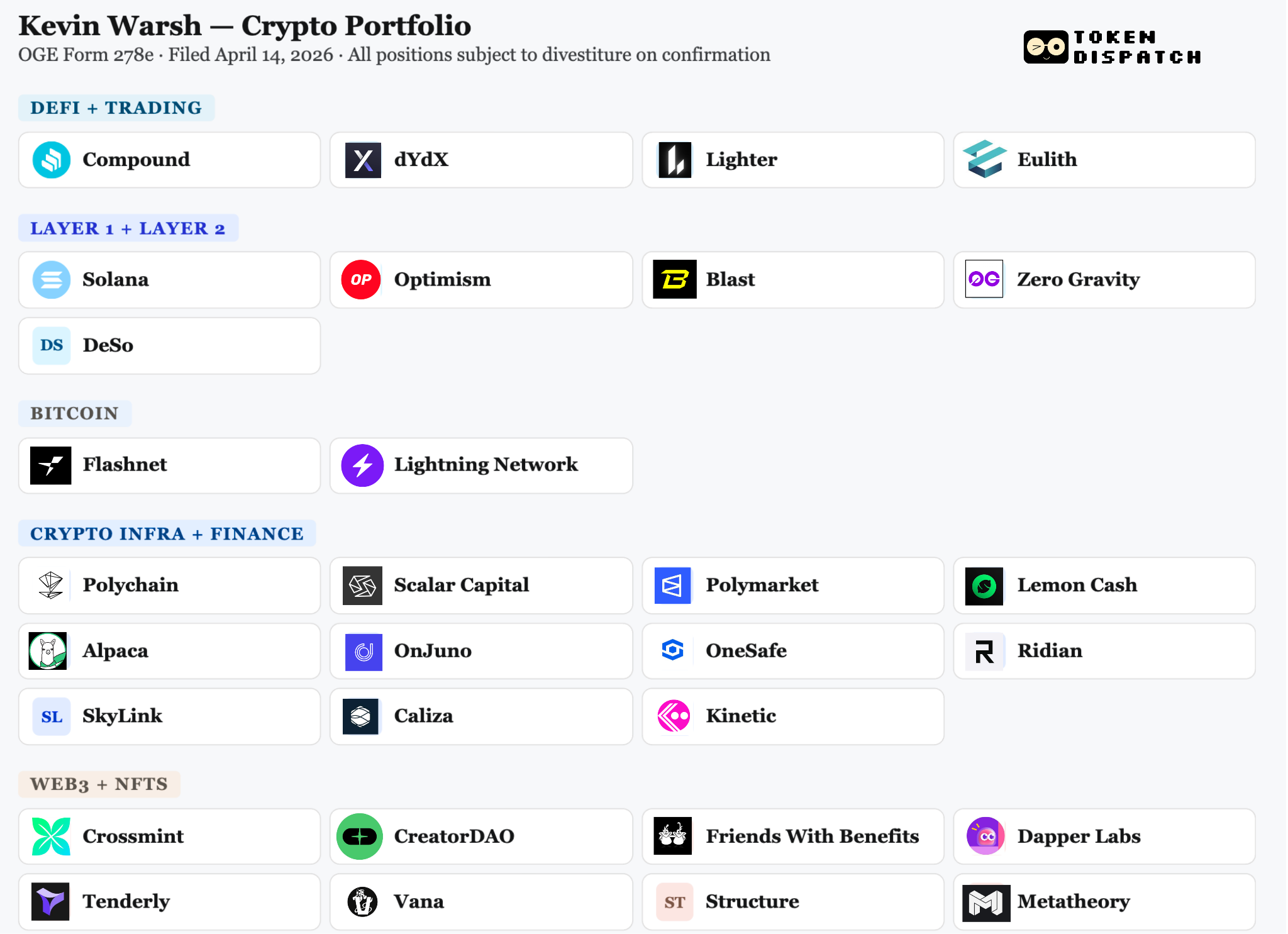

Before Kevin Warsh can run the Federal Reserve, he has to sell his stakes in Solana, dYdX, Optimism, Polymarket, Dapper Labs, and about twenty other companies. It’s a strange prerequisite for a job, but it is the law, and it applies equally to anyone seeking wants to oversee the American financial system, regardless of how well they understand it.

The disclosure that triggered all this arrived on April 14. Sixty-nine pages filed with the Office of Government Ethics, clearing the last bureaucratic hurdle before his confirmation hearing. The document is a standard compliance form. It is also, if you know where to look, one of the most consequential paper trails ever laid before a Senate committee.

Warsh and his wife, Jane Lauder, whose family interests include the Estée Lauder cosmetics company and whose Forbes-estimated net worth is around $1.9 billion, hold combined assets of at least $192 million.The bulk of that sits in two Juggernaut Fund LP positions valued at over $50 million each, tied to his advisory work with Stanley Druckenmiller’s Duquesne Family Office. The underlying assets are shielded by confidentiality agreements. The OGE certifying official flagged those specifically and confirmed that, once Warsh diverts the required holdings, he will be in compliance with federal ethics law.

The portfolio spans DeFi protocols, Ethereum scaling networks, Bitcoin payment infrastructure, and prediction markets. Reads like he went through the entire crypto industry and deliberately ordered something from every section. Through AVGF I, Warsh holds indirect stakes in Solana, Optimism, and the Lightning Network. Through DCM Investments 10 LLC, the disclosure lists dYdX, Polychain Capital, Compound, Blast, Lighter, and Lemon Cash. A separate AVF fund series captures Dapper Labs, DeSo, Friends With Benefits, and Zero Gravity. He also holds a direct stake in Metatheory, a Web3 gaming company, valued between $1,000 and $15,000. Flashnet, a Bitcoin merchant payment startup, is in there. Polymarket is in there.

Most of these crypto positions sit within fund vehicles whose individual line items are reported without dollar values, which under OGE rules, means each is worth less than $1,000. These are small venture bets, not concentrated positions. The size is not really the point; the breadth is. This portfolio covers L1 blockchains, L2 scaling solutions, DeFi lending, decentralised derivatives, NFT infrastructure, Bitcoin payments, and prediction markets. The only categories missing are memecoins, gaming tokens, mining companies, and direct Bitcoin. Everything he owns is infrastructure, financial plumbing, or developer tools.

What The Money Says

What Kevin Warsh’s money thinks is that crypto is the next layer of financial infrastructure, built on protocols that handle real transactions, and that the people building those protocols are doing something that, from a certain angle, looks a lot like fintech.

The closest thing to a speculative bet in the entire disclosure is Friends With Benefits, a social token community, which, given everything else in the portfolio, reads more like someone dragged him to a dinner and he wrote a small cheque to be polite.

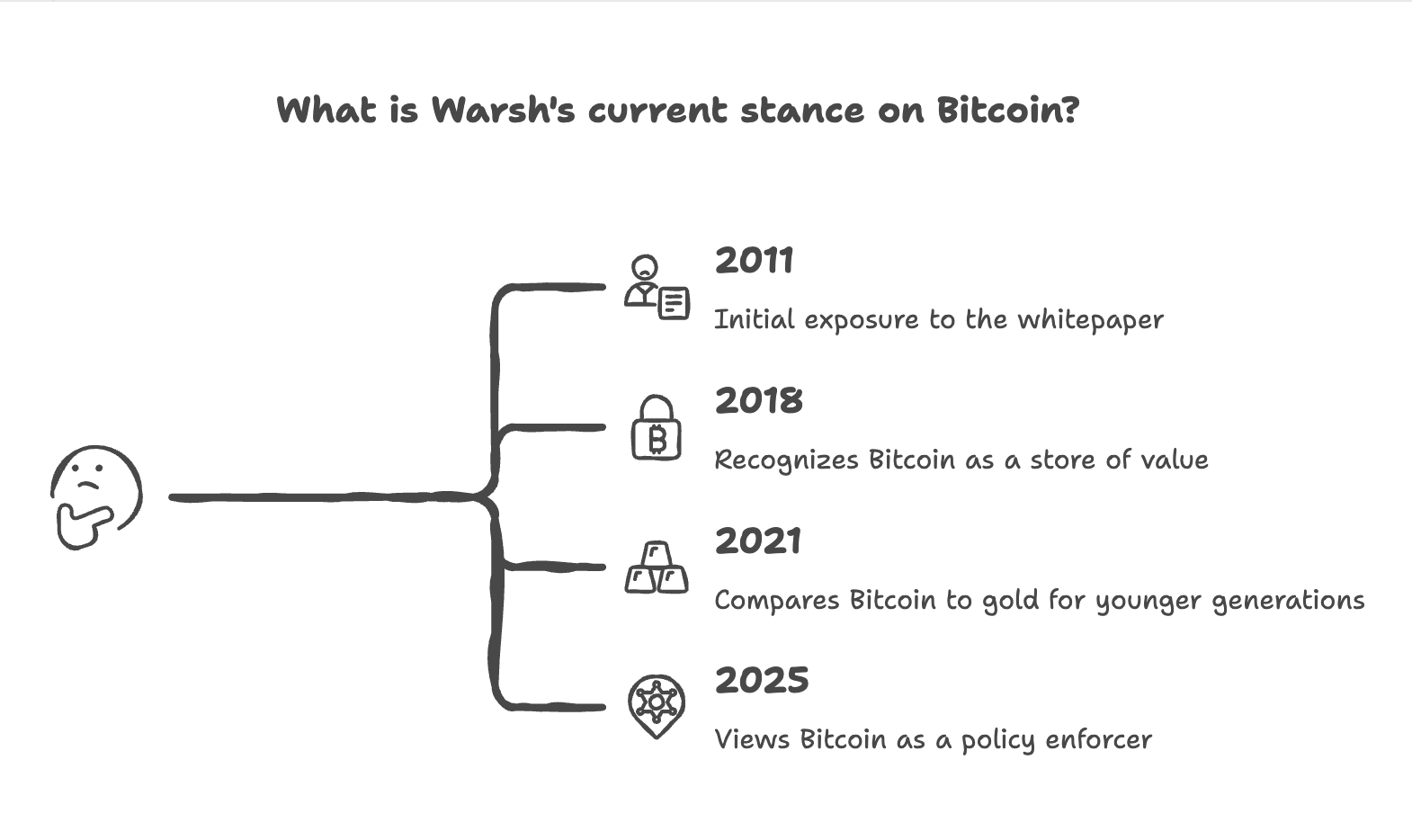

His public statements track with this. In 2011, Warsh saw the Bitcoin whitepaper at a dinner hosted by Marc Andreessen. In 2018, he wrote in The Wall Street Journal that Bitcoin could become a sustainable store of value similar to gold. In 2021, he stated on CNBC that Bitcoin is the new gold for those under 40. And in 2025, at the Hoover Institution, he provided his most comprehensive statement to date: Bitcoin is not a replacement for the dollar, but it can serve as an excellent policeman of monetary policy. I wouldn’t call Warsh a Bitcoin maximalist. A monetary policy professional who treats Bitcoin as a legitimate signal of the dollar's health may, in some ways, be more useful to the industry.

Warsh earned $10.2 million in consulting fees from Duquesne Family Office, the investment arm of Stanley Druckenmiller, one of the most credible macro investors in the world and one of the few at that level who has spoken seriously about crypto.. This is the same Druckenmiller who told Morgan Stanley last month that stablecoins will be the entire US payment system in 10 to 15 years. And then in the same interview called the rest of crypto “a solution looking for a problem.” Warsh’s crypto exposure flows through the same network as arguably the most credible macro investor alive. Druckenmiller says stablecoins are the future and everything else is noise, and Warsh’s portfolio is full of the infrastructure that makes stablecoins work, and it starts to look like a shared thesis.

Warsh has promised to divest everything. Selling liquid token positions is straightforward enough. Unwinding LP stakes in Polychain Capital or venture fund positions in illiquid early-stage companies is considerably less so. Some funds with multiple LPs would not typically require divestiture under OGE rules. But the OGE certifying official specifically flagged the Juggernaut Fund positions and made full divestiture a condition of compliance. The underlying assets in those positions remain undisclosed due to pre-existing confidentiality agreements.

Federal ethics rules generally require a one-year cooling-off period for matters directly affecting recent financial interests. That could prove relevant as the Fed weighs in on stablecoin legislation, tokenised deposits and securities, and CBDC research. Think about what that means in practice. Congress is actively debating stablecoin frameworks right now. The CLARITY Act is still working through the Senate. Banks are running pilot programs on tokenised deposits. The Fed has an ongoing role in all of it. And the person running the Fed, the person who has actually invested in DeFi protocols and Bitcoin payment infrastructure and prediction markets, may spend year one watching from the sidelines while colleagues who have never used a crypto wallet weigh in instead.

It would be strange to write about Warsh’s crypto holdings without noting the context in which he was nominated. The Trump family’s crypto ventures generated substantial proceeds before a single piece of crypto legislation was signed. World Liberty Financial, the DeFi project with Barron Trump listed as “DeFi visionary” on its website, had generated at least $1.2 billion in realised proceeds for the Trump family by early 2026, according to The Wall Street Journal. The executive order that opened 401(k) accounts to crypto was signed by a president whose family was simultaneously cashing out of crypto ventures.

Warsh’s holdings are small venture bets through fund structures. Trump’s family’s holdings are large, concentrated positions in projects that benefit directly from federal policy. These are different things in scale and structure. The connecting point is that the president who benefits financially from a crypto-friendly Fed chose a Fed chair nominee with financial interests in the crypto industry he will oversee. Whether this represents blatant corruption, strategic alignment, or simply the natural evolution of American institutions is a matter of perspective. One that usually depends on whether or not you happen to own the assets in question.

Senator Thom Tillis has said he will oppose any Fed nominee until the DOJ investigation into Powell is fully and transparently concluded. The committee sits along party lines, meaning a single Republican defection could delay confirmation. Powell’s term as Fed Chair ends May 15. If Warsh is not confirmed before then, Powell remains in a kind of caretaker role while oil is above $100, the situation in Iran is unresolved, and the market is trying to decide whether the Fed has a leader.

For the crypto crowd, the Warsh disclosure is a classic ‘good news, bad news’ joke. The good news? We finally have a Fed Chair who knows the difference between a liquidity pool and a swimming pool. The bad news? Because he knows how the sausage is made, federal ethics laws have effectively put him in a digital corner for a year, forced to watch his ‘no-coiner’ colleagues try to regulate technology they probably think is a sequel to The Matrix.

Both things can be simultaneously true. He understands DeFi from the inside. He also thinks the Fed’s primary mandate is monetary stability, and that asset price inflation is a symptom of policy failure. Those views are going to make for some very interesting FOMC meetings.

The Warsh disclosure is less a signal of institutional shift and more a quiet acknowledgement of path dependency. Our past choices and technical evolutions inevitably constrain the future. For decades, the Federal Reserve operated on legacy rails. As the architecture of money shifts from paper to protocol, the “path” is naturally widening.

This is a slow, steady integration of new literacy into an established system. A realisation that to govern the future of the dollar, one must first understand the language in which that future is being written.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.