Hello,

In the history of the internet, every attempt to embed a ‘Buy’ button has failed. Back in 2014, Facebook tried to add it to its news feed, where billions of its users could scroll past products and purchase them directly without ever leaving the app. But nobody ever clicked on it. Pinterest tried buyable pins in 2015, on what was truly the most shopping-brained platform on the internet. People literally go there to make boards of things they want to buy, and it still didn’t work.

Instagram shopping probably had the best shot of all of them: a billion users, the most visual product feed ever, and a whole generation that grew up buying stuff they saw on their phones, and Meta still had to bury the Shops tab because people would scroll, save or screenshot, do everything except actually press the buy button.

In September 2025, OpenAI thought it had cracked what none of them could. With 900 million weekly active users, Stripe as payment rails, and Walmart as a partner, they rolled out ‘Instant Checkout’ to let users find products through conversation and buy them right there without leaving the chat window. This was the best-resourced attempt at a platform buy button anyone had ever tried, but six months later, OpenAI has rolled it back. But why?

Check out today has become a full-blown platform war between Amazon, Google, and Stripe. In this piece, I will explore why Instant Checkout failed (it has nothing to do with the technology) and make the case for how stablecoin-enabled agentic rails can end this by making the fight itself pointless.

")

Why the Buy Button Never Worked

The simplest explanation for why Instant Checkout failed is that the tech was half-baked. There were complaints about incorrect product data, outdated prices, and inaccurate inventory levels.

And it implies that the idea was great and that a better execution could have fixed it. But I don’t buy it. I think the idea itself is broken, and the last decade of failed attempts to embed buy buttons confirms my bias.

Nearly every failed technology overestimates what it can do and underestimates how people behave. For example, the smart fridge was supposed to order groceries for you in 2016. Samsung’s smart fridge couldn’t get a single grocery chain to integrate its ordering system because no retailer wanted to build for a screen with a few thousand users.

Voice commerce on Alexa died because you physically cannot compare products through a speaker: shoppers need to see options side by side, and a voice interface that reads out five product descriptions is worse than just opening your phone. The problem with all these isn’t that the tech didn’t work or that people are lazy. It’s that they stripped more from the shopping experience than they added, and neither the consumer nor the merchant got enough in return to justify switching from what they already had.

Instant checkout fits into the same bucket, but there’s a trap specific to agent-driven purchasing that makes it even harder to implement. Whenever a purchase is complex enough that you’d benefit from an AI handling it for you, like picking furniture or choosing a laptop, the AI isn’t reliable enough to make the right call. And when a purchase is simple enough that an AI can actually reliably handle it, like reordering toothpaste or restocking coffee, the purchase is already so easy that the AI isn’t solving an actual problem.

The easier the purchase, the less you need AI to handle it; the harder the purchase, the less AI can handle it. There is no product category where an agent checkout is both competent enough to work and useful enough to matter.

“I want AI to do my laundry and dishes so that I can do art and writing, not for AI to do my art and writing so that I can do laundry and dishes.” - Joanna Maciejewska

And it gets worse. The whole idea behind agentic commerce is that AI can find you the perfect product so you don’t have to wade through options. But people presented with a single option are less satisfied with their product than those presented with three to four alternatives. The act of comparing and choosing is part of what makes you feel good about buying something.

When that is outsourced to an agent, it takes away the part where the purchase feels like your own decision. We saw a version of this back in 2007, when Google rolled out the “I’m Feeling Lucky” button that bypassed the search results page entirely. It instantly redirected you to the top-ranked website for your keyword. Less than 1% of Google users ever clicked on it.

Now, let’s say you take all the complaints about Instant Checkout and try to fix them. People want a cart feature that can hold multiple items instead of single-item purchases? Let’s add a cart. They want it synced with their existing accounts? Add account syncing. They want loyalty points, bundle suggestions, and delivery window options? Add all of that. Then they also want to browse and compare before buying? Let’s build that too.

But once you’ve done all of that, look at what you’ve actually built. You’ve built an e-commerce site. And at that point, the customer can just go to a real e-commerce site they already know and trust, which does all of this better because it has 15 years of optimisation.

So, when consumers have always opted out of buy buttons, there is no product category where agent checkout actually works. So why the push — and from whom? The answer is in the nomenclature itself. It’s called “agentic commerce,” not “agentic shopping,” because shopping involves discovery, comparison, and research. Commerce is where the transaction completes.

The companies most aggressively investing in agentic checkout right now are all payment processors and card networks, because Visa and Stripe earn revenue when transactions complete, not when people browse. There’s a reason AI applications that would actually save consumers money, like automatically renegotiating your cable bill or finding you a better savings rate, aren’t getting anywhere near the same level of investment.

Because those applications reduce transaction volumes, whereas agentic checkout increases them. The whole push to automate the purchase step is driven by the payment industry's desire to smooth over the one moment in the funnel where a person can stop and decide not to buy.

The Checkout War

Since then, every major platform has been racing to build its own systems and solutions to own the transaction layer, and the reason has less to do with any of them wanting to make shopping easier. Their responses also differ greatly from each other.

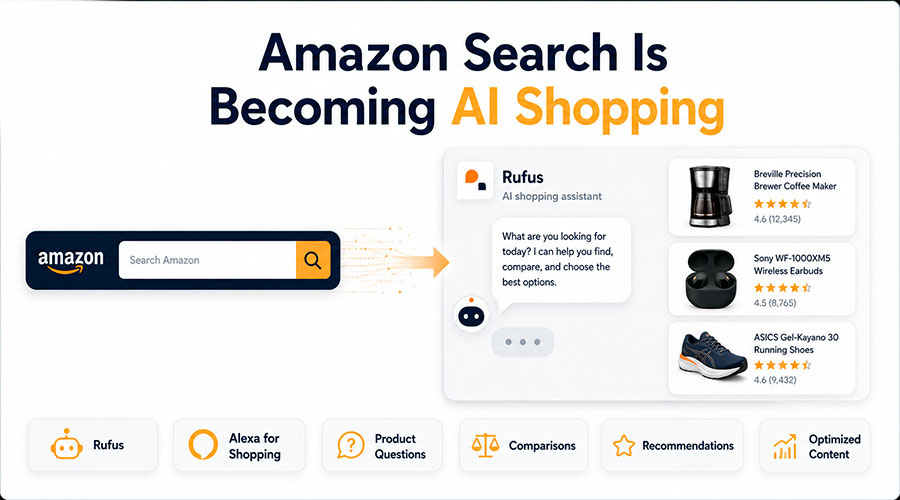

For instance, Amazon’s response is to lock agents out. It blocked dozens of AI crawlers from its platform and sued Perplexity for scraping its listings. It then created its own AI assistant within its platform, called Rufus, which recently powered about 40% of Amazon’s holiday transactions. Amazon doesn’t want to solve for agentic commerce for the open internet. It just wants to make sure your AI-assisted purchase, in any form, still happens inside Amazon, where the $68.6 billion in ad revenue and the Prime flywheel stay intact.

Google is playing the opposite hand: instead of blocking agents, it wants to arm them. It has built Universal Cart, which gives users a seamless shopping cart experience across Search, Gemini, YouTube, and even Gmail, and sits atop 60 billion product listings. Its Agent Payments Protocol can provide AI agents with tamper-proof spending mandates and programmable limits. They are applying the same logic they used for Google search: to be the infrastructure everyone builds on, because an open ecosystem always benefits Google the most.

And there is a subtle strategic play here. Google doesn’t need to put ads inside Gemini at all. It can use what people ask Gemini to improve its ad targeting on YouTube, Search, and all its other applications, acting as a signal-gathering layer rather than an ad surface. OpenAI has one product to monetise; Google has a dozen.

Then there’s Stripe, which processed $1.9 trillion last year, and it doesn’t care about who owns the front end at all. In its annual letter, it called agents a “new customer type” for the internet businesses, and compared this moment to the mid-90s, when there was an AltaVista for every Google. Stripe wants to be the rails regardless of whichever product wins, and it’s building its own agent commerce stack to make sure of it. Because right now, every major player is building their own incompatible standard. The fragmentation is only getting worse.

And they are all building on top of a card infrastructure that was never designed for how agents actually need to pay. An agent completing a task might make a dozen payments across multiple countries, in amounts and currencies ranging from fractions of a cent for an API call to thousands of dollars for a flight. And it can also be for services that have no website, legal entity, or credit history to underwrite.

The Rails That End the War

Whenever a transaction takes place on traditional card rails like Visa or Mastercard, the card processor has to approve the merchant and assume the merchant’s risks. In other words, the processor underwrites the merchant, meaning the merchant must be a legal entity with a website and an operating history.

This is because today’s card system’s risk models were built to underwrite businesses that sell to humans, and in the case of agentic transactions, there are no humans involved; it’s just one software endpoint that sells to other software. As a result, the agents can never be approved to use these payment methods.

Visa could theoretically retool to support these micro-agent-powered transactions and broaden its underwriting. But the card networks’ whole stakeholder ecosystem of issuers, acquirers, fraud teams, and merchants is optimised for transactions in the $20 to $1,000 range. So, retooling for sub-cent payments means accepting lower revenue per transaction dramatically, and the people who profit from the current model have no incentive to agree to it.

This is the classic innovator’s dilemma: the economics that make card networks dominant in human commerce are exactly what prevent them from serving agentic commerce at scale. Not to mention that the card stack we have today took 15+ years to ship things like Stripe Link and 3D secure. Agentic adoption can’t wait 15 years for the upgrades again.

Stablecoins solve this by turning dollars into software that can be moved across borders. Right now, moving dollars across the internet is more like shipping a physical package than sending an email. You have an ACH that takes days, a SWIFT that charges exorbitant fees and routes through correspondent banks, with verification on top of all of this, adding even more friction. If you compare this to a stablecoin transfer, it settles in seconds and costs a fraction of a cent, whether the amount is $0.001 or $100,000.

The recipient doesn’t need a legal entity or a merchant account because the rails are permissionless, so there is no underwriting process to pass through. Micropayments can work natively because there is no fixed fee floor, eliminating transaction costs. And because stablecoins are fully programmable money, you can encode spending rules directly in the payment itself, which is something card infrastructure has no equivalent for.

Coinbase recently launched Agentic Wallets to address this. With this, you can give an agent spending permissions enforced by a smart contract. The contract defines exactly which token can be used, how much, for what time period, and who the authorised spender is.

If you compare this with a traditional card network, the limits are enforced by the bank’s software, and it can be delayed, overridden, or even bypassed during an outage. A spend permission is enforced by the smart contract itself, so it can never overspend because, by default, the blockchain will not execute the transaction. And all of this can be wrapped in the backend through account abstraction with passkeys and social recovery, so the crypto plumbing disappears, and it works like any other banking or financial app.

The window to move on this is narrow since payments are sticky products. Devs building agents need a payment system that works right now, and cards are nowhere near ready. When they start building their payment flows on stablecoin rails because nothing else supports what they need, those integrations won’t migrate back to Visa, even once Visa eventually figures it out. New relationships built on stablecoins become old relationships still built on stablecoins, and the window for this is 12-18 months, while card networks are still trying to understand what agents even are and how they play out.

The checkout war is a fight over who gets to be the next middleman. Stablecoin-powered rails and wallets are a bet that the middleman was never necessary. And that’s why this will take longer than any of us wants. There is too much money in being the middleman for anyone to let it disappear easily.

That’s all for today.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.