Hello,

New technologies rarely come as clean replacements. They usually attach themselves to the infrastructure people already trust. That’s where teething troubles often emerge.

Cards did not eliminate cash overnight. Neither did mobile payments. Now, stablecoins are learning the same lesson.

One of the hardest parts of transitioning from older to newer rails for moving money is making that technology usable within the systems where people already live, shop, travel, and get paid. That’s where the value leaks, but it’s also where great businesses find opportunity.

At a pharmacy in Buenos Aires, a customer can hold USDT or USDC in a wallet, but the cashier still wants a card that can move those stablecoins and make a payment. The merchant doesn’t care about Tron, Base, gas fees or settlement finality.

Stablecoins only solved part of the problem by giving people access to hold dollars. Crypto cards help move digital dollars between the holder and the merchant. But when all cards offer similar rewards and move money between the same players, the differentiation lies in owning the deeper payment stack behind every swipe.

In today’s analysis, I will explain why crypto cards must vertically integrate across the payment stack.

Onto the story,

Prathik

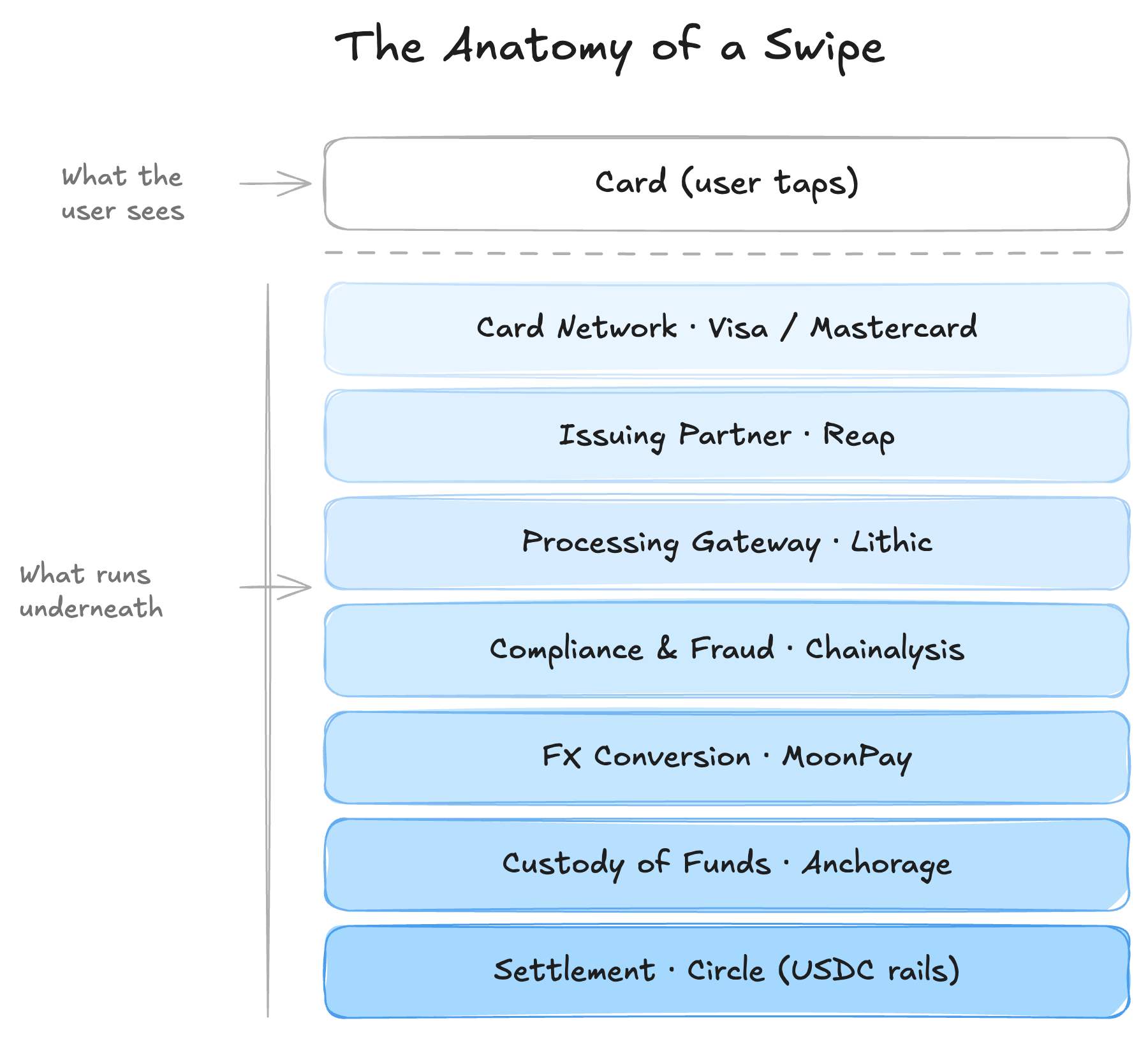

The Anatomy of a Swipe

A card swipe is one of my favourite things about finance. It looks so simple yet conceals a dozen actors orchestrating a complex chain of tasks. On the face of it, you just tap or swipe the card, the terminal approves, and the merchant hands you the receipt. But underneath it is a stack that includes an issuing partner, a processing gateway, a card network, a compliance partner, and a fraud monitoring body. The process also has to maintain custody of funds and process the FX when the user’s balance and the merchant’s currency differ.

When stablecoins enter the picture, you must address additional questions: Who holds the stablecoins, who converts them, who manages the routing, and who covers the volatility and settlement risk?

A crypto card solves the user’s problem at the surface. If you have USDT or USDC in a wallet, the card lets you spend it without forcing the merchant to touch crypto.

But as a business, the card is the least interesting part. In a world where everyone is offering cards to spend your crypto with similar rewards stacked on top, the only differentiation is owning enough of the stack so that every transaction creates value in more than one place.

Every layer of the payment stack charges the merchant a fee to pass the money along to the next layer. The best way to optimise such a stack is for a player to vertically integrate multiple layers and undercut other players by charging the user a substantially lower fee for moving the money.

Saurabh explains how this works for cross-border payments in his Stripe piece for Decentralised.co.

Crypto cards sit at a similar intersection.

A report by Memento Research notes that most cards today have similar propositions, usually built around prepaid balances, cashback or points. The moat in this environment is no longer the card itself.

How do you differentiate in such an industry? By operating across different layers of the stack underneath. One card may own more of the API orchestration, settlement logic and compliance stack. Another may mainly own the consumer relationship. How deep each one goes determines how much it earns.

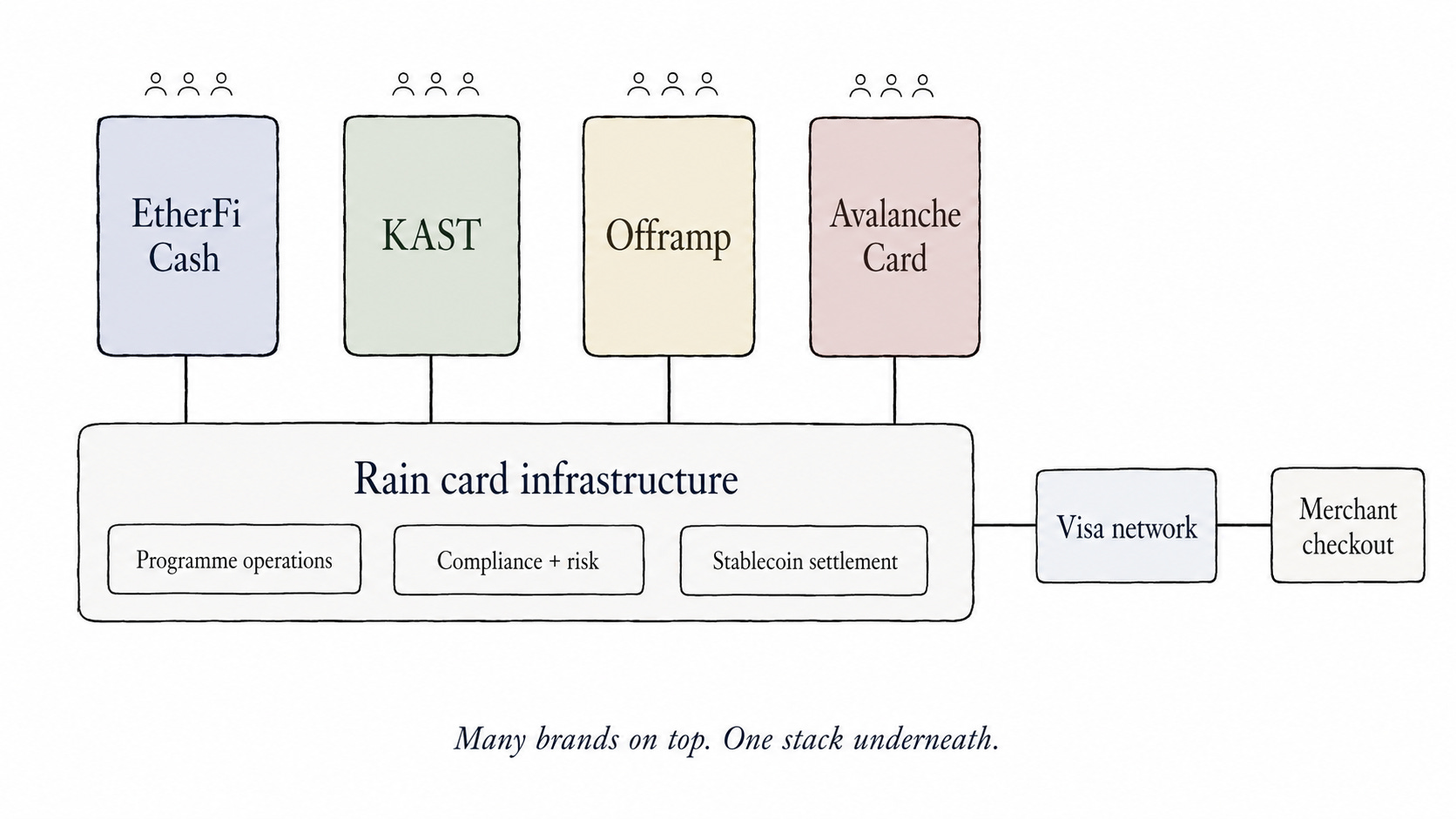

Consider a crypto-native case of Rain cards. Rain powers stablecoin cards and global money movement for platforms, fintechs, and institutions. It makes tokenised money like stablecoin usable in the real world through cards, wallets and everyday payments.

The Rain Case: Depth as Moat

Rain is a Visa Principal Member, which is the regulatory wedge that lets it issue cards or card programmes directly on Visa rails rather than renting infrastructure from an issuing bank.

When it offers a crypto card to its users, it also provides backend infrastructure spanning APIs, compliance layers, and settlement logic. This allows fintechs and wallets to launch stablecoin-linked card programmes.

Rain cannot afford to focus solely on winning customers who can tap their cards at stores. In that case, it will be competing with half a dozen other card providers trying to do the same thing. Instead, it is branding itself as a product that coordinates accounts, cards and global money movement through a unified API. Rain’s status as a Visa Principal Member allows it to help its partner wallets launch card programmes in just six weeks. Without a platform like Rain, a wallet would have to separately coordinate for months with an issuing bank, a processor, a compliance vendor, a settlement partner and local payment providers. Rain compresses all these into one single infrastructure layer.

Joel’s piece on vertical integration is useful here. In this, he argues how durable crypto businesses are those that control the supply side, demand side and distribution together. A similar argument can also be applied for cards in payments.

Here, the user’s stablecoin balance is the supply, the desire to spend it is the demand and wallet or fintech integrations form the distribution. Rain shows how owning the layers across these three layers helps in standing out.

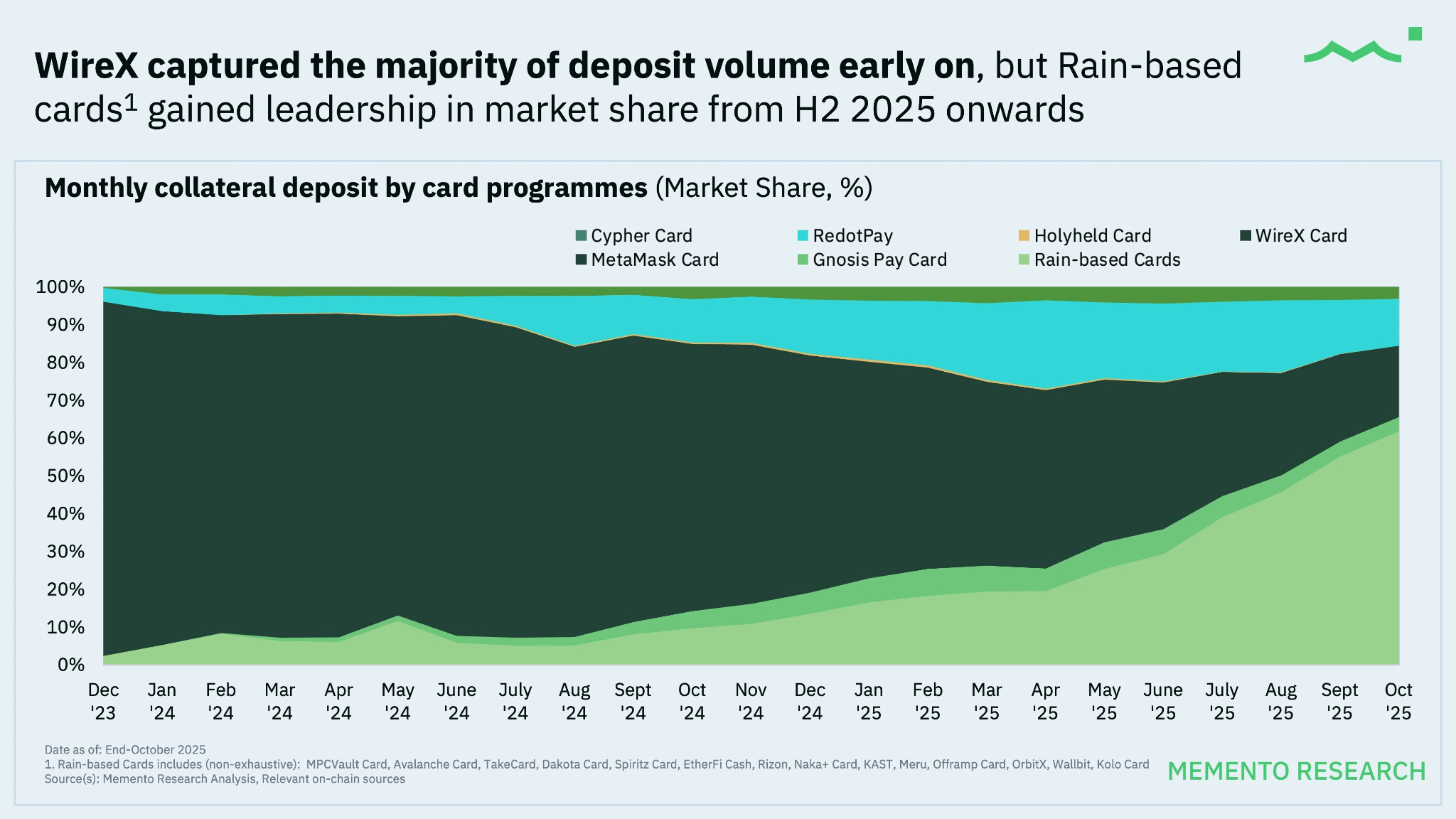

The numbers in Memento’s report validate the vertical integration thesis for cards.

It shows that Rain-based cards consistently led in deposit volumes because Rain offered the underlying infrastructure for multiple card programmes, including EtherFi Cash, KAST, Offramp, and the Avalanche Card. From the second half of 2025, a wave of new card programmes launched with Rain as their core infrastructure partner, helping Rain-based cards gain deposit-share leadership.

Building across multiple layers of the stack also gives a distribution advantage.

A normal card brand has to acquire customers one by one through ads, referrals, rewards or community campaigns. Rain can acquire them in batches by becoming the card infrastructure inside wallets and fintech apps that already have users. If EtherFi Cash, KAST, Offramp and Avalanche Card all run on Rain, each partner brings its own community and distribution, while Rain sits underneath the transaction flow.

The front-end brand may still belong to the wallet, but the programme operations, compliance, settlement and orchestration sit deeper in Rain’s stack. So the pharmacy in Buenos Aires may never know that the Avalanche card being used at the counter is powered by Rain. The user may not know either. But Rain still benefits because the swipe runs through infrastructure it helped build.

This is why comparing crypto card brands at face value is misleading.

A RedotPay card and a Rain-powered card may both let a user spend stablecoins at a merchant terminal. But from a business-model perspective, the value they capture depends on how many layers in the stack they operate on.

Better Risk Control and Higher Ceiling

The more of the underlying stack a card company owns, the more it can shape the user experience and the economics. If the business is only a front-end, it is fragile and vulnerable to changes made underneath.

It could lead to the problem of over-dependency and create a single point of failure.

A crypto card brand can promise cashback, points, metal-card aesthetics and instant spending. But if the issuing partner changes its risk rules, the card can stop onboarding users. If a processor tightens merchant category restrictions, some payments may fail. If a banking partner pulls out, off-ramp availability can shrink. If a card network changes compliance requirements, the business has to adjust overnight.

The user experiences the most disruption. Uncertainty around the terms of using the card can lead to frustration, which in turn leads to a customer-support nightmare. The rented infrastructure comes back to bite the card providers.

Memento’s report also notes that most card programmes sit on top of issuers, processors and a few crypto card-as-a-service providers. This could leave the card providers at the mercy of others who own various layers across the stack. We have seen this happen before.

In October 2023, Binance ceased its debit card services in the European Economic Area (EEA) after Paysafe, its banking partner in the region, ended offering its embedded wallet solution to the crypto exchange.

It also acts as an economic ceiling.

If a crypto card company rents issuing, processing, compliance, FX and settlement, then its room to monetise is limited to what remains after all those partners take their cut. It may still grow fast, but its ceiling is capped at the number of customers it can sell its cards to. This doesn’t give it control over the most important cost lines in the transaction.

The more fragmented the stack, the harder it becomes to offer lower fees, better rewards or more reliable settlement without going underwater on every transaction.

Vertical integration changes that equation.

A company that owns more of the stack can decide where to undercut its competitors with compressed fees. A vertically integrated brand can subsidise the front-end card because it earns from settlement and orchestration layers on the back-end. It can offer better rewards because it captures economics across multiple layers. The multi-layer presence even allows the company to move faster into new markets because it is not busy stitching together the compliance, issuer and processor stack in each new country across different geographies.

When half a dozen other card providers offer cashback and rewards to acquire customers, Rain can subsidise deeper and make money by coordinating the movement of stablecoins from wallets to merchants across compliance, orchestration and settlement layers.

This is the journey I see more crypto cards heading toward.

Card providers can still choose to continue building branded card programmes to acquire more users. Some might even build successful businesses by packing an attractive reward structure with intuitive design and token incentives. But their margins will still depend heavily on the infrastructure providers that they will have little control over.

On the other hand, there will be card companies that serve as the infrastructure underneath. These brands might still be less visible to the end users, but more important to the market. When five wallets launch cards on top of the same provider and compete for the same consumer, the infrastructure provider will be sitting cross-legged in the background, earning from all of them, irrespective of who wins the race.

This is how any industry matures. Swiping a card will remain the simplest activity in finance, and so the least profitable. The value for capturing will be in running the stack that coordinates the complex web of tasks underneath the swipe or tap of the card.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.