What The Default Does

How $12 trillion in retirement savings is about to move toward Bitcoin without anyone deciding to.

Whatever option is set as the default - the one you get if you do nothing is the one most people end up with. They are not necessarily choosing it, because choosing requires effort, and most people, most of the time, do not expend effort on things they do not fully understand or have not been asked to think about. This is called “the default effect” in behavioural economics.

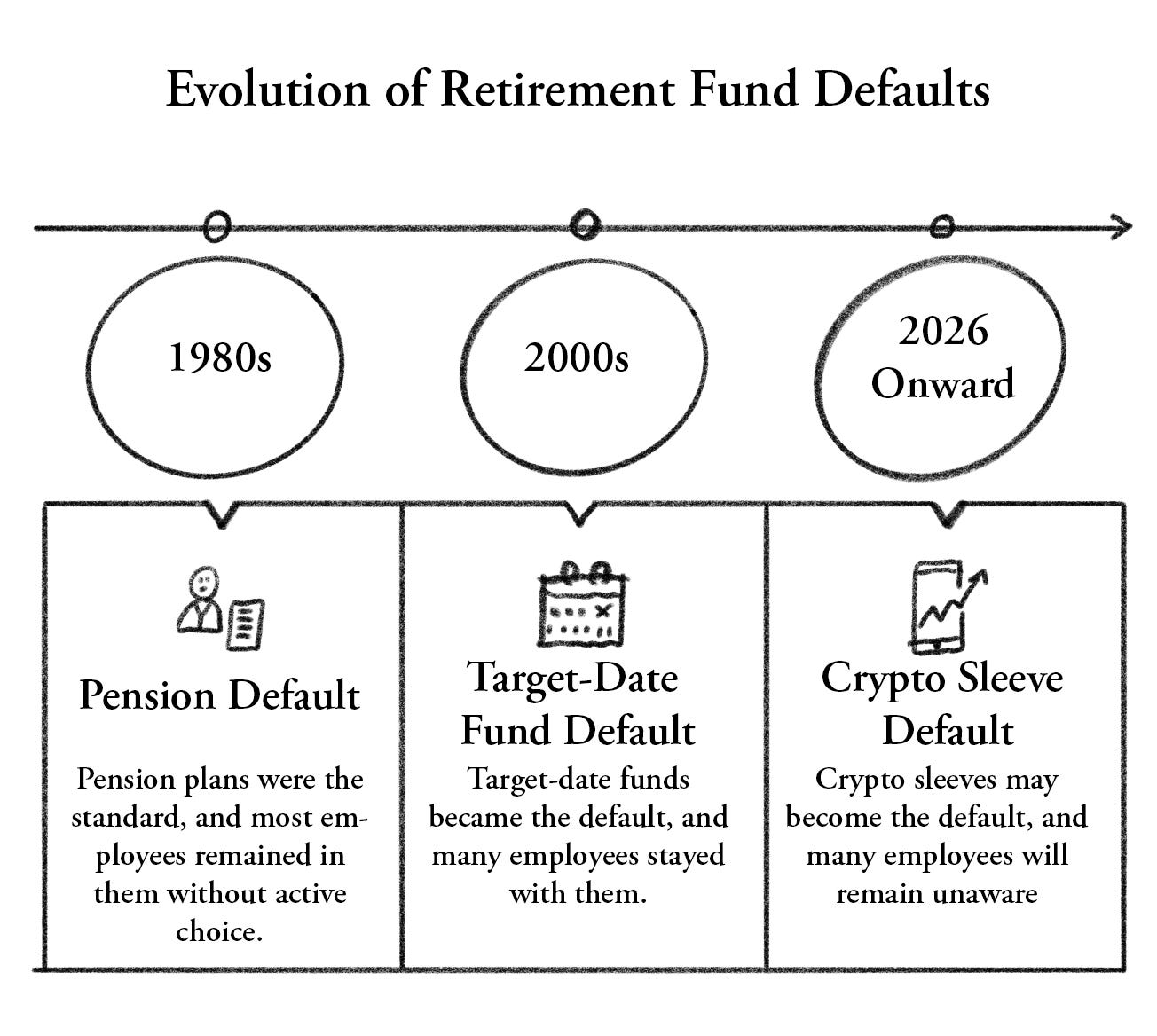

The entire history of the American retirement system is a story about defaults. In the 1980s, the default changed from pension to 401(k), and most workers went along with it without fully understanding what they had given up. In the 2000s, target-date funds became the default option in most plans, and tens of millions of people ended up in them without ever consciously selecting them. Each of these shifts moved enormous amounts of money and reshaped how an entire generation would eventually retire. Most of the people affected only found out later, when they looked at a statement.

Sometime in the next few years, a new default will be built. It does not look like a default yet. It looks like a proposed rule from the Department of Labour, sitting in a 60-day comment period, written in the language of fiduciary prudence and ERISA compliance. But defaults rarely announce themselves as defaults. They arrive as options, become common, and then become assumed.

On 30 March, the Department of Labour published a rule that could open the $12 trillion sitting in American 401(k) plans to crypto for the first time. Indiana already passed a law in March requiring state retirement plans to offer at least one crypto investment option by July 2027. Wisconsin holds $321 million in Bitcoin ETFs through its pension system. Michigan has $45 million in BTC and ETH ETFs. Florida and New Jersey are working toward similar positions.

Let’s start with the wall that kept crypto out.

Before this rule, crypto was not technically banned from 401(k) plans. The barrier was something more effective than a ban.

Under ERISA, the law governing retirement plans, fiduciaries can be held personally liable for investment decisions that lose money. Not the company or the fund, but the individual who made the call. More than 500 suits have been filed since 2016, alleging ERISA violations, with more than $1 billion in settlements since 2020. Plan administrators have watched colleagues get sued over excessive fees, over index fund selection, and over the specific share class of a mutual fund. The litigation is relentless, creative, and personal.

Think about the incentive structure that is created. You run a retirement plan, add Bitcoin, but then Bitcoin crashes by 50%. A plaintiff’s lawyer sends you a letter, and you spend three years in depositions defending your personal assets. Now, let’s say you do not add it. Bitcoin goes to $200,000. Nobody sues you for that. The rational move, every single time, was to stay away. And almost everyone did.

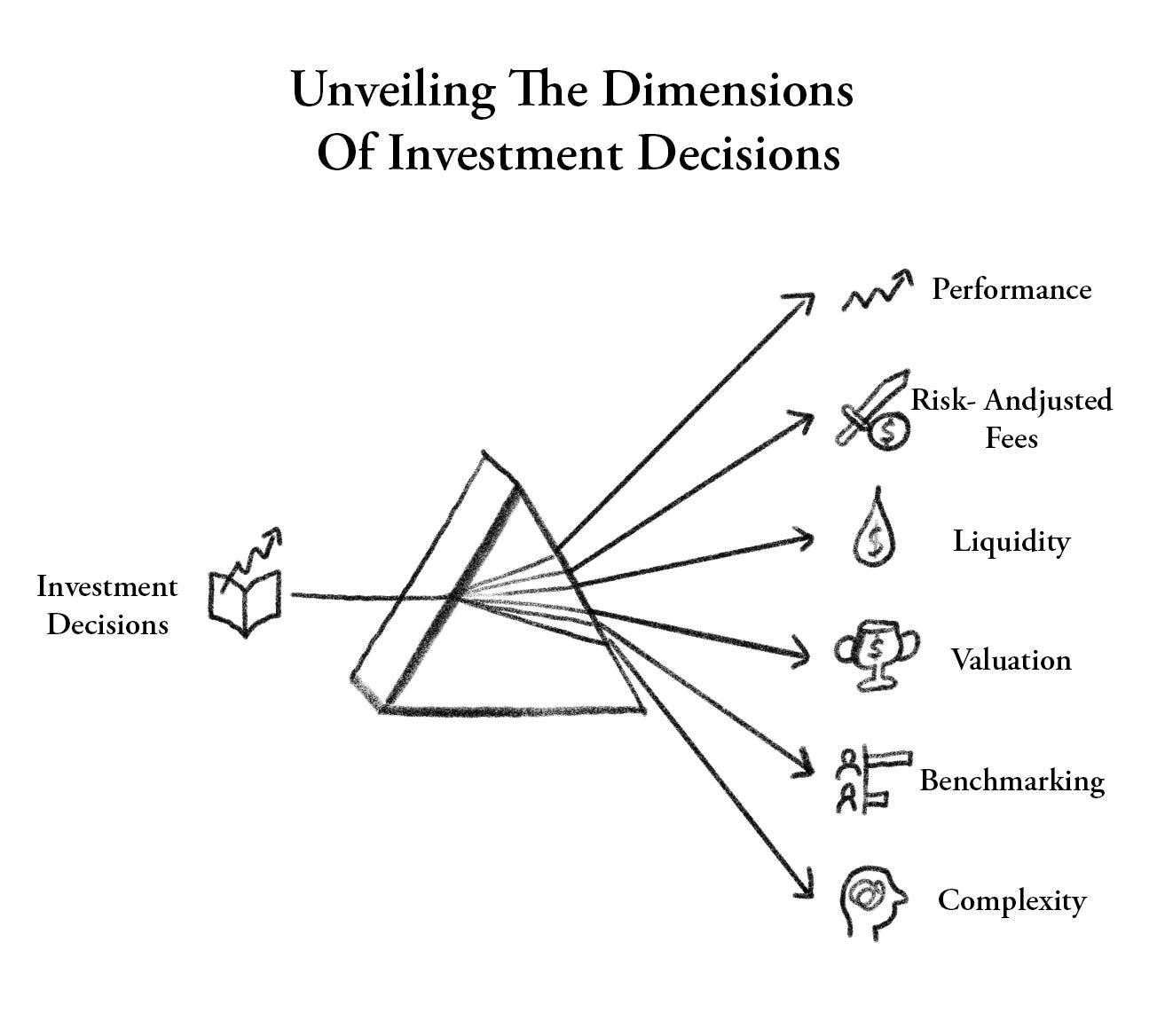

The Biden DOL made it explicit in 2022, with a formal guidance telling fiduciaries to exercise “extreme care” before touching digital assets. That guidance is now gone. In its place is a six-factor safe harbour. Fiduciaries who follow a documented review process covering performance, fees, liquidity, valuation, benchmarking, and complexity are presumed to have met their duty of prudence under ERISA. Follow the process, and you are protected against a personal lawsuit even if the asset drops in value.

Don’t mistake a change in the rules for a change in the market. The investment is just as volatile as it’s always been for the average person. This rule is really about protecting the fund managers, not the participants. It fixes the lopsided legal risk that kept crypto sidelined for a decade, making it ‘safe’ for the fiduciary to finally say yes.

The Mechanism

The DOL itself anticipates the main channel will be target-date funds. This matters enormously for what actually happens to ordinary savers.

A target-date fund is what most people pick when they start a job. You choose the fund closest to your expected retirement year, the 2045 fund, say, and it automatically adjusts its mix of stocks and bonds as you age, growing more conservative as 2045 approaches. Most people who have one have never looked at it twice.

If crypto is invested through a target-date fund, the investor never consciously buys Bitcoin. Their retirement portfolio simply acquires a 1 to 3 percent slice of it, professionally managed and automatically rebalanced. Most people who own gold in their 401(k)s do not know it is there. This is how gold got in. Through the same vehicle, and the same logic. Nobody asked the people whose money it was.

Fidelity moved first in 2022, offering plan sponsors the option to include Bitcoin before the Biden guidance pushed everyone back. Fidelity was offering plan sponsors the option to include digital asset investments in their investment menus, allowing participants to invest up to 20% of their account balances in Bitcoin. What has been missing is the legal cover for plan sponsors to use it without fear of personal liability. That cover is now being written.

The Money

U.S. 401(k) plans hold around $12 trillion in retirement savings. A 1% allocation amounts to roughly $120 billion flowing into digital assets, more than all DeFi TVL combined. Even 0.1% is $12 billion, roughly the size of a top-five Bitcoin ETF.

Every previous wave of institutional crypto adoption came from active decisions. ETF buyers chose to buy. MicroStrategy chose to hold. Banks chose to build custody products. Each of those decisions can be reversed. A CFO can sell the treasury position. An ETF investor can redeem. The 401(k) channel is structurally different in a way the industry has been waiting for since spot ETFs launched. Retirement money is passive, and it sits for 30 years. It does not panic-sell during crashes or respond to Fear and Greed readings. It does not care what oil prices did last week.

Morgan Stanley’s Amy Oldenburg noted that 80% of crypto ETF activity currently comes from self-directed investors rather than advisor-recommended allocations. The 401(k) market is almost entirely advisor-driven. The DOL rule opens a specific channel that has been structurally inaccessible because those controlling access had too much personal liability at stake to open the door. This is also the argument crypto has been making about itself for years. That the real adoption wave would not come from traders or tech early adopters. It would come when the infrastructure of ordinary savings pointed in its direction without anyone having to make a conscious choice. Target-date funds are that infrastructure.

A 50% drawdown in a trading account is a bad quarter. A 50% drawdown in a 55-year-old teacher’s retirement account is a different situation. Bitcoin has drawn down more than 80% in previous bear cycles. The current cycle has been closer to 50%, which some read as maturity. But losing half your retirement savings is not made more comfortable by calling it progress.

TD Cowen’s Jaret Seiberg wrote that he remains sceptical that the rule will encourage fiduciaries to act until courts have confirmed the safe harbour language actually protects them from litigation. ERISA is a process-based law, but courts interpret it. The Supreme Court’s removal of Chevron deference means agencies can no longer expect courts to defer to their own regulatory frameworks. The safe harbour may be real on paper. We don’t know whether it survives the first wave of litigation when a target-date fund with a crypto sleeve loses 40% in a bear market.

The comment period closes June 1. The DOL can modify the rule, withdraw it, or proceed after that date. Even if it finalises without changes, the path from proposed rule to actual crypto in actual retirement accounts runs through compliance teams, investment committees, recordkeeper integrations, and fiduciary review processes that will take months, more likely years. Indiana's July 2027 deadline is a hard mandate. The federal rule is a soft permission. The two will produce very different timelines.

Stocks were added to retirement accounts through mutual funds in the 1980s. International equities through target-date funds in the 2000s. REITs, inflation-protected securities, and commodities. None of them arrived because retirement savers demanded them. The product infrastructure and regulatory alignment happened simultaneously, and the industry moved before most people noticed.

Crypto is at that inflection point now. The spot ETFs are the product. The DOL rule is the regulatory alignment. Fidelity, Schwab, and Morgan Stanley are the distribution. The CLARITY Act, which codifies crypto asset classifications into statute, gives fiduciaries the legal footing to complete a prudence review with documented confidence. Every piece is in place except one.

Somewhere down the line, a plan administrator adds Bitcoin to a target-date fund. Bitcoin drops to 60%. A retiree loses a chunk of their savings. A lawyer files a suit.

At that point, the only thing that matters is whether a judge agrees the safe harbour protected the person who made that call. Nobody knows the answer to that yet. The DOL thinks it will. TD Cowen thinks it will take years to find out.

Until that first case gets heard and decided, every plan administrator in America is being asked to trust a piece of paper that has never been tested in court.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.

Defaults are rarely accidents.

They are features of systems stretched too far, too long.

Worth reading what breaks when nothing intervenes.

🕯️

I am a Certified Financial Planner with 46 years in the investment / insurance / retirement industry. Thejaswini's article displays crisp, well-informed writing, and is imo spot on. I know a lot of smart guys and commentators, but this is some of the best composed, well thought out prose I've seen in a while. And it makes me feel better about my 60% drawdown on my crypto accounts. Bravo!