Hello,

Do you know that a partnership called Cede & Co. in New York is the registered legal owner of around 83% of all publicly traded stocks in America? When you buy Apple shares through Schwab or Robinhood, the legal owner of those shares is still Cede & Co.

Cede is the nominee of the DTC (Depository Trust Company), and their own representation letter filed with the SEC says word-for-word that it “has no knowledge of the actual Beneficial Owners of the Securities.” So basically, Apple does not know you own their stock. Only your brokerage does, because you are their customer. But in the actual ownership chain, you don’t even exist. The word “Cede” itself comes from Latin, and it literally means “giving up power or territory.” It couldn’t be worse.

So I went down looking into how this happened, and what it actually means for you, and whether tokenisation, the thing crypto built to fix all of this, is any different?

")

The Chain, and the Crisis

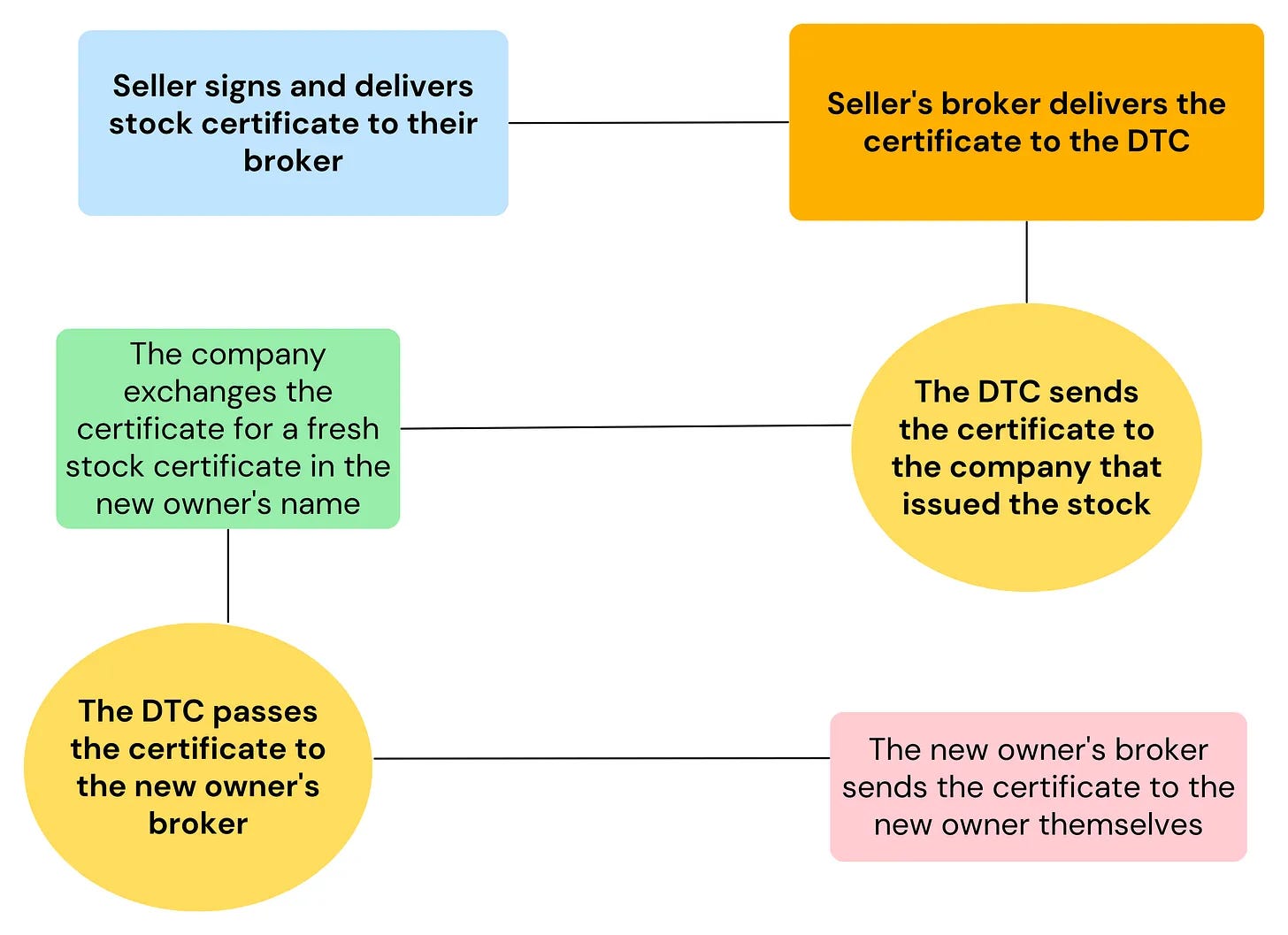

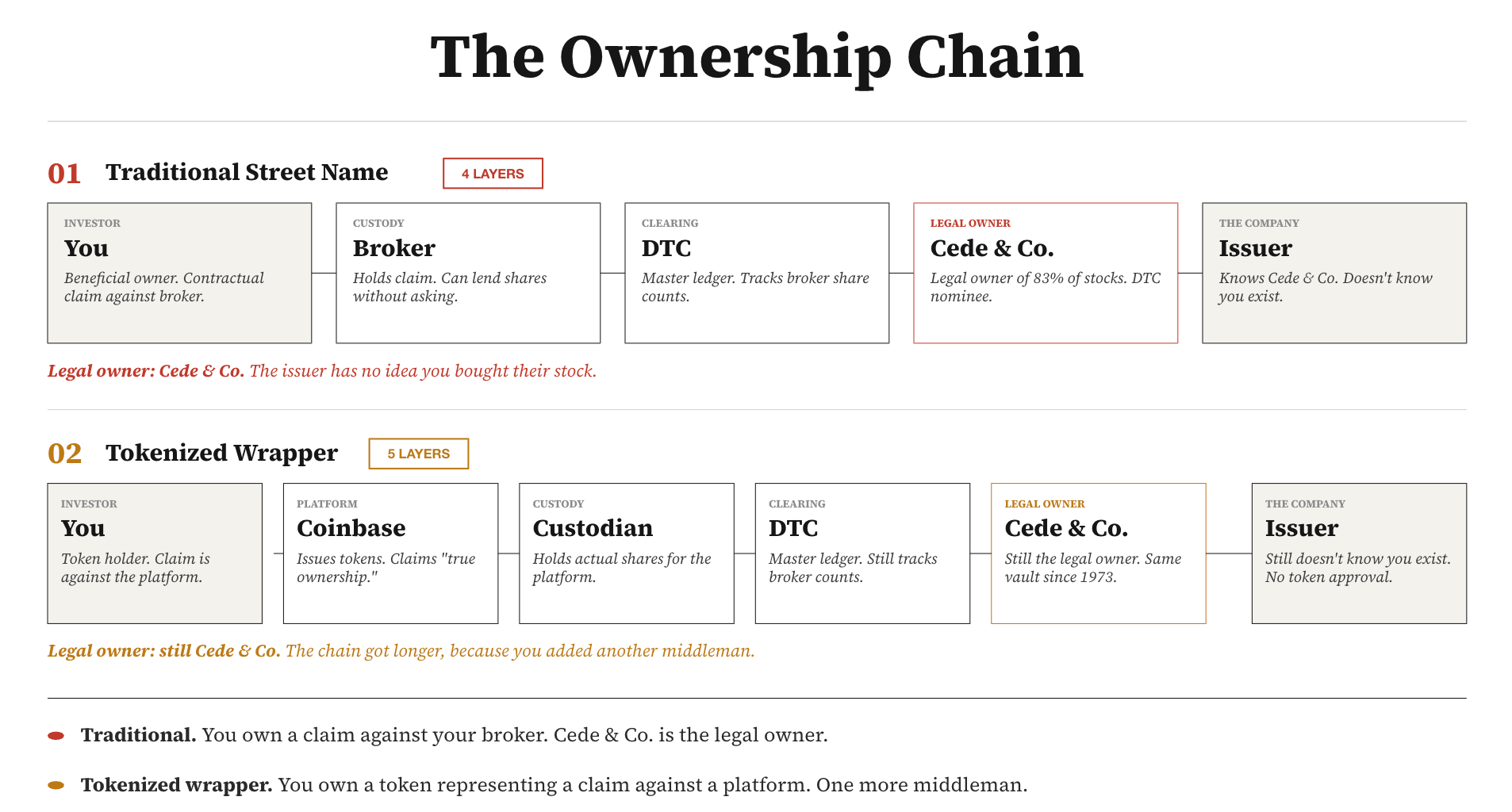

So what you actually hold when you buy a stock through a U.S broker is technically called a “Security entitlement,” which is just a polite way of saying you have a contractual claim against your broker.

What essentially happens when you buy a stock is: the DTC updates its records to show that your broker now owns the stock, and your broker updates its records to show that you own the stock. There are three layers of IOUs between you and the actual stock, and what you have is a promise from someone who might have the real thing.

Because of how this chain works, your broker also has the right to lend your shares to short sellers without your consent. Meaning, someone could be actively betting against the stock you bought, using your shares, and you would never know. This also means you don’t actually vote at shareholder meetings; your vote goes through the same chain of middlemen as your ownership. And because these securities are reused as collateral throughout the trading day, multiple institutions end up reporting ownership of the same asset simultaneously.

By some estimates, only about one in three parties actually owns a US Treasury bond. The other two are just holding claims on something that’s already been pledged to someone else. And the wild part is how we even got here.

In the late 1960s, the entire American stock market was still based on physical paper. Stock transfers used to mean moving actual certificates between firms, and a single transfer could require up to 33 different kinds of forms. Each afternoon, hundreds of couriers, many of them retired cops and firemen, used to carry suitcases and steamer trunks stuffed with stock certificates through lower Manhattan, walking them from one brokerage to another. At one point, there was a firm that Merrill Lynch later absorbed, but it had 600 employees whose entire job was handling certificates.

By 1968, the trading volume had hit 20 million shares a day, which was enormous for that time but roughly 1% of what we do now. This led to the back offices being completely broken down, and the NYSE started closing on Wednesdays and cutting hours for the rest of the week just to catch up on all the pending paperwork.

The pressure was so much that it even broke firms like Goodbody & Co., which had been on Wall Street for decades. And with that much chaos, a lot of organised crime emerged. The Attorney General told the Senate in 1971 that more than $400 million in securities was stolen in just three years. A 22-year-old stock clerk at a firm was indicted for stealing $900,000 in IBM certificates.

At one point, the Congress threatened to federalise the entire post-trade operation, so they decided to stop the current way of operating entirely. Instead, they created a centralised vault, locked all the certificates in it, and updated ledger entries when ownership changed, rather than physically moving anything. This was called immobilisation, and the DTC was set up in 1973 as that vault.

But there was a second option, called dematerialisation, which could have removed paper certificates entirely and given every stockholder direct electronic ownership of their shares. They went with immobilisation instead because it was faster to roll out during crises, and it was supposed to be a temporary fix. Then, in 1994, a UCC amendment made it a permanent law in all 50 states, and since then, it’s still running that way.

Phantom Shares, Old and New

This new way of tracking ownership through ledger entries rather than actual certificates introduced new kinds of errors. One where two different parties can claim ownership of the same shares. For example, when a short seller borrows a share and sells it, the buyer holds what looks like a real share in their brokerage account, but the original share still exists in the lender’s records, too.

So both show up as owned and can be lent out again. And if you do this enough times, the number of claims on a stock can exceed even the number of shares that actually exist in the market.

In 2017, when Dole Food was taken private, its shareholders filed claims for 49.1 million shares against only 36.8 million that actually existed. That’s 33% more claims than the number of shares that existed. These are called ‘phantom shares,’ and they’re not due to fraud or manipulation but to the design of the current settlement system, which runs through the same Cede & Co. structure. The DTC’s own ledger could not track all the trades that had passed through it until the company decided to go private.

Something similar happened with GameStop on a much larger scale. In early 2021, the short interest in its stock had exceeded 140% of the float, meaning more shares had been sold short than existed. The squeeze made headlines, and at the peak of the rally, brokers like Robinhood froze the buying while still allowing sells. Reddit’s GameStop community started asking how their brokers even had that kind of power, and that was when they found that their shares were not registered in their names but held by Cede & Co., and were being lent to the same short sellers they were betting against.

So they started pulling their shares out of brokerages entirely and transferring them to Gamestop’s own transfer agent, to put their names directly on companies’ books. By 2023, around 76 million shares had been registered directly, roughly a quarter of the entire company.

Coinbase recently launched tokenised stocks, claiming “true equity ownership” with full shareholder rights and dividend payouts. But if you look at the mechanics, a token backed one-to-one by shares held at a third-party custodian is still a claim against the custodian. The only thing that changed is the database it runs on, from a ledger at DTC to a ledger on the blockchain, but the number of intermediaries between you and the actual shares is still the same. If anything, you added one.

In the traditional system, the issuer’s register lists Cede & Co. as the legal shareholder. And Cede holds on behalf of the DTC. The DTC records which broker owns how many shares. And the broker records your name against a portion of that. There are four layers between you and the company whose stock you bought, and the company has no idea you exist.

In the tokenised wrapper model, as built by Coinbase and Robinhood, nothing changes either. A custodian still holds shares through the DTC, registered in the name of Cede & Co. The token platform issues claims against the custodian’s holdings. And you hold a token that represents a claim on the platform.

Last year, Robinhood began offering tokenised exposure to OpenAI in Europe through this model. The tokens did not represent direct ownership of the company’s shares. They represented ownership in an SPV that holds the shares on your behalf. So you own a piece of the vehicle, and OpenAI would have no idea you exist. Within hours of its launch, OpenAI publicly announced that it had nothing to do with these tokens and had never approved any transfer of its equity.

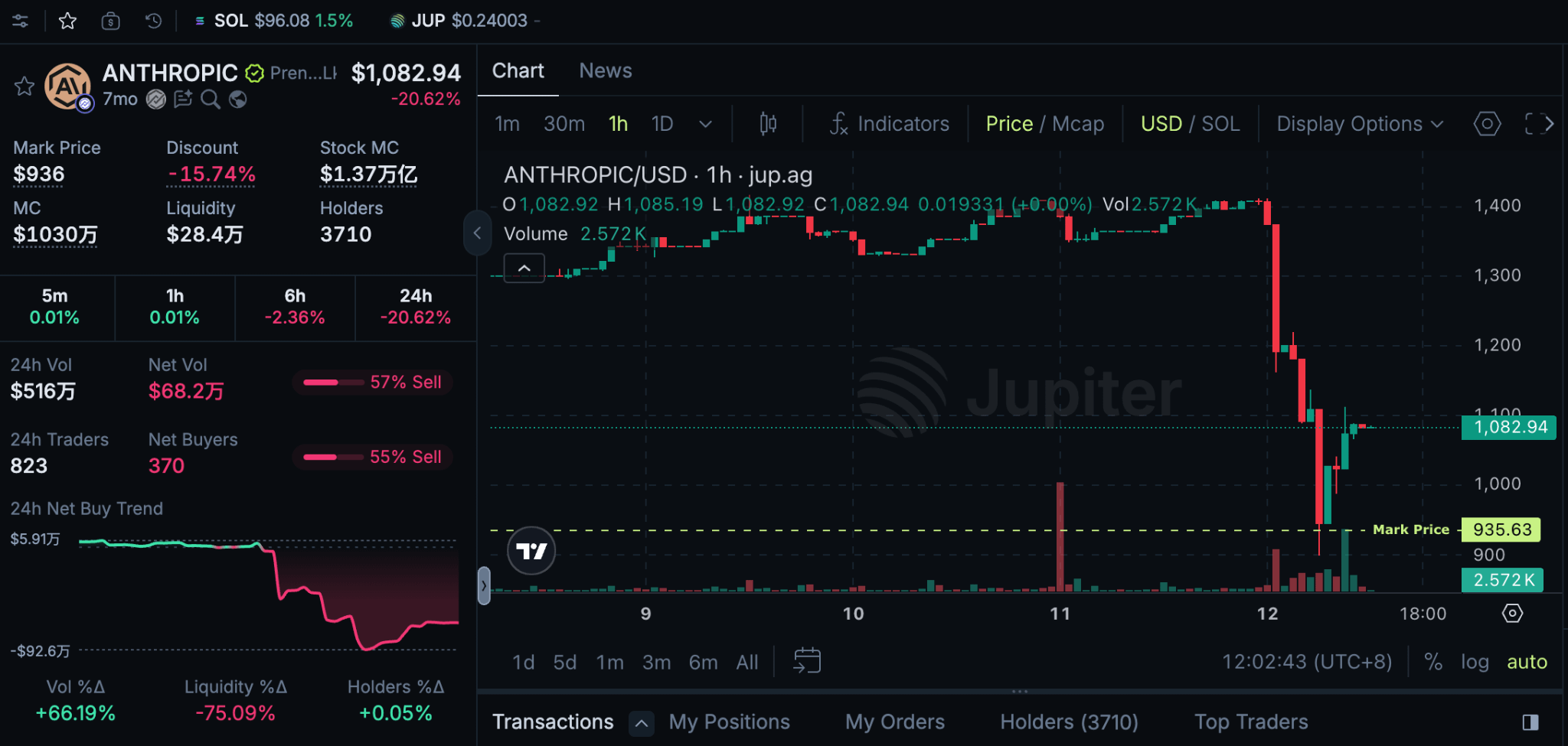

Anthropic went even further in May 2026, and declared that any sale of its stick not approved by its board is void. PreStocks had been running a tokenised Anthropic market for months, and when the announcement came, the price of its tokens dropped 27% within hours.

It goes to show that exposure to a stock’s price movement and ownership of the stock are two completely different things. One gives you price upside, but the other gives you rights, a vote, and a legal claim that a court would recognise.

The most extreme case was SpaceX, where all crypto exchanges promised and sold tokenised access to its anticipated IPO, collecting over a billion dollars in orders. The hype was off the charts because retail investors who had never had a way to buy into SpaceX before could do so now, and it felt like crypto was finally delivering on its original promise of access. But then the main provider, xStocks, could not deliver the underlying shares, and every exchange had to cancel and refund the orders.

There was literally nothing to tokenise because the entire product is built on the claim of an asset that no one in the chain could source.

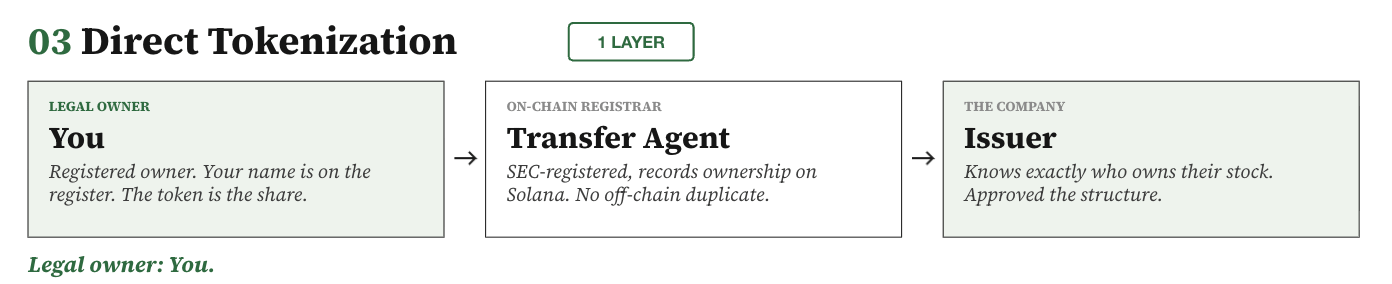

There are also exceptions to this that show how it can work, as well as a third model to do it. Superstate is an SEC-registered transfer agent that records legal ownership directly on Solana. The tokens represent direct shares with no custodian between you and the company. This is what dematerialisation was supposed to be fifty years ago, and the only time when “ownership” actually means what people think it means. Prathik will cover this side in more depth on Friday, so watch out!

Kraken also ran its tokenised stocks through its own broker-dealer, and it held where everyone else’s collapsed. In fact, Singapore’s Central Depository already gives every retail investor direct legal right to their shares, with direct voting and no nominees in between.

The regulatory path is already available. In May 2025, the SEC confirmed that a registered transfer agent can use a blockchain as its official shareholder register, with no off-chain duplication required. Superstate already does this on Solana, where you hold the token, and your name is on the transfer agent’s master file as the registered owner. Securitize runs on the same model and powers BlackRock’s BUIDL fund, which holds over $4 billion in tokenised assets, and the NYSE chose them in March 2026 to build its tokenised securities platform.

Countries like Switzerland, Germany, and Liechtenstein have also passed laws recognising on-chain records as the legal instrument of ownership. But the problem is that the intermediary chain itself is a $20 billion-a-year business in the US alone. Broadridge pulls in roughly $3.4 billion annually from processing proxy materials and investor communications alone. When the DTC itself ran a tokenisation pilot in late 2025, it still chose a model in which Cede & Co. remains the registered owner, preserving every intermediary in the chain.

To be fair, there is also a case where being a wrapper could be valuable. For someone in Lagos or Jakarta who has never had a way to buy Apple or Nvidia stock, a tokenised claim, even through an SPV, is still access they did not have before. But when OpenAI can reject your tokens within hours and Anthropic can void them with a single board statement, that access will only be as strong as its weakest link. And as we saw with SpaceX, when nobody in the chain can even source the underlying shares, the access doesn’t even matter. The point is that you should not have to choose between global reach and actual ownership.

And that’s the whole story, most of what the industry calls tokenised ownership today is the same IOU from 1973 on a new database. The tools exist, and a few teams are actually using them, but the rest of the industry chose to become the new middleman because that is where the real money is for them.

That’s all for today!

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.