We tried everything.

NFTs were supposed to onboard creatives. Web3 gaming promised to bring blockchain to the masses. Social protocols like Farcaster and Lens promised a decentralised future for digital communities. Zora would prove that content could become a financial asset. Friend.tech made social capital literally tradeable. Memecoins — well, no one claimed those were civilisation-building, but someone was always saying they’d bring in the next wave of retail.

And then there are prediction markets. Polymarket might be the closest we’ve gotten to a genuine breakout, but it peaked on a U.S. election cycle, and the question hanging over it now is whether it can hold engagement when the stakes are lower. There’s also the whisper nobody wants to say out loud: the platform’s accuracy came partly because people with real information were trading on it. That’s a complicated thing to hand to a regulator or a mainstream user.

So here we are in February 2026. Bitcoin is deep in institutional custody (forget the numbers for now?). Stablecoins just got normalised overnight by GENIUS. The infrastructure is more mature than it’s ever been. And if you open the App Store and filter by Finance, the top crypto apps are Coinbase, Kraken, and Crypto.com. Trading exchanges. They’ve been trading exchanges for a decade. The breakout consumer app is still missing.

Why?

Why Are We Not There Yet?

Crypto evolves in violent bull-bear cycles. Most innovation shows up publicly only when it collapses. The public associates crypto with chaos. When Bitcoin crashes, people say, “I told you so.” They don’t understand the mechanics. But we can’t blame them for that. The signal-to-noise ratio is terrible.

Crypto was never built for the general audience. Builders focused on their own ideological path which is decentralization, censorship resistance, and self-sovereignty, and expected the public to catch up. But the public never asked for those things. They wanted faster payments, better savings rates, and easier ways to send money internationally. Instead, crypto offered seed phrases, gas fees, and manifestos about overthrowing the financial system.

Meanwhile, the world outside crypto moved on. AI took over the narrative. ChatGPT reached 100 million users in just two months. People who’d never heard of transformers were suddenly using AI daily. Crypto had no equivalent moment. The technology that was supposed to be the next internet got eclipsed by the technology that actually felt like the next internet.

Trust crises piled up. Macro instability became the baseline. And inside crypto itself, endless scandals kept proving the skeptics right. Do Kwon and Terra Luna. Three Arrows Capital. Celsius. FTX. Every few months, another “reputable” crypto entity turned out to be running on fumes or misusing customer funds. The regulatory response, Operation Chokepoint 2.0, and the SEC’s enforcement-only approach made things worse by driving legitimate projects offshore while doing little to stop actual scammers.

And very importantly: the UX still isn’t consumer-grade.

Compare the UX of a crypto social app to Instagram: On Instagram, you download the app, sign up with your phone number, and you’re in. You see the content immediately. Intuitive. No learning curve.

Now compare that to Farcaster or Lens. First, you need a wallet. Write down a 12-word seed phrase on paper and store it somewhere safe, lose it, and everything is gone forever, with no customer support to call. Then you need ETH to pay for gas to mint your profile. You have to understand what gas is, why it fluctuates, and why you might pay $5 one day and $50 another day for the same action. Connect your wallet, approve transactions, sign messages you don’t understand, and hope you don’t click a phishing site. Only after all that can you start using the social features, which are still missing the algorithmic feed, creator tools, and network effects that make Instagram compelling.

Or compare setting up a wallet to opening Cash App: Download, enter your phone number, link a bank account, done. Three steps. Five minutes.

Crypto wallet? You choose between dozens of options (MetaMask, Phantom, Coinbase Wallet), download, generate a seed phrase, write it down, store it securely, understand Layer 1 vs Layer 2, fund it with crypto from an exchange (which requires KYC and bank transfers), then learn how to manage gas, approve token permissions, and avoid scams.

For most people, this is a wall.

The friction is enormous. But the builders don’t feel it. The entire feedback loop of who builds, who tests, who gives feedback, and who invests is insular. When your beta testers all have MetaMask installed and understand gas fees, you never feel the friction that kills adoption for normal people. It’s like asking fish to notice water.

The graveyard is instructive.

Friend.tech tried to financialise social connections. The pitch: buy and sell “keys” to access private chats with crypto influencers. It generated $90 million in fees at peak, then collapsed to $71 in daily revenue before developers abandoned it. The problem wasn’t the technology. The problem was that nobody actually wanted their social graph to be a financial instrument.

Farcaster raised $150 million from a16z to build decentralised social media. Ex-Coinbase founders. Genuine technical credibility. Daily active users briefly hit 100,000, then collapsed to 4,360 engaged users. Monthly revenue fell to $10,000. The founders left to build a stablecoin company. The problem was that nobody cared whether their Twitter alternative was decentralised.

Axie Infinity built an entire parallel economy in the Philippines during COVID. Players earned more than minimum wage breeding digital creatures. Then, token economics compressed, and everyone stopped playing. The problem wasn’t the game mechanics. The problem was that nobody wants to play a game that feels like a job unless they’re desperate for money.

Who’s Actually Doing It Now?

The companies closest to real consumer success are financial platforms integrating crypto rails.

Coinbase

Coinbase is building what CEO Brian Armstrong calls the “everything exchange.” His 2026 roadmap makes this the company’s top priority—integrating crypto, equities, prediction markets, and commodities across spot, futures, and options.

What they’ve launched:

Stock trading. Zero-commission equities. 24/5 trading alongside crypto in the same app. The pitch isn’t “come learn about blockchain.” It’s “trade everything in one place.”

Prediction markets via Kalshi integration. You can bet on elections, Fed decisions, and sports outcomes without leaving Coinbase. The crypto part is invisible.

Perpetual futures for international users. Lending will borrow up to $5 million against BTC, $1 million against ETH. Primary token sales where retail users can buy tokens pre-listing via USDC.

Custom stablecoins where brands can create their own branded stablecoins backed by USDC. Stablecoin checkout is embedded into Shopify, with Checkout.com and PPRO launching in 2026. UK savings accounts offering 3.75% AER, FSCS-protected. They’re applying for a national trust charter that would grant expanded banking powers.

Coinbase is building infrastructure to help everyone come on-chain. A super app for their own users, yes, but more importantly, the Rails backend powering institutions, fintechs, and traditional banks entering crypto.

Base hosts over $7 billion in on-chain assets. cbBTC became the second-largest asset at roughly $2.5 billion. Their Morpho integration shows $2 billion in collateral backing over $1 billion in loans.

Robinhood

Robinhood is coming from the opposite direction: a stock trading app that’s rapidly becoming a full-stack crypto platform.

What they’ve launched: ETH and SOL staking for U.S. users. Perpetual futures with up to 7x leverage in Europe. Over 1,000 tokenised stocks, U.S. stocks, and ETFs available as tokens for EU customers, 24/5 trading, zero commissions. Their own Ethereum Layer-2 blockchain called “Robinhood Chain,” built on Arbitrum, is currently in testnet.

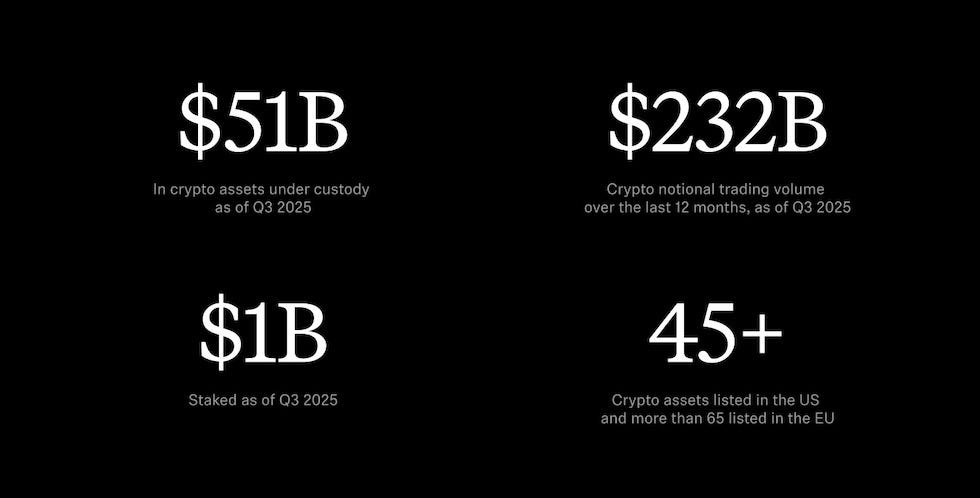

$51 billion in crypto assets under custody as of Q3 2025. $232 billion in crypto notional trading volume over the past twelve months. An AI assistant called Cortex that curates insights and market analysis for Gold members. A credit card where cash back auto-converts to crypto. Staking is positioned as the “top feature” and primary driver of user engagement for 2026.

They acquired Bitstamp to strengthen the global crypto infrastructure. They’re expanding into Indonesia. They’re building Robinhood Social, a feed where traders post alongside their actual trades and P&L.

They already have the neobank infrastructure, including direct deposits, credit cards, and cash management layering crypto on top.

Then there is the crypto’s favorite:

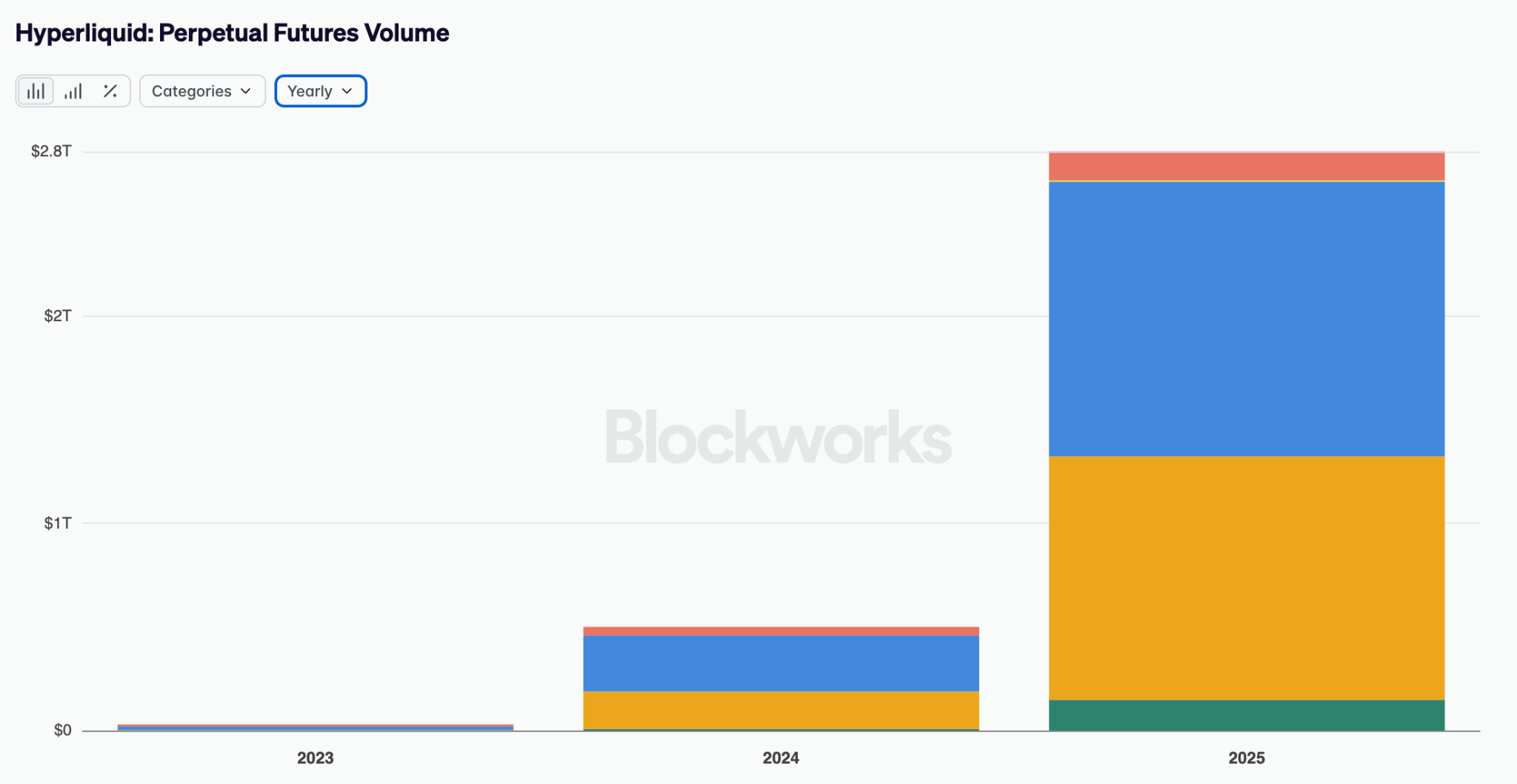

Hyperliquid handled $2.8 trillion in perpetual futures volume in 2025. It made the Forbes Fintech 50 with $0 raised. This is arguably crypto’s biggest consumer product success story.

But Hyperliquid isn’t a consumer breakthrough, but a crypto-native success story. It serves people who already understand perpetual futures, leverage, and order book dynamics. The volume came from traders already in crypto, looking for better execution. It just gave existing users a better venue.

What Are We Missing?

What would the perfect crypto consumer app actually look like? Not generic answers— specifics.

Invisible wallets. No seed phrase anxiety. Social recovery or biometric security. Progressive custody that starts simple and adds security as balances grow. The technology exists: account abstraction, passkeys, smart contract wallets. But adoption is slow because builders prioritise decentralisation purity over user experience.

Fiat on and off-ramps that are seamless. Instant settlement. No waiting three to five business days for ACH transfers. No explanation of the difference between USDC and USDT. No minimum deposit requirements. Just connect your bank account and move money.

No jargon. “Send $50 to Sarah” instead of “enter recipient address and specify gas limit.” Natural language interaction that understands intent. Error recovery that lets you undo transactions or cancel pending operations.

Familiar UI that doesn’t feel like operating a spaceship. One-click everything - payments, swaps, yields, social features. Progressive disclosure of crypto concepts for people who want to learn, complete abstraction for people who don’t.

A consumer-grade trust layer. AI-powered risk warnings that say “this looks like a rugpull” before you approve a transaction. Portfolio management that automatically optimises DeFi yields. Tax automation that handles reporting seamlessly. Protection that normal people expect from financial products.

Compliance is built in but invisible to the user. Selective disclosure, where you can share specific balances without revealing your full wallet. Transaction privacy through shielded transfers when needed. Identity protection, pseudonymous by default. Data sovereignty, where users control all personal information.

A strong narrative that explains why this matters without requiring a belief system. Not “overthrow the financial system” or “be your own bank.” Just “this is better at the thing you’re already trying to do.”

It should not feel like “using crypto.” It should feel like a better bank app.

The problem is that most crypto apps are built by crypto people, tested by crypto people, and funded by crypto people. When your beta testers all have MetaMask installed and understand gas fees intuitively, you cannot feel the friction that kills adoption for everyone else.

Crypto solves problems most people in developed economies don’t have. Self-custody and censorship resistance are genuinely important principles. But for someone with a functioning bank account and a stable currency, they’re abstract threats, not daily pain points. The pitch has been “you should want this because of what could happen” rather than “this is concretely better right now.” That’s a losing argument against Venmo and Cash App.

What We’re Not Appreciating

We act like crypto failed because we don’t have a flashy consumer app. But step back. The infrastructure is incredibly mature.

Stablecoins work. They’re functional infrastructure moving real value across borders daily. Security has improved massively. Smart contract audits are standard. Multi-sig wallets are common. Insurance protocols exist. The catastrophic hacks that defined 2021-2022 have become less frequent as the industry learned hard lessons.

DeFi rails are efficient. Uniswap, Aave, and Compound are protocols that process billions in volume with minimal downtime. Total value locked across DeFi exceeds $300 billion. Institutional players are using these rails for efficiency gains.

Institutions are building on it. BlackRock launched a tokenised money market fund. JPMorgan processes blockchain-based repo transactions. Traditional finance is quietly using crypto infrastructure because it works better than legacy systems for certain use cases.

Liquidity is deeper than ever. The bid-ask spreads that plagued early DeFi have compressed. Arbitrage bots keep prices efficient across venues. Professional market makers provide depth.

Institutional adoption came before retail. That’s unusual but important. If you believe AI agents are the future, AI agents need stablecoins. They need programmable settlement. They need crypto rails. Chris Dixon agrees that AI agents need programmable money, and traditional banking can’t provide it. As AI becomes mainstream, crypto infrastructure becomes essential infrastructure. So infrastructure might matter more than hype. The foundation is there. What’s missing isn’t technology.

Crypto consumer apps will win. But only when they stop trying to look like crypto.

The apps that break through won’t ask people to “use crypto.” They’ll offer something concretely better for a problem people already have. Savings that earn more. Payments that move faster. Transfers that cost less. Identity that travels with you. Ownership that’s actually yours.

The bank account will feel familiar. The interface will make sense. And somewhere in the background, stablecoins will settle, smart contracts will execute, and blockchains will finalise, without the user ever having to think about it.

Every generation builds tools it doesn’t fully understand yet. The people who laid telegraph cables across the Atlantic in 1858 thought they were building a faster way to send messages. They couldn’t have imagined they were building the nervous system for a global economy.

We tend to judge new infrastructure by the first things people build on top of it. The first things are almost always wrong. Imitations of what came before, dressed up in new technology. Horseless carriages. Moving photographs. Digital newspapers.

The real transformation comes later. When someone who grew up with the infrastructure builds something that couldn’t have existed without it. Something the original builders never imagined.

The application they’ll build ten years from now won’t look anything like what we’re currently debating on crypto Twitter. It won’t be a better version of something that already exists. It’ll be something we don’t have language for yet.

Our job right now isn’t to build that thing. We can’t. Our job is to make sure the infrastructure is there, that it works, and that it’s reaching the people who will one day build on top of it without ever reading a whitepaper.

Finance is how we get there. Because it’s the thing that puts the tools in enough hands so the real builders, the ones we haven’t met yet, can start.

That’s the strategy that’s been working all along. Not a pivot or a surrender. We just kept getting distracted by horseless carriages.

The most important crypto application hasn’t been imagined yet. And that’s the most bullish thing I can say about this industry.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.

Best article I've read of yours, solid suggestions stated with forward-thinking passion!

the best crypto app won't feel like crypto. that's basically the whole thesis