Hello,

On May 21, I said in Strategy’s Alchemy of Capital that the corporate BTC treasury giant’s STRC preferred debt instrument bends before it breaks. I wrote that STRC was engineered to trade at $100 and that it could strain in unfavourable conditions, but is likely to hold.

Five weeks later, STRC trades at $74 today, down 26% from par. I’d admit that’s more than just bending, especially when I look at the other metrics around the debt instrument.

Just 10 days after I wrote that piece, Michael Saylor sold 32 bitcoin, worth ~$2.5 million at the time. That was the first time Strategy sold anything from its bitcoin stack in years. Although that barely dented its $65 billion stack, a lot has changed in the market in which Strategy operates. And that also changes a lot of things for Strategy.

In my last piece, I stress-tested scenarios that could undermine the thesis behind the debt instrument and the self-feeding reflexive loop that ensures STRC trades at par. But some of those scenarios unwound sooner and more aggressively than I’d expected.

In today’s piece, I look at what exactly happened and where STRC could go from here.

On to the story…

Even after adding 3,600 BTC in the last four weeks, Strategy’s bitcoin stack is worth 25% less. During this time, both the crypto market and bitcoin, which implicitly powered the market’s belief in STRC, have seen about 20% of their market cap erode.

STRC, whose price had never dropped below $90 since its launch, has slipped every single day from $99 on June 1 to $74 on June 26.

Its implied volatility, a forward-looking metric reflecting market sentiment and expectations, had crossed the 10% mark only on seven occasions in the three months before it sold its first BTC. That has shot up almost tenfold, from 8.22% to 78%, in 19 trading days.

Stripping out the numbers shows how the market’s perception of STRC has changed drastically over the last month. STRC was supposed to behave like a calm, boring instrument, in contrast to bitcoin. Strategy pitched it as a credit instrument that traded near $100 and paid a dividend. For months, it traded just like that. In the last 30 days, though, STRC has been closing lower every single day. The instrument that traded at about $100 consistently for months now trades at $74. Its 30-day historical volatility has risen from 4.3% to 34.6% over the last month.

Although Strategy has yet to miss a dividend payment on the outstanding STRC instruments, what’s changed drastically is that its price now fluctuates more wildly than the risky asset it was supposed to shield people from. While the prospective investors were promised predictability, that’s the one thing the instrument can no longer offer.

Implications for Strategy

The most immediate consequence is that Strategy’s funding machine is stressed.

When STRC traded at or near $100, Strategy could issue new shares through its at-the-market programme, collect the proceeds, and buy more bitcoin. That loop powered everything. But issuing a share with a $100 par value when the market will only pay $74 for it means Strategy must still pay an 11.5% dividend on $100 while receiving just $74 in cash. No company does that voluntarily. So the ATM issuance has paused, and the bitcoin-buying flywheel that ran on preferred capital has gone quiet.

The notional value of outstanding STRC preferred shares more than doubled, from $5 billion to $10.5 billion, between March 18 and May 18 this year. But Strategy hasn’t issued a single share ever since.

In my last piece, I described the loop running forward: issue STRC, buy bitcoin, bitcoin rises, confidence grows, issue more STRC. I treated the reverse as a tail scenario, where if the belief in the loop failed, the loop could unwind. That was less than six weeks ago.

But since STRC holders have a preferred right to receive their dividends, the company will still have to pay them out of its cash reserves or, worse, by liquidating its BTC stack.

In May, Strategy’s cash reserve had fallen to $871 million, down 60% from where it stood ($2.25 billion) when I wrote the last piece. That was after the company repurchased $1.5 billion in aggregate principal amount of convertible notes expiring in 2029, for approximately $1.38 billion in cash. It has since been rebuilt to around $1.4 billion, including expected cash proceeds from shares sold under Strategy’s ATM that had not yet settled as of that date.

Set that against annualised preferred dividend obligations that have climbed past $1.2 billion across STRC instruments. That figure swells even further when you add payment obligations toward other instruments.

Although Strategy is far from insolvency, thanks to its BTC stack that it can partly liquidate, the bigger trouble is not the math but the slipping investor confidence in its instruments.

Reviving Investor Confidence

There is a growing debate on crypto forums arguing that Strategy should sell a meaningful chunk of its bitcoin stack to rebuild confidence. But it’s a double-edged sword.

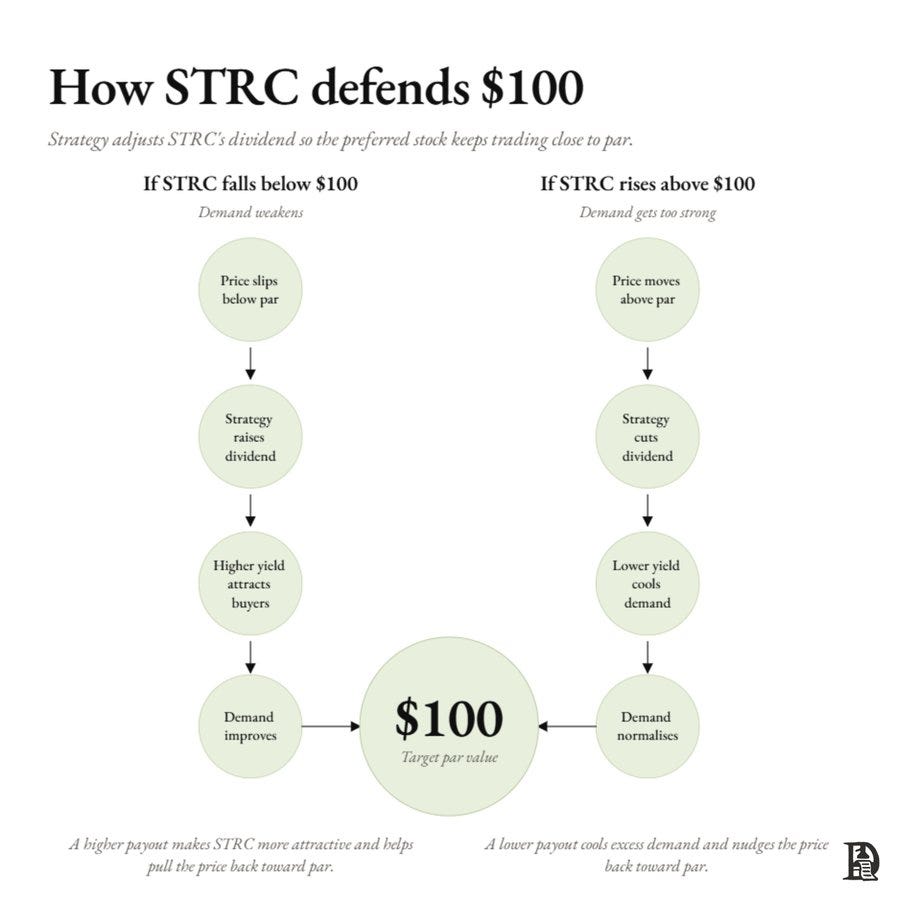

STRC was designed to trade at its par value of $100, and the entire loop of raising additional funds to pay off dividend obligations revolved around its ability to keep the trading price close to par.

If Strategy has to revive investor confidence in STRC and bring its par value back to $100 from $74, it must raise its dividend rate to make it more attractive. But raising the interest rate would mean a larger dividend payout. At the current level of outstanding STRC instruments, a 50-basis-point dividend hike would add about $50 million in annual obligations.

The interest rate hike might still attract enough buyers for STRC. In that case, it will be forced to repeat what it did on June 1: sell more of its BTC stack to pay its dividends.

The payment obligation is a math problem. But selling a portion of its BTC stack could pose a psychological and larger dilemma for Strategy.

In 2025, dozens of companies copied Strategy’s digital asset treasury playbook. They issued stock, bought bitcoin, traded at a premium to their net asset value, and used that premium to raise more capital. Nearly all of them stopped buying when bitcoin slumped, and premiums vanished.

Strategy survived that episode specifically because it did not sell. The “never sell” commitment was what held up the investors’ belief in the entire capital structure.

But that commitment has now taken a U-turn. Although Strategy remains a net buyer of BTC, Michael Saylor explicitly admitted during Strategy’s Q1 earnings call that the company will consider selling its BTC stack to fund its dividend payments.

That statement didn’t trigger investor concerns for over a month. But the single act of selling just 32 BTC, which is less than 0.004% of its BTC stack, on June 1, has done considerable damage to the investor confidence.

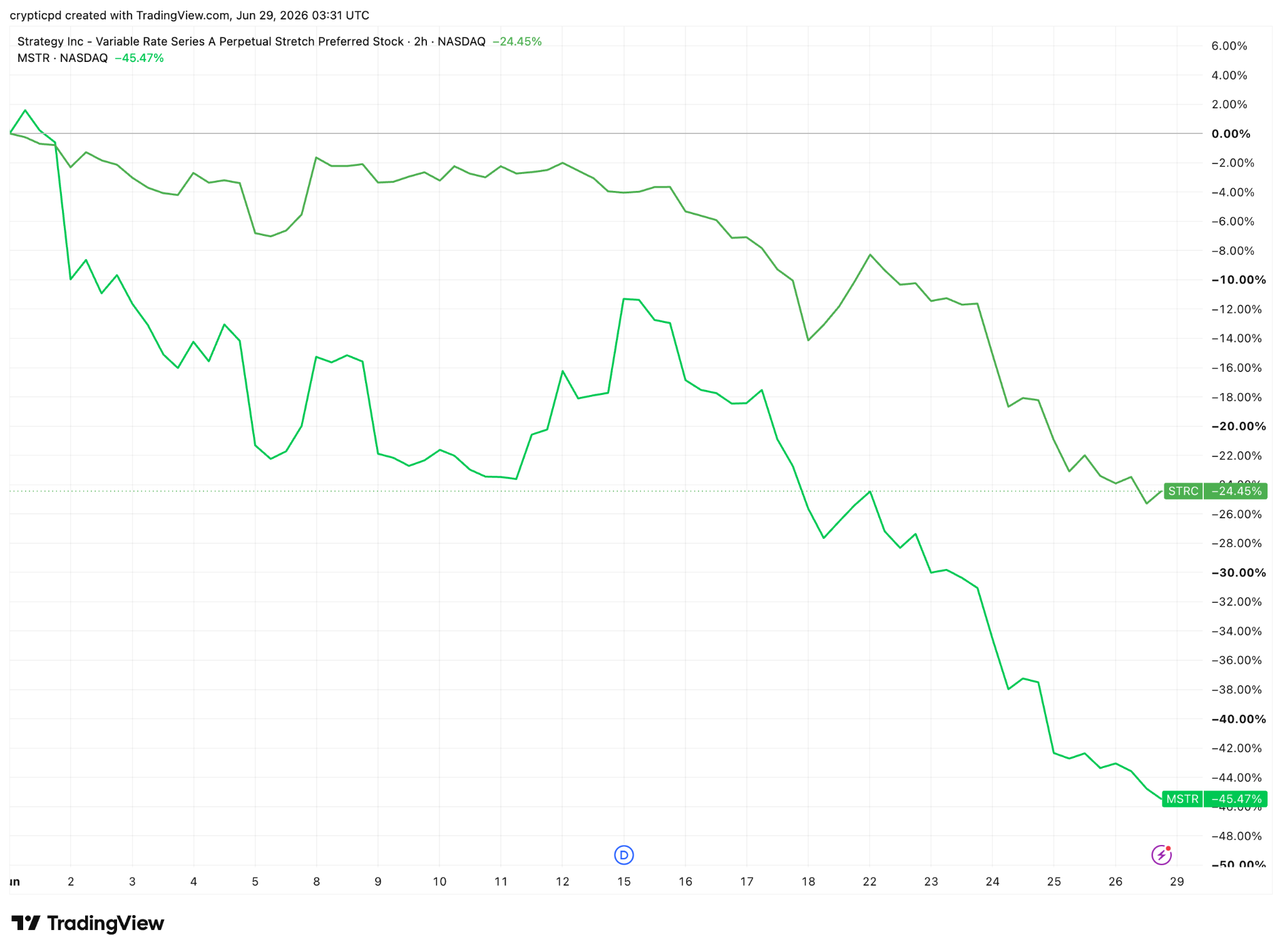

The STRC price has dropped by 25%, while the price of common equity stock MSTR has slumped by 45% since the day Strategy sold 32 BTC. In fact, MSTR’s price has slipped below $100 for the first time in more than two years.

This is where the psychological dilemma arises for prospective investors.

Strategy can solve the near-term payment problem by selling bitcoin. In accounting terms, that is possible. The company has a large BTC stack, and selling a small portion of it to fund preferred dividends doesn’t threaten solvency. But no public company is valued only on accounting logic. The story that the company tells the world plays an important role in deciding how the public values it. Strategy sold the story of being a company that buys through cycles, refuses to sell into weakness and uses capital markets to accumulate more BTC.

Once that selling line is crossed at scale, every future dip in Strategy’s cash reserves and every fall in STRC’s price will invite the same question: “Will they sell again?”

This question is the dilemma. If Strategy does not sell, investors may worry about how it will fund its dividend payments. If it does sell, investors will worry that the story of the BTC stack being untouchable is no longer true. The first stresses the cash-flow fundamentals, while the other tests the company’s story that the investors bought into.

This is the reflexive loop that I spoke about in my last piece. The same belief that helps a model like STRC sustain could lead to its downfall, even when the fundamentals seem healthy. Even now, Strategy’s reserves and BTC stack will keep it safe from bankruptcy, but eroding investor confidence alone can lead to reduced interest in buying more STRC and a free-falling STRC price.

We saw this exact pattern kill the DAT copycats. The moment a treasury company starts selling into weakness, the premium disappears, the issuance window closes, and the stock re-rates to a discount. With STRC, Strategy would be repeating 2025, but with its own capital structure at stake this time.

Looking beyond Strategy’s Stretch

When you step back from the company, this episode tells us what it could mean for the industry beyond this one instrument.

The broader crypto market shed roughly 20% of its market cap over the last month. Bitcoin ETFs have recorded seven straight weeks of net outflows, their longest streak ever since launch. The Fed has turned hawkish, and the May PCE inflation print was 4.1%. While none of these was about Strategy, the unwinding of STRC is happening inside this environment. It’s hard to deny that the two don’t feed off each other.

With exchanges making it easier for retail investors to gain BTC exposure, it could also be a case of capital rotation from high-cost or less stable Bitcoin instruments like ETFs, DATs, and proxy holdings like Strategy.

The rise of perpetual contracts and the ease with which retail investors can use leverage on these contracts, with minimal margin risk, allow them to do what they once could only do with MSTR. The wavering correlation between MSTR/STRC and BTC price is less trustworthy than the near-perfect correlation a BTC perp contract has to the spot BTC price. This makes it a no-brainer for an investor to prefer a perpetual contract over a proxy for BTC exposure.

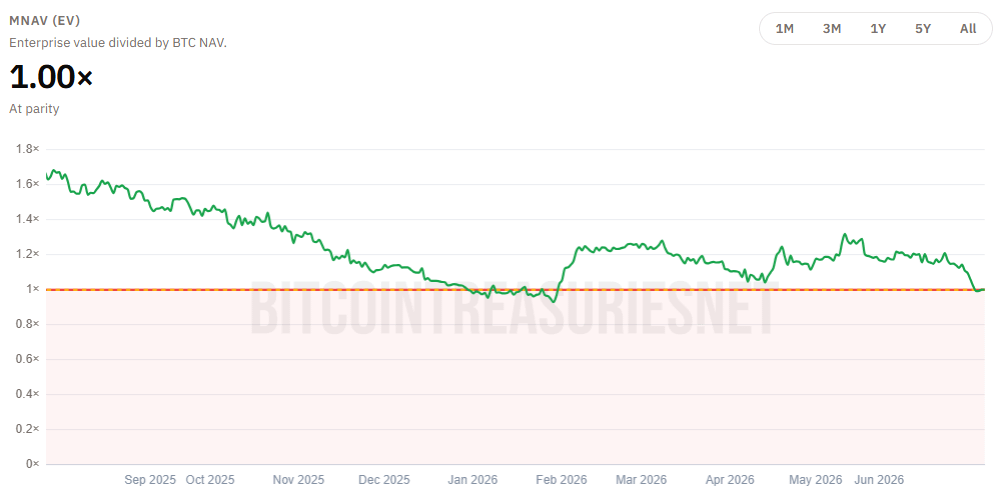

But STRC failing is its own undoing. The instrument is struggling to find demand because its credit story has broken down. The investors have lost confidence in Strategy’s ability to sustain a loop around a credit instrument whose dividend payouts had to be sourced by issuing the same instrument. When that loop broke down, it dragged MSTR’s price down with it. MSTR’s premium to net asset value has compressed to near-parity, implying the market doesn’t value the company above its underlying assets.

This completely inverts the structure that Strategy relied on. For years, the BTC price drove Strategy’s stock, which in turn drove its ability to raise capital. This capital funded its bitcoin purchases. Now the instrument’s credibility is driving the stock price, which in turn feeds back into perceptions of bitcoin exposure. A tale of tail wagging the dog.

This raises a question I did not expect to be asking when I wrote the last piece. If STRC’s fate is increasingly about Strategy’s credit and less about bitcoin’s price, what does that mean for the dozens of other bitcoin treasury instruments that launched in its wake?

Strive’s SATA preferred stock, the closest structural clone of STRC, hit an all-time low of $79 the same week. SATA holders are paid a 13% annualised dividend daily. Strive holds roughly 19,800 BTC at a cost basis of $96,000, which is 60% above the current price levels. Strive has zero debt, no convertible overhang and no maturity-cliff risk. Yet, it broke below par.

Metaplanet in Tokyo holds over 40,000 bitcoin and has issued its own preferred instrument, MARS.

The fact that even a debt-free, structurally cleaner instrument like SATA could not hold par shows us that this is not a Strategy-specific problem. This might mean that the market is repricing the entire asset class for what they are. Not bitcoin proxies and crypto bets, but as credit instruments with all the fragility that comes with credit.

Strategy may recover from here if it were all about fundamentals. If BTC climbs back to $80,000, the collateral story revives in theory, and the ATM window reopens. But only if it were all that easy.

Strategically selling more of its BTC stack in the days to come might technically be far less than what the market’s daily trading volume can absorb. But a broken belief among investors alone can trigger a panic and lead to a market-wide sell-off.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.