Hello,

Up until last week, if you asked ten lawyers whether Ethereum was a security or a commodity, you’d get twelve different answers and a bill for $50,000. That’s been the reality of building anything in crypto in the United States. There were no clear rules because the regulator refused to establish them and later sued for non-compliance, citing an after-the-fact interpretation.

The SEC under Gensler brought 88 enforcement actions against crypto projects, and 92% of those were for registration violations, meaning companies were punished for failing to register under a framework the agency never clearly defined. It was absurd; everyone in the industry knew it was absurd, but no one could do anything about it because the alternative would mean leaving the country.

But that changed last Wednesday when the Senate Banking Committee voted 15-9 to advance the CLARITY Act. Elizabeth Warren called it a bill that “blows a hole in securities law since 1929.” She’s half right. The bill was shaped with heavy industry input. But the hole it blows should have been blown years ago.

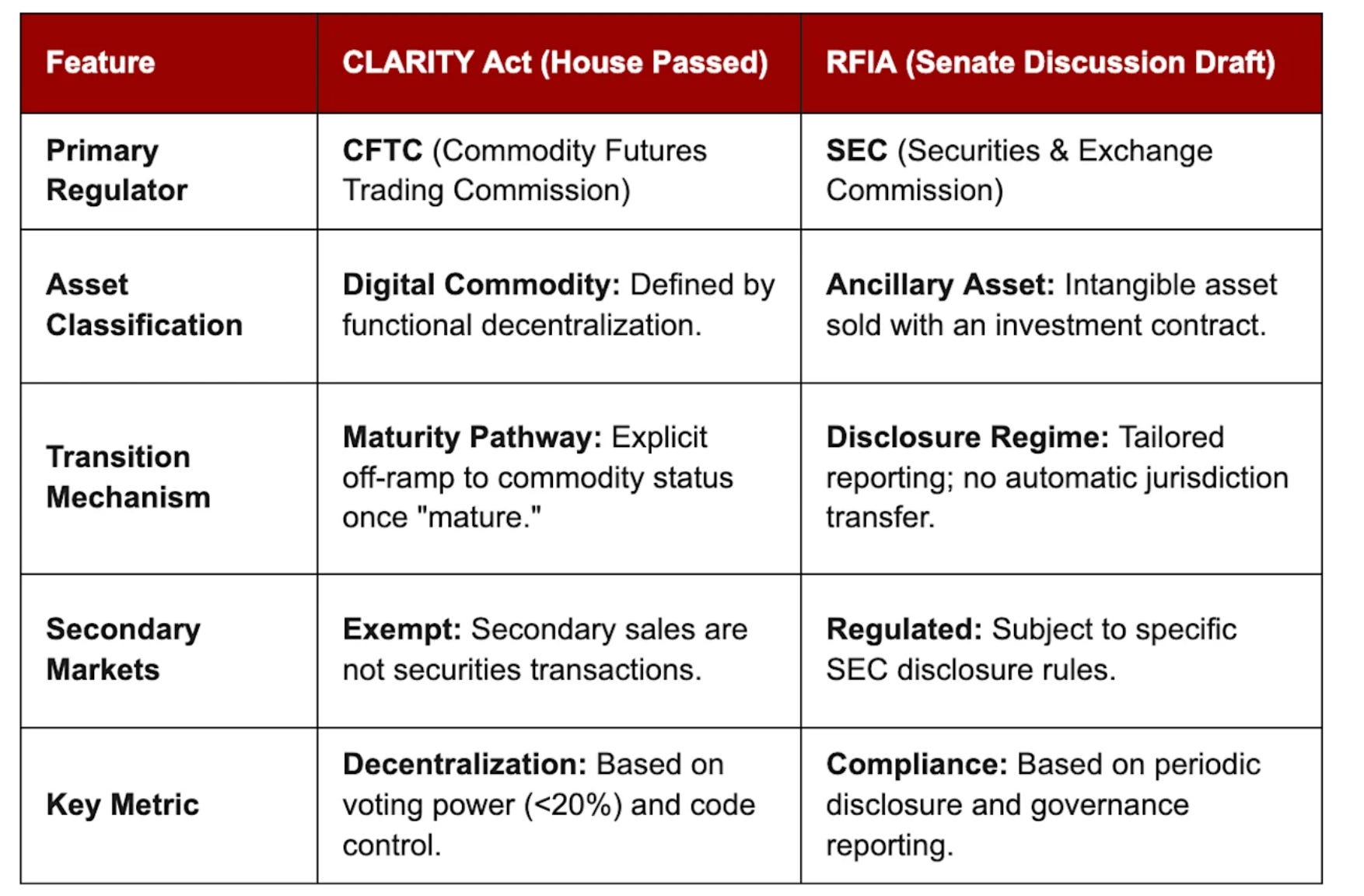

What does the CLARITY Act actually do? It gives the security-or-commodity question an answer backed by a real test. By default, every token starts as a security. The moment you raise money by selling tokens and promise to build something with that capital, that’s an investment contract under Howey, and you fall under the SEC. That much hasn’t changed; it’s been the case since crypto fundraising began.

What’s new is that there’s now a way out. The bill introduces what it calls the “mature blockchain” test. If your chain is open-source, runs on pre-established, transparent rules, and no single person or group controls more than 20% of the token supply, you can go to the SEC and say, We’re decentralised enough; review us. If they don’t push back within 60 days, your token is reclassified as a digital commodity, and regulatory authority changes from the SEC to the CFTC.

This shift from the SEC to the CFTC matters greatly because the two agencies operate in completely different ways. The SEC treats tokens like stocks, which means full registration, detailed disclosures, and continuous reporting obligations. The CFTC treats them like commodities, such as oil or wheat, with lighter oversight and lower costs, and its main job is to make sure markets run fairly rather than to decide who gets to participate in them. For any project that passes the decentralisation test, the day-to-day cost of being a regulated entity drops significantly.

You get four years to get there. You can file a notice with the SEC saying your blockchain intends to reach maturity within that window. As long as you’re making progress, you operate under a temporary exemption. But if you hit the four-year mark and you’re still not decentralised enough, the exemption goes away, and you’re back under full securities law with even stricter disclosure requirements than you started with.

If you pair this with the GENIUS Act for stablecoins, which became law last year, you will see that, for the first time, the United States has a complete regulatory framework for digital assets. Stablecoins have clear rules about reserves, licensing, and who can issue them. Tokens now have a concrete test that determines whether they fall under the SEC or the CFTC, and that test includes a specific threshold: 20%. But what does it mean for existing and new projects with a token? That’s where it gets interesting.

The Impossibility of Grassroots Launches

The biggest crypto assets will have no trouble with this test. Bitcoin has no single entity with anywhere near 20% ownership and has been treated as a commodity for years. Ethereum runs on over 1.07 million validators after the Merge and has the most distributed infrastructure of any smart contract platform.

The SEC and CFTC’s joint interpretive release from March 2026 already identified 18 tokens as digital commodities, including Bitcoin, Ethereum, Solana, XRP, Cardano, Chainlink, and Avalanche. If you hold any of these, you can breathe easy knowing the regulatory question is answered, and your token sits on the commodity side of the line.

The problem starts when you look past those 18 names in that list. Take Solana, it made the commodity list, but it sits in a grey area. It got there through an interpretive release, which is a regulatory opinion.

An interpretive release is basically the SEC and the CFTC issuing a statement saying, “This is how we read the existing law.” It carries weight; markets react to it, but it has no legislative backing. The next SEC chairperson can issue a new interpretation and change Solana’s commodity status overnight, without going through Congress or holding a vote.

The other group that needs to pay close attention is everyone who hasn’t launched a token yet. Under this bill, every new token is presumed to be a security from the moment it’s created, and escaping that means years of SEC disclosures, legal filings, and semiannual reporting. At the same time, you work toward the maturity threshold.

Hiro Systems, one of the few projects that actually tried to go through the SEC’s existing registration process, spent over $15 million on compliance and legal defence alone, which was more than they raised in the offering itself.

That gives you a sense of the real cost here. The bill includes a $50 million exemption cap for how much you can raise while your chain is maturing. Still, the compliance infrastructure needed just to operate within that exemption is so expensive that only venture-backed teams with law firms on retainer can realistically use it.

It means that if you’re a small team trying to build something new without institutional backing, you will have a hard time passing this test. The kind of grassroots, community-driven launches that gave us Ethereum in 2014, where anyone could participate in an $18 million raise with no regulator asking questions, those become illegal to pull off under this framework.

The DeFi Safe Harbour That Almost Wasn’t

The commodity classification and the decentralisation test got all the attention. But the DeFi developer safe harbour in Sections 309 and 409 may be the most important part of the bill.

The bill says that if you write smart contract code, run a validator, or build a self-custodial wallet, you are not a financial intermediary. You don’t need to register as a broker, you’re not a money transmitter, and the government can’t come after you as one. Code is not custody. That’s now written into the bill.

The credit for this goes to a guy named Roman Storm. Storm built Tornado Cash, a privacy tool on Ethereum. He didn’t hold anyone’s money, couldn’t freeze or reverse transactions, and couldn’t shut the protocol down even if he wanted to. The code was open-source and ran on its own. The U.S. government convicted him in August 2025 for operating an unlicensed money-transmitting business anyway, because no law at the time distinguished between writing software and running a money-transmission operation.

But the protection still has huge problems. During the committee vote, a last-minute amendment changed the wording regarding when a developer can still be subject to regulation. It now says that if you’re acting pursuant to an agreement, arrangement, or understanding to control a protocol, the safe harbour doesn’t cover you.

That means, on protocols like Aave or Compound, token holders who regularly vote on upgrades and treasury decisions could now easily be read as having an “arrangement,” and that alone would be enough to strip the protection from everyone building on those protocols.

The safe harbour covers the back end, smart contracts, validators, and node operators. But it says nothing about front-end interfaces. And almost nobody interacts with DeFi through raw smart contracts. They use websites like app.uniswap.org or app.aave.com. If a regulator decides that running one of those front ends constitutes operating a financial service, then the safe harbour protects the code but not the product that anyone actually uses. And this could now become the next big regulatory battle in DeFi.

Jake Chervinsky, who runs the Hyperliquid Policy Centre, said: “If the bill doesn’t work for DeFi, it doesn’t work at all.” And it’s true because if that language stays as written, the safe harbour protects developers on paper, but at the same time, exposes them in practice.

Warren also tried to pass an amendment that would give the Treasury the power to sanction DeFi protocols, just as it did with Tornado Cash back in 2022. It failed 11-13, and every Republican voted against it.

Right now, it’s unclear whether the government can legally sanction software that no one controls. That question will end up in court eventually. And when it does, the lawyers defending DeFi protocols will be able to point to this vote and say, Congress already debated this exact question, and they decided the government shouldn’t have that power. That’s a strong argument to have in your pocket, and it came out of a failed amendment.

Who Wins, and What Happens Now

The biggest winners here, though, are the banks. By effectively killing SAB 121, the CLARITY Act removes the accounting rule that forced institutions to treat customer crypto as liabilities on their own balance sheets. This was the primary wall keeping banks out of the custody game. Now, every major financial institution can hold Bitcoin and Ethereum without blowing up its capital ratios. Institutional custodians like BitGo and Anchorage can finally graduate from simple storage to building out prime brokerage and clearing services with genuine legal backing.

Tokenisation platforms are also about to see their theoretical TAM become reality. Market estimates for tokenised assets are currently wild guesses, ranging from $2 trillion to $30 trillion by 2030. Those trillions haven’t moved because there was no regulated path for trading these assets. The CLARITY Act clears that blocker, creating the legal bridge that institutional capital needs to actually cross the chasm.

But the most interesting shift lies in the interaction between this bill and the GENIUS Act. Because the stablecoin law bans passive yield on holdings, you can no longer just park USDC on an exchange and collect 5%. Yield now requires active participation – staking, governance, or providing liquidity. This means hundreds of billions in capital that once sat idle are now being directed toward structured DeFi protocols such as Pendle, Morpho, and Maple Finance. Lawmakers probably didn’t intend to create a massive forced migration of capital into DeFi, but by making passive holding unproductive, they’ve done exactly that.

The CLARITY Act is better than what came before, which was a decade of legal uncertainty in which the government regulated crypto by filing lawsuits rather than creating the rules. But it’s also a bill shaped by the companies already here, and it shows.

The compliance costs, the four-year maturity timelines, and the legal infrastructure required to use the exemptions all favour the projects that have the money and the lawyers to navigate them. If you’re Coinbase, this is the framework you’ve been asking for. If you’re building the thing that comes next, the rules were written before you got to the table.

That’s always been how regulation works, though. Whether that’s what crypto was meant to become, we still can’t say.

That’s all for today!

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.

I suggest you look into Canton network if you haven’t already I go into detail