“Forecasts usually tell us more about the forecaster than of the future.”

— Warren Buffett

Hello,

Money filters out cheap talk. Advocates believe this is why prediction markets are reliable. We saw people accurately predict the 2024 U.S. Presidential Election results on Polymarket and Kalshi. However, prediction markets aren’t new, nor is their success in accurately predicting political outcomes.

In October 1988, a group of economists at the University of Iowa backed their academic curiosity with a small-scale, real-money prediction market. They launched a futures market on the presidential election where participants could buy contracts that paid $1 if George H.W. Bush won and $0 if Michael Dukakis did. On election eve, Bush contracts were trading at 53 cents, while the conventional polls called the race tight. Bush ultimately won with 53.4% of the vote and a healthy 8-point margin.

Since that academic experience, such real-money futures markets have outperformed the conventional polls in every election in which forecasting was done more than 100 days in advance. In 74% of U.S. presidential elections since 1988, prediction markets have come closer to the eventual outcome than the polls.

This success stems from the mechanism that forces the expression of genuine belief backed by real money at stake, something the surveys could never do. The person who actually believed Bush would win bought the contract and held it. There was little incentive for random participants to spoil the prediction by placing $50 behind a claim they didn’t believe in. When this behaviour is aggregated across thousands of traders, the information converges on a price that reflects the genuine conviction of a larger population, rather than a small, disproportionate sample.

Iowa’s small academic experiment, run on a shoestring budget, has evolved into an institutional infrastructure today.

Last week, a working paper by Fed-affiliated economists said Kalshi, the largest regulated prediction market in the U.S., could serve as a valuable real-time benchmark for policymakers. The same week, NYSE president Lynn Martin said Polymarket, the world’s largest prediction market by volume, moved S&P futures on election night by pricing a Donald Trump victory before any news organisation called the race. Later, Kalshi announced a partnership with a trading platform handling $2.6 trillion in daily institutional volume.

In today’s deep dive, I will examine whether prediction markets can serve as a reliable barometer for policymaking and what risks they pose.

Prediction Markets as Policymaking Tools

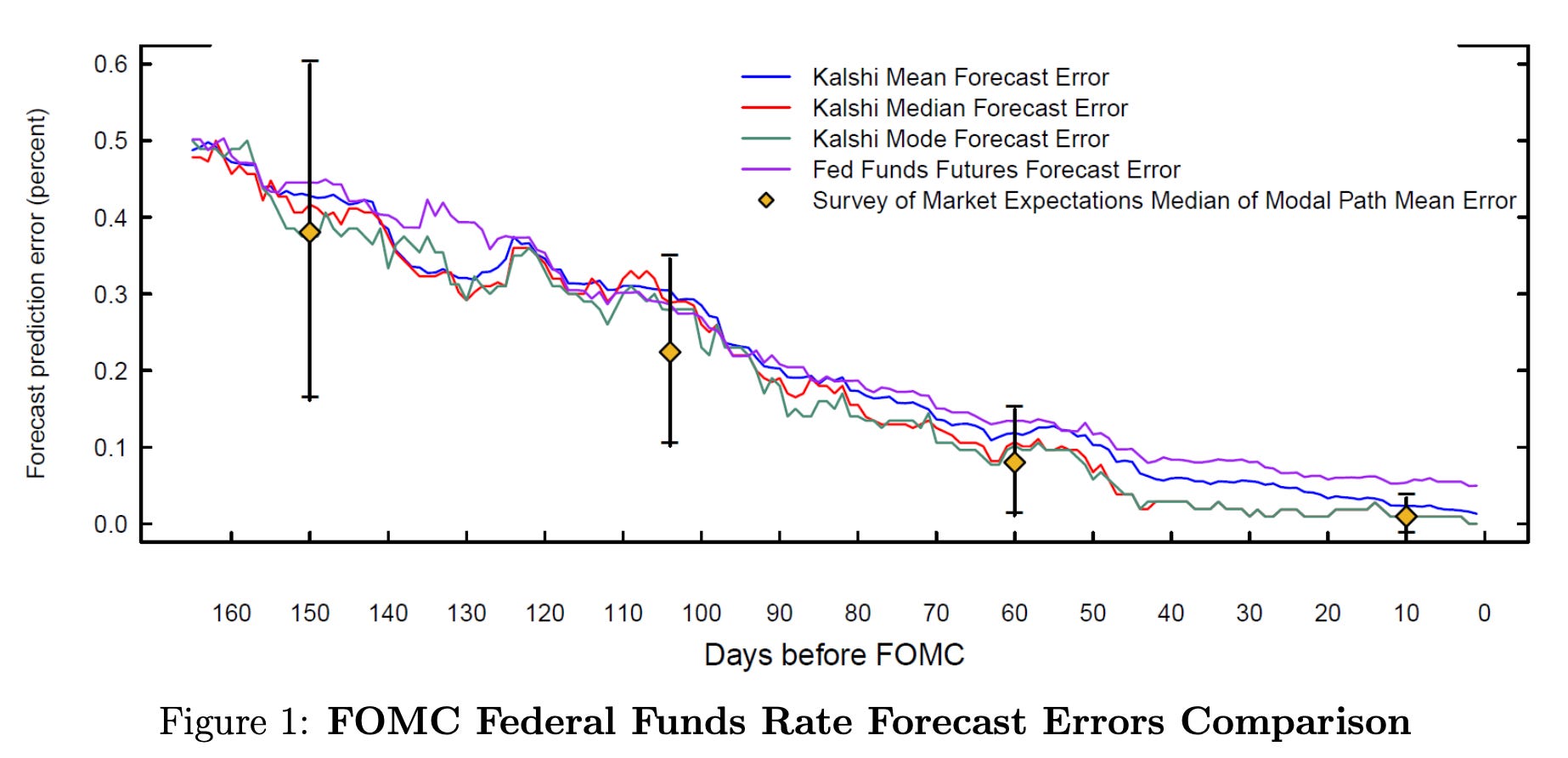

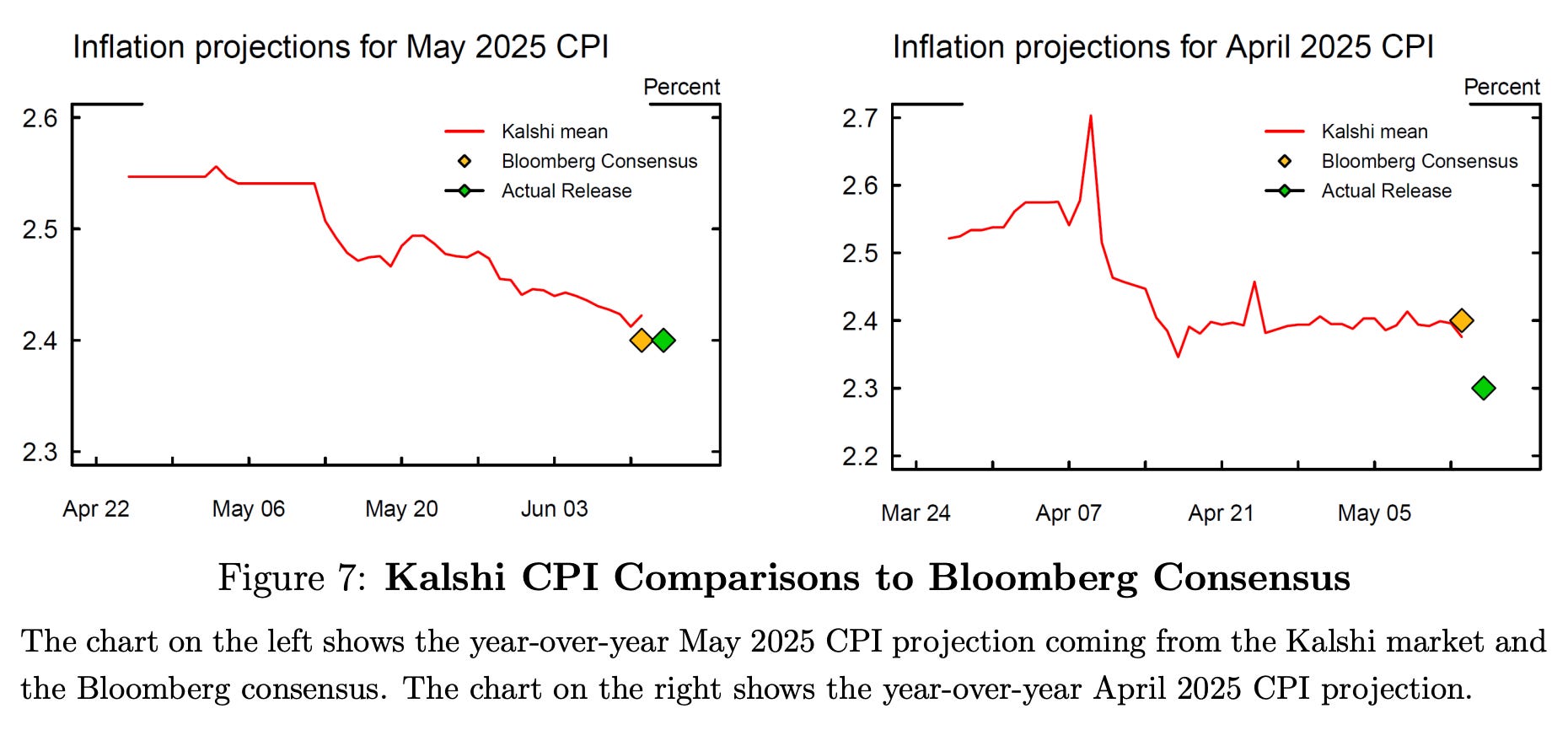

The working paper found that Kalshi’s predictions were statistically similar to Bloomberg’s consensus, with almost identical forecast errors for core CPI and unemployment.

In fact, the paper also finds that Kalshi’s forecasts for the core CPI are significantly superior to Bloomberg’s estimates.

Despite similar statistical performance, what sets Kalshi apart is its ability to provide more frequent, real-time updates to probability curves for macroeconomic indicators such as GDP growth, core CPI, and unemployment. For estimates like inflation, the Bloomberg consensus is available only in the months leading up to a release. That makes conventional estimates less frequent, with wider gaps that don’t reflect real-time updates to expectations.

Kalshi not only provides predictions for an outcome but also the real-time range of uncertainty and tail risks. In early April 2025, uncertainty about trade policy temporarily heightened inflationary expectations. Although the uncertainty did not materialise, Kalshi priced the changing dynamics in real time. The monthly Bloomberg estimates will never capture this nuance.

Today, Kalshi’s market odds move in real-time when a Fed governor speaks at an FOMC meeting. They price in every remark by the governor and offer policymakers a glimpse of how traders interpreted the intended message.

For instance, when Christopher J. Waller made accommodative remarks ahead of the July 2025 FOMC, the probability of no rate change dropped to 75%. After the June jobs report came in stronger than expected, it snapped back above 90%. The entire expectation of traders, backed by real money, is visible to policymakers in a way that no other instrument currently does.

Who’s Trading on These Markets?

Before deciding how much to trust prediction markets, it is important to examine who is trading and what the volume represents.

Between September 2024 and January 2026, the volume on the FOMC meetings grew 11-fold from $59 million to $660 million on Polymarket. In total, Polymarket’s FOMC markets have processed $2.6 billion, more than the platform’s culture, economics, geopolitics, and science categories combined.

So, who is trading such volumes on FOMC meetings? While there’s no easy way to find out on a pseudonymous prediction platform like Polymarket, I’d like to guess. It’s difficult to look beyond macro hedge fund analysts involved in drafting the labour statistics report or money market fund managers who profit if rate cuts don’t come.

Why them? Iowa markets worked because people putting money where their mouths are outnumbered participants who were just betting on noise without reliable information. Noting the risk of over-assuming, I’d like to think that when real stakes and money of this magnitude are involved, people with reliable information will gravitate toward the market, leading to more accurate price discovery.

What to Watch Out For

None of this means that prediction markets can be the perfect measuring tools for policymakers.

The probability in prediction markets also reflects traders’ risk preferences. It is not a raw reflection of expectations of an outcome. For example, when Kalshi prices a 15% probability of an adverse CPI print, whereas conventional surveys price at 10%, the gap can be justified by two factors. First, prediction markets may be pricing in real-time information that the Bloomberg consensus misses. Second, traders might be paying a premium on prediction markets to hedge against unfavourable outcomes.

Policymakers must understand what the gap reflects before they look at the information as a signal for their policymaking.

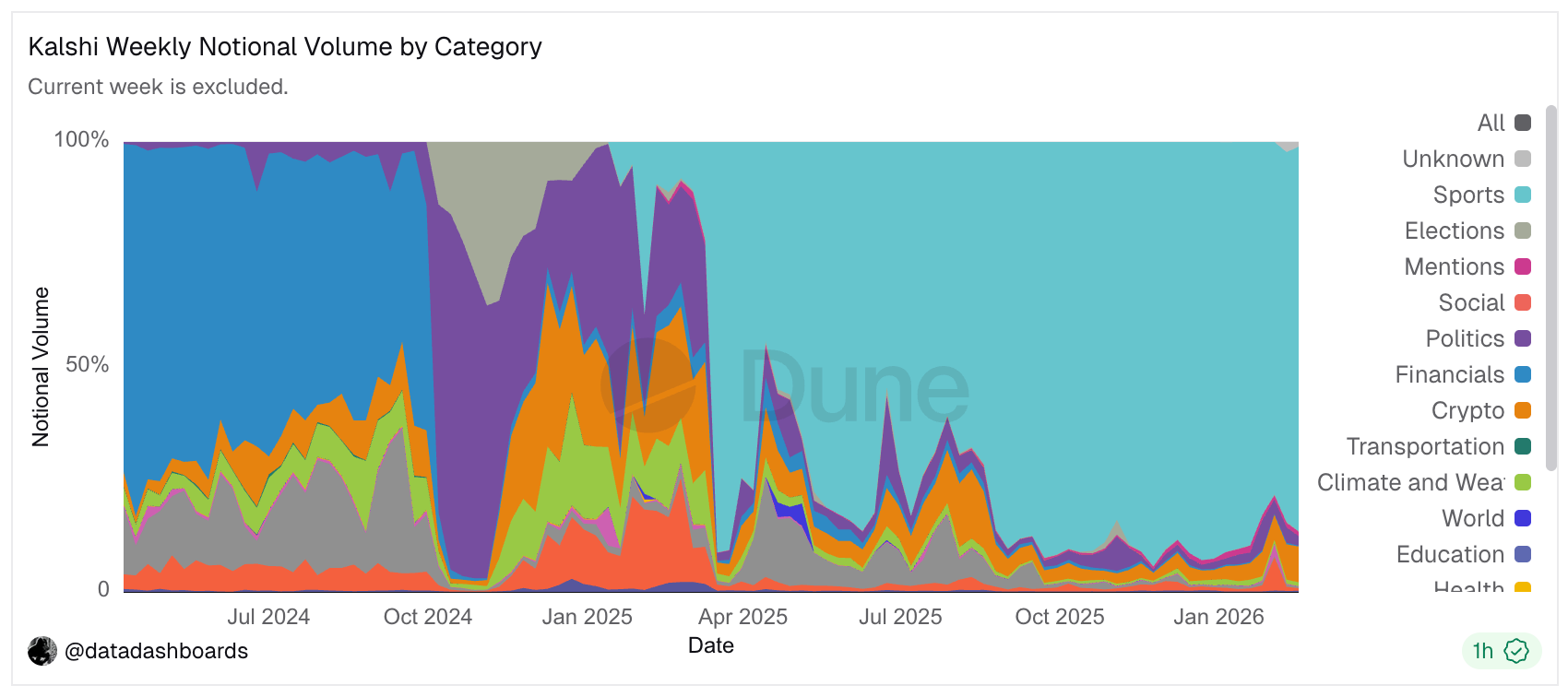

While Kalshi appears to be reliable for macroeconomic signals to policymakers, over 85% of its total notional volume is accounted for by the Sports category.

Currently, at least 20 federal lawsuits are contesting the regulatory arbitrage enabled by prediction markets through nationwide sports betting. FOMC markets on Kalshi are reliable partly because sports betting provides the platform’s baseline liquidity through active traders, tight bid-ask spreads, and market-making infrastructure that keep all Kalshi markets functioning. Macro markets benefit from this foundation even though they operate independently. If sports betting disappears under regulatory pressure, the platform loses the liquidity engine that keeps spreads tight and prices continuous across all categories, including FOMC. Thinner macro markets become easier to move with less capital, and therefore more susceptible to manipulation.

The working paper recommends using Kalshi as a monitoring tool, not a decision-making input. But making that intention public is itself the problem.

The authors suggest using Kalshi more as a tool to interpret incoming data and check the real-time interpretation of Fed communications. Yet, since the intention to refer to prediction markets is made public, it could create a feedback loop.

For example, a policymaker at the Fed could see Kalshi pricing a 15% probability of a rate cut, lower than what they expected to convey with their decisions. In response, they might soften the phrasing in their next remarks, which could then prompt conventional rate markets worldwide to move. The problem here is that while Kalshi’s FOMC market is $660 million, the Fed Funds Futures market is tens of billions of dollars. The former needs a relatively small position to swing the odds. A well-capitalised actor who understands that moving Kalshi can influence what the Fed says next, if not what it decides, can use a relatively small position to move a much larger market. Policymakers’ communication can become the target of manipulation.

This scenario highlights the difference between Iowa’s 1988 futures markets and the prediction markets of 2026. The Iowa economists were trying to determine whether a market with real stakes could produce better forecasts than a survey. At the time, policymaking wasn’t being closely watched enough to deter manipulators.

The prices reflected genuine belief because these prices did not move the world. They merely allowed those with opinions to monetise them. Once the Fed publicly announces, if and when it does, its intention to use prediction markets as policy input, that property is lost. It also introduces a performative element to trading.

Yet, it is not a miscalculated suggestion to include prediction market odds in the policy toolkit. Financial commitment still filters out cheap talk. Informed participants continue to dominate price discovery. What results is a signal that surveys can never match in terms of speed and distributional richness. And this case is stronger for FOMC markets than any other application. There are participants on both sides, enabling genuine hedging capabilities, and the markets are more reflective of real-time expectations through frequent pricing of real-time events.

Policymakers should make it mandatory to demand open-source data transparency as a condition of official adoption. If the data cannot be audited, the manipulation could go undetected. They should understand that both the signal and noise come from the same place. People with real money and genuine beliefs can tell you in real time what they think.

The window of opportunity for anyone powerful enough to game the system did not exist when Iowa economists ran their academic experiment for decades. Today, that window is wide open than ever before.

That’s it for this week’s piece. I will be back with the next one.

Until then, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.