Hello,

Money often becomes useful only when it reaches its destination. A salary earned abroad can’t pay for rent, school fees, utilities and groceries back home until it passes through banks, FX desks, payout partners, and local compliance checks. Until then, it is a mere value in motion and not a medium of exchange.

The same problem is now showing up on-chain. Stablecoins move money globally in code, but their usefulness is tied to where they can plug in, who is allowed to use them, and which rules govern their reserves and redemption.

This concept stood out to me when I was reviewing Dune’s ‘Beyond Dollarisation: The Rise of Local Currency Stablecoins’ report.👇🏾

In today’s quantitative analysis, I will explain the factors that influence the growth of non-dollar local-currency-pegged stablecoins.

Onto the story,

Prathik

The Regulatory Teeth

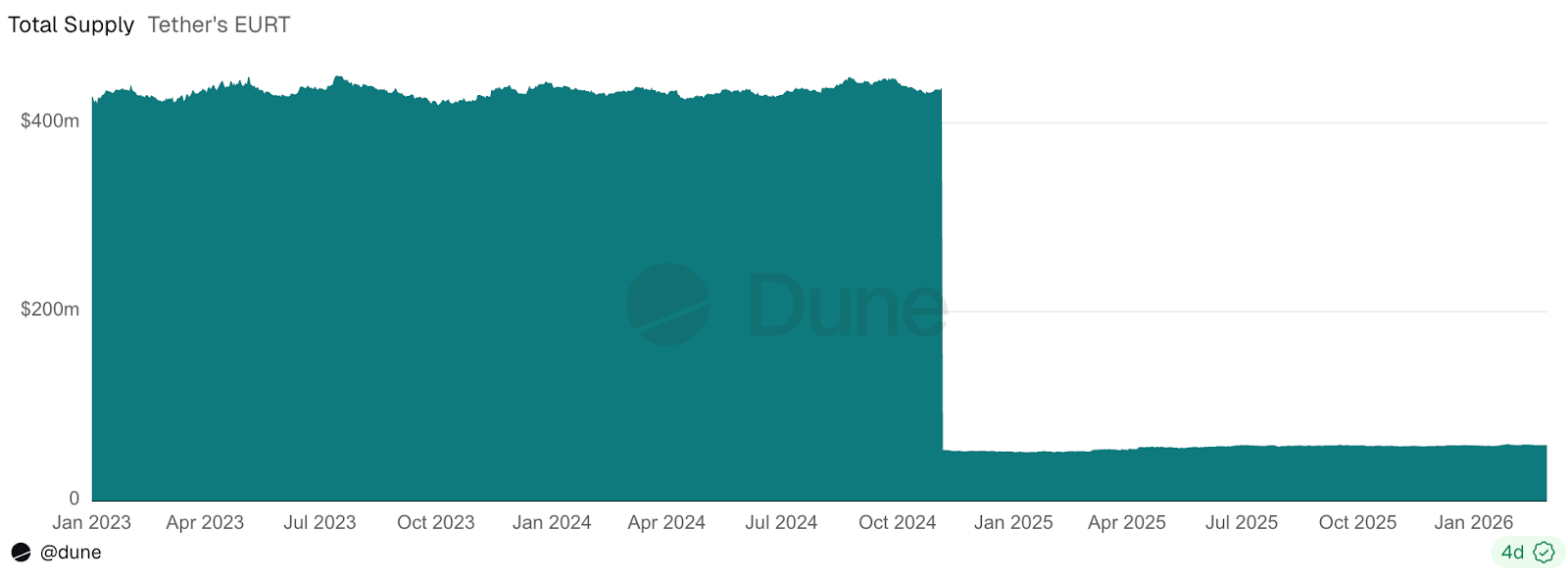

Nowhere is the role of regulations more evident than in what happened with Tether’s euro-pegged stablecoin. When Europe’s Markets in Crypto-Assets (MiCA) regulation became applicable in 2024, it almost immediately spelt a death knell for Euro Tether (EURT).

One of the earliest and once-largest non-dollar stablecoins, EURT saw its circulation fall from over $400 million to around $50 million. As a result, the total supply of local currency stablecoins in circulation fell from $1 billion to $350 million.

Crypto enthusiasts often assume that code alone is enough. They create a token, add liquidity, and expect the market to do the rest. But non-dollar stablecoins are not just abstract internet money. They are trying to become better digital versions of euro, yen, baht and other local currencies that can move on public rails without being at the mercy of banking hours. Yet they operate within a domestic financial system, with reserve requirements, licensing norms, payment networks, and redemption expectations.

The shutdown of EURT is a reminder that being early and the largest is not enough. A change in the domestic rulebook can wipe out the first-mover advantage.

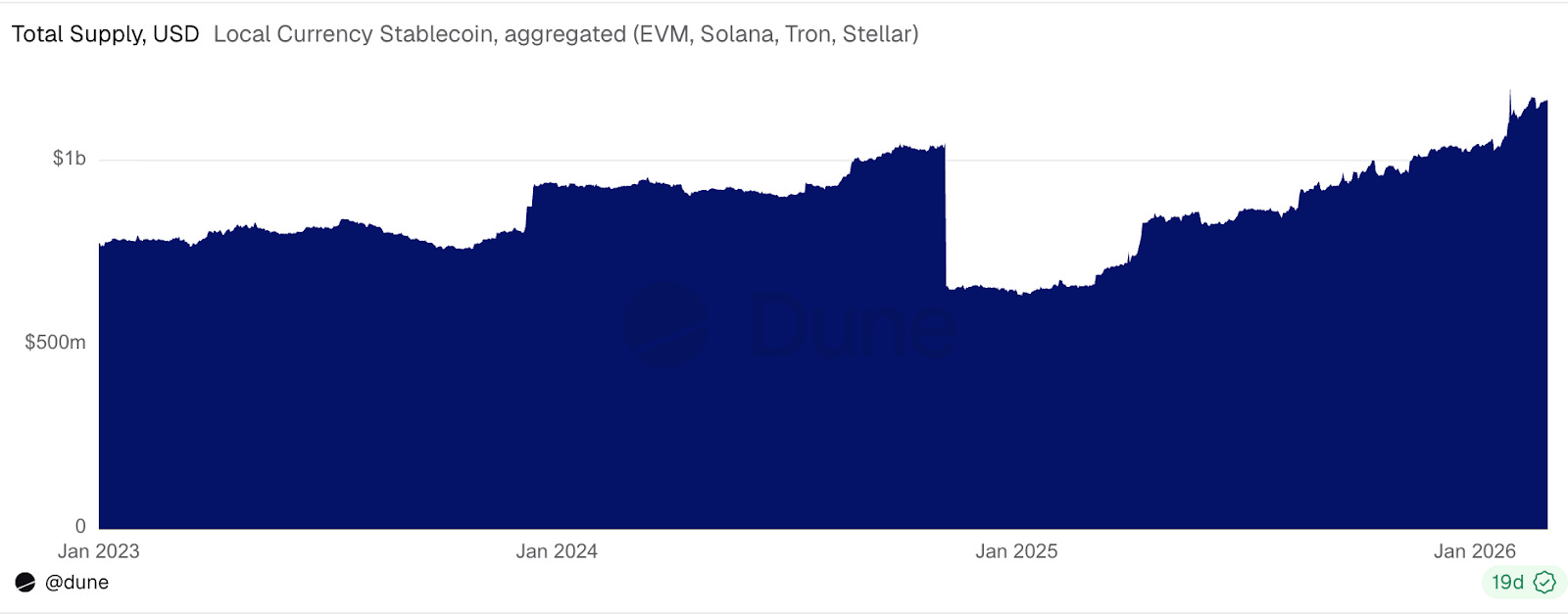

But regulation is not all bad for stablecoins. If that were the case, non-USD stablecoins might have stalled after the discontinuation of EURT.

If we exclude EURT, the total non-USD stablecoin supply nearly tripled, from ~$350 million in January 2023 to $1.1 billion by February 2026.

Widening the Market

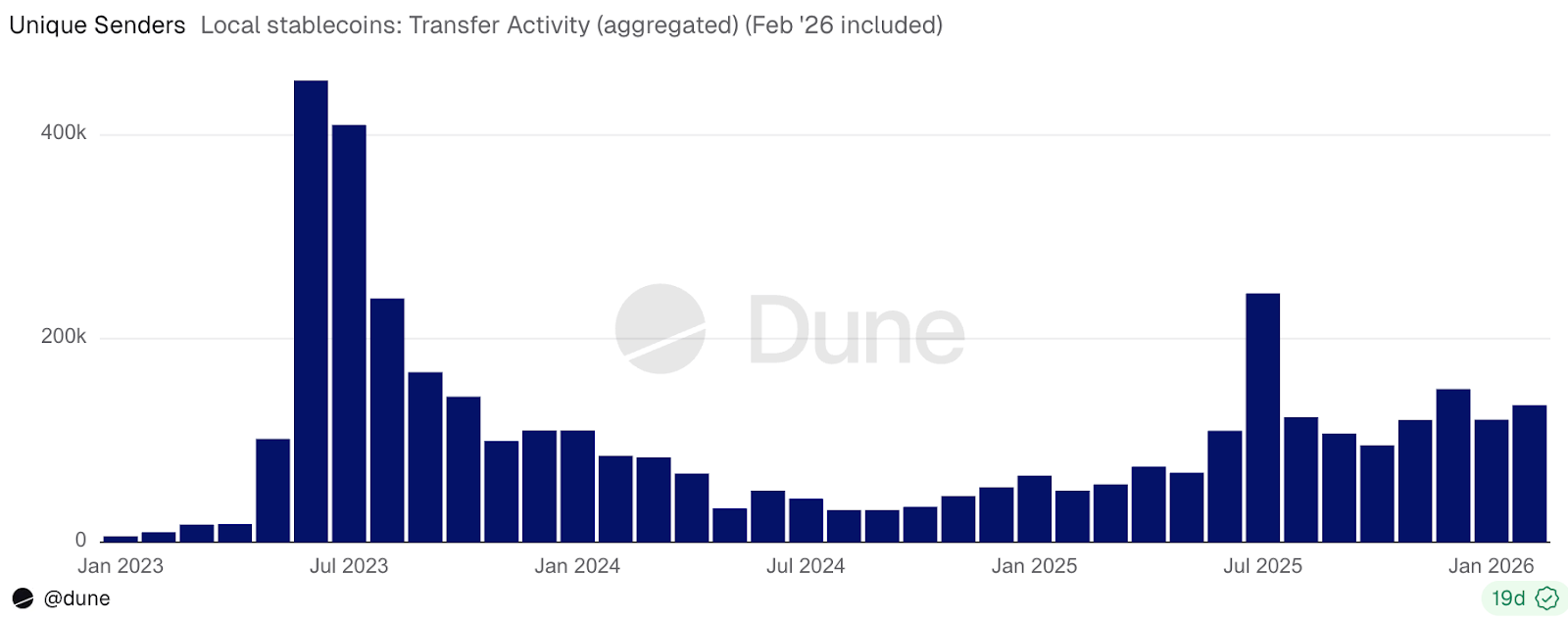

Along with circulation, the number of addresses holding such a stablecoin balance grew from approximately 42,000 to over 1.2 million during the same period.

Monthly transfer volume rose from $600 million to $10 billion, a 16-fold increase. Monthly sending addresses climbed 22 times, from around 6,000 to 135,000.

The fact that both holders and senders grew faster than the supply suggests that the market expanded through increased participation.

Therefore, regulation is not always detrimental to the market, like it was for Euro Tether. Here, it attracted more stablecoin issuers and users.

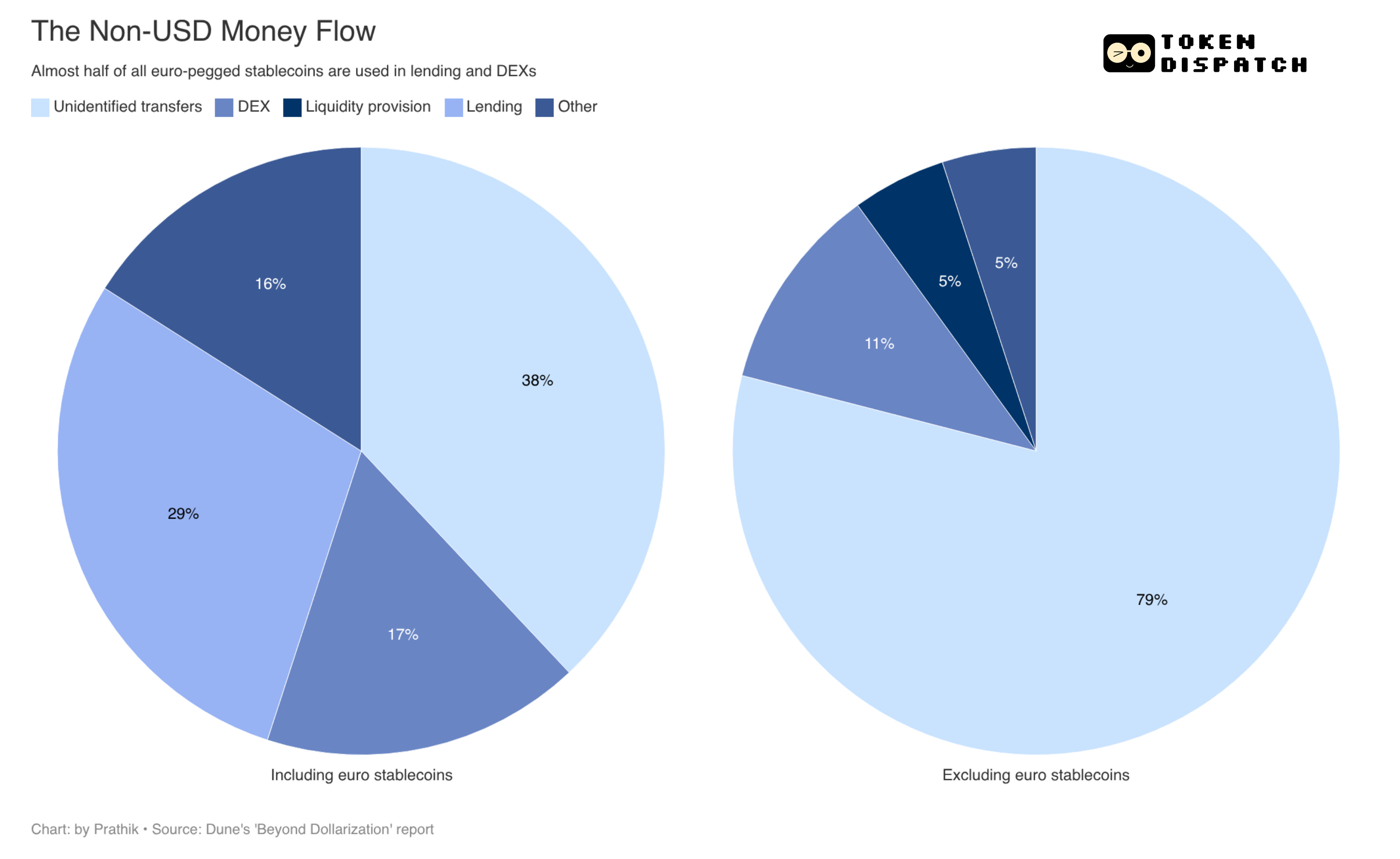

Where is Non-USD Money Flowing?

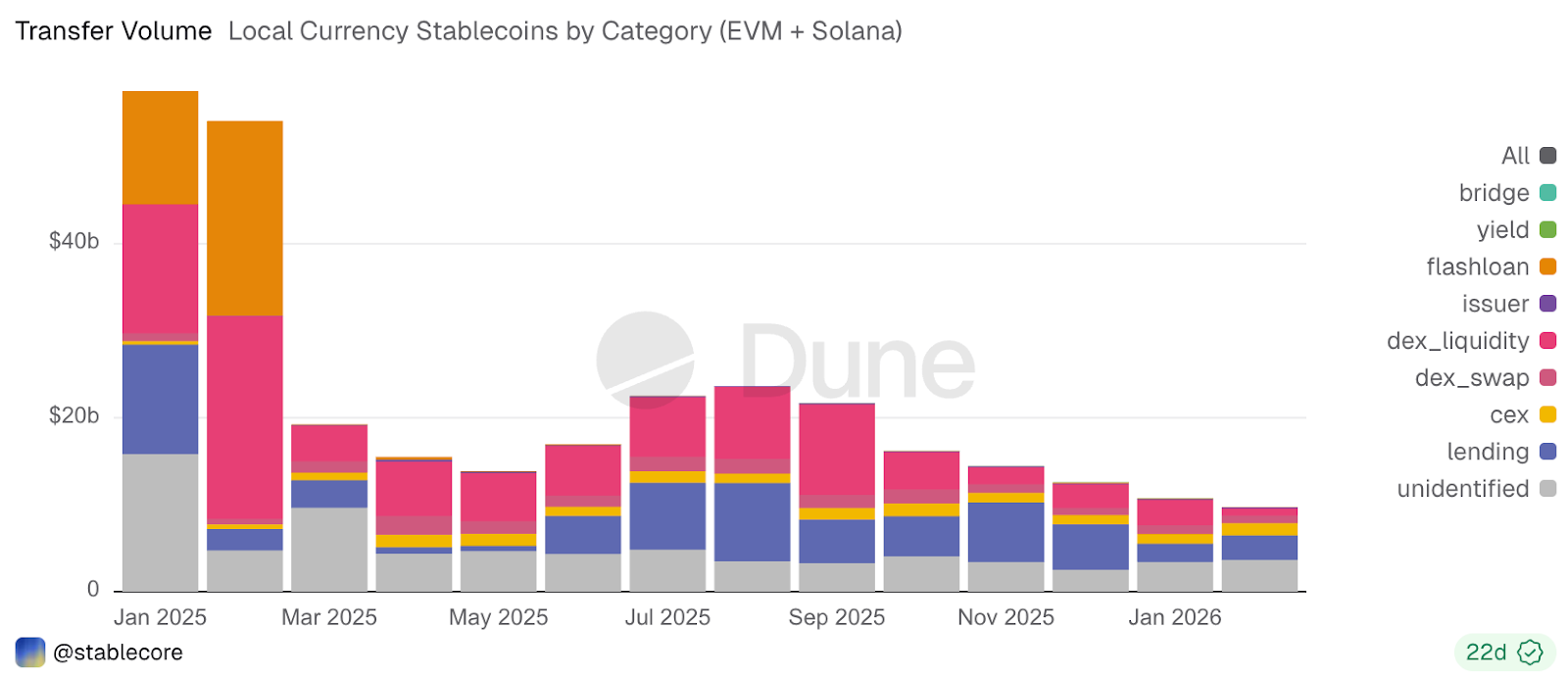

By early 2026, unidentified transfers accounted for 38% of the total transfer activity in local-currency stablecoins. This likely reflects payment and settlement activity, including peer-to-peer transfers and transfers from self-custodial wallets to payment providers.

This was followed by lending at 29%, DEX activity at 17%, and CEX-related flows at 14%.

This breakdown shows that non-USD stablecoins are being used for two main purposes on-chain. One is using them to make payments, while the other is using them as money in motion between peers or businesses. Another is using them across DeFi primitives, such as lending and trading.

But there’s a caveat in this data. When you exclude euro-pegged stablecoins from the picture, the market takes a different trajectory.

Euro stablecoins, which account for over 90% of total transfer volume, are being used like financial assets in their own right. Users are parking them in lending markets, using them in DEXs, and treating them more like on-chain cash that can earn, collateralise, and circulate across DeFi. This gives local-currency stablecoins a more mature appearance.

EURC, along with EURS, EURm, and EUROe, has found its way into DeFi yield-generating venues such as Aave, Morpho, and Fluid.

When you strip out euro stablecoins, the remaining non-USD digital money is mostly used for settlement infrastructure.

Almost 8 in 10 non-USD, non-euro stablecoins fall into the unidentified transfers bucket. It likely captures wallets moving money, businesses settling obligations, remittance-style transfers, and payment flows passing through service providers.

The dominance of euro-pegged currencies among non-USD stablecoins suggests that the next phase of growth is more likely to be concentrated in DeFi primitives. Outside of the euro, the non-USD stablecoins will first scale as infrastructure to move domestic money across digital rails before they can be used in DeFi primitives.

This growth remains crucial, as it will come from stablecoins used for payroll, treasury management, merchant settlement, remittances, and foreign exchange (FX).

All of these sectors are more regulated than DeFi primitives, since operational money cannot tolerate ambiguity as well as a speculative asset can. If a token is expected to operate within domestic payment systems, treasury workflows, and compliance-heavy environments, it will demand predictable reserves, clear redemption processes, and legal clarity. Thus, regulation will play a crucial role in the adoption of non-USD stablecoins.

This also explains why growth is showing up in areas with mature financial systems. The report pointed out that activity in Brazilian Real (BRL) and Japanese Yen (JPY) accelerated following improvements to local frameworks. At the same time, the report noted that markets without dedicated regimes, such as Indonesia, lagged.

I also find an economic case for non-USD stablecoins.

Cross-border payments still carry high conversion costs, and remittances lose a significant chunk to FX spreads and intermediaries. More local-currency stablecoins can reduce the value that needs to be detoured through dollars before it reaches its destinations. That can reduce FX costs, remove settlement friction, and let businesses and individuals hold value in the currency they earn, spend and save in.

The potential is much larger than DeFi alone. Euro stablecoins have set a strong precedent for integrating local digital money into financial systems. However, reducing the cost, speed, and dollar dependency in cross-border money movement will be a bigger win on a global scale.

The issuers who can make local currencies easier to send, settle, and embed into existing payments infrastructure will be the ones to benefit from the enormous potential of non-USD stablecoins. If they can build conducive conditions for better adoption, DeFi integration will follow naturally.

That’s it for this week. I will be back with another one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.