The World Is Flat, and So Is Your Claim

Robinhood launched Stock Token, but you are buying a Jersey debt

Run a numbers game out of a barbershop, and you’re a criminal, like people were for a hundred years. But you have the state playing the same game, and now it’s the lottery.

Then how do you reliably sell something the law doesn’t let you sell? Money travels downhill to the kind word. A payday advance is a loan that can get someone sued. Not licensed to write becomes credit default swap insurance.

Last week, Vlad Tenev switched on Robinhood’s own blockchain and Stock Tokens at a keynote named “The World Is Flat.” Cute, because so is what we’re buying.

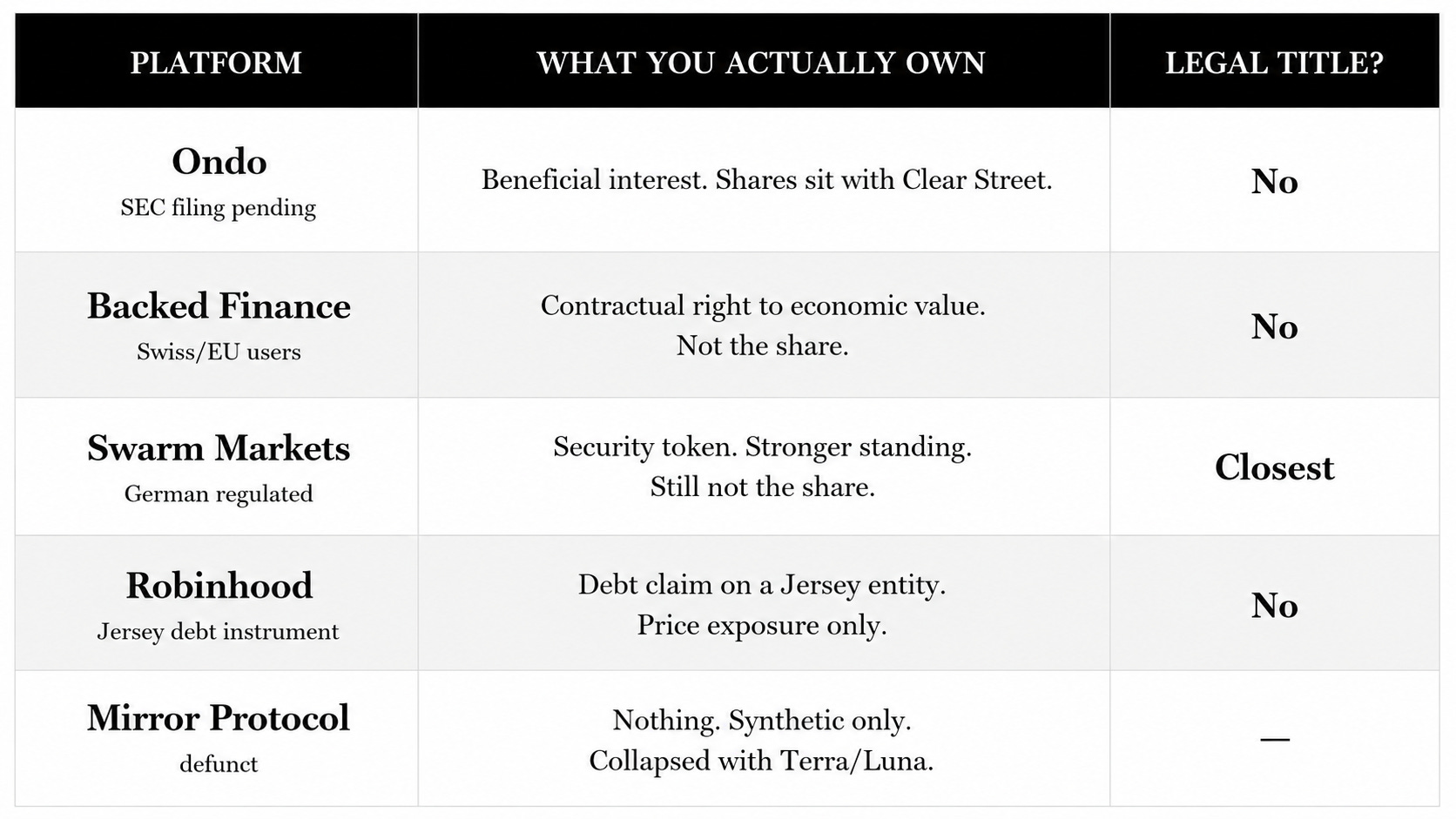

When you grab the Nvidia token, you get the price of Nvidia stock and none of the rights. If the company blows up, you have no claim on it. Well, that’s a risk that something tokenisation comes with. A work in progress, Ondo has filed an SEC filing, but as of today, unresolved.

In Robinhood’s case, what you are owning are debt securities.

The debt securities are issued by Robinhood Assets (Jersey) Limited. You lent money to a shell company on a tax island in the English Channel, and it pays you whatever the stock does.

I want to take you back to a year ago, in June 2025, in Cannes. Robinhood handed European users $5 in free “OpenAI” and “SpaceX” tokens to hype the launch. Private companies. You can’t buy their shares at any price unless they invite you. OpenAI saw the tokens with its name on them and posted a warning saying, “We did not approve any transfer. Please be careful.” Elon Musk, who cofounded OpenAI and now hates it, replied by calling the company “fake.”

Robinhood’s CEO, Vlad Tenev, then admitted that the tokens aren’t “technically equity”; they just give people “exposure.”

So why wrap a stock as debt and run it out of Jersey? Because the SEC has a map.

Equity is when you own a piece of the company.

Debt is when the company owes you money.

Robinhood stock tokens give you debt that looks like equity. You’re not a shareholder. If you buy Nvidia through this instrument, Nvidia doesn’t know you exist.

You’re buying a debt instrument from a Jersey company. That Jersey company owes you a payment based on Apple’s price movement.

If Apple goes up 20%, the Jersey company owes you 20%. Good.

If the Jersey company goes bankrupt, you’re a creditor. You join the queue of people waiting to get paid. The actual Apple shares the Jersey company holds might cover you. Might not. Depends on how messy the bankruptcy is.

If Apple itself goes bankrupt separately, you’re even further removed. You don’t hold Apple shares. You hold a promise from a company whose value was tied to Apple shares that are now worthless.

So why is Robinhood doing this at all? Start with the worst day in its history.

In January 2021, GameStop was squeezing, and Robinhood users were piling in. Then Robinhood had to turn off the buy button. The two-day settlement system behind US stock trades hit it with a collateral bill in the billions that it couldn’t post overnight, so it froze buying on the hottest stock in the country. Retail felt sold out. Congress hauled Tenev in to explain. The trust never fully came back.

This could be Tenev’s fix, five years later, by deleting the two days. A stock that settles on a blockchain clears in seconds, not T+2. No settlement lag means there will be no giant collateral call. This gives zero reason to kill the buy button again. That’s the case he’s made since January 2026, and it’s why Robinhood handed the SEC a 42-page proposal in 2025 asking for a tokenised-asset rulebook.

In January 2026, three divisions of the SEC released a joint statement on tokenised stocks. They split the mess into buckets. The real stuff is in one bucket. A company puts its own shares on a chain, and you own real equity. Another was called the ‘linked security.’ That’s a token that some third party issues to mirror a stock's price. It doesn’t carry any of the company’s obligations, and it doesn’t give you any rights as a shareholder. The SEC explained that a linked security could be dressed up as debt, for example, as a structured note. The holder assumes a risk that a typical shareholder would never take. If that outside party goes bust, that’s your problem now.

Two months later, in March, the SEC and the CFTC issued a joint release that left the January rules in place.

Robinhood built the linked security out of Jersey on purpose.

The same SEC memo described a cousin product, the “security-based swap,” which is a side bet that tracks a stock. Trouble is, you can’t sell one of those to normal people. Federal rules block offering a swap like that to anyone who isn’t an “eligible contract participant,” which means a rich or institutional investor. A debt security has no such wall. Slap the words ‘structured note’ on it, and you can hand it to a 19-year-old with ten bucks. Robinhood chose the wrapper that appeals to the largest crowd with the least hassle.

They locked Americans out.

Stock Tokens went live in more than 120 countries. Not the US. Also shut out Canada, the UK, Switzerland, and the UAE.

Europe gets a different wrap. Robinhood’s first set of tokens, now called Classic Stock Tokens, launched in Cannes in June 2025 and is subject to EU MiFID II rules. Each token is issued by a European Robinhood entity and is 1:1 backed by a real share held in custody. Since then, the catalogue has grown from 200 to over 2,000 assets, with a minimum buy-in of 1 euro. So Robinhood already runs the backed, real-share version in Europe.

This whole model relies entirely on the transparency of public markets. Because a public stock at least has a price set by the market every second. Anthropic and OpenAI don’t trade. So the token’s “value” leans on somebody’s guess about a company that publishes nothing and answers to no outsider.

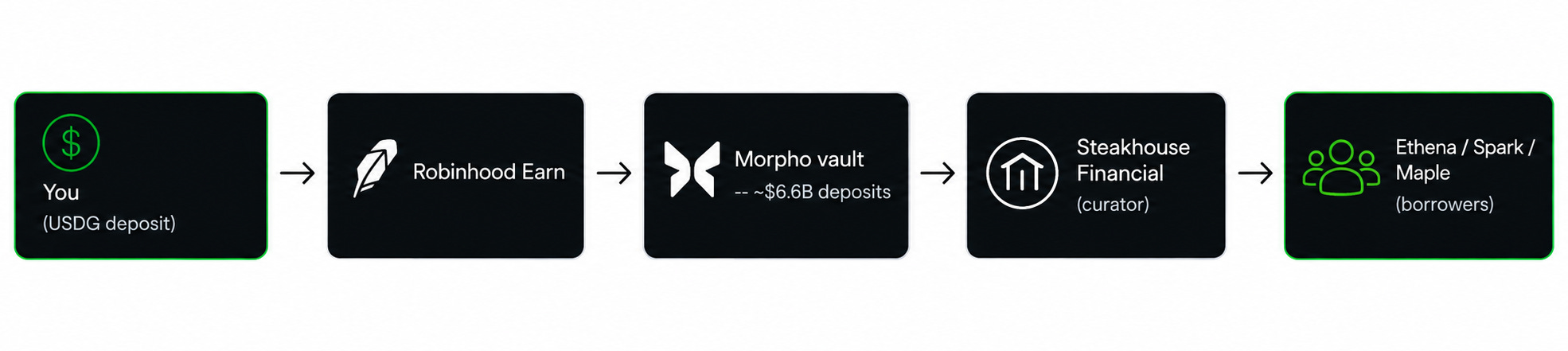

Now, the 7% yield comes from a separate product called Robinhood Earn. US-only, oddly enough. It pays you for lending out a stablecoin called USDG. Your dollars flow into a Morpho lending vault run by a shop called Steakhouse Financial, then get pushed further downstream into other protocols like Ethena and Maple. Morpho holds around $6.6 billion in deposits. The rate floats with demand. Robinhood bought insurance through Lloyd’s of London in case a smart contract gets drained.

Count the hands your money passes through there. Robinhood, then Morpho, then Steakhouse, then whoever Steakhouse lends to. The insurance covers a hack. It does nothing when the yield drops to zero. Rates move, and a lending yield drops when borrowing demand dries up, the same as any money-market rate. The thing to watch is your principal sitting four counterparties deep. The Lloyd’s cover pays out if a contract gets hacked. It does nothing if USDG loses its peg, or if borrowers default in a wave the vault can’t cover. That’s how money like this usually goes missing.

Because the tokens sit on a blockchain, you can post them as collateral and borrow against them. Handy. But a smart contract can’t look up Nvidia’s price, so it asks an oracle, a price feed, usually Chainlink. Feed the contract a bad number, and it’ll happily liquidate people or release funds it shouldn’t. Rigged oracle prices were one of the top ways DeFi got robbed in 2024 and 2025, with tens of millions lost across dozens of separate hits.

The only piece of real, voteable, own-a-slice equity anywhere in this whole setup is Robinhood’s own stock, HOOD, trading on Nasdaq the old kinda way. They kept the ownership for themselves.

Why? Every trade runs through Robinhood’s spread; the chain is Robinhood’s, and a busy new product overseas keeps HOOD’s story growing without a US regulator in the room. Ownership-free tokens are a cleaner business.

Robinhood Chain is an Arbitrum Orbit network that runs on ETH for gas and skips a token of its own, which kills the usual speculation and also means Robinhood earns nothing from issuing one. The plan is to make it the settlement rail for tokenised everything, stocks and ETFs, stablecoins and commodity perps, eventually private-company shares, all in one place, trading around the clock. If that works, Robinhood, a brokerage that routes your order to somebody else’s exchange, becomes the exchange, the clearinghouse, and all at once.

In Robinhood’s defence, the rules are changing fast. Atkins has buried the sue-first era at the SEC and is drafting an innovation exemption, a sandbox that lets firms run tokenised products under lighter rules while the permanent ones get written. The CLARITY Act has been sitting on the Senate calendar since June. Once cleared, the grey zone Robinhood is renting starts to shrink.

That’s likely the whole plan. Coinbase ran for years before it got its blessing. Kraken did the same. Build the thing in a soft spot in the law, prove people want it, then bring it home once the rulebook catches up and you can screw the protections back on.

Seen that way, the token you buy today is a rough draft of a better one.

A few days before Robinhood’s launch, on July 2, Ondo put real tokenised stocks on Ethereum through an SEC-registered transfer agent, with actual shares in custody with ownership behind them. On-chain voting for 250-plus companies. Coinbase also sells these, with dividends paid straight to you. Both are legal for Americans right now.

Going full SEC-registered in America costs more and puts a regulator in the room.

Robinhood already eats that cost in Europe, so the Jersey wrapper is a choice. It upgrades the day the law forces it, or the day a rival hands Americans the real share and walks off with the customers.

Build now, regulate later, right?

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.