The Art of Professional Stalling

The legislative clock is the banking lobby's favourite weapon.

The American Bankers Association recently walked into the Senate, looked everyone in the eye, and claimed that if we let stablecoins pay out a little yield, $6.6 trillion would vanish from banks. Presented with a financial apocalypse of such breathtaking gloom, the senators dive for the “pause” button.

Mission accomplished. In D.C., all you need is enough rhetorical chaff to ensure the status quo survives the session. No need to win the argument.

While the senators were asking questions, the White House dropped its own report. It turns out the banks’ “Great Deposit Migration” was... a bit of an overshoot.

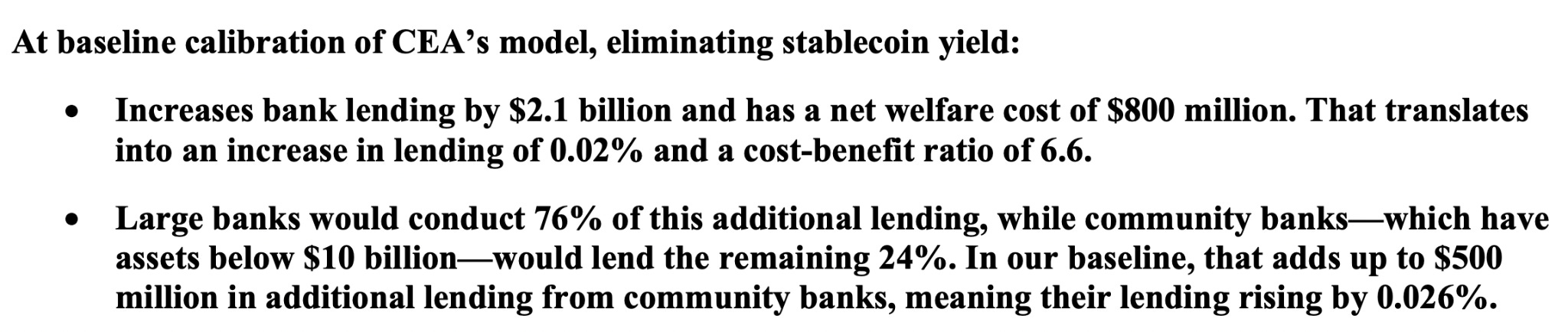

The White House report found that banning stablecoin yield would boost bank lending by $2.1 billion, 0.03% of the total. This little protectionist stunt would cost consumers roughly $800 million. The banks were wrong. More importantly, they were expensively wrong for the American public. And yet, the bill remains a permanent resident of the committee room.

The banking lobby knows the most powerful force in the universe is a Senator’s desire to get to the beach.

With the Senate recess just a few weeks away, the lobbyists just needed to talk until the clock ran out. The bill is now gathering dust in a committee room, the banks are keeping their deposits, and the rest of us are footing the bill for the delay.

Today, we are talking about the final nine weeks of a four-year marathon.

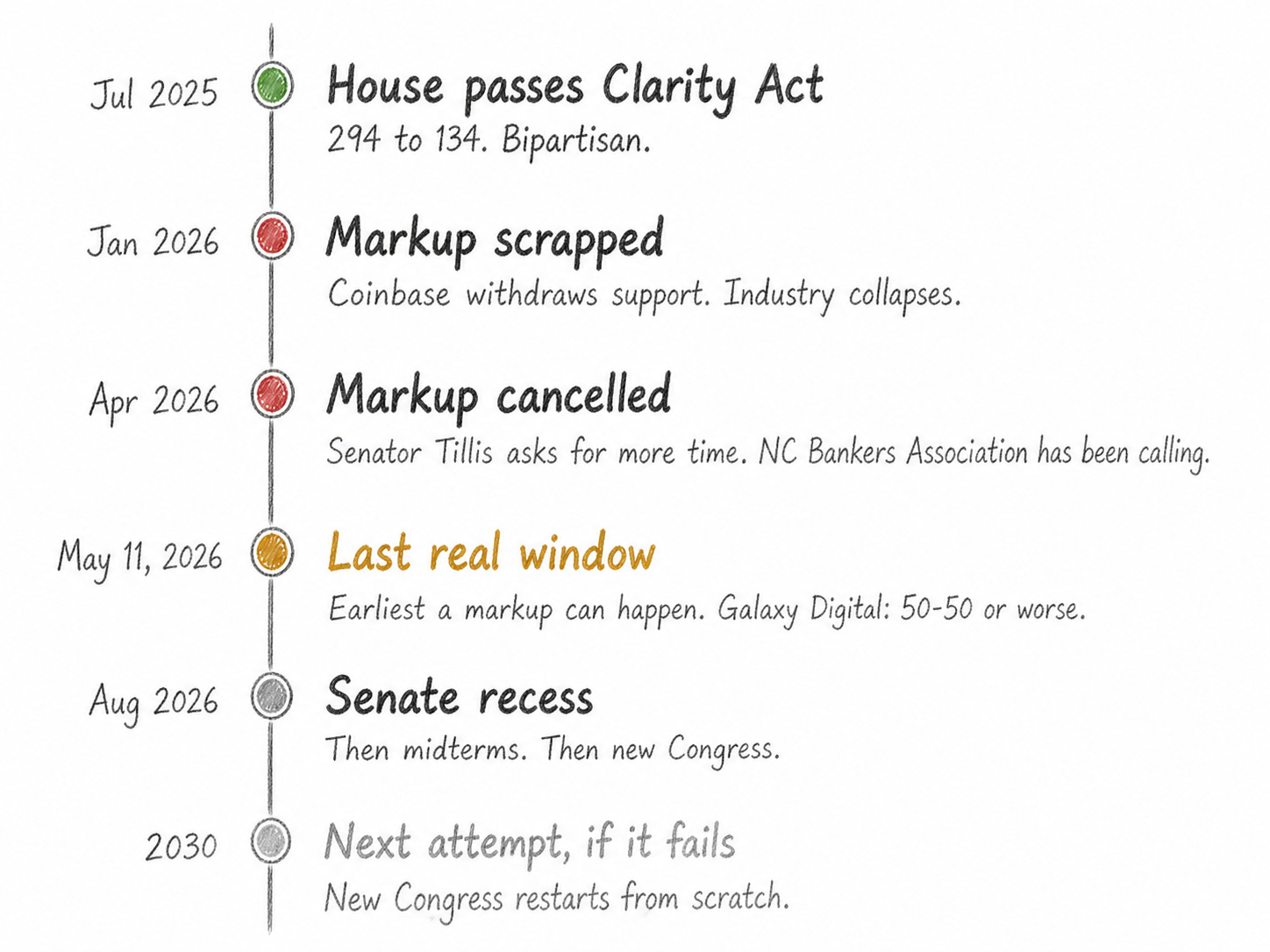

In July 2025, Congress passed the GENIUS Act, which did two things. Regulated stablecoins and banned stablecoin issuers from paying interest. It was a massive win for the banks, who successfully argued that if people could choose between a 5% yield on a stablecoin and 0.01% plus a “free” toaster at a bank, the entire global economy would spontaneously combust. Congress, terrified of math, signed it immediately.

But the GENIUS Act had a loophole. While issuers couldn’t pay interest, their “affiliates” and exchanges could still offer “rewards.” Crypto companies sprinted into that hole because they like money, and banks immediately started tattling because they hate competition.

Here’s where we talk about the Clarity Act. This was the “Fix Everything” bill, designed to close the loopholes and finally decide if the SEC or the CFTC gets to hold the leash on DeFi. It cruised through the House with a bipartisan 294-vote landslide.

Then it reached the Senate Banking Committee, where it has since become a “permanent lawn ornament.”

A January hearing was all set until Coinbase CEO Brian Armstrong pulled the rug. He withdrew his support over “concerns” about DeFi and token restrictions, but mostly because the bill threatened stablecoin rewards, which just happens to be how Coinbase makes a mountain of cash. Essentially, Coinbase pockets the interest earned on the government bonds backing those stablecoins, tosses a smaller ‘reward’ to the users to keep them loyal, and keeps the massive difference as high-margin profit. Funny how that works.

An April markup was considered likely, then ruled out after Senator Thom Tillis of North Carolina asked Chairman Tim Scott for more time to work through a compromise with banking groups. “It’s very important to me not to accelerate things,” Tillis told reporters, “to hear everybody and give them a rational basis for what we do accept and what we don’t accept.” The North Carolina Bankers Association had been running aggressive outreach to his office for weeks. Senator Tillis represents North Carolina. Love a beautiful coincidence.

At Bitcoin 2026 last week, Senator Cynthia Lummis warned that while the Clarity Act is 99% sorted, it’s also on life support. If it misses this year’s window, the bill is dead until 2030, when a fresh Congress restarts the entire gruelling process from zero.

The Senate is currently on recess, meaning the earliest markup can’t happen until the week of May 11. With only nine working weeks left, that’s tough math. Galaxy Digital currently pegs the odds at 50-50, which might be the optimistic view.

Can stablecoins pay yield? One slippery question.

The current compromise, brokered by Senators Tillis and Alsobrooks, attempts to split the hair right down the middle. It bans “passive yield” but greenlights “activity-based rewards.”

Banned: Getting paid for just holding a stablecoin (too much like a bank account)

Allowed: Getting paid for using it (the “credit card points” of crypto)

But no one has managed to define the difference in a way that makes both bankers and the crypto community happy. This ambiguity is a gift to the banking lobby. Every week spent arguing over semantics is another week closer to the August recess. The White House has stopped pretending to be neutral. The Council of Economic Advisers published an analysis in April that found the banks’ argument to be wrong. The White House crypto council’s Patrick Witt described the banking pressure as “greed or misunderstanding,” without specifying which.

The crypto industry hasn’t exactly been its own best advocate. When Coinbase’s Brian Armstrong yanked his support in January, he handed a gift-wrapped excuse to every Democrat looking for a reason to vote “no.”

Now that David Sacks has moved to a broader advisory role, the heavy lifting falls to Patrick Witt and the White House Crypto Council. They’re doing their best to keep the mood up, claiming the delay is just a chance to “resolve differences” and that we’re “closer than ever.” It’s a nice sentiment, but it ignores the fact that in politics, being at the one-yard line doesn’t matter if the clock hits zero.

Meanwhile, the market has continued building without waiting for anyone’s permission. Morgan Stanley launched MSNXX, a money market fund structured specifically for the management of stablecoin reserves under the GENIUS Act. Coinbase launched CUSHY, a stablecoin credit fund with tokenised shares. Agora is pursuing a bank charter. Products launching with asterisks, compliance teams adding caveats, innovation happening in spite of the uncertainty rather than because anyone has clarity about what is permitted.

The deposit threat that the banks are lobbying so hard against does not appear to care about the lobbying. Standard Chartered projected that banks could lose $1.5 trillion in deposits to stablecoins by 2028, regardless of whether yield is permitted.

Senator Alsobrooks’ March promise of ‘universal unhappiness’ was meant to signal a breakthrough. But in a Senate that’s currently on recess, a compromise that makes everyone unhappy is often just an excuse to do nothing at all.

The yield ban might slow the movement of money. But no amount of lobbying fixes a product problem. A 4.5 percentage point gap between what a savings account pays and what a stablecoin can pay is one.

If the Clarity Act dies this summer, the next Congress starts the process from scratch in 2027. A new bill gets written, negotiated, lobbied against, and markup gets scheduled, rescheduled, and postponed. It is 2030. The banks are asking for more time. Senator Tillis, or whoever replaces him, says it is very important not to accelerate things.

The stablecoin industry will be larger by then, less regulated, and considerably less interested in asking permission.

That’s it for today. Monday begins soon.

Stay tuned.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.