The Bitcoin Mining Dilemma ⛏️

With mining profits dwindling - large miners are absorbing or driving out smaller players, diversifying into AI and high-performance computation infrastructure and some adopting Bitcoin as treasury.

Hello, y'all. FOMO about missing out on Coldplay live? Play Muzify quiz to score the concert ticket👇

A little over a month ago, Canadian Bitcoin miner Cathedra Bitcoin website said it was a “bitcoin mining company”. One that was “working closely with the energy sector to secure the Bitcoin network.”

September 19 onwards, though, the company’s website reads “Cathedra is a bitcoin company”.

It announced a significant shift in its business strategy after seven years of mining operations.

The company will now focus on acquiring Bitcoin directly from the open market, following an approach similar to that of MicroStrategy.

The firm will consider issuing equity, debt options, or hybrid securities to finance Bitcoin acquisitions, similar to MicroStrategy and Metaplanet.

The company’s website reads “Cathedra is a bitcoin company”.

The share price has declined 91% since its peak in October 2021, now trading at $0.08 USD on Canada's TSX Venture Exchange.

While not abandoning mining entirely, Cathedra plans to develop data operating centres to generate predictable cash flows for Bitcoin purchases.

Cathedra currently holds 23 Bitcoin, worth $2.5 million, ranking it 45th among corporate Bitcoin holders.

Reason? Dwindling inflows in bitcoin mining.

The company will “make all capital allocation decisions with the intention of maximising our shareholders’ per-share bitcoin holdings”, the company said in its September 16 - Bitcoin Treasury Strategy Memo.

Mining was not a reliable way to grow shareholders’ bitcoin per share, Cathedra said in the memo.

Indeed, nine of the ten largest (by market capitalisation) publicly listed bitcoin mining companies hold less bitcoin per share today than they did three years ago. And as a bitcoin miner ourselves, Cathedra has not fared better by this metric.

Bitcoin mining profitability declined for the third consecutive month when it hit a "recent record" low in September, showed a JPMorgan report.

This is not something recent. Neither is this just limited to Cathedra.

Bitcoin mining firm Rhodium Enterprises and six subsidiaries have filed for Chapter 11 bankruptcy. The company's liabilities range between $50 million and $100 million, while its assets are estimated at $100 million to $500 million.

The bankruptcy filing follows Rhodium's failure to repay $54 million in loans owed to lenders in July.

Core Scientific, one of the largest Bitcoin mining companies, filed for Chapter 11 bankruptcy protection in December 2022.

US Bankruptcy Judge Christopher Lopez approved Core Scientific's Chapter 11 restructuring plan, allowing the bitcoin mining company to cut $400 million in debt and emerge from bankruptcy by late January.

The company then pivoted towards providing infrastructure for artificial intelligence (AI) and high-performance computing (HPC).

There were more - Hut 8 Mining Corp and Bitfarms - who diversified into AI.

Then there was Marathon Digital.

The largest publicly listed Bitcoin miner announced its diversification in August 2024.

Not AI, though.

The $5.56 billion worth company took a leaf out of the books of the biggest publicly listed Bitcoin champion - MicroStrategy.

It decided to follow Michael Saylor’s strategy and start buying Bitcoin to give its shareholders exposure to the risky asset.

Read: Saylor's Trillion-Dollar Dream 💰

The struggle of Bitcoin miners

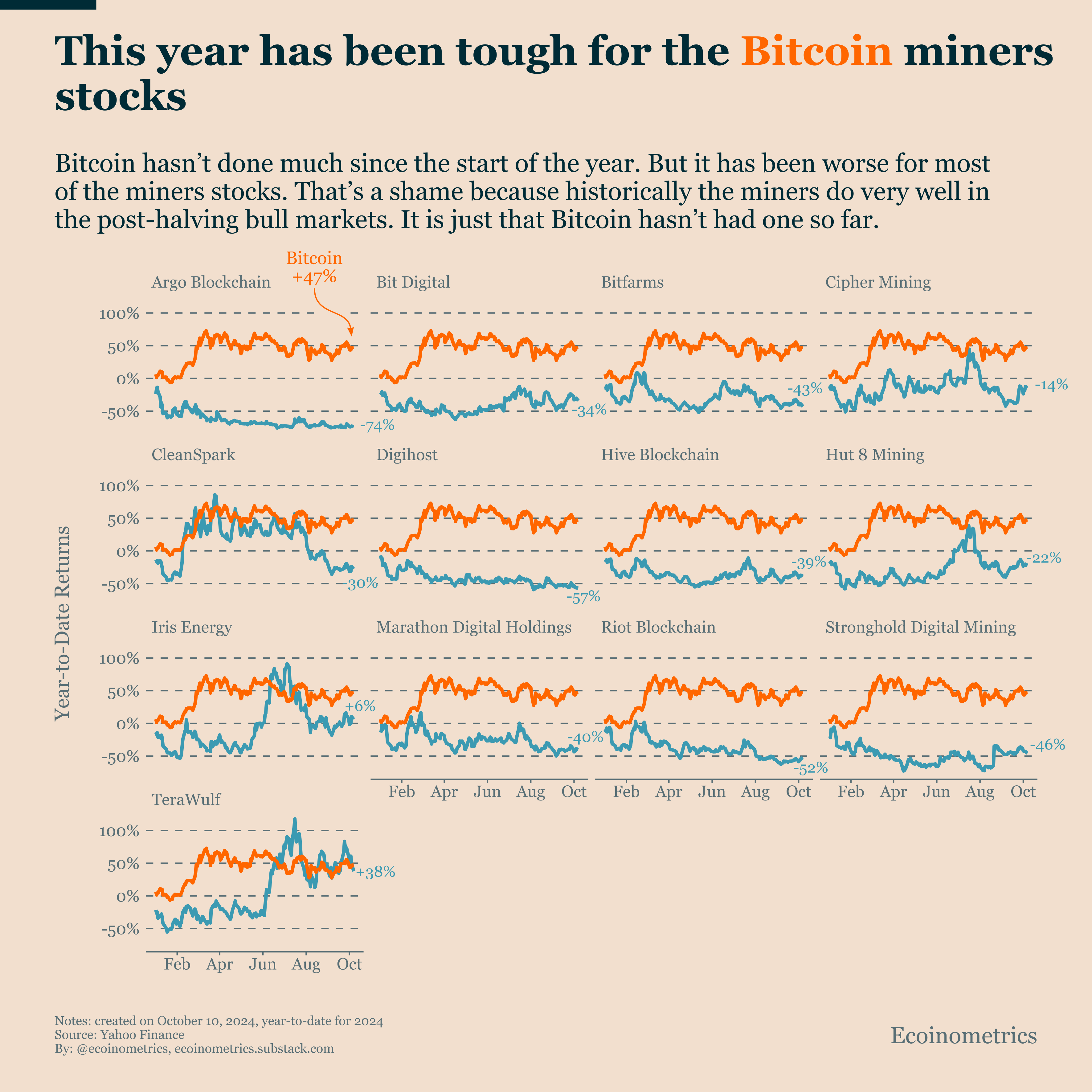

Bitcoin has shown limited movement since the beginning of the year. While it's up approximately 50% year-to-date, this gain is primarily attributed to the ETF launch. Since March, the cryptocurrency has been either flat or slowly trending downward.

The situation for Bitcoin miners has been even more challenging.

All mining stocks are underperforming Bitcoin

Most are experiencing negative returns

Why the mass exodus?

Mining revenues have been dwindling for a long time now.

What drove down revenue? Multiple things.

Firstly, US miners’ hashrate has gone up recently due to more competition in the mining space.

Higher hashrate means more computing power is being used to mine Bitcoin, making it more difficult to earn the same reward.

So, hashprice, the daily profitability, has decreased over 50% since before the halving.

What’s with halving?

Well, that’s another thing driving down revenues for miners.

The quadrennial event halves the number of Bitcoin that is rewarded to miners each time they solve the complex mathematical problem.

Miner revenues have taken a big hit after the most recent halving event in April.

The reward for mining a block (excluding transaction fees) started at 50 BTC in 2008 and is currently down to 3.1 BTC per block.

Meaning, same computational power being spent to mine and earn lesser Bitcoin rewards.

This has driven up average mining costs as well, since the halving event.

The missing ingredient

Typically, miners perform exceptionally well during post-halving bull markets, often significantly outperforming Bitcoin itself.

The primary issue is the absence of a post-halving bull market.

The current market conditions have not yet aligned with this historical pattern. It's not that Bitcoin miners are inherently poor investments; rather, the necessary conditions for their success have not yet materialised.

Problem of consolidation and centralisation

Bigger miners with larger risk appetite have made it tough for players with inferior processing infrastructure to compete.

Top four miners dominate the mining space with more than 80% share.

Heavy computation also makes Bitcoin mining a cost-intensive process.

Think of lots of environmental and carbon footprint.

Just like the old-school, traditional gold mining.

That also brings in a lot of bad PR from critics.

Plus, regulatory scrutiny and rules that follow.

But here’s the catch.

The Home for All the Music Lovers

Muzify - is more than just a platform; it's a journey into the world of music.

It provides an interactive experience through quizzes and exploration tools. For artists it’s a powerful tool for artists to connect with their fans.

Through custom quizzes artists can engage their audience, receive direct feedback, and build a loyal following eagerly anticipating their next release.

The platform offers a direct line to fans, fostering a sense of connection that goes beyond mere listening.

The GOLDen opportunity

Bitcoin is gold’s rival in the decentralised finance (DeFi) world.

Both of them seen as a store of value.

While gold has shown proven status of a stable asset during uncertain times, Bitcoin has largely been considered a risky asset.

But on the flip side, Bitcoin has outperformed the precious metal.

And, gold mining has direct environmental impact: soil degradation, deforestation and water pollution.

But, Bitcoin mining is not manual mining.

Meaning, the computation can be optimised to cut environmental and carbon footprint.

Especially, with AI.

For years, Bitcoin's price has followed a predictable pattern, surging every four years in tandem with global liquidity expansions and halving events. This cycle led many to believe that Bitcoin would continue to outpace gold indefinitely.

The past year has painted a different picture. While Bitcoin remains range-bound, gold has steadily appreciated.

The ratio of Bitcoin to gold has dropped from 32 ounces per BTC to 24 ounces, a significant reversal from its peak of 34 ounces during the 2021/2022 COVID-19 monetary expansion.

What's driving this shift? It's not Bitcoin's weakness but gold's unexpected strength. In a period without increased global liquidity or monetary expansion, gold's rise stands out as the anomaly.

China's central bank has played a crucial role, actively purchasing gold for nearly two years. This move aligns with a broader trend of central banks diversifying away from US dollar dependence.

These institutions show little interest in Bitcoin, explaining the divergence we're witnessing.

The return of global monetary expansion, historically a catalyst for Bitcoin's price surges. Until then, gold seems poised to maintain its ground against its digital rival.

What works for miners?

The synergy between Bitcoin mining and AI computing is emerging as a potential lifeline for the industry.

Miners' access to abundant energy resources and existing data centre infrastructure positions them uniquely to meet the growing demand for AI computational power.

This pivot not only offers a new revenue stream but also hedges against the volatility of the cryptocurrency market.

Core Scientific signed a landmark $4.7 billion deal with CoreWeave to provide 270 MW of hosting capacity for AI and HPC over 12 years.

Bit Digital launched Bit Digital AI, expecting to generate $92 million in annualised revenues by August 2024.

Hut 8 Corp secured a $150 million investment to develop its next-generation energy and AI infrastructure platform.

This shift leverages miners' existing infrastructure and power resources, potentially unlocking $38 billion in value for mining companies by 2027.

Miners who pivoted to building capabilities in artificial intelligence (AI) and high-performance computing (HPC) space have benefitted. The others, not so much.

Stock prices of Core Scientific and TerraWulf have stock up significantly while others such as Marathon Digital (MARA), Riot Platforms (RIOT), and CleanSpark (CLSK) have underperformed despite increasing their Bitcoin production.

Take MARA, for instance.

It produced its highest Bitcoin output since the April halving, while Riot increased its mined Bitcoin by 28%. But stock prices of both these companies did not reflect their production gains.

Token Dispatch View

With mining profitability dwindling persistently, expect larger and more efficient miners to absorb or drive out smaller players.

Consolidation by larger miners could lead to increased risk of centralisation that could jeopardise Bitcoin's decentralised ethos.

Even the largest mining companies are exploring innovative strategies to enhance their long-term value.

Miners must invest heavily in more energy-efficient hardware and use AI to cut down costs. Possible collaborations or expansion of miners into renewable energy space to gain cost leverage.

Some miners are also likely to take the Cathedra and Marathon Digital route to accumulate Bitcoin by mimicking MicroStrategy's approach.

Read: Should You Invest in MicroStrategy’s Bitcoin Bet? 🍔 🤔

Some are already leveraging their existing infrastructure to accommodate AI and HPC services, which require substantial power - something miners already possess. This could help beef up their revenues.

While the year has been tough for Bitcoin miners, their underperformance is largely due to current market conditions rather than fundamental flaws in their business models.

For investors willing to wait for the onset of a bull market (which is not imminent), mining stocks could still present a valuable opportunity.

Week in Funding 💰

Yellow Card. $33M. Cryptocurrency exchange to send, receive, and store your crypto with your Bitcoin wallet on Yellow Card.

Bitnomial. $25M. Marketplace connecting digital asset hedgers with institutional traders with derivatives exchange and digital asset settlement systems.

Canyon. $6M. OnChain AI Oracle leverages advanced cryptographic technologies to ensure verifiable AI power.

If you want to make a splash with us, check out partnership opportunities 🤟

Our sponsorship storefront on Passionfroot 🖖

This is The Token Dispatch find all about us here 🙌

If you like us, if you don't like us .. either ways do tell us✌️

So long. OKAY? ✋

The pivot to AI and high-performance computing sounds like a smart diversification strategy for miners. But it's interesting that despite increasing their Bitcoin production, companies like Marathon Digital haven’t seen stock price gains. It shows that even with higher output, investor sentiment seems tied more to Bitcoin's broader market trends than just production numbers.

It’s fascinating how these companies are adapting. Cathedra’s shift from mining to becoming more of a Bitcoin accumulator mirrors what MicroStrategy did, but on a smaller scale. It’s clear that mining alone isn't as sustainable long-term, but I wonder if this approach could stabilize the industry or if it’s just delaying the inevitable for smaller players.