Hello Dispatchers, happy Saturday!

Remember when sending money to a friend meant writing a cheque and waiting days for it to clear? Then came Venmo, Cash App, and Google Pay, making transfers as simple as a few taps on your phone. "Request $20 for pizza" and within seconds, the money arrives.

In the decentralised finance (DeFi) universe, cryptocurrencies offer to make payments, including those crossing borders, easier and cheaper.

Let’s face the reality though: imagine trying to send cryptocurrency to a friend. You'd need their wallet address — a 42-character string like 0x9A81cD12d6Ff38a123... One mistake, and your money could vanish forever. No wonder crypto remains intimidating for most people despite its decade-plus existence.

These are conducive conditions for disruptions to happen, though.

Payment giants that businesses and individuals world over have trusted for decades — Visa, Mastercard and the like — are embracing cryptocurrency. Not Bitcoin or Ethereum, but stablecoins – digital dollars that combine the stability of traditional currency with the speed and programmability of crypto.

Why does this stablecoin bet matter?

These are not gambles on volatile crypto price movements. It's a bet on something far more fundamental: how money moves and how we store value. And that might just change everything.

Secure your Bitcoin with Hardware Wallets

Trezor has transformed crypto security from a complex puzzle to a user-friendly playground, so you can be the boss of your financial future.

Securely store, manage, and protect your coins with Trezor hardware wallets, app & backup solutions.

The Silent Revolution in Money

Stablecoins in circulation have gone 3x to $240 billion in market cap in just the last four years. Standard Chartered expects this figure to grow 10x to $2 trillion in next three years.

These digital dollars maintain a steady 1:1 value with the US dollar, or any other currency they are pegged to, making them fundamentally different from volatile cryptocurrencies.

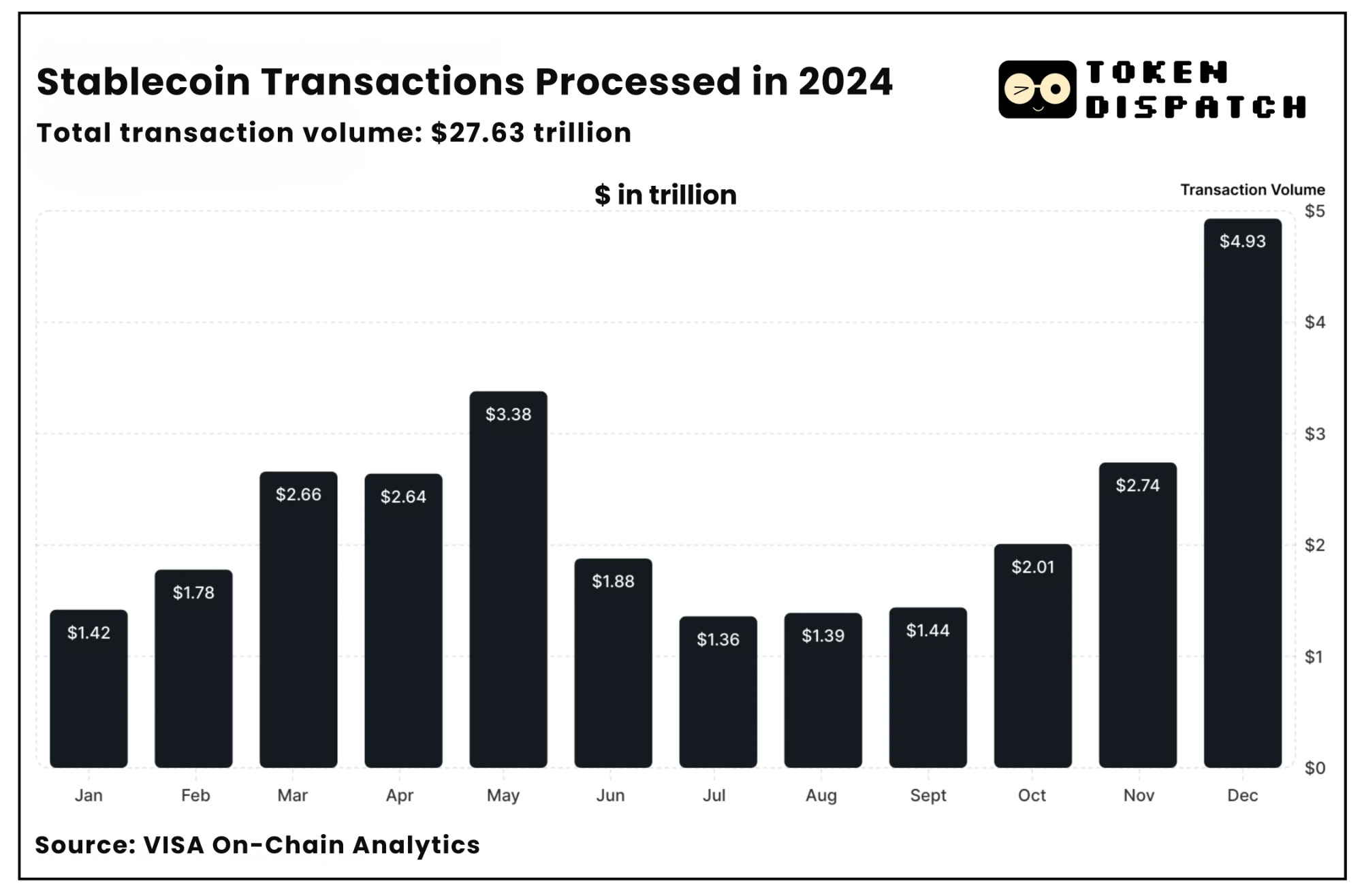

In 2024, stablecoins facilitated over $27.63 trillion in transfers, exceeding the combined volume of Visa ($15.92 trillion) and Mastercard ($9.76 trillion).

Although 70% of stablecoins figure was accounted by bot activity, that doesn’t necessarily invalidate them. Bots are often used to achieve efficiency through quicker transactions and lower costs.

These transactions weren’t driven by speculation, but by everyday utility: remittances, payments, and protection against inflation.

The mechanics are straightforward: you give the issuer a dollar, they give you a digital token. When you're ready, you trade it back for a dollar. The tokens live on blockchains, allowing them to move globally without traditional banking friction or costs.

Two Problems, One Solution

Stablecoins are solving two fundamental problems that have always challenged global finance.

First, payments. Moving money across borders remains shockingly inefficient even after all the progress made in the digital world. Traditional remittance services still charge an average of 6.62% in fees and can take days to settle. Even digital solutions like PayPal often impose currency conversion charges up to 4%.

Stablecoins, by contrast, move globally in minutes for pennies, regardless of amount or destination. This explains why stablecoin adoption is surging in developing economies including Argentina and Nigeria, where these problems are most acute.

The second problem is store of value. For millions living in countries with unstable currencies, stablecoins offer a way to hold dollars without a US bank account. All you need is a smartphone. This makes stablecoins different from previous crypto innovations, which required users to accept price volatility as the cost of financial freedom.

It’s the simplicity of stablecoins that uniquely position them to reach mass adoption. They don't ask users to understand blockchain technology or accept new monetary theories. They simply offer a better way to access something everyone already understands: the US dollar.

Get 17% discount on our annual plans and access our weekly premium features (Mempool, Game On, News Rollups, HashedIn, Wormhole and Rabbit hole) and subscribers only posts. Also, show us some love on Twitter and Telegram.

Giants Join the Party

Traditional players including Mastercard and Visa are now integrating stablecoins into their global networks to do one thing - make money move.

Mastercard announced last week that users of popular crypto platforms like MetaMask, OKX, Binance, and Crypto.com can now spend stablecoins at any of the 150 million merchants that accept Mastercard globally.

Not to be outdone, Visa partnered with Bridge to enable stablecoin payments across Latin America, with plans to expand to Europe, Asia, and Africa.

Remember we spoke about how nervous sending money to a 42-character string cryptic address is like? Well, Mastercard made that as simple as transferring money using Venmo or Cash App. With Crypto Credential, the payment giant allows simpler addresses like @elsa.eth.

PayPal took a different approach by launching its own stablecoin, PYUSD, integrating it directly into its existing payment apps.

Days of seeing crypto or decentralised finance as a threat? Long gone.

Got questions about a hot crypto topic that you want help understanding? Ask your question using the form and our crypto experts may answer it along with your name in the next Thursday’s News Rollups.

Mastercard's Chief Product Officer Jorn Lambert said:

"When it comes to blockchain and digital assets, the benefits for mainstream use cases are clear. We believe in the potential of stablecoins to streamline payments and commerce across the value chain."

The Path to Mass Adoption

Stablecoins already process more transaction volume than traditional payment networks, but it still lags in terms of transaction count.

The traditional giants have understood that the next billion users won't come from crypto enthusiasts but from everyday people solving practical problems.

Hence, they have targeted key regions that could drive this adoption.

Latin America, where inflation volatility makes stablecoins attractive as savings vehicles. Argentina, Venezuela, and Colombia have seen explosive growth in stablecoin usage as citizens seek protection from local currency devaluation.

Southeast Asia, where remittance corridors between countries like the Philippines, Indonesia, and Singapore benefit from stablecoins' low fees and instant settlement. Workers sending money home can now save hundreds of dollars annually in remittance fees.

Africa, particularly Nigeria and South Africa, where stablecoins bypass currency controls and provide access to global commerce despite limited banking infrastructure.

With Visa and Mastercard connecting these wallets to their merchant networks, users don't need to understand the underlying technology to benefit from it.

The icing on the cake? Even the governments of the top economies are lending their support.

The US Securities and Exchange Commission (SEC) last month issued a guidance advising that certain types of dollar-pegged tokens will not be considered as securities.

As we write this, the US politicians are debating two separate bills around stablecoin regulation.

Read: How STABLE is the GENIUS Act? ⚖️

Token Dispatch View 🔍

The stablecoin revolution represents something rare in technology: a genuine solution to longstanding problems. Unlike speculative crypto assets that create new behaviours, stablecoins improve upon something billions already do — send, save, and spend money.

Crypto purists might see Mastercard and Visa's involvement as contradicting the decentralised ethos of blockchain. After all, stablecoins were meant to eliminate intermediaries, not create new ones.

Yet this integration highlights a crucial reality: adoption requires both innovation and familiarity. By combining the stability of traditional finance with the efficiency of blockchain technology, these partnerships could drive mainstream adoption faster than pure decentralised solutions.

Challenges remain significant.

Regulatory frameworks are still evolving, with Congress considering legislation that would require stablecoin issuers to be fully licensed and maintain 100% cash-equivalent reserves. Questions about centralisation persist: if Mastercard becomes the gatekeeper deciding which wallets and coins are supported, we risk recreating the very power dynamics crypto sought to disrupt.

Nevertheless, the direction is clear. Stablecoins are becoming infrastructure rather than just a product. Their utility in solving real problems – cross-border payments, inflation protection, financial inclusion – is driving adoption regardless of whether they perfectly fulfil crypto's original libertarian vision.

As stablecoins mature, they're spawning an entirely new financial ecosystem. We're witnessing a shift from simple transfers to sophisticated services built on stablecoin rails.

Early stablecoin use cases focused exclusively on trading and transfers. Today, we're seeing lending protocols, yield-generating strategies, and payment infrastructure being built around these digital dollars. Companies are beginning to explore programmable money features that traditional currencies simply can't match – like automatic revenue sharing, conditional payments, and escrow without intermediaries.

Traditional finance is responding with its own innovations. Banks that initially resisted stablecoins are now exploring how to incorporate them into their service offerings.

What's particularly powerful about this ecosystem is its composability. The ability for different services to seamlessly interconnect. Just as the internet enabled countless applications to be built on standardised protocols, stablecoins are creating an open financial layer that developers can build upon.

This innovation cycle is accelerating as regulatory clarity improves. The progress policymakers make in the US and elsewhere will dictate how well stablecoins will act as the rails for the future of finance.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. You can find all about us here 🙌

If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us.

Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains sponsored content and affiliate links. All sponsored content is clearly marked. Opinions expressed by sponsors or in sponsored content are their own and do not necessarily reflect the views of this newsletter or its authors. We may receive compensation from featured products/services. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.