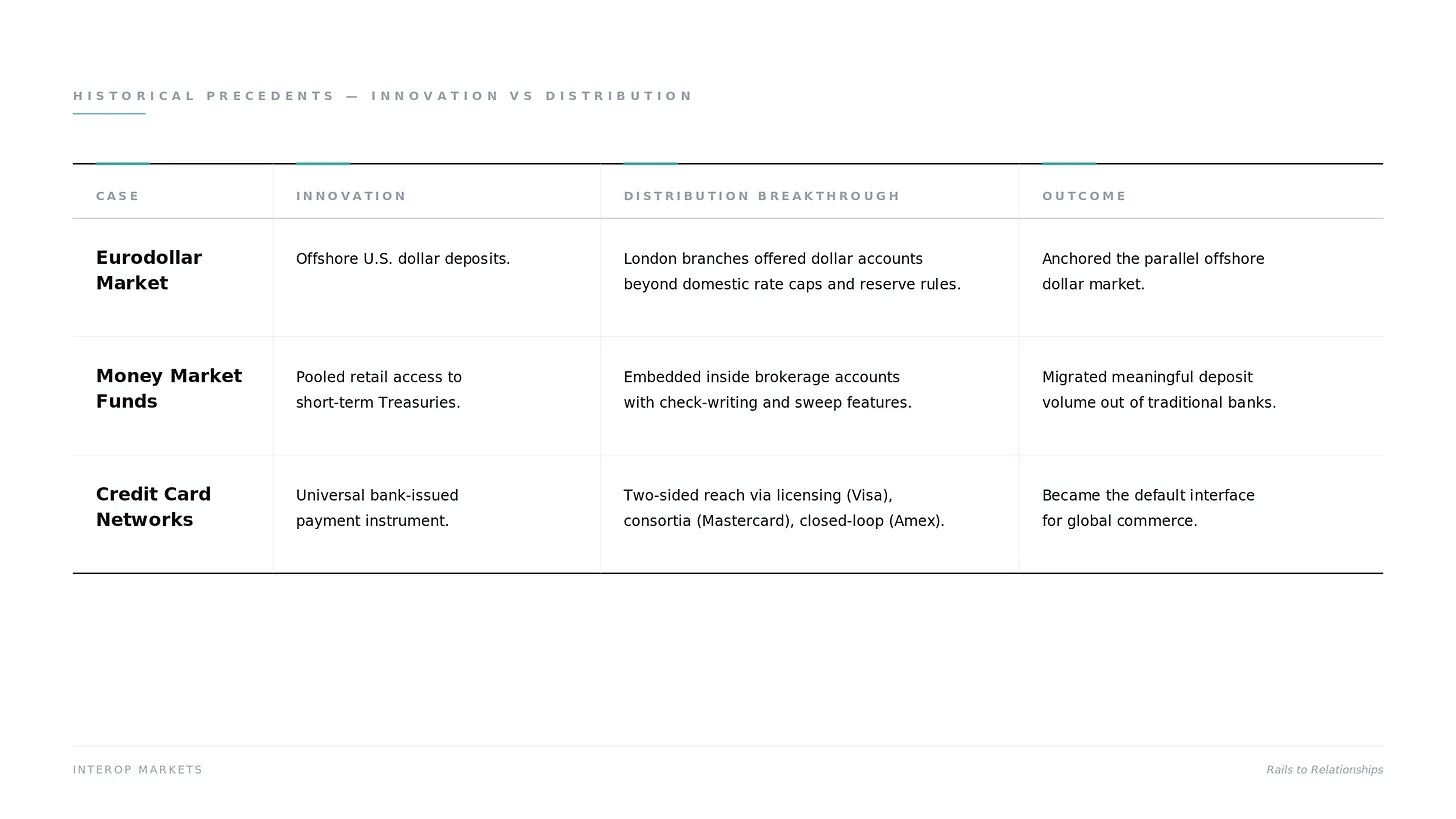

The rise of the Eurodollar market in the 1960s provides the definitive historical precedent for balance sheet migration driven entirely by distribution. The underlying infrastructure (the US Dollar and commercial bank ledgers) remained static. The catalyst was a pure geographic shift in the access point.

By launching dollar-denominated accounts in London, financial institutions systematically bypassed domestic interest rate caps and reserve requirements, engineering a profound innovation in regulatory distribution. This manoeuvre provided global capital with a highly-optimised container maximising both utility and yield. Establishing this offshore channel triggered a balance-sheet migration so complete that it permanently forged the parallel global financial system operating today. The currency rail held firm, while the geographic pivot in distribution simply unlocked a vastly superior economic container.

The Interface Revolution

In the late 1970s, as inflation surged, traditional bank deposits became a liability for savers because interest rates were capped. The “Infrastructure” for a solution (short-term government debt) already existed. However, the average investor could not easily buy T-bills in small increments.

The rise of the money market fund is a useful example. Firms like Fidelity and Merrill Lynch embedded these funds into brokerage accounts with check-writing and sweep features, allowing them to function like cash balances. This made higher-yielding instruments accessible within familiar workflows and gradually shifted a meaningful share of cash away from traditional deposits.

Integration Over Innovation

The rise of card networks is a useful example. In the 1950s and 60s, many banks launched proprietary travel and entertainment cards. Most failed to scale, but it had nothing to do with inferior plastic or slower processing times. They never established distribution across both sides of the transaction.

The networks that succeeded solved this problem in different ways. Visa, originally BankAmericard, expanded through a licensing model that allowed thousands of banks to issue cards, leveraging existing customer relationships. Mastercard followed a similar path through a bank consortium, building broad acceptance and reach. American Express took a different approach, issuing cards directly and owning both the customer and merchant relationships within a closed-loop system.

The structure varied, but the outcome was consistent. Each model achieved scale by embedding itself into both sides of the transaction, becoming the default interface for commerce by controlling access.

The Lesson for Digital Assets

These precedents reveal a recurring law: Infrastructure is the invitation, but distribution is the mandate.

● The Eurodollar proved that capital will migrate to wherever the distribution is most efficient and least constrained.

● The MMF proved that the interface (cheque-writing on a brokerage account) determines which container the balance sheet chooses.

● The Credit Card proved that leveraging existing trust networks is faster than building a new network from scratch.

In 2026, the crypto-native system is still in its early stages of distribution. The infrastructure for yield and continuous settlement is already in place, but it has not yet been integrated into the interfaces institutions rely on. Adoption will come from embedding these capabilities into existing workflows, from consumer financial apps to the treasurer’s daily operating environment.

Distribution in Digital Assets

The 2026 landscape makes one thing clear. Decentralised infrastructure is in place, but distribution remains concentrated. With a total market cap of roughly $2.5 trillion, economic activity is already clustering around a small number of access points.

The relevant question is where default relationships are forming. These are the platforms that sit at the interface with the user, and increasingly, at the centre of capital allocation.

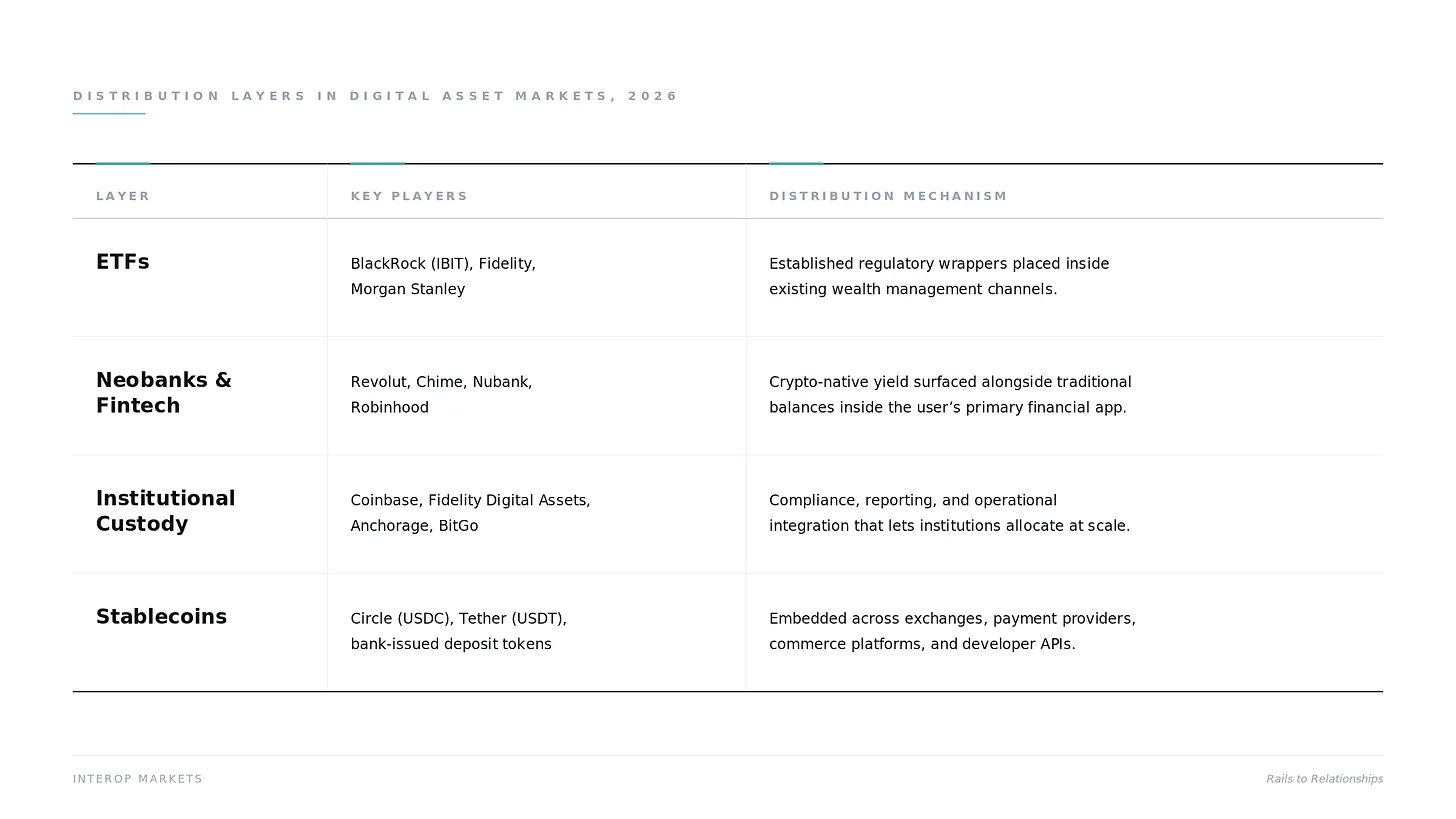

ETF Familiarity

The approval and maturation of spot ETFs have provided a clear example of how distribution drives adoption. By placing digital assets within an established regulatory wrapper, firms like BlackRock, Fidelity Investments, and Morgan Stanley have made them immediately accessible through existing wealth management channels.

This has translated into scale. As of Q1 2026, U.S. spot Bitcoin ETFs hold over $128 billion in assets, reflecting not just demand for the asset, but the reach of the distribution layer through which it is delivered.

BlackRock’s IBIT has emerged as a benchmark because it sits inside these systems and is backed by one of the most trusted brands in global finance. It appears alongside other ETFs, within familiar workflows and allocation models. Adoption followed integration, not novelty. In effect, the asset class has been mapped directly onto the balance sheet workflows of the world’s largest pools of capital.

Neobank Proximity

A different form of distribution is emerging through neobanks and fintech platforms. Applications like Revolut, Chime, Nubank, and Robinhood increasingly serve as the primary financial interface for a large segment of users. Within these environments, new products do not need to be discovered. They simply appear alongside existing balances.

As crypto-native yield, whether through staking or tokenised assets, is placed next to traditional accounts, the decision to allocate becomes a matter of interface design rather than infrastructure. The distinction between a USD balance and a USDC balance begins to collapse into a simple choice within the same system, subject to what these platforms are permitted to offer.

In 2026, roughly 30% of American adults hold some form of crypto exposure. For many, their primary relationship is no longer with a physical bank, but with an application. Distribution, in this context, is not about access to a new system. It is about integration into the one users already rely on.

Custody Opportunity

Firms like Coinbase, Fidelity Digital Assets, Anchorage Digital, and BitGo are becoming core distribution nodes for institutional capital.

Their role extends beyond safekeeping. They provide the compliance, reporting, and operational integration required for institutions to participate at scale. In this context, custody becomes the interface through which capital is allocated, not just where assets are held.

As these platforms expand into trading, financing, and settlement, they increasingly resemble full-service financial environments. The underlying infrastructure remains important, but allocation decisions are made through these controlled interfaces. Distribution, in this layer, is defined by permission, integration, and trust.

Stablecoin Settlement

Stablecoins are moving beyond their role within crypto markets and becoming part of broader financial and operational workflows. Their relevance now extends into payments, settlement, and treasury functions, where they are increasingly integrated into existing systems.

Firms like Circle have focused on building this distribution through partnerships with banks, payment providers, and financial platforms. The objective is not just issuance, but placement within the systems where transactions already occur.

A similar pattern is beginning to emerge in software and AI-driven environments. As developers build applications and autonomous agents that operate programmatically, stablecoins are being integrated as a native payment mechanism. In this context, adoption will follow the stablecoins that are most accessible within developer tools, platforms, and APIs, extending distribution beyond financial interfaces into software itself.

Emerging Hierarchy

The structure has shifted. Early efforts focused on building the rails. Today, the advantage lies with those who control the interface.

Whether it is an ETF ticker, a neobank application, or a prime brokerage platform, the entities capturing the economics are the ones that present new capabilities within familiar systems. They translate complex infrastructure into formats that align with existing habits, and in doing so, become the default point of access.

This is what ultimately determines where balance sheets move. Capital does not migrate because the infrastructure improves. It migrates when the interface makes allocation seamless within the systems it already uses.

Stablecoins as the Clearest Example

Stablecoins are the purest manifestation of the distribution thesis. They are not merely “digital dollars”; they are the primary distribution vehicle for the US financial system in the 21st century. While the industry spent years debating the merits of different Layer 1 protocols, stablecoins quietly became the “killer app” by solving a distribution problem rather than a technical one. They made the world’s most trusted balance sheet (the US Treasury) accessible to anyone with an internet connection, 24/7.

Stablecoins are introducing a new form of competition in the deposit market. They package short-duration government-backed assets into a programmable, portable, and continuously accessible format. As distribution improves, capital can move more easily between traditional accounts and these digital alternatives.

The Utility Gap

The persistence of Tether (USDT) is the ultimate proof that distribution beats “better” infrastructure. For years, critics pointed to USDC’s superior transparency, regulatory standing, and institutional backing. In a vacuum, USDC is the “better” product.

Tether established early distribution in offshore trading markets and across many emerging economies. It became a primary liquidity instrument across exchanges and a widely used medium for cross-border transactions.

By the time regulated alternatives entered the market, Tether was already deeply embedded in trading, settlement, and informal financial flows. Its presence across platforms and use cases created a level of integration that is difficult to displace.

Programmable Liquidity

The next phase of stablecoin distribution is the shift from passive holdings to active use. In 2026, these assets are increasingly being integrated into operational workflows.

This is showing up across a few key areas:

● In supply chain finance, large corporates are beginning to use stablecoins to accelerate settlement with suppliers, reducing reliance on traditional correspondent banking timelines.

● In commerce platforms, companies like Shopify and Stripe are enabling merchants to hold and manage balances in stablecoin form, introducing new options for liquidity management.

● In software environments, as applications and autonomous systems transact programmatically, stablecoins are being integrated as a payment layer for real-time, granular transactions.

In each case, adoption is driven by utility within existing systems rather than by exposure to new asset class.

Extending Distribution

Banks are responding to stablecoins by extending their own distribution. Deposit tokens and bank-issued digital assets will allow them to bring existing balance sheets onto new rails while maintaining control of access.

The objective is to preserve their role at the point where dollar-denominated value is accessed and deployed. As these instruments are integrated and eventually embedded into payroll systems, trade platforms, and software environments, the competitive dynamic shifts toward distribution.

As the market continues to scale, value accrues to the entities that control the interface through which transactions are initiated and managed.

Institutional Constraints

If the technical rails are ready and the economic incentives of the balance sheet are clear, why has the “Great Migration” not yet reached its terminal velocity? The answer lies in the final, and most formidable layer of the distribution moat: institutional friction. For a Chief Investment Officer or a Corporate Treasurer, capital allocation is governed by fiduciary responsibility, regulatory constraints, and operational requirements.

Distribution, in an institutional context, is the process of neutralising these three specific types of friction.

The Regulatory Distribution Gate

In the retail world, distribution is about “eyeballs.” In the institutional world, distribution is about licenses. An institution cannot legally park a balance sheet on a protocol, no matter how efficient, if that protocol sits outside its regulatory perimeter.

In 2026, distribution is increasingly concentrated around assets packaged within familiar legal and regulatory structures. Tokenised Treasury funds such as BlackRock’s BUIDL and Franklin Templeton’s FOBXX illustrate this pattern.

These instruments allow institutions to hold digital assets within existing investment frameworks, including structures that qualify as regulated investment companies. The format is new, but the pathway to allocation remains unchanged. These assets are accessed through standard brokerage systems and integrated into existing balance sheet management.

Workflow Lock-in

Large-scale capital does not move via a browser extension or a mobile app. It moves through established “Workflow Hubs” like the Bloomberg Terminal, Aladdin, or Charles River. These platforms are the ultimate distribution monopolies because they own the daily habits of the financial professional.

Early digital asset infrastructure was built as a parallel system. It required users to step outside their existing workflows to access it. For institutions, this created friction at the point of allocation.

Distribution is now shifting toward integration. Digital asset custody and exposure are being embedded into existing reporting, risk management, and portfolio systems. The objective is to make on-chain positions appear alongside traditional assets and behave consistently within the same operational framework.

Distribution Runs on Trust

In finance, trust is embedded in the distribution layer. Capital is allocated through counterparties that meet established standards for regulation, creditworthiness, and legal recourse.

The failures of major crypto intermediaries in 2022 and 2023, including FTX and Celsius, reinforced the importance of this framework. Established institutions such as BNY Mellon and State Street entering digital asset custody extend that layer of trust into new formats. Their role is not just to provide infrastructure, but to make digital assets compatible with existing expectations for balance sheet allocation.

Compliance at the Interface

The final piece of institutional distribution is integrating compliance into the interface itself. To access large pools of capital, digital asset systems must meet real-time requirements for transaction monitoring and anti-money laundering.

The firms gaining traction are embedding these controls directly into the point of access. By the time capital reaches the underlying system, the relevant checks have already been performed. Compliance, in this structure, becomes part of the distribution layer rather than a separate process.

This allows institutions to interact with programmable liquidity within established regulatory expectations, making allocation operationally viable at scale.

Where Distribution is Moving

As we look toward the 2027–2030 horizon, the “Interface War” is entering a phase of total invisibility. The goal of distribution is no longer to convince a user to “use crypto,” but to embed digital asset utility so deeply into existing platforms that the end-user (whether a retail saver or a corporate treasurer) doesn’t even realise they have migrated their balance sheet.

Invisible Distribution

The next great capital reallocation will be driven by Embedded Finance. In this model, the distribution node isn’t a bank or an exchange; it’s the software in which the economic activity already occurs.

● ERP Integration: SAP and Oracle sit at the centre of institutional financial workflows. As new forms of liquidity integrate into these systems, allocation decisions can be executed within existing treasury processes. When excess cash can be directed into tokenised instruments from within the same system used for cash management, the balance sheet moves as part of the workflow rather than through a separate interface.

● Supply Chain as a Ledger: Distribution is extending into supply chain and trade systems. Platforms that manage global logistics are beginning to integrate stablecoin-based settlement into their core software, connecting payment and transaction data more directly. As settlement becomes embedded within these workflows, financial activity moves closer to the underlying commercial process, creating new pathways for liquidity and credit to be applied in context.

Banking Platforms

Traditional banks have long served as the primary distribution layer for capital. Leading incumbents are now extending this role into programmable liquidity, leveraging their decisive structural advantages: decades of fiduciary relationships, comprehensive regulatory licenses across jurisdictions, deep integration into enterprise systems (Bloomberg Terminals, Aladdin, custodial dashboards), and the bedrock of deposit insurance together with general balance-sheet trust. These moats make it exceptionally difficult for neobanks or crypto-native platforms to achieve meaningful distribution at an institutional scale.

This advantage is decisive. While fintechs and crypto platforms can capture retail flows and smaller corporate wallets through superior user experience, meaningful “distribution arbitrage” at the multi-trillion-dollar institutional level remains limited. Banks do not need to out-innovate the underlying rails. They simply need to embed on-chain yield, settlement, and programmability into the interfaces and trust networks they already own. In this sense, the Interface War is one that banks are structurally wired to win.

● White-Label Liquidity: A hybrid model is beginning to take shape. Banks provide the trust, regulatory framework, and client interface, while yield is sometimes sourced from external, on-chain systems. In this structure, the bank’s role evolves from holding static pools of capital to managing flows across a broader set of financial environments.

● Deposit Tokens: The bank account of 2028 is likely to take a different form: a licensed deposit token that remains compatible with existing banking systems while extending into digital asset networks.

Agentic Distribution

A further shift is emerging as financial activity becomes more automated. As software systems and autonomous agents begin to manage capital, distribution extends beyond human interfaces and into code.

In this environment, allocation decisions are shaped by parameters such as integration, programmability, and capital efficiency. Systems that are easier to incorporate into software workflows become more likely to be used.

Distribution, in this context, is determined by presence within the tools and environments where these decisions are executed. Assets and protocols that integrate cleanly into developer ecosystems and meet operational and compliance requirements are more likely to be selected as default components within these systems.

The Point of Allocation

The arc of the last decade is clear. The underlying systems have been built. Capital can now move across them. What matters now is how that movement is directed.

The infrastructure is in place: secure custody, scalable networks, and programmable assets. These capabilities made participation possible. The next phase is defined by how capital is allocated across them.

As we have seen, capital does not move on technical capability alone. It moves when the pathway is integrated into existing systems and aligned with economic incentives. Distribution is what makes that movement operational.

Where Value Settles

As we move toward 2030, the distinction between digital assets and traditional finance becomes less relevant. The underlying systems are converging, combining the efficiency of new infrastructure with the stability of existing balance sheets.

In this environment, financial power sits with those who control the interface through which liquidity and collateral are accessed and allocated. The role of financial institutions evolves accordingly, from holding assets to managing flows across increasingly integrated systems.

The infrastructure is in place. The balance sheet is becoming more mobile. What determines outcomes now is distribution.

That’s it for today.

See you with the next one,

Sebastien Davies

Disclaimer: The piece was originally published in Edition 3 of Interop Markets

We will be featuring good writing and writers we love from time to time. If you have recommendations, send them our way.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.