Reinventing Savings with Ample 💰

Why Ample wants to make people save by making it feel like winning

Hello,

Two decades ago, I used to play an action game where you could accumulate coins and face a choice: spend a few coins on a guaranteed common skin or gamble everything on a randomised chest where you’d probably get nothing but a chance at an exclusive skin. I picked the chest. Almost every time. I don’t remember ever hitting a jackpot. And, no, I wasn’t bad at math. I knew the odds were against me. But there was a human behavioural element at play there. The three seconds before the chest revealed if I’d won, the wheel would spin, and the animation built anticipation. That was it. That’s what people who picked the chest did it for. The adrenaline lasted all of three seconds. Game studios built a $20 billion annual economy on randomised rewards and loot boxes.

You think it is irrational? We see a similar human behaviour, albeit from the other side, in finance.

People happily pay a recurring sum of money to avoid a tiny chance of catastrophic loss and call it insurance. We accept a small, guaranteed cost to immunise ourselves against a low-probability disaster. Finance has built an industry worth over a trillion dollars around this fear.

On the flip side, the lottery market is estimated at over $370 billion.

What’s common in all such systems is that they take something away from the player. We call it the ‘sunk cost’ in economics. The game takes away your coins. The lottery contest takes away your ticket price. The insurance system takes away your premium. The expected value of each of these contracts is always negative.

What if it wasn’t?

What if you could experience the excitement and anticipation of winning big, without ever losing your principal amount? What if what was being redistributed as a “reward” is not the cumulative sunk costs of the participants but just the interest earned on your deposits?

Someone ran this experiment for 70 years, but only in one country. Today, someone else has replicated this, but at scale and accessible worldwide.

The 70-Year Proof

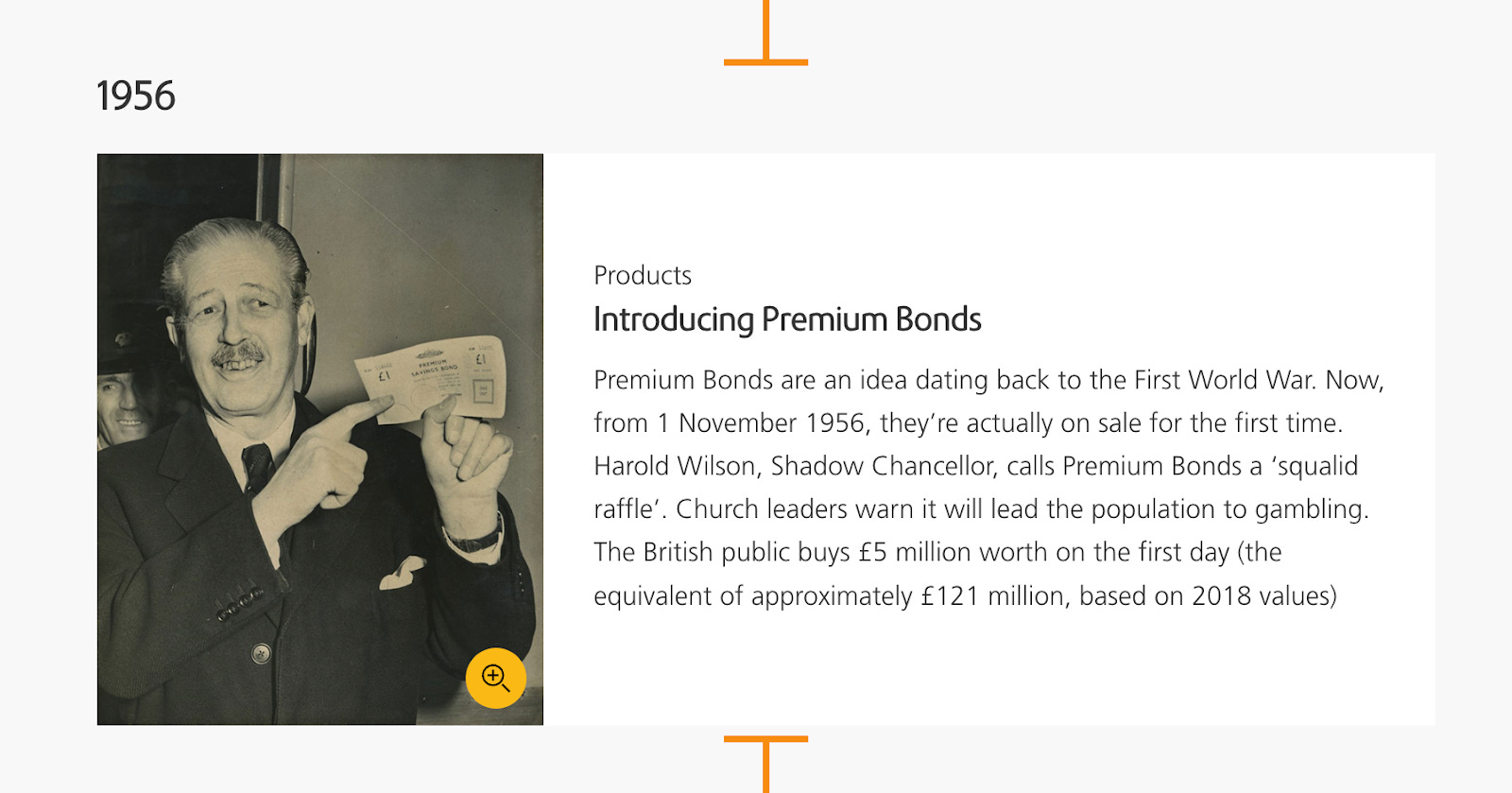

In 1956, Harold Macmillan, then Chancellor of the Exchequer, introduced Premium Bonds to the United Kingdom. Rather than distributing interest among depositors in a linear fashion, the government pooled all deposit yields and redistributed them as randomised prizes.

Your principal stayed intact, fully backed by the Treasury.

Today, about 24 million people have invested over £240 billion in Premium Bonds (PBs). That’s over a third of the UK population. Electronic Random Number Indicator Equipment (ERNIE), the random number generator, selects winners and distributes millions of prizes every month, ranging from £25 to a million-pound jackpot.

From a rational perspective, most holders would earn more in a savings account or an index fund. Yet, PBs survived because they targeted the human behaviour that reveals how people feel about saving with a remote chance of earning a jackpot return, rather than a fixed, modest interest income. These bonds made holding money exciting and anticipatory rather than passive and boring.

This may not materialise into winnings for short-term investors, but people believed they stood a chance of hitting the jackpot if they held their investment for long enough. A classic belief that we all carry when we play any game of dice. You expect to hit a six if you keep rolling the dice long enough.

Though the probability of winning a jackpot doesn’t favour the investor from an economic standpoint, the realisation of not risking capital while standing a chance of winning an outsized prize made psychological sense. That’s what helped Premium Bonds survive every macroeconomic crest and trough the UK experienced over the last 70 years, including interest rate cycles, inflation spikes, financial crises, the rise of the internet, and generational turnover. Nothing came close to threatening the product.

The model was effective, yet it was confined to the UK. Many others tried to emulate the strategy. The U.S. experimented with it through credit unions in the early 2010s, but couldn’t scale it to the same level as PBs.

Here, the reasons were structural and had nothing to do with psychology. The strategy needed a government issuer, a legal framework that exempts the product from gambling regulations, and the ability to operate without intermediaries extracting value along the journey.

Some found a way around this.

Yotta, a U.S. fintech company founded in 2019, came close to replicating the model. It offered a savings account where interest was distributed as lottery-style prizes. People lapped up the product. There was no doubt about the product-market fit. Demand rose.

But Yotta faced another, bigger problem. It was built on traditional financial infrastructure by relying on partner banks, middleware providers such as Synapse, and reconciliation layers. Traditional banking infrastructure is built for linear, predictable and recurring interest payments. PBs needed a specialised financial infrastructure that left no room for fragmented custody and intermediary fees. So, when Synapse collapsed in 2024, over 100,000 Americans lost access to over $265 million in funds.

Yotta managed to prove the thesis right, but the infrastructure pulled it down.

Enter Blockchain

Layer3, an on-chain finance platform, is the latest one to double down on this thesis. Its team built Ample, a platform that takes the Premium Bonds model and backs it with on-chain infrastructure.

The same model that accepts deposits, pools yield, distributes it as randomised prizes and preserves principal; but on blockchain this time.

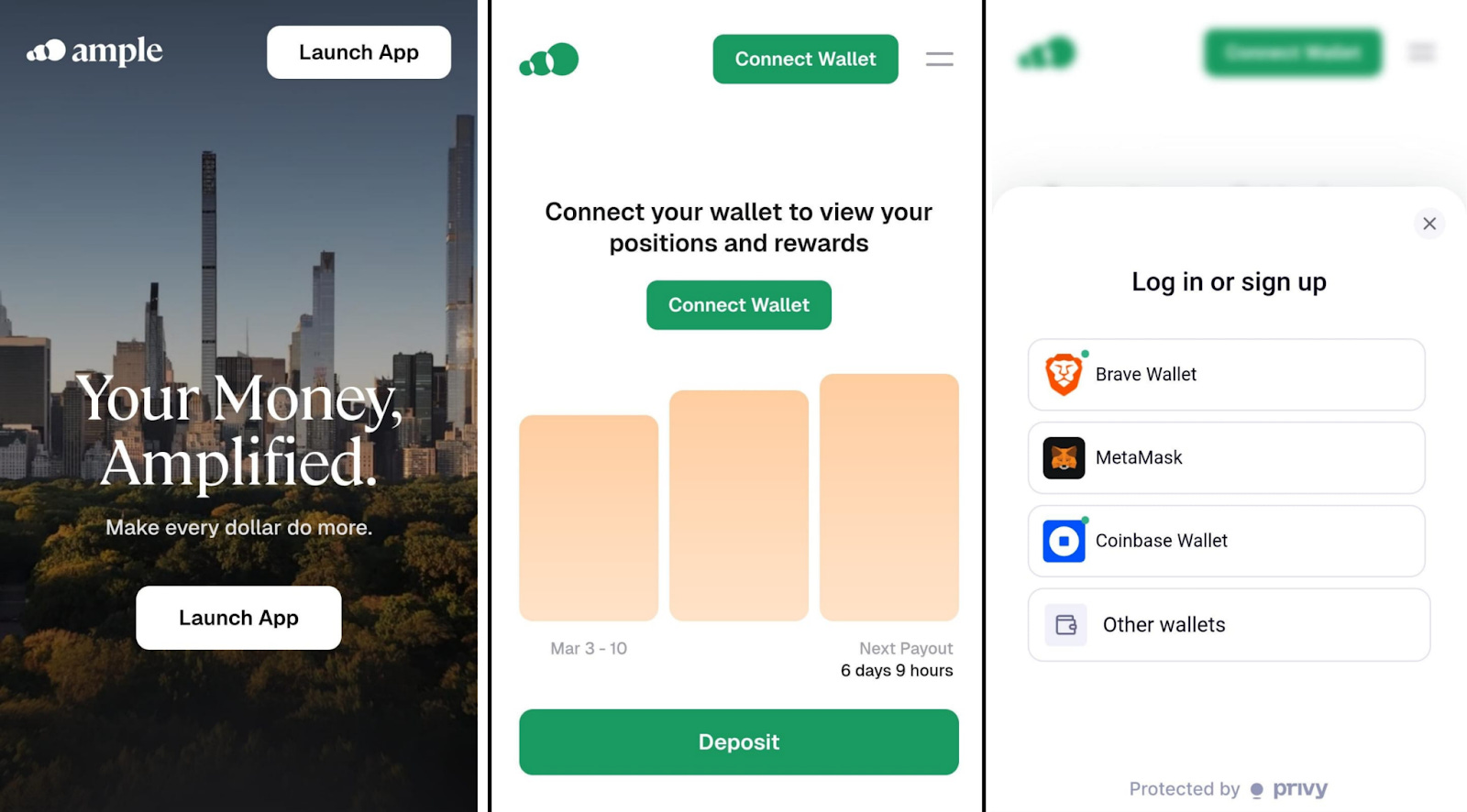

You can connect your wallet, deposit USDC into the protocol and get started.

Ample then supplies the assets to on-chain lending markets to earn yield. Instead of distributing yield proportionally, the app aggregates it into a prize pool and distributes it randomly at weekly intervals to selected participants. These winners are selected using verifiable randomness encoded in smart contracts.

Your principal stays in the smart contract, under your ownership and doesn’t transfer to any intermediary institution. What’s better? The prize logic, unlike in traditional setups, is transparent and auditable. Fees are explicit and programmatic.

There are no partner banks holding deposits and no Synapse-style reconciliation layer.

This is the single biggest reason why it looks more promising than the previous models. Ample removes the entire opacity and middleware stack that killed Yotta. All components of the model, including the deposit, yield, prize logic, and payout, live in the same observable on-chain system.

The Engagement Loop

Although the winners are ultimately selected at random, factors such as how long they have been depositing, whether they have a continuous deposit streak, and whether they are saving with multiple people influence their ticket multiplier by a small percentage.

Ample layers the core mechanism with engagement elements that feed into each other. The ‘Tickets’ feature awards the user tickets proportionate to their deposit size. The more tickets you hold, the likelier you are to win a payout. ‘Streaks’ rewards users for depositing consistently every week with ticket multipliers.

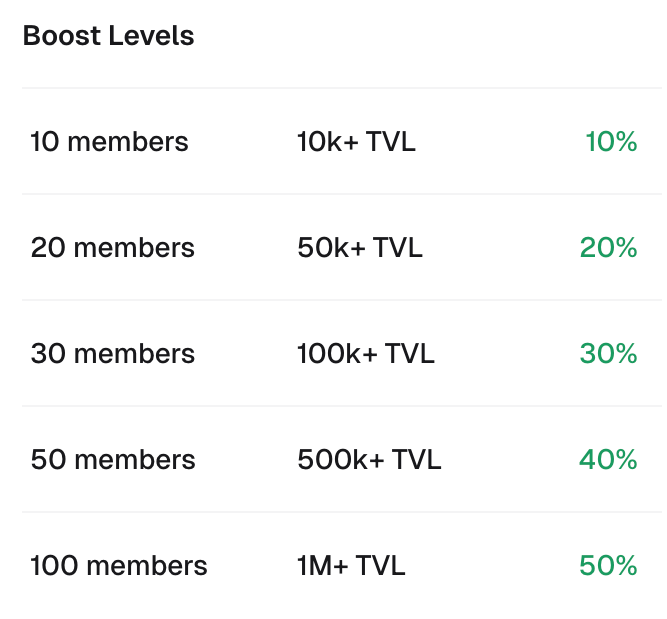

It even rewards users with more boosts to their chances of winning a payout when they form a team and bring their connections on board.

The more members you bring to the platform and the higher the value of collective deposits the team makes, the bigger the boost you earn.

The B2B Growth Card

Ample’s scope for growth is tied to the size of the prize pools. Larger pools will sustain user excitement, something that is fundamental to the entire model. Currently, Ample has only scratched the surface. Its potential will come alive when the prizes are big enough to make someone’s week.

What excites me about Ample is that it doesn’t limit itself to being a consumer-facing app. It wants to position the product as a savings infrastructure on top of existing platforms. Any wallet or fintech app where users hold idle asset balances should be able to plug into Ample and offer prize-linked savings under the hood without building any of the yield aggregation, randomness, or payout logic themselves, Zeel Patel, Ample Product Lead, tells me.

Zeel expects Ample to replicate, for prize-linked savings, what Privy did by integrating with Aave on Arbitrum, giving every wallet built on top of it access to that yield source. Early explorations and discussions are underway with wallets and exchanges.

Even if one major wallet embeds Ample, the depositor base could expand by orders of magnitude, blowing up the prize pool and turning the draw exciting for the users. That’s what will set the flywheel started.

Although the thesis is proven, there are a few things that could go wrong.

Every consumer application faces initial problems with distribution, discovery, and retention; Ample is no different. The product needs wallets and fintechs to embed it for the behavioural thesis to work at scale. Ample’s advantage here is that the team isn’t starting cold. Its team has experience building Layer3, the platform that has already scaled to millions of users in the consumer space, and those distribution muscles carry over.

Another nuance here is that this is a new concept for most users. But the fact that the product is psychology-driven and not rate-driven will give Ample an edge over other products that are overly dependent on rate cycles. The behavioural shift has already started playing out.

One beta user deposited $10, won over $300, and came back with $2,000. The team has seen this trend pick up. But it means every new user has to be converted through experience, which could be a harder acquisition path, but not impossible. This is where the social engagement layer could exhibit network effects and drive user adoption.

What Comes Next

The stablecoin supply has touched $300 billion. With a growing population wanting to hold digital dollars at scale, they will need somewhere productive to put all that new money. Some place that doesn’t eat into the purchasing power of these dollars. With Aave, Euler and Morpho holding billions in deposits and years of operational history, the narrative has aligned in favour of stablecoin usage and fintech products built on blockchain infrastructure.

This could give Ample a conducive space for mass adoption if it can materialise its integrations across major platforms that hold stablecoin balances.

But there’s something more interesting that makes me feel optimistic about what lies ahead for Ample.

The Ample team sees a future in which tokenisation across treasuries, gold, and equities expands the class of assets that prize-linked savings can tap into. If prize-linked savings works for USDC, there is no reason it can’t work for tokenised gold, treasuries or any other yield-bearing asset in tokenised form.

In the long-term, Ample expects to route credit and spending through the same engagement structure. If it can pull that off, it will have delivered a globally scaled-up and universally auditable version of Premium Bonds, where the anticipation of a reward can exist inside a product, the principal is preserved, and the expected value never turns negative.

That’s it for today. I will be back soon with another one.

Hoping to get lucky with the next payout at Ample,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.