Hello,

Loans are bets on collateral. For over a decade, the SaaS companies enjoyed excellent access to debt by using their revenues as collateral. These subscription revenues were predictable and recurring, which made the collateral strong and reliable.

In the past decade, private credit funds have turned their $8-billion loan book into a $500-billion one, backed by this revenue. It seemed like a perfect model until AI arrived and disrupted it, rendering these subscriptions redundant. A customer paying $50,000 a year for enterprise software can now choose AI agents instead.

These SaaS revenues are no longer reliable and are being replaced by the chips that run the AI computation. The $40,000 chip, which sits in a data centre and loses about a third of its value every year, is now being used as collateral to secure debt.

It’s not the ideal collateral, but the shift is happening nevertheless.

The shift inverts a century of credit logic. Normally, you’d lend against a company’s cash flows rather than against its equipment. A going concern with predictable revenue is any day safer than a depreciating machine. But with AI, software revenue has become less predictable than the chip that’s rendering the business redundant.

This shift has built an entire financing stack, from Wall Street futures to DeFi protocols, around that inversion.

Onto the story,

Prathik

This is not the first time physical equipment has been considered more creditworthy than the company using it. We have seen it happen during the American railroad era.

In the 19th century, railroads needed enormous capital to scale. But because of their speculative and overleveraged nature, no bank wanted to underwrite such credit risk. There was no problem with locomotives. They were tangible and carried resale value. If the railroad went bankrupt, you could repossess the engine and sell it to the next operator to recover the value.

The Philadelphia Plan created an entire debt product to address this gap. A trustee held title to specific rolling stock and allowed investors to fund about 80% of the railroad cost. The railroad made lease payments, and if it defaulted, the trustee took back the equipment.

The takeaway was that by separating the asset from the entity, you could finance an unreliable industry by betting on its most reliable component. The system was so efficient that when Penn Central collapsed (America’s largest bankruptcy until then) in 1970, the equipment obligations were honoured at 100% face value without having to seize and shut down the rails.

Later, aircraft finance also adopted the same trustee structure. The structure also laid the foundation for the principle behind modern secured lending: when the company is risky but the asset is essential, lend against the asset.

GPUs follow the same principle. Here, too, the entities using them are largely fragile competitors like AI labs, neocloud operators and inference providers. Their only moat is the generation of chips they have access to’. A better model on better hardware can displace their market position overnight. Just like the locomotives of the railroad era, the chip here is the essential asset. It sits in a secure facility and generates measurable revenue.

GPUs are also unwinding the old collateral regime.

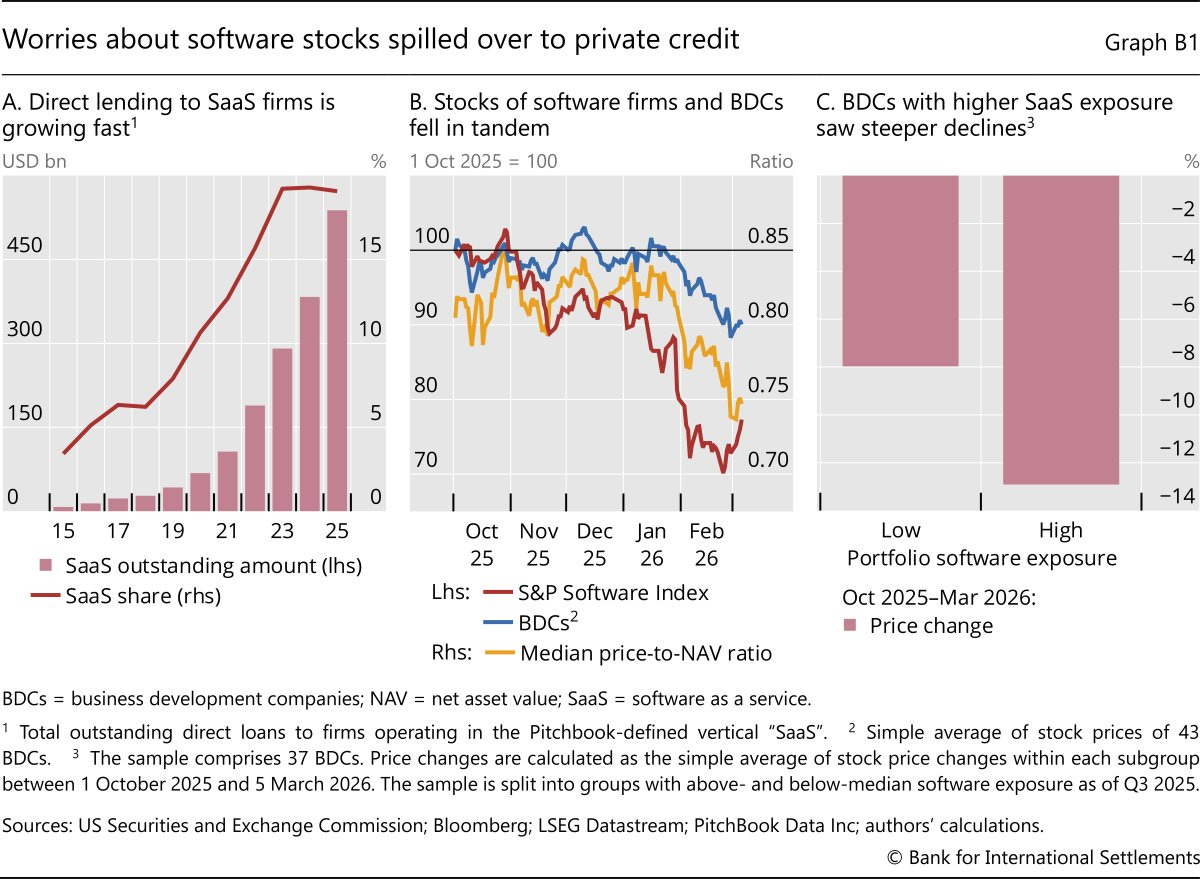

The Bank for International Settlements (BIS) published data showing that private credit’s SaaS loan book grew from almost nothing to a fifth of all direct lending in a decade. The rush to service SaaS companies with debt was built on the assumption that software revenue will be durable. That assumption cracked when AI agents offered a cheaper alternative. Software stocks fell 30% in four months, and UBS warned that private credit defaults could hit 13% in an aggressive disruption scenario.

SaaS subscription revenues are no longer the best collateral in tech.

But lending against GPUs has some inherent issues.

If you want to lend against a house, there’s an appraisal industry, comparable sales data, and a century of price indices. But until May 2026, a GPU had no equivalent data. GPU rental rates were scattered across bilateral deals, opaque broker markets, and DePIN protocol dashboards that most bank credit committees had never heard of.

But that changed three weeks ago. On May 12, the CME Group announced GPU compute futures with Silicon Data. CME’s pivot tells you traders want exposure to compute the same way they want exposure to oil and corn. A week later, Intercontinental Exchange (ICE) announced a competing product with Ornn.

These derivatives add a price-discovery layer to GPU lending, helping scale the credit market. But there’s another problem here. Traditional asset-backed securitisation involves bundling loans, tranching and risk-rating them, and getting them to trade. This takes 2-3 years for a new asset class. That’s too long a timeline for hardware that becomes obsolete in 3-4 years.

Computing assets also differ fundamentally from other traditional assets in how their values move. Over time, a house tends to be worth more than you paid for it. So the collateral appreciates. On the other hand, a GPU declines from the moment it is installed.

The day NVIDIA ships Vera Rubin chips, the resale value of its Blackwell chips falls. Today, there is no direct depreciation hedge. Maybe the market could develop GPU depreciation derivatives. But we are not there yet.

So, time is of the essence when you want to issue a loan against an asset that depreciates rapidly.

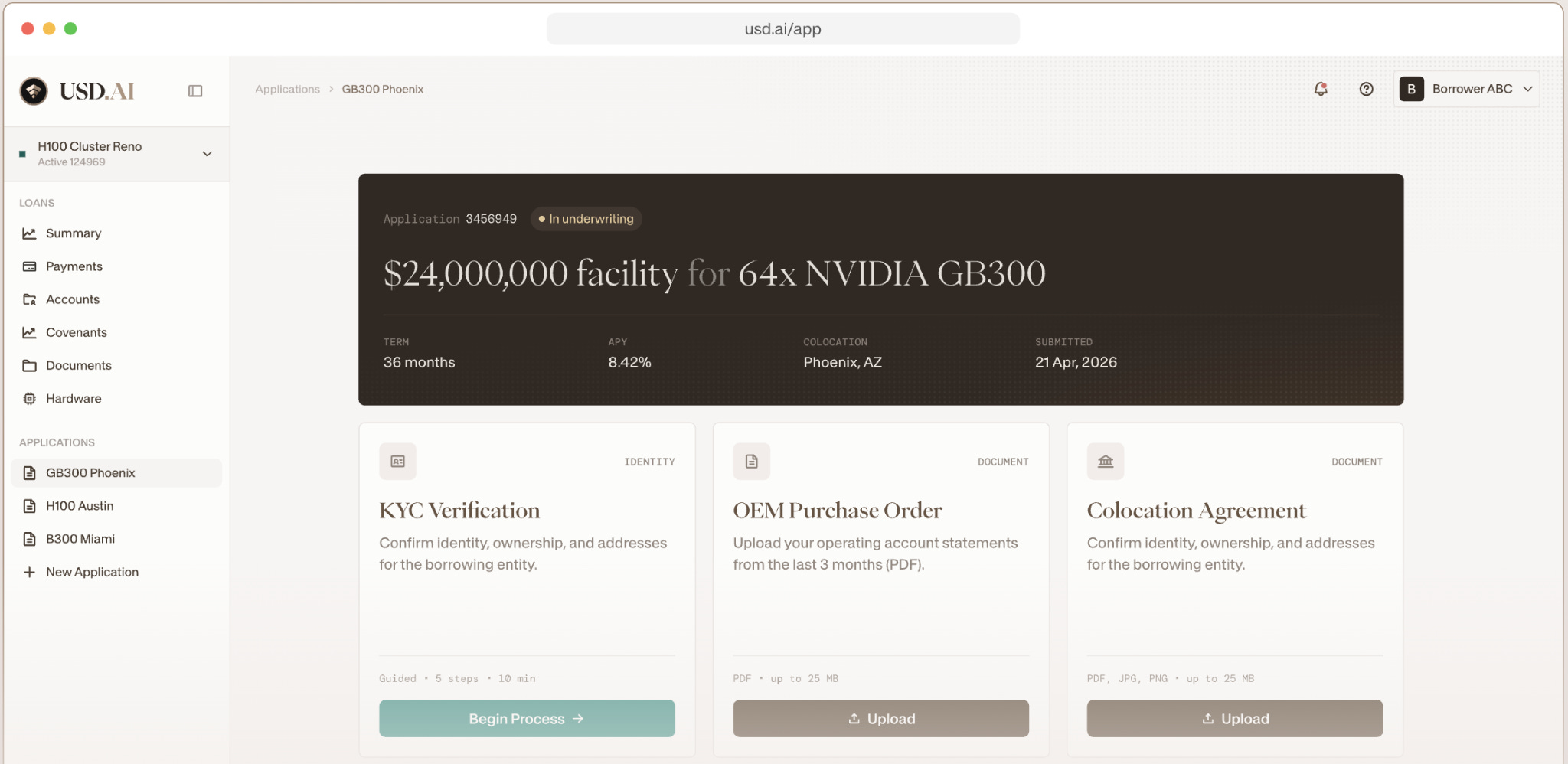

Enter crypto. Permian Labs’ USD.AI lends against individual GPU chips through special-purpose vehicles (SPVs), covers the loan risk through Barker’s collateral warranty, is fully reinsured by Munich Re, and tokenises the debt the moment the loan is created. So far, it has approved over $1.28 billion in GPU-backed facilities. This cuts the timeline for securitising a loan from years in traditional cases to near-instant deployment using on-chain credit products.

The USD.AI model changes who can access compute.

Today, the GPU financing market is skewed in favour of the big players. If you’re Meta, you borrow $27 billion at investment-grade rates. A mid-sized AI company is forced to go to a private credit fund that could charge as high as 25% interest, Permian Labs CEO and co-founder David Choi said on a DCo podcast last week. If you run a small AI firm, you must rent compute by paying roughly three times the ownership cost over the chip’s life.

USD.AI lends against the chip itself, not the company. A $100,000 deal for a handful of RTX Pro 6000s gets the same underwriting process as a $300 million facility. The borrower’s corporate profile is less important than the hardware, the revenue it generates, and its insurance coverage.

Asset-backed loans work only when the financial system moves as fast as the collateral depreciates. On-chain issuance is one way to do that.

But can GPU-backed debt hold up during a market downturn? Nobody knows. The market hasn’t been tested yet. Lenders have not been forced to repossess and bulk-sell a rack of H100 chips because the next-generation chip got shipped. Even the insurance backstop hasn’t been tested yet, although being live since February 2026. The secondary market for used GPUs is yet to mature.

But the industry isn’t waiting. It has already started building the pricing infrastructure around the asset.

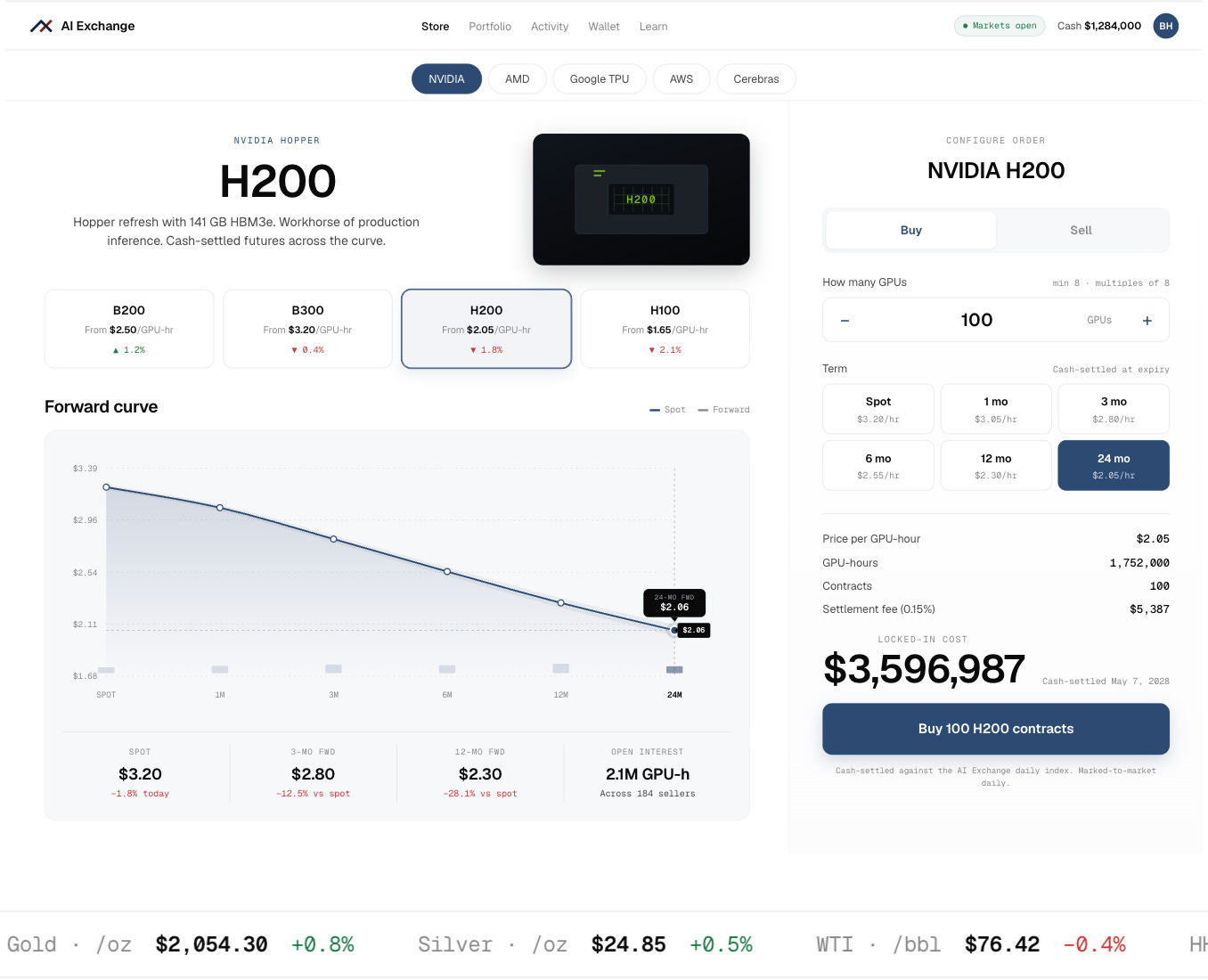

Architect, which started as a trading technology company, is now turning compute into a tradeable commodity through an exchange platform. Its American Innovation Exchange is a U.S. derivatives market built specifically for the AI economy, with contracts tied to GPU compute costs and other AI supply-chain inputs such as energy, power and metals.

Architect offers futures and options across H100, H200, B200, and B300 chips, with contracts ranging from monthly to yearly. Its target customers include traders, neoclouds, hyperscalers, model labs and lenders trying to hedge long or short compute exposure.

Although there is no resale market here, a derivative contract on a used H100 chip indicates its value after its first use. A futures market on computing power tells us what the market thinks a chip’s earning power may be worth.

These contracts don’t solve the problem altogether. If a borrower defaults, somebody still has to take custody of the machines, verify the hardware, find a buyer and sell the chips to recover value. But it adds a market price for depreciation and future compute demand, which the GPU credit currently lacks.

So, should we abandon GPU-backed credit markets? It isn’t an option. The old market built on SaaS cash flows is deteriorating rapidly. The hyperscalers, including Microsoft, Google, Amazon, Meta, and Oracle, are spending a combined ~$800 billion on AI infrastructure in 2026. All this needs financing.

None of these problems is unique to GPU-backed loans. Every collateral regime in financial history faced a version of this problem. Mortgage-backed securities had to survive the 2008 crisis. Auto loan asset-backed securities (ABS) faced subprime stress. But there is a pattern in this. Once a debt market emerges, it scales, encounters a downturn that tests its recovery assumptions, and then either reforms or contracts.

GPU credit is still being built in real time. While CME futures help in price discovery, DeFi protocols provide speed, and private credit funds provide scale.

Right now, most AI companies rent compute because they can’t get a loan to buy it. Renting often accounts for 80% or more of their total costs without offering them any ownership. It’s as good as paying rent for an apartment forever because no bank will give you a mortgage. USD.AI’s thesis is that once chip-level lending scales, every AI company can own compute the same way home ownership expanded once mortgage securitisation made housing debt tradeable.

Historically, the company was the most fundamental unit around which finance was organised. Banks lent to the company, investors invested in it, valuation was derived based on its cashflows, and the world trusted its durability. The entire credit system, from leveraged loans to SaaS-backed private credit, was built on the assumption that a well-run business outlasts its equipment. The AI company may not have brand value, but the hardware it uses may have a resale market. This shift can alter what the financial system treats as the fundamental unit of value. The chip could outlive the company.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.