Hello

It always starts the same way. At least for those who have been in the crypto space long enough. A new network emerges, claiming it will finally make Bitcoin useful and move it beyond being a passive asset. They promise to make the asset part of the financial infrastructure, facilitating liquidity, boosting yield, and securing the future of finance.

Then the hype drains away, the bridges crack, and the coins return to where they were.

Yet, here we are again, with another project claiming it will finally make it work. There are some differences, just as there have been in every prior attempt, but will this one succeed?

In today’s piece, I will examine the moving pieces of the latest attempt to bring Bitcoin’s liquidity into DeFi.

AI Agents that Trade, Predict, and Evolve!

DeAgentAI has built the largest AI Agent infra across Sui, BSC & BTC, solving what every AI dev struggles with, identity, continuity, and consensus, the holy trinity for making AI actually autonomous.

Their flagship products?

AlphaX → A crypto prediction engine that hits 9/10 signals.

CorrAI → A no-code quant playground for designing and deploying DeFi trading strategies.

Truesights (launching soon) → InfoFi network that rewards real alpha, not just noise.

Backed by top-tier VCs, and a team from Carnegie Mellon, UC Berkeley, and HKUST, they’re scaling what’s basically the “ByteDance of Web3.”

Except instead of serving you TikToks, their algorithms are training autonomous AI Agents.

When Starknet, the Ethereum Layer 2 that uses zero-knowledge proofs, announced at the end of September that users could stake bitcoin directly on its rollup and earn STRK rewards, it felt like déjà vu. But this time, there’s a twist. Here’s a crypto project claiming to make BTC useful, yet it’s based on an Ethereum L2.

Starknet branded its programme as “BTCFi Season”, promising trustless yield. It also claimed to be the first fully trustless BTC staking on any L2. The programme is “designed to support ecosystem protocols that would enable highly liquid BTC pools on DEXs (decentralised exchanges) and Money Markets and borrowing of stablecoins against BTC”, as noted on its webpage.

The data looked impressive.

By October 9, 2025, total value locked (TVL) had surged to $222 million, a 65% increase from $135 million two weeks earlier. On October 6, app fees reached $63,594, the highest in over a year and a half, while revenue, which is the portion of fees the protocol keeps for itself after paying out costs to liquidity providers, hit $39,962 for the day, data from DeFiLlama showed.

As wrapped-BTC liquidity started entering staking pools, both usage and fee capture began to swell together. Even the price of Starknet’s native token, STRK, rose over 50% to peak at $0.1968 on October 6 from under $0.13 on September 30.

These numbers were early signs that Starknet’s strategy of moving Bitcoin into DeFi to generate rewards is starting to reap rewards. But, the early numbers for every bridge that came before also showed a similar response.

In October 2018, Wrapped BTC (WBTC) brought the first version of this dream to life. By issuing an ERC-20 token backed 1:1 with real BTC, it gave traders a way to bring BTC into Ethereum’s DeFi ecosystem. However, it couldn’t eliminate trust. BitGo, the custodian, held the keys. It took over a year and a half, until the DeFi summer in 2020, for WBTC to take off. Yet for most Bitcoiners, it appeared like a glorified IOU.

Even before WBTC’s arrival, there were other attempts at bridging Bitcoin.

Almost a decade ago, the smart contract platform Rootstock (RSK) invited Bitcoin miners to merge-mine a smart contract sidechain. Then there was Liquid, which built a federation of notaries for faster settlement of exchanges. Both promised speed and scalability without compromising security but ultimately fizzled out. Without clear use cases, what would users do with the coins?

Early decentralised bridge attempts, like renBTC and tBTC version 1, looked elegant but crumbled under their own mechanics. Only after a complete redesign of the tBTC did version 2 finally stabilise.

There were also projects like Badger and Thorchain, which aimed to bring BTC liquidity into DeFi. Each attracted some capital for a quarter or two, but none could achieve large-scale adoption.

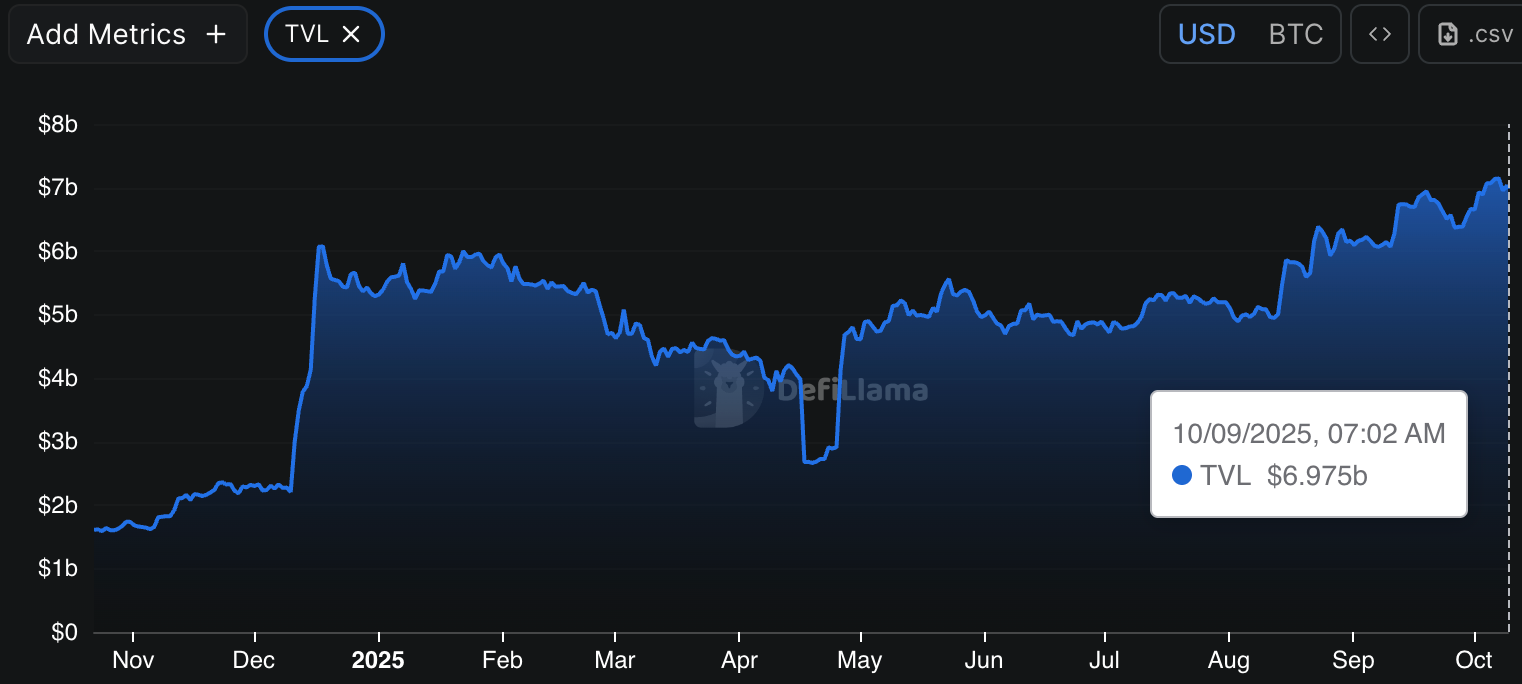

It was not until 2024, when Babylon was launched, that things began to change. The lesson learnt over the years was clear: you can’t drag Bitcoiners off their chain. Babylon learnt from the lesson and kept BTC home. Instead of requiring users to wrap or bridge their Bitcoin, Babylon allowed BTC holders to stake their coins and help secure other Proof-of-Stake (PoS) networks, earning rewards without ever having to leave the Bitcoin network.

In return, those who staked their Bitcoin received rewards in multiple tokens: BABY, OSMO and SUI. The idea worked, and within months, Babylon proved that there was an appetite for yield as long as the keys stayed in the hands of the Bitcoin holders.

In just one year since its launch, the TVL grew from over four times to roughly $7 billion, up from $1.6 billion.

Parallel rails also formed.

Threshold’s tBTC offered a trust-minimised bridge so Bitcoin could circulate in DeFi, now including Starknet, without a central custodian. Mezo took a different tack: let users keep BTC and unlock fixed-rate loans and a BTC-centric stable balance (MUSD), while Garden Finance focused on fast, intent-based BTC swaps between Bitcoin and EVM/Solana. Together, they showed demand for yield and liquidity that respects self-custody.”

Starknet, on the other hand, takes a different approach. It plans to bring bitcoin out into the world, similar to past efforts, but this time with proper cryptography and an economic model it claims is strong enough to survive beyond initial incentives.

Starknet’s method involves users wrapping their BTC into tokens like WBTC, LBTC, and tBTC, then bridging them into Starknet’s rollup and delegating the wrapped BTC to a vibrator. Starknet allocates up to 25% of its total staking power to Bitcoin, while STRK holders retain the remaining 75%, ensuring that governance remains local.

In return for staking, BTC holders earn STRK emissions, boosted by a 100 million STRK incentive pool announced by the Starknet Foundation. These rewards can reach up to 4% for basic staking and even higher for liquidity-pool strategies. As a liquid token representing staked BTC, users can lend or trade it while still earning yield.

The aim is to create a self-sustaining loop: as more BTC gets staked, the system grows stronger and generates more activity. Thanks to zero-knowledge tech like Circle-STARKs, Starknet’s rollup can verify BTC data in milliseconds, eliminating the need for oracles or multisig bridges. The economics echo Ethereum’s early staking phase, where token rewards helped build trust and momentum until network usage could support itself.

Yet, the ghosts of older models still haunt Starknet’s approach. Custody risk has not disappeared, but rather fragmented. Instead of a single BitGo, there are now several wrappers, each with its own model of trust. Liquidity can still be elusive, especially if high, early yields fade before DeFi demand matures. And then there is the human element. Bitcoin holders’ instinct to keep their holdings secure and static remains a challenge . for onboarding BTC to Starknet and using it in DeFi.

Starknet’s bet is that higher yields and a simpler user experience (UX) can change their behaviour.

The model contrasts heavily with Babylon’s model. Starknet asks holders to bridge/wrap a slice of BTC onto an L2 so it can be used in DeFi and staked for STRK-denominated rewards. Babylon, instead, lets holders keep native BTC in self-custody on Bitcoin and delegate its economic security to consumer chains, earning those chains’ rewards without moving the coins.

Babylon’s $7 billion of staked BTC shows how deeply self-custody resonates with bitcoin holders. It’s too early to comment on Starknet’s modest $4.7 million worth of BTC staked. Both paths may be valid, as one involves patient capital, while the other appears opportunistic.

What gives Starknet a real shot is its timing.

DeFi in 2025 is no longer a playground; it has matured into a full-fledged industry, with $170 billion in TVL. Auditors, insurance, and institutional funds like Re7 Capital are setting up BTC-denominated yield vaults. ZK rollups are no longer in beta testing phases. The tools required for liquid staking and cross-chain accounting are now well-developed - key ingredients that previous Bitcoin bridges lacked.

The irony is that Starknet and Babylon’s approaches could end up validating each other. If Babylon proves that BTC staking can be self-custodial and economically sound, it legitimises the concept of “productive BTC.” If Starknet manages to keep wrapped Bitcoin safe and liquid, it shows that DeFi can increase bitcoin’s productivity without imploding. The success of both could reinforce the idea that bitcoin can secure and provide liquidity to networks beyond its own.

A year from now, we will either be writing another obituary or a Babylon-like success story. I have seen history throw worse odds than this.

That’s it for this week’s deep dive.

Until then … stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.