The Data Goes First

The data that prices every asset on Wall Street just moved to a blockchain.

In 1981, Michael Bloomberg got fired from Salomon Brothers. He was 39, had worked there for 15 years, and walked out with $10 million in severance and a very specific grievance about how Wall Street handled information. His response to being fired was, by any reasonable standard, unhinged. He started showing up at Merrill Lynch’s offices every morning with cups of coffee, wandering the hallways, handing them to strangers, and explaining that he was going to build them a computer that knew everything. The traders took the coffee. They were less sure about the computer.

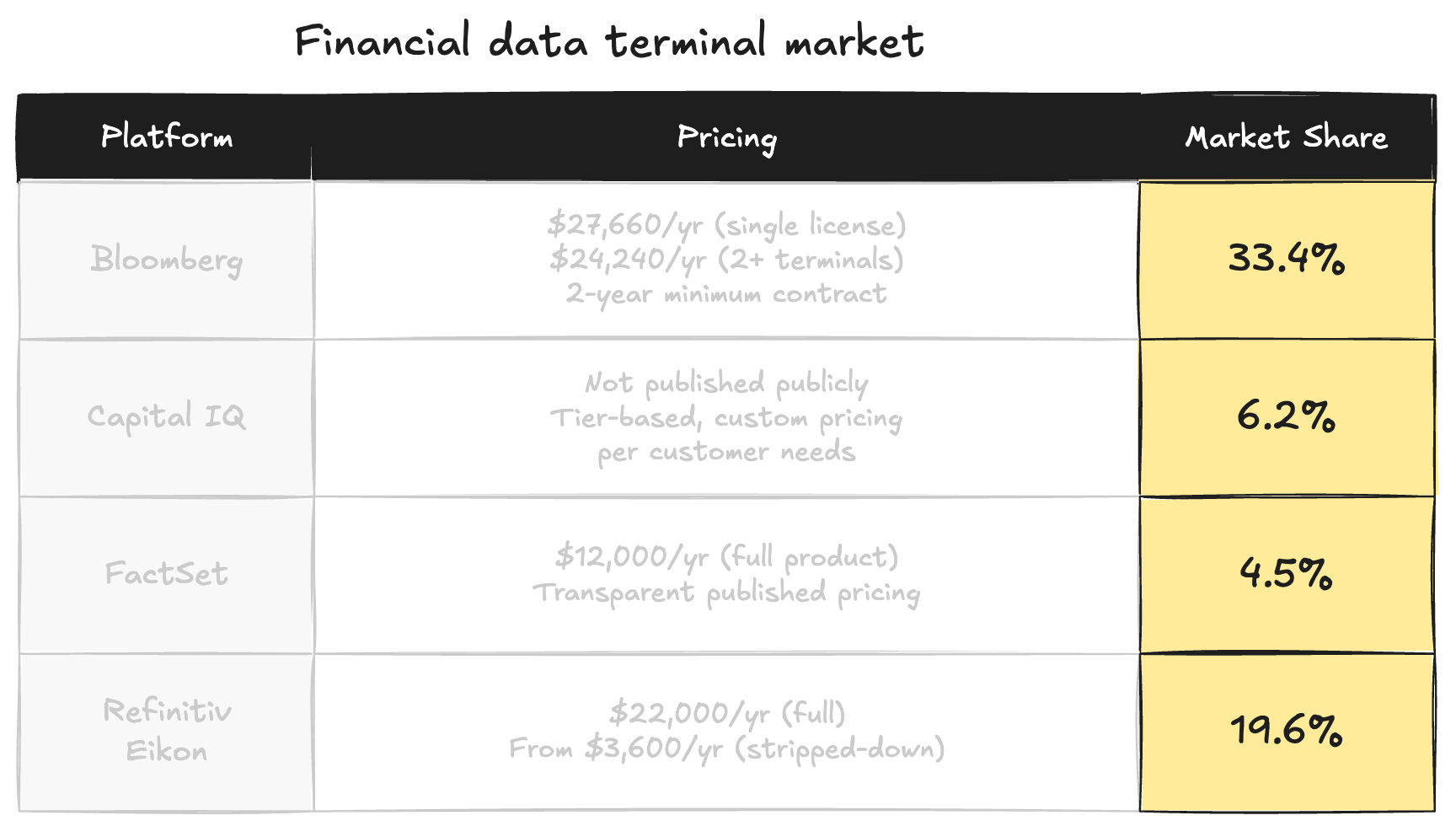

Forty-four years later, those computers cost $27,000 a year each. There are 350,000 of them, and Bloomberg collects roughly $10 billion annually from a business whose entire structural genius is that he inserted himself between the institutions that had the data and the people who needed it, and charged a toll on everything that passed through. The data was never Bloomberg’s. Merrill Lynch had it. Goldman had it. Every trading firm on Wall Street had it. Bloomberg just built the tollbooth, convinced everyone the tollbooth was the destination, and raised the price every year because what were you going to do, go back to calling brokers on the phone?

That model has survived every technological shift over four decades because no one could figure out a better distribution mechanism. Until, apparently, last Wednesday.

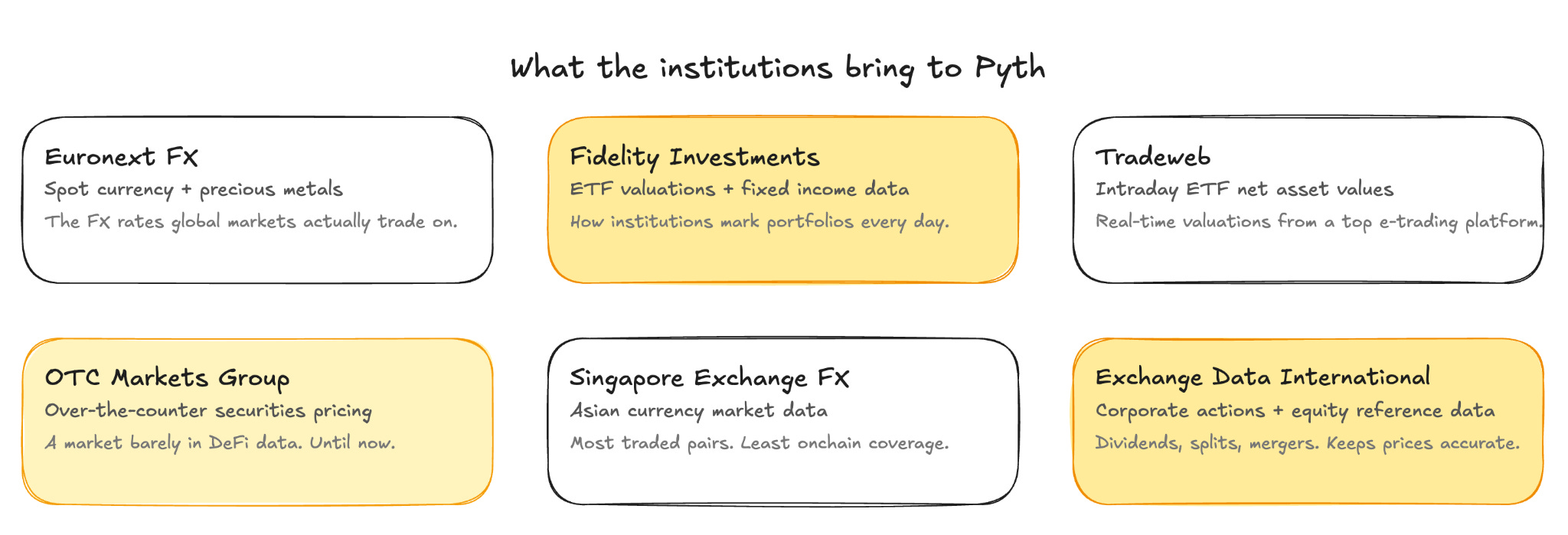

On April 9, six of the institutions whose data fills that tollbooth started publishing it somewhere else: Euronext, Fidelity, Tradeweb, OTC Markets Group, Singapore Exchange FX, and Exchange Data International, directly on-chain through Pyth’s new Data Marketplace, accessible to any developer on any of 100 blockchains. You don’t need a contract, a two-year minimum commitment, or a proprietary keyboard with yellow and green buttons.

Now write this down: the interesting thing about building a monopoly on other people’s data is that the other people eventually notice.

The financial data industry is worth around $30 billion annually and is one of the least discussed monopolies in the world, possibly because the only people paying attention to it are the ones already paying for it.

Bloomberg controls around 33% of the global financial data market, generating over $10 billion a year from its terminal business alone. Refinitiv, now owned by the London Stock Exchange Group after a $27 billion acquisition, holds around 20%. ICE Data Services reported $2.8 billion in market data revenue. After that, you have FactSet, S&P Global, Morningstar, and a handful of regional players serving niche segments. Together, the top four vendors control the overwhelming majority of how financial data moves from the institutions that generate it to the firms that need it.

The model is identical across all of them. Institutions such as exchanges, trading firms, banks, and asset managers generate pricing data as a byproduct of their work. They sell or license that data to vendors. The vendors package it, normalise it, add analytics on top, and sell it to everyone else at a significant markup, under long contracts, with proprietary access methods that make switching painful. A Bloomberg subscription locks you in for two years. Cancelling early costs 50% of the remaining contract value. Besides, everything about the Bloomberg experience is designed to make leaving feel harder than staying. The keyboard is different. The data format is different. Even the messaging system that half of Wall Street uses to talk to each other runs through Bloomberg, which means switching terminals also means giving up your contact list.

This has worked for four decades because the vendors solved a really hard problem of getting data from hundreds of sources, cleaning and normalising it, and delivering it with low latency across global infrastructure. Bloomberg earned its position.

Blockchain is a better distribution mechanism. Maybe not for everything, and not yet at full scale. But for the specific problem of connecting institutions that have data to developers who want to build with it, a public on-chain infrastructure with programmable access is structurally superior to a proprietary terminal with a two-year contract. By turning the data into an API with no switching costs, you provide any developer on any chain permissionless, self-serve access. That is what Pyth is.

Euronext, Exchange Data International, Fidelity Investments, OTC Markets Group, Singapore Exchange FX, and Tradeweb began publishing their proprietary market data directly on-chain through Pyth’s new Data Marketplace.

Euronext FX: Spot currency and precious metals. The FX rates global markets actually trade on.

Fidelity: ETF valuations and fixed income data. How institutions mark portfolios to market every day.

Tradeweb: Intraday ETF pricing. Real-time valuations from one of the largest electronic trading platforms.

OTC Markets Group: Over-the-counter securities. A market that barely exists in today's DeFi data.

Singapore Exchange FX: Asian currency pairs. The most traded FX market with the least on-chain coverage.

Together, these six cover a significant portion of the asset classes that DeFi has never been able to build around reliably because the data feeding those assets was not institutional-grade.

Why does data before assets matter

Everyone in crypto has been talking about the tokenisation wave for two years: tokenised Treasury bills, tokenised bonds, tokenised stocks. The whole conversation assumes the hard part is getting the assets on-chain.

But the hard part was the data. Before you can trade a tokenised Treasury bill in a DeFi protocol, you need to know what it is worth right now, to the second, with the same accuracy Goldman uses when pricing that instrument at a trading desk. Before you can build a lending protocol around real-world assets, you need price feeds that run continuously, sourced from institutions that actually make the market, not scraped from a website and updated every few minutes.

DeFi protocols require accurate, real-time traditional financial data for derivatives, loans, and structured products, but have historically relied on limited or slower data sources. This is why DeFi has been mostly crypto-to-crypto for its entire existence. The data feeding those products was not reliable enough, not fast enough, and not sourced from institutions with the credibility to make it defensible in a compliance conversation.

Pyth Pro, Pyth’s institutional subscription tier launched in September 2025, delivers price feeds with 1ms latency across more than 2,200 instruments. Polymarket integrated Pyth Pro in April 2026 to settle new markets for traditional assets, including major equity indices, commodities, and U.S. stocks, replacing manual or exchange-specific data with a standardised source aggregated from over 125 trading firms. Hyperliquid now runs perpetuals on oil and gold using Pyth feeds. The data quality is reaching the point where serious financial products can be built around it without apology.

The tokenisation wave needs this layer to function at scale. You cannot build a reliable fixed-income product on-chain without a reliable fixed-income price feed.

The original oracle problem in crypto was simple: smart contracts live on-chain, and prices live off-chain. Something needs to bridge the two. Chainlink, the dominant oracle for most of DeFi’s history, solved this by running a large network of independent nodes that fetch prices from third-party sources (exchanges, aggregators, data APIs) and submit them on-chain. Many independent sources, many independent nodes, reasonable decentralisation, acceptable latency.

Pyth took a different approach from the start by going directly to the institutions that are actually trading. More than 120 institutions now publish data through Pyth, including global exchanges, trading firms, and market makers. Instead of describing the Bitcoin price to Pyth second hand, Jane Street becomes the publisher. The data comes from the source, not from someone describing the source.

This is faster, more accurate, and more directly tied to real market activity than aggregated feeds. It is also more centralised in a structural sense: a smaller club of publishers who all know one another, validating their own data. Pyth has staking and slashing mechanisms designed to create economic incentives around accuracy. But the better framing would be that Pyth chose speed and data quality over maximum decentralisation. For institutional finance, that is probably the right trade.

Pyth was created with heavy involvement from Jump Crypto, an organisation that played a significant role in the events of 2022 that most people in crypto would prefer not to revisit. The publisher network is a small club of institutions that largely know one another and validate each other’s data. The staking and slashing mechanism creates an economic incentive for accuracy, but Pyth is both faster and higher-quality than what came before, and more centralised than the marketing suggests. You are not replacing a monopoly with a commons. You are replacing one concentrated system with another concentrated system that happens to run on a blockchain.

The PYTH token hit an all-time high of $1.20 in March 2024 and currently trades around $0.046, down roughly 96% from its peak. The obvious reason: using Pyth’s data does not require holding or buying PYTH. The network can grow substantially while the token remains range-bound, a known problem that Pyth’s reserve programme, which allocates a portion of protocol revenue to open-market PYTH purchases, is attempting to address.

Getting data from the institutions that generated it to the desks of people who needed it required hardware, proprietary networks, sales relationships, and ongoing support. Bloomberg solved all of that and charged accordingly. The data generators had no alternative distribution mechanism, so they sold their data to the middleman, and the middleman kept the margin. Blockchain removes that specific friction. Not the analytics, the workflow, or the keyboard. Just the part where someone had to carry the data from one place to another and charge for the privilege.

However, Bloomberg sells a workflow. The terminal, the keyboard, the messaging system, the analytics, the support team. Traders build their entire professional lives around it. Pyth sells none of that. It is a data layer that protocols plug into. The only overlap is the underlying data itself, and that is the part that just moved.

It matters because, if Fidelity publishes its ETF valuations on-chain, any developer anywhere can read that data without negotiating a licensing agreement, without paying $32,000 a year, and without waiting for a vendor to normalise the format. The data becomes programmable infrastructure rather than a proprietary product. The institutions keep control of what they publish and retain attribution rights. The middleman’s job, moving data from source to user becomes unnecessary.

These six institutions are choosing Pyth as a primary distribution channel, which is a different category of commitment from a pilot. Pilots get shut down when the person who championed them gets a new job. Primary distribution channels become operational dependencies.

Tokenised bonds, tokenised equities, tokenised everything. Most of that is still months or years away from meaningful scale. But the raw material that makes real-world asset products possible in DeFi is now accessible without a contract, a terminal, or a two-year minimum commitment.

Michael Bloomberg spent months walking Merrill Lynch’s hallways with free coffee because the data he needed was locked inside institutions that had no reason to give it to him. He built his entire business on that friction.

The tollbooth does not disappear all at once. Every monopoly in data distribution ends the same way. Not with a fight, or a law, not with a revolution. Mostly with someone, somewhere, asking why they were paying for something they already had.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.