God forbid a crypto project actually reads the federal regulations before writing code. For a decade, the entire industry has been tested and strangled by its own self-inflicted loopholes. Which is entirely fair.

You are moving massive, terrifying chunks of global money; you do not get a pass for sloppy homework. If you leave a structural gap open, the market or the state will violently correct you.

So, obviously, crypto developers spent years trying to smash that window with a brick. FTX offered tokenised stocks in 2020 and got completely vaporised by regulators. Gone. Then Binance tried it a year later and quit after ninety days because, I don’t know, pressure?

And Mirror Protocol built these synthetic copies that vanished into actual nothingness when the Terra blockchain collapsed (RIP). But why did we always assume the tech mattered more than the law?

But okay, if crypto's actual end game is to become the core infrastructure for global finance, we have to get the behaviour right. And learn to hate shortcuts. Ondo was built very carefully, but the capital flowing through is chaotic. Let’s look at the numbers to see how they got here and why the reality looks a teeny-weeny-tiny different.

Which brings us to Ondo Global Markets. They fixed the legal issue first. When they launched in September 2025, they skipped the offshore islands entirely, no Bahamas, no Seychelles, nothing beautiful for the eyes. They went straight to the SEC with a confidential registration statement, putting real shares inside a US broker-dealer.

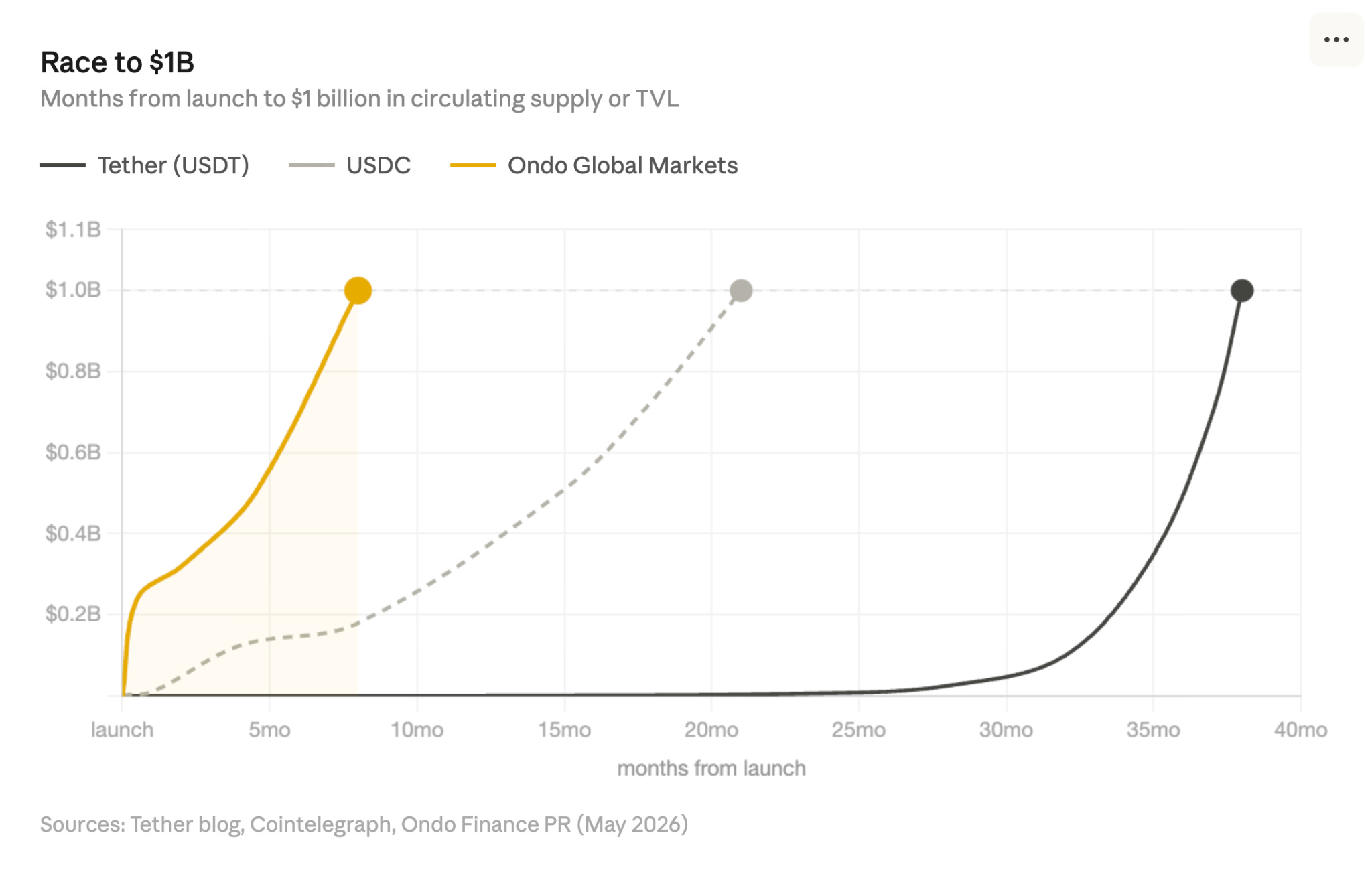

Tether hit $1 billion in circulation in December 2017, 38 months after launch. USDC crossed that line in July 2020, 21 months after Circle and Coinbase launched it. Ondo Global Markets crossed $1 billion in tokenised stocks in 8 months. The comparison is a little weird; let me explain why.

Stablecoins totalling $1 billion were held by thousands of traders across dozens of exchanges and used daily as dollar proxies by people who could not access USD bank accounts.

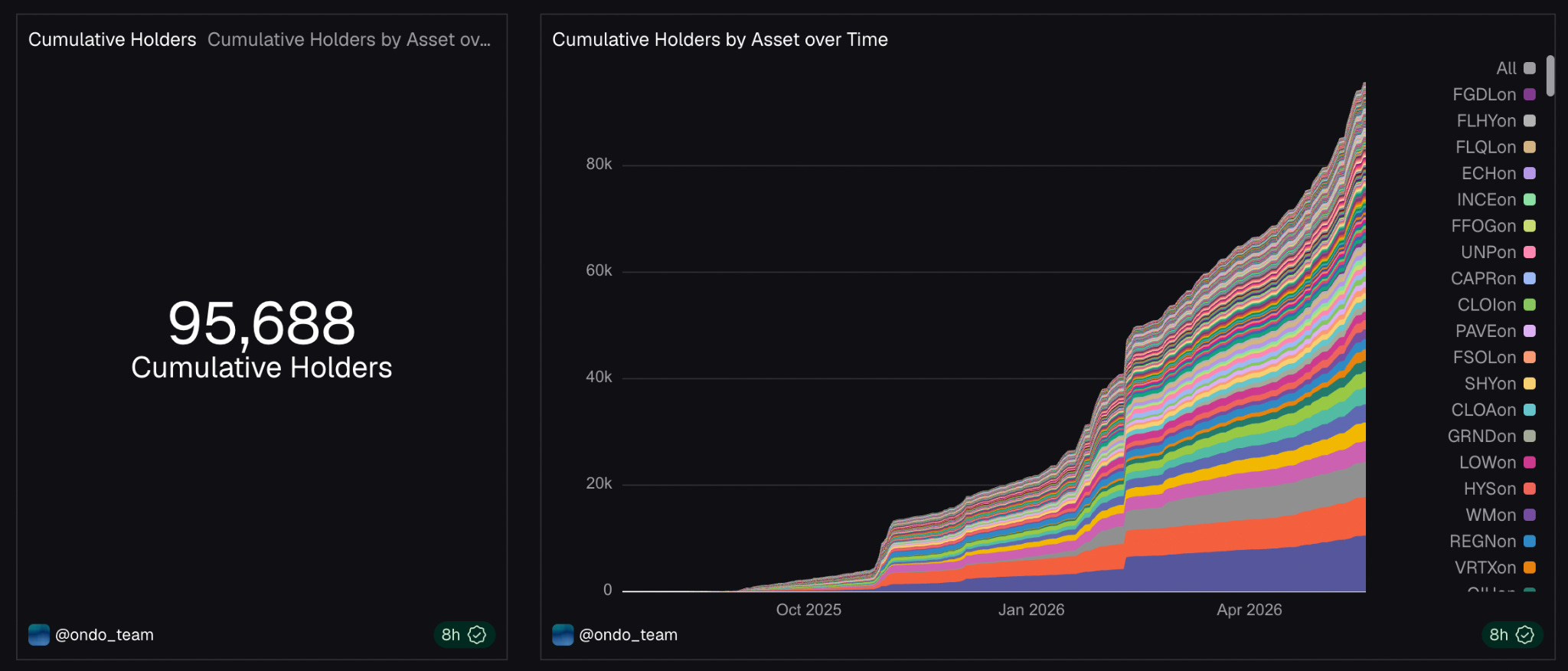

Ondo’s $1.03 billion value locked is now spread across 95,688 wallets, an explosive doubling of its user base in just a matter of weeks. Yet, the underlying behaviour remains highly concentrated, with a legacy cohort of just 81 whale wallets historically controlling 84% of the capital. The retail long tail is massive but has a tiny footprint; 56% of all wallets hold less than $20, and 72% of users flip their positions in less than a day.

I highly doubt this is what “the brokerage account is next” looks like. It might be what it looks like before it looks like that.

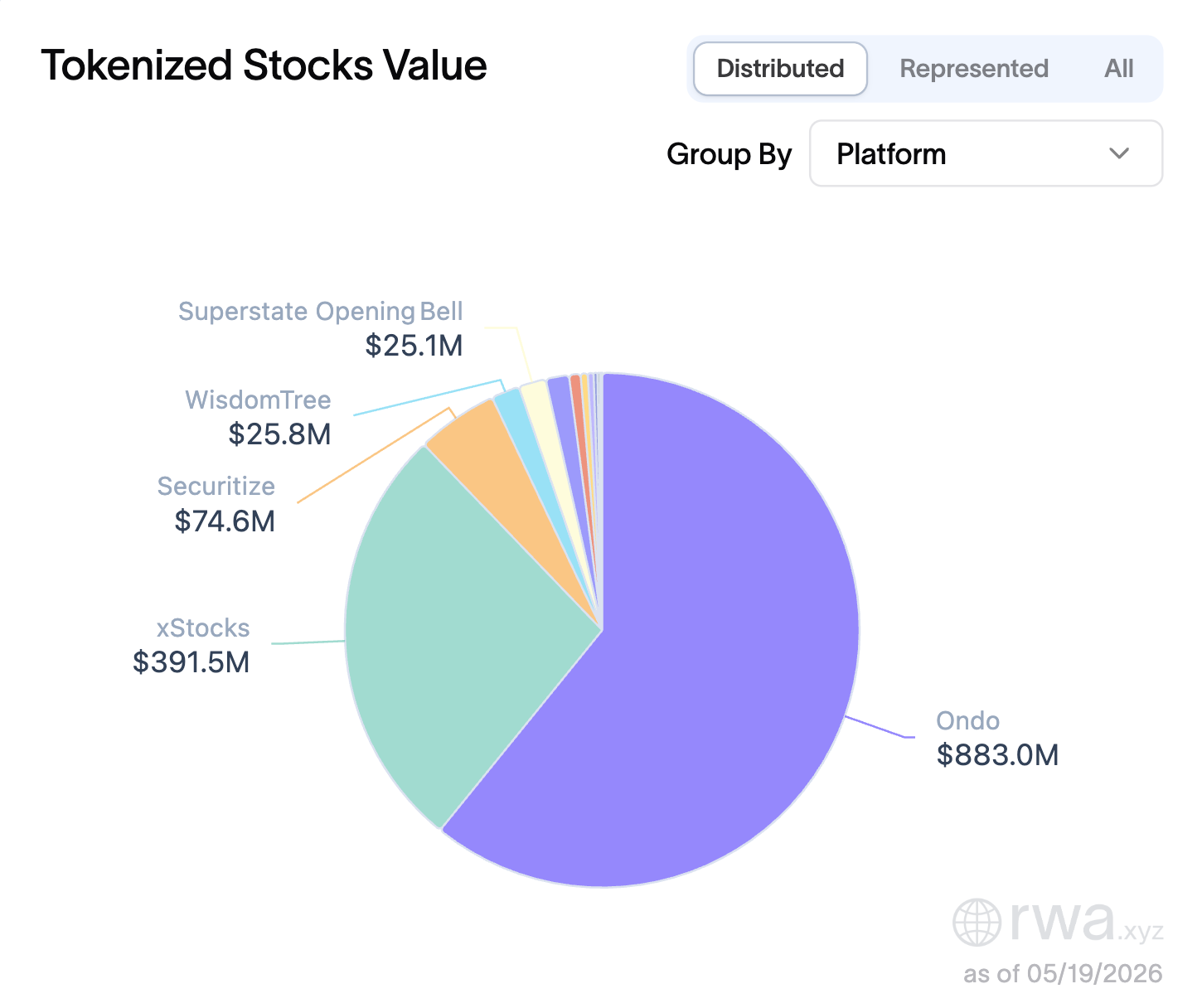

Separating the specific product from the broader company ecosystem, that $1 billion figure belongs strictly to Ondo Global Markets, the equity arm trading Apple and Nvidia. If you look at Ondo Finance as a whole, including its tokenised Treasury products such as OUSG and USDY, the total value locked jumps from $1.3 billion in May 2025 to $3.7 billion today. The institutional cash is piling up in fixed income, but the equity experiment is concentrated in a tiny handful of hands.

Start with what is new and verifiable. Ondo Global Markets launched in September 2025 and became the world’s largest tokenised equity platform within 48 hours. It offers 260+ US stocks and ETFs across Solana, Ethereum, and BNB Chain, each token backed by actual shares held inside a US-registered broker-dealer. Trading runs 24 hours a day, five days a week. Token holders get dividends.

Before May 2026, holding a tokenised stock, you still missed out on proxy voting. This is a mechanism that lets shareholders vote on CEO salaries, board members, and corporate mergers. Without it, crypto equities were just receipts tracking a price, which made the whole idea look less attractive at times.

Then Ondo hooked up with Broadridge, the apex predator of corporate paper-pushing that handles trillions in annual shareholder communications. Now, OGM holders can route actual, official proxy votes directly from a crypto wallet into real-world shareholder meetings. No tokenised stock product before Ondo ever pulled this off, and that’s why it’s such a flex.

On May 6, JPMorgan, Mastercard, Ripple, and Ondo completed the first cross-border redemption of tokenised US Treasuries, settling in under five seconds. Franklin Templeton tokenised five of its ETFs through Ondo. The DTCC, the clearinghouse that settles roughly $2.5 quadrillion in securities annually, brought Ondo into its tokenised securities consortium alongside BlackRock and Goldman Sachs, with production trades scheduled for July 2026. Clearstream and 360X partnered with Ondo in April to provide issuance, custody, trading, and collateralization services.

The cumulative trading volume across OGM is $18 billion, according to Ondo itself. Ondo holds 60-63% market share among tokenised equity issuers. The platform’s TVL doubled between January and May 2026.

Previous tokenised stock products died from regulatory asphyxiation. FTX, Binance, Mirror Protocol.

Ondo internalised this. The company filed a confidential registration statement with the SEC in February 2026, the same process public companies use before an IPO. If approved, Ondo becomes the first issuer of transferable tokenised stocks subject to SEC reporting requirements. A delay in the result of this is bad. A rejection is even worse. Everything downstream, DTCC integration, Broadridge proxy voting, and EU distribution, gets more complicated if the SEC says no to the core product in its home market.

The platform is not available to US investors.

Ondo Global Markets is accessible across 30 European countries in the EU and EEA, in Abu Dhabi through a Binance-operated regulated venue, and in various other non-US jurisdictions. Americans are prohibited. The company whose stock you are tokenising does not allow its own citizens to participate.

But look at who is using the product. BNB Chain, Binance’s chain, is disproportionately adopted in South and East Asia and accounts for 44% of OGM’s total TVL. Of the $287 million attributable to centralised exchange wallets, Binance holds 65%, Bitget 22%, and Gate.io 10%. Bitget’s user base is 67% Asia-Pacific, according to its own disclosure. In December 2025, Bitget handled 89.1% of all tokenised stock trading volume within OGM, approaching $1 billion in cumulative trades. No US exchange, not Coinbase, not Kraken, not Gemini, appears in OGM’s CEX holdings data.

The best available geographic estimate puts 45-55% of value-weighted OGM users in Asia-Pacific, 25-30% in Europe, and 10-15% in the Americas, with the US share functionally zero. A billion-dollar American stock platform, built by an American company, used almost entirely by non-Americans. That is the market Ondo found before finding the US market.

Buying American stocks from the outside is a bureaucratic nightmare for roughly 4.6 billion people. China banned funding foreign accounts, India slaps a 20% tax on larger transfers, and Nigerians face 13% wire fees alongside brutal estate taxes. With strict US rules forcing firms like Fidelity and Vanguard to close international accounts, the walls around Wall Street are only getting higher.

The vast majority of these wallets buy a stock and flip it within 24 hours. Only a tiny fraction of users hold onto their positions for more than three months. That’s why this looks to me more like a fast-paced trading sandbox for non-Americans who have been locked out of the standard financial system.

The project generates millions in fees, but the protocol token holders don’t see any of that cash. The corporate entity keeps the revenue. The token holders just get to vote on a small, unrelated lending protocol while chasing online rumours about getting a cut of the fees later. Like traditional asset managers, the corporate arm keeps the money while the token stays speculative.

Yet, this is exactly what early stablecoins looked like before they got recognised globally and reached a $323 billion market cap. A few years ago, putting a dollar on a blockchain was considered a sketchy, glitchy, total wildcard experiment used by people who couldn’t get a bank account. Today, we have giant credit card companies and massive global banks casually routing billions of dollars through them.

Ondo could try the same long game, slowly sucking up massive volume by turning government debt accessible. Almost winning, but a few more loopholes to be patched.

You do not actually own the stock; you own a structured debt note issued by an offshore shell company that promises to track the price.

If a smart contract is hacked, traditional courts rely on the broker’s database, not the blockchain.

The tokens are stuck in a walled garden. One cannot just swap them freely on Uniswap because every wallet has to be strictly whitelisted and geo-blocked. Until the SEC approves their filing, it is tied to a heavily restricted secondary market.

We are already seeing the cracks of this explosive, bottlenecked demand. Their tokenised Nvidia stock recently slammed right into its regulatory cap of 10,000 individual wallet holders.

Until legal walls come down, it remains a highly sophisticated, multi-million-dollar proof of concept for global investing. Which is a very impressive start.

Until next time,

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.