The Lending Split

DeFi lending is breaking into two architectures, and institutions have already picked their side.

Hello,

Every lending protocol in DeFi runs on the same principles. You deposit stablecoins or ETH into a shared pool, borrowers take from that pool by posting collateral, and a DAO decides which assets are safe enough to borrow against and at what ratios. Aave grew to $50 billion in deposits based on this model. And for most of DeFi’s history, this was the only way, so its effectiveness was never really questioned.

But on April 18, 2026, a hacker exploited a bug in Kelp’s LayerZero bridge and minted $292 million worth of fake rsETH tokens. They deposited those tokens into Aave as collateral and borrowed real ETH against them. Within hours, every major Aave market hit 100% utilisation, meaning every available dollar in the protocol was already lent out. Over the next three and a half days, $15 billion in deposits were drained from the protocol. Ultimately, Aave had to organise a coordinated bailout to raise $160 million from ecosystem participants to cover the losses.

The exploit was Kelp’s fault, but the scale of the damage fell entirely on Aave’s governance. This happened because back in January, they voted to raise rsETH’s loan-to-value ratio to 93%, which squeezed the safety buffer on those positions to just 7%. That single decision led to one of the largest bank runs in DeFi lending.

On the same day, some of the illegitimately minted rsETH tokens also appeared on Morpho, the second-largest lending protocol in DeFi. And the total exposure there came to just $1 million, spread across two small, isolated markets.

I’ve been digging into this for some time now, and I think there’s a lot more to this story than just the exploit.

")

The Difference

To understand why Aave lost $15 billion and Morpho barely even felt it, we need to understand how money is deposited into each protocol.

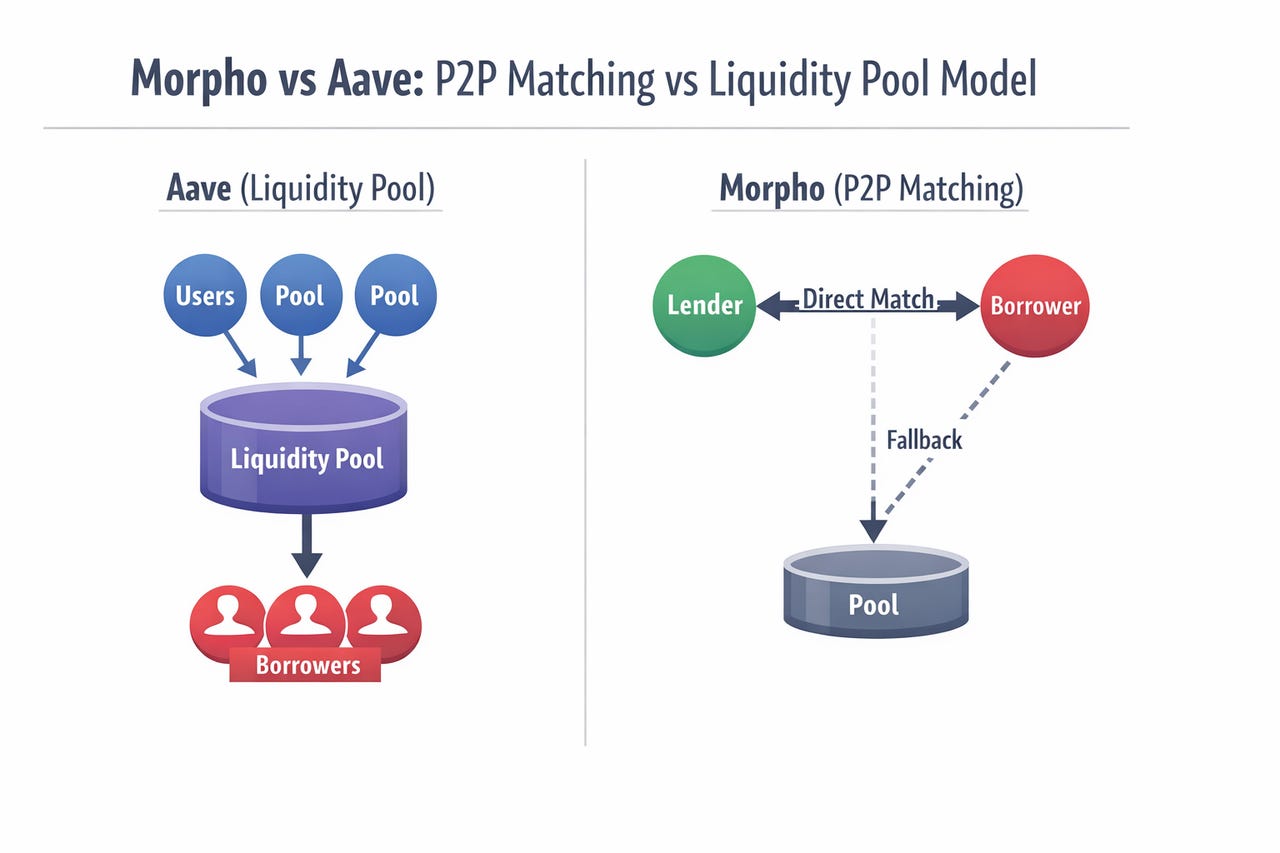

When you deposit USDC into Aave, it goes into a single pool, which then backs loans against ETH, staking tokens, and whatever else governance has approved. You don’t necessarily get to choose which collateral type your money is being lent against; that decision is made internally by the DAO through voting. So when rsETH collapsed, a lender who had deposited USDC and never even heard of rsETH woke up to find their money locked. Their capital was in the same pool, which was drained.

But the part that made me angry was that, while the markets were frozen and lenders couldn’t pull their money out, Aave’s governance lowered borrowing rates on the frozen WETH market to protect rsETH-leveraged borrowers. The depositors who put in WETH and stablecoins, who took the least risk, were earning even less in supply yield as a direct result because Aave’s supply rates are tied to what borrowers pay.

In any traditional credit environment, the safest lenders get paid first. But here Aave inverted the whole hierarchy, and likely because the borrowers running leveraged rsETH loops were also the most active governance participants. And that’s why the people who took the most risks had the most political power to protect themselves when things went south.

Aave also introduced a new insurance system, Umbrella, in late 2025 to protect against such losses. Users can stake WETH and agree to have it slashed if the protocol needs to cover bad debt. When the Kelp crisis hit, 18,922 out of 23,507 staked aWETH entered an unstaking cooldown, which was almost 80% of the insurance pool at that time, trying to move out at the same time.

And it failed, because on-chain insurance is voluntary, which means the people providing it can pull out whenever they want. And they will always want to pull out when there’s an actual crisis, because that’s the only time their capital is at real risk. So the insurance is only there when you don’t need it.

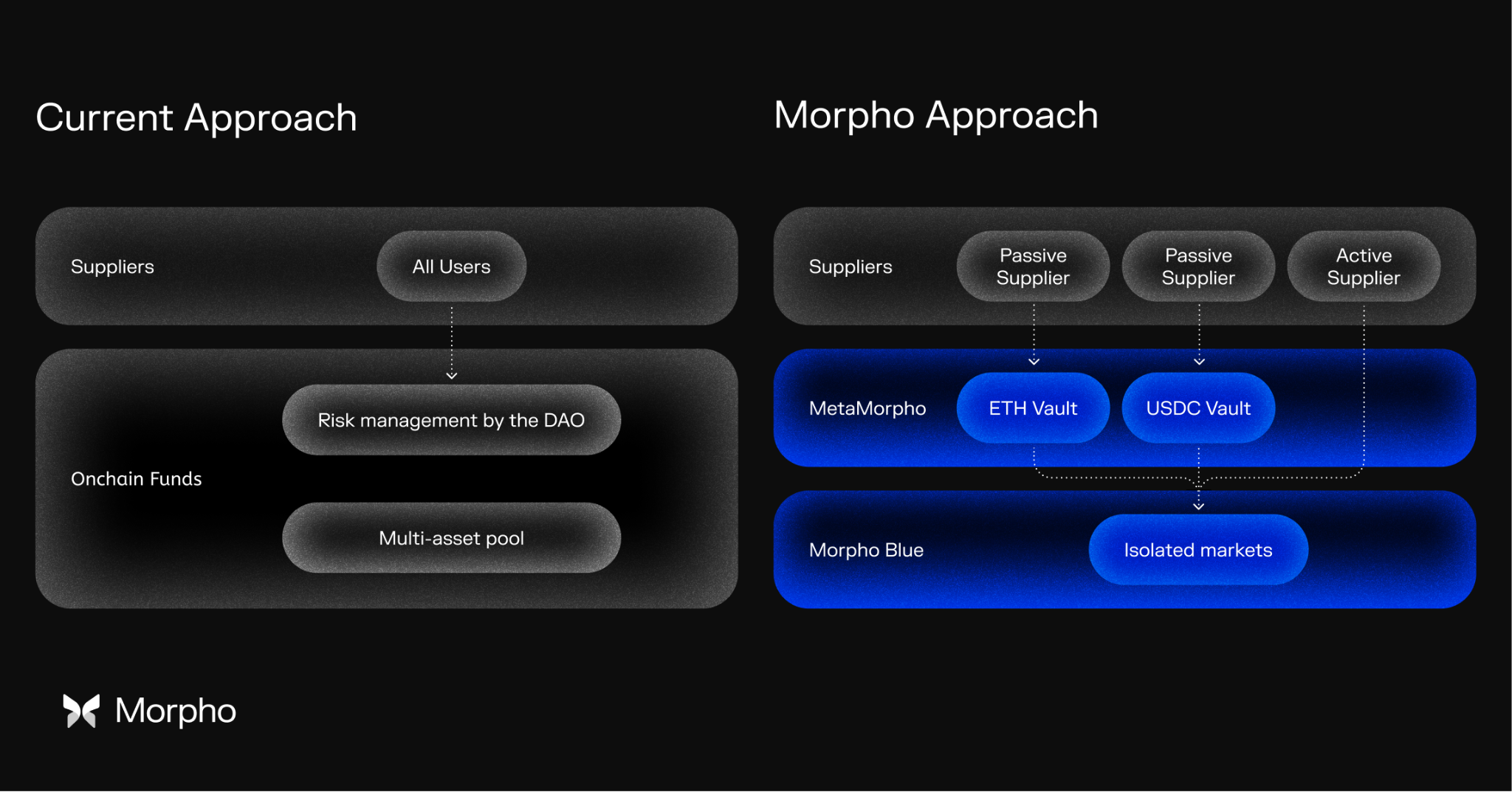

Morpho’s model works very differently. Instead of having a single shared pool, anyone can create an isolated lending market on Morpho by setting some fixed parameters: the loan asset, the collateral asset, the oracle, and the interest rate model. Once deployed, those parameters cannot be changed. If you want a different level of risk exposure, you will have to create a new market.

On top of this, Morpho also has an independent risk manager called Curator firms, like Gauntlet and Steakhouse Financial, which build vaults that allocate capital across multiple Morpho markets based on their own analysis. They charge performance fees, and if they incur a loss, the loss stays in their vault. There was also a point when Gauntlet advised Aave governance, but its recommendations could be overridden by token voters chasing higher yields. Morpho does not permit that.

The Hidden Cost

Aave and Morpho are two of the most widely adopted crypto lending models today. Aave runs on what’s called shared-pool lending, where all deposits go into one pot and risk is decided through governance voting. Morpho, on the other hand, runs an isolated market model in which each lending pair is separate, and curators manage risk independently.

The Kelp exploit revealed flaws and loopholes in the shared-pool model. But even when nothing breaks, this model has a cost that doesn’t get talked about much. Aave’s three largest Ethereum markets – WETH, USDT, and USDC currently account for about 89% of all borrows on the protocol. In those markets, supply rates consistently sit 25 to 35% below borrowing rates. That entire difference is capital sitting idle in the pool, earning nothing for depositors, while borrowers pay full rates on the other side.

Utilisation-based interest rate curves are good at pushing rates up when conditions are risky, but when borrowing demand is low, they have no way of putting idle capital to work. It just sits in the pool unproductively. And across just those three markets, that amounts to roughly $52 million a year in value that drains out of the system. That is close to a quarter of Aave’s Q1 annualised revenue, gone to pure spread inefficiency. Even if you set the reserve factor to zero and remove Aave’s fee cut entirely, the idle capital problem persists because it’s built into the way shared pools work.

Morpho’s rate model targets 90% utilisation, which is significantly higher than the 60-80% range Aave aims for. And it can afford to run that high because deposits on Morpho are never reused as collateral for other loans, which eliminates the cascading liquidation risk that forces shared pools to keep so much capital idle as a buffer. If too much capital is borrowed, rates automatically rise, so more depositors come in. If too little is borrowed, rates go down, encouraging borrowers to take out loans. The system balances itself continuously without any governance vote.

You can already see it performing better because the top USDC vaults on Morpho already pay higher yields to depositors than both Aave and Compound, even after curator fees. Morpho’s loan-to-deposit ratio is at 41% against Aave’s 39%, but it’s applied across billions in deposits and compounds for every lender on the platform daily.

What do institutions trust most?

You might be surprised to learn that Coinbase routes its entire crypto-backed lending product through Morpho. Over $2 billion in loans have been originated, with more than 100 million Coinbase users having direct access to Morpho-backed yield.

Most of them have no idea they’re using DeFi, and the reason Coinbase chose not to build its own lending engine or use any other lending platform is that Morpho’s infrastructure allows it to control the risk parameters, pick its own curators, and own the product experience end-to-end.

Apollo Global Management, which manages over a trillion dollars and has a 30-year track record in private credit, recently signed a 48-month cooperation agreement to acquire up to 90 million MORPHO tokens, about 9% of the supply. Their tokenised fund positions are being used as collateral on Morpho, with Gauntlet curating their vaults and stress-testing market strategies.

And it goes further, Anchorage Digital, the first crypto-native bank to receive a federal charter in the US, integrated Morpho Vaults for institutions holding tens of billions. Société Générale’s SG-FORGE became the first fully regulated bank to integrate DeFi lending through Morpho. These regulated financial institutions chose Morpho because the isolated market model allows them to meet their own compliance requirements without relying on a DAO for decisions.

Every one of these institutions wanted a lending infrastructure where they could set their own risk parameters with their own curators. And if you compare that with Aave’s model, they can’t achieve it there because a DAO sits in the middle of every market. But with Morpho, these partners can own the entire product.

The regulatory backdrop only makes this more urgent. The GENIUS Act bars stablecoin issuers from distributing yield directly, which means stablecoin providers will need neutral infrastructure to keep their assets productive. US officials project that stablecoin reserves held in US Treasuries will jump from $120 billion to over $1 trillion by 2028. That capital will need a lending layer that lets these allocators control the risk on their books. Right now, Morpho is most suited to offer that.

That’s all for today!

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.