Of everything in a game, the field carries the most weight. A team wins some and drops some, and season to season, the trophy moves around. But own the ground they play on and write the rulebook they play by. Every match runs on your turf and pays you rent no matter who lifts the cup.

This is BlackRock in crypto right now, even though all you can think about when I say this are ETFs.

BlackRock launched one; it swallowed something like a hundred billion dollars. Every outlet on earth ran the same piece about how the suits finally came for crypto. Fine, true. Also, the decoy.

An ETF is a product. You buy it, you sell it, it is right there in your brokerage account next to your index funds. If BlackRock’s Bitcoin fund vanished tomorrow, crypto would shrug and keep moving.

But today, I want to talk about the BUIDL playbook.

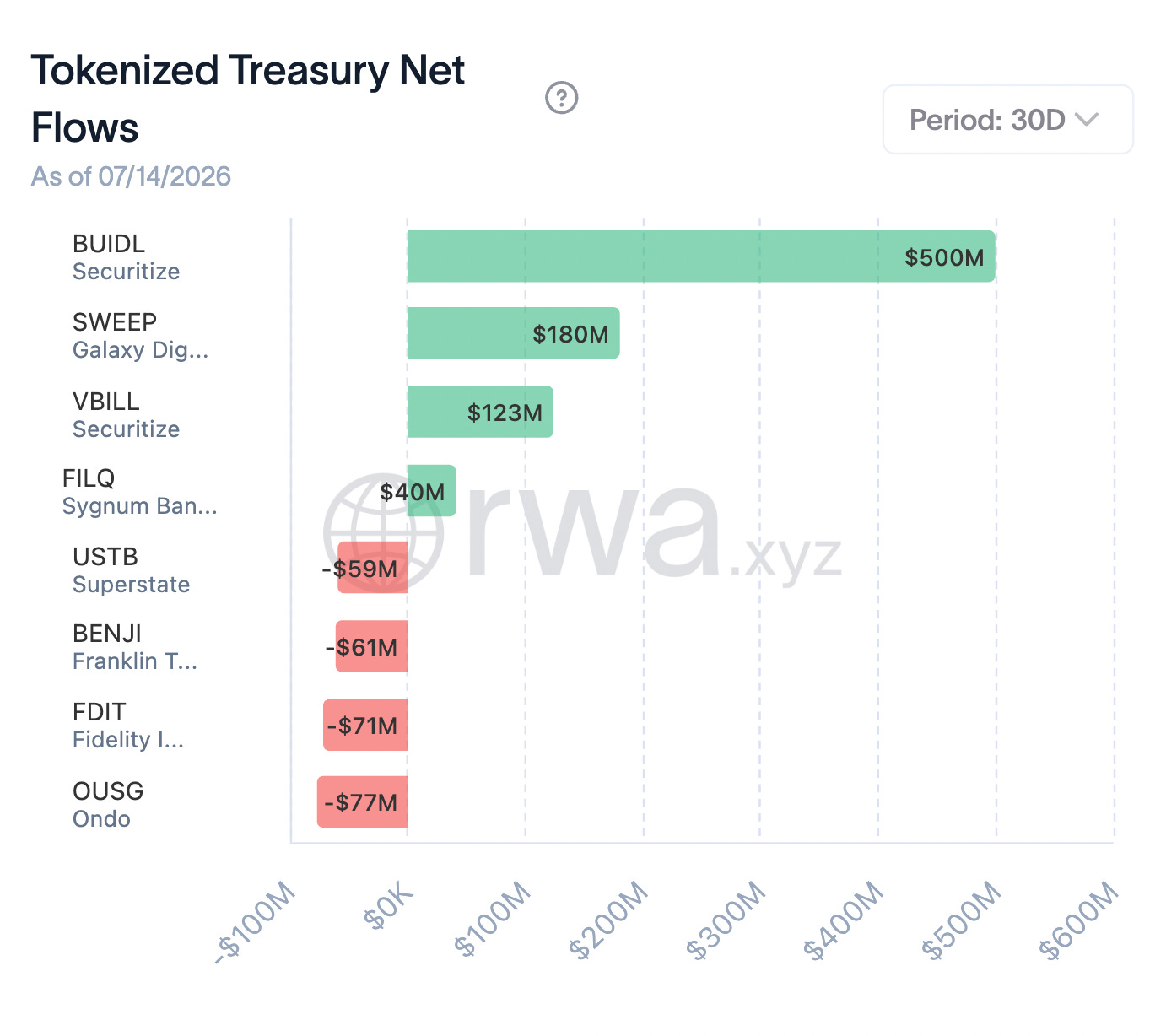

BUIDL is BlackRock’s tokenised money fund. It’s a pile of short-term US Treasuries and cash, chopped into on-chain tokens, that pays yield straight to whoever holds them. It launched in 2024, holding about $2.5 billion, which sounds small and is small. But I was looking at what it was turning into.

BUIDL holds Treasuries, so what’s inside the fund is the safest thing you can own. The danger is how you get in and out of it. BUIDL is permissioned. Only wallets that BlackRock and its partner Securitize have approved can hold it or move it, there’s a whitelist, which BlackRock controls. You can only cash it out during set hours, on BlackRock’s terms. BlackRock, or a regulator leaning on BlackRock, can freeze a wallet or halt redemptions. An ordinary crypto token moves the instant you tell it to. In BUIDL’s case, someone else can switch off for you. That is the reason it’s a risk, and it’s why everything built on top of it inherits that risk.

BUIDL is becoming the collateral the rest of on-chain finance gets built on. Today we are talking about that very sovereign takeover.

Start with Ethena and USDe. It is a synthetic dollar that’s now the 3rd-largest stablecoin. Ethena runs a second dollar, called USDtb, and more than 90% of its backing is BUIDL. When USDe’s engine sputters in a rough market, USDtb is the shock absorber it leans on. So BlackRock’s Treasuries already sit a layer below one of crypto’s largest dollar assets.

And a couple of weeks ago, it went further. BUIDL became the main reserve for the stablecoins that Ethena now builds for other companies, a core ingredient in a whole product line.

Let’s be precise about how much of USDe leans on BlackRock, though. On a calm day, barely any of it. USDe is backed mostly by crypto held against short futures, with only about 7% parked in plain stablecoins, including USDtb.

Ethena has $6 billion circulating supply, but only an $65 - $80 million native reserve to absorb market losses. When the funding trade stops paying, Ethena can’t rely on its own tiny buffer. It has to aggressively dump its capital into the Treasury fund.

So BlackRock becomes load-bearing right when things are breaking, the one moment you’d least want to learn your floor belongs to someone else.

In a standard crypto panic, if you want to exit a position, you interact with an automated smart contract. It doesn’t care who you are. But BUIDL is a permissioned, whitelisted token. If BlackRock’s compliance desk flags an address, or if regulatory pressure forces it to pause redemptions, that liquidity instantly freezes.

If the collateral under a stablecoin, or under an exchange’s margin system, can’t be sold at the exact moment everyone needs to sell, then every loan and every leveraged bet resting on it is trapped too, and they all unwind together. Traders think moving into a Treasury-backed asset is the safe play. They’ve traded the risk of crypto prices swinging for the risk that one company, on the worst possible day, won’t let them out.

Since April, big traders on the OKX exchange can post BUIDL as margin, the money they put up to back their positions. Meanwhile, the tokens sit off to the side in custody at Standard Chartered, a proper global bank. The collateral earns Treasury yield while it works. It’s the first time a bank that size has done this for crypto. Idle margin became a paying asset, and the asset is BlackRock’s.

A couple of weeks ago, BlackRock wired USDe into Aladdin.

Aladdin is BlackRock’s risk management system. It’s software that monitors portfolios and models what could go wrong. By adding USDe to Aladdin, BlackRock is now closely tracking it. The system is named after Aladdin, the story where a lamp grants wishes, but in this case, the benefits mostly go to whoever controls the lamp.

BlackRock isn’t doing crypto a favour with the USDe integration if you think so.

What they are doing is using their software to pull the inner data, risk profiles, and structural behaviour of the on-chain financial system into their own brain.

They know which players are overleveraged and roughly where prices have to fall before those positions are forced sold. So when a sell-off starts, BlackRock already knows which dominoes go first. Even if you think you are an independent crypto founder running a sovereign protocol, you are ultimately forced to price your risk using BlackRock’s proprietary math.

USDC, the second-largest stablecoin with around $78 billion in market cap, keeps the bulk of its cash reserves in a fund that BlackRock itself manages.

When you add it all up, BlackRock is a big buyer in crypto and also, crypto is being built on top of BlackRock’s collateral and margin, with its risk system overseeing both.

What does this look like from inside? A trader holds USDe, which leans on USDtb, which is mostly BUIDL, and then borrows against that USDe to place another bet. That’s what collateral does. It disappears into the foundation, and everything heavier gets stacked on top of it, meaning the loans and the leverage other people pile on those dollars, all of it assuming the bottom layer will hold and will let them out. If it doesn’t, they all have the same problem at the same moment.

Ethena may be loud, but other exchanges have started taking tokenised Treasuries as margin too, some from BlackRock, others from rivals like Franklin Templeton. BUIDL is the biggest one in the room. The biggest usually keeps winning. Traders want to hold the same collateral everyone else holds, because that’s the one that’s easiest to borrow against and sell in a hurry. So money keeps flowing to the biggest option, which makes it bigger still.

BlackRock has done this before and won it.

Index funds were cheap and slow, the oatmeal of investing. BlackRock rode its iShares brand as that oatmeal ate the world, and today the three big index shops, BlackRock alongside Vanguard and State Street, are the largest shareholders in close to 90% of the companies in the S&P 500. And for that, they just stayed under everything as the money piled in.

Aladdin did the same on the operational side. That risk platform now runs the books on north of $20 trillion in assets, somewhere above a tenth of all the financial assets on the planet. Much of that money belongs to firms that compete with BlackRock and still pay to use its system. So even the competition uses BlackRock’s math to measure its own safety. That means BlackRock sees every card on the table.

You want the measure of how deep that goes; look at 2008. When the crash hit and the US government found itself holding a mountain of toxic mortgage assets it couldn’t price, it hired BlackRock, asking it to put a number on it.

It happened again in 2020. When COVID froze the bond market, the Fed hired BlackRock to run the rescue, buying corporate bonds and bond funds by the billion. A large share of what BlackRock bought, on the government’s behalf, was BlackRock’s own funds. The money wasn’t BlackRock’s. It was public, the Treasury put up the cash, and taxpayers were on the hook for any losses. The government let BlackRock decide where the money went, and a chunk of it went into BlackRock’s own products. Its flagship credit fund swelled from $28 billion to $47 billion in two months on the back of it. BlackRock ran the buying and supplied the thing being bought, and when people cried foul, the reply was that BlackRock was just the agent and the conflicts were handled with care. BlackRock issues the collateral and runs the system that prices it, all handled with care. Look carefully, and that is the seat BlackRock is building in crypto now.

If tokenised dollars keep settling on BUIDL, and DeFi keeps parking its reserves there, and risk keeps getting priced through Aladdin, BlackRock becomes the operating system of crypto.

So why does this matter more than the ETFs? Because an ETF and collateral are different things. An ETF is just demand. People buy it for exposure, and if they change their minds, they sell, and no one else is touched. Collateral is the opposite. Once protocols use BUIDL to back their dollars and their loans, they can’t pull it out easily, because pulling it out means unwinding everything sitting on top of it, every dollar it backs and every leveraged bet resting on those dollars. So nobody pulls it. It stays put by default. People keep it because removing it has become too dangerous to try. You can sell an ETF in a second. You can’t rebuild the foundation of a system while everyone is still standing on it.

But this is the early days. That $2.5 billion in BUIDL is a small next to the stablecoin market, which runs past $300 billion, most of it Tether and Circle. On today’s numbers, BlackRock isn’t the floor of anything.

And you could argue this is good news. Crypto’s whole history of blowups runs on junk collateral, made-up tokens propping up other made-up tokens until the morning they all fall down together. Putting US Treasuries, watched by the most trusted name in the business, under your synthetic dollars is how you stop that. More trust.

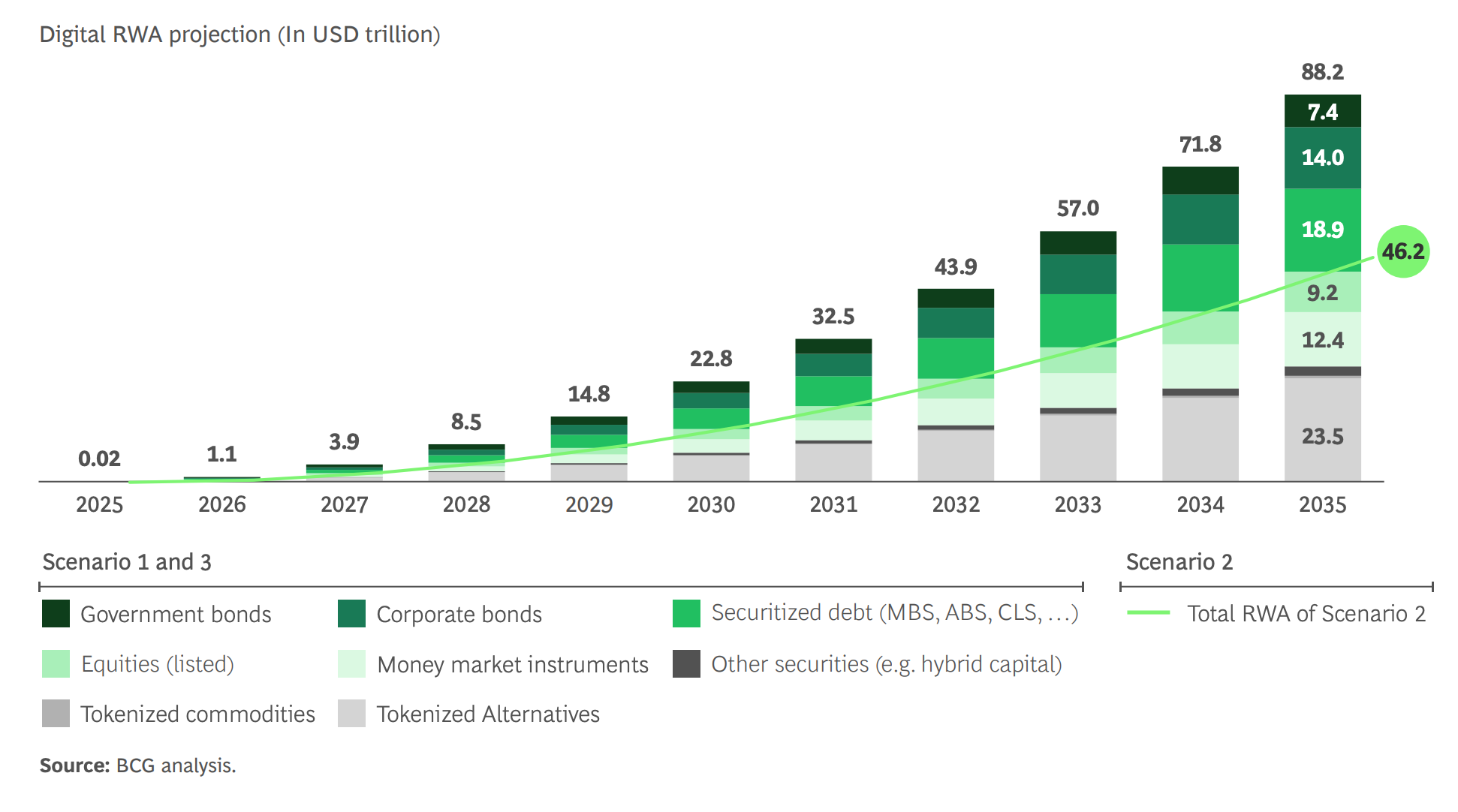

But first of all, size is the wrong lens. The right one is position. Ask how much is built on top of BUIDL, not how big BUIDL is on its own. A $2.5 billion fund that a dozen other products lean on matters far more than a $50 billion fund that nothing else touches. BUIDL is the largest single fund in the tokenized-Treasury market, a roughly $15 billion category that has more than tripled in a year, and Boston Consulting Group puts tokenised real assets on a path to $16 trillion by 2030. It’s small today. But it’s the base everything else is starting to settle on.

Secondly, the control. It’s the same deal every industry has already signed with BlackRock. You take the stability, hand over the control. It feels like a steal because the stability is the part you can see, and the control is the part that doesn’t bother you yet. And BUIDL is a permissioned, whitelisted, redeemable fund on BlackRock’s terms.

To grow and avoid crashes, crypto protocols needed ‘safe’ assets to back their tokens and support their trades. That’s why they started, or may start, using BlackRock’s BUIDL fund.

If the whole industry relies on BlackRock’s models to measure risk and its assets to back their dollars, changing the system becomes impossible; any change could destroy the market.

The industry gets the stability it wanted, but at what price?

That’s all for today. See you soon with another one.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.