Hello,

I pay about $5 a month for home internet in India. It’s a 100 Mbps plan with unlimited data, and half the time they throw in a Netflix subscription to sweeten the deal. A few years ago, that same connection would have cost $25 or more. Then a company called Jio entered the market, started a price war with incumbent telcos, and the whole market repriced within a couple of years. Today, internet access in India is so cheap that it barely registers as a household expense.

For the longest time, I assumed this was how things worked everywhere. Once enough cables land and a competitor shows up, prices eventually fall. Africa has 25 submarine cables and over a million kilometers of terrestrial fiber. There’s no shortage of bandwidth at the coast. Yet broadband across the continent still costs about 15% of gross national income per capita, which is seven times the international affordability target. About 600 million people still lack meaningful internet access.

My $5 plan in India would cost over $100 a month in Nairobi, and even the most basic connection starts at $15. The median Kenyan household earns about $170 a month. The average Indian household earns about $250 a month, which is higher but not by a sufficient factor to explain a 10x to 30x gap in what people pay for the internet. There is enough bandwidth to serve the entire coast, but something inland consumes it before it reaches more users.

This piece is about what’s actually broken in the African internet landscape, how a DePIN project called Share is trying to fix it, and why its use of crypto is unlike anything I’ve seen before.

Why Africa Pays the Highest for Internet

To understand that, we need to look at where the money in Africa’s internet ecosystem actually goes. Google’s Equiano gave West Africa twenty times the bandwidth it had before. Meta built 2Africa, the longest subsea cable ever. Between them and the 23 other cables already in the water, African landing stations, the buildings on the coast where submarine cables come ashore, today have more bandwidth than most of the continent can use.

But none of that bandwidth is useful until it reaches the person paying for it, and that last stretch is where the entire problem starts. The next part is turning that into a connection for a household 50 kilometers inland, which means someone has to build local infrastructure, buy upstream capacity, set up billing, and sell service, one building at a time. That work today falls on thousands of small ISPs, most of them one or two-person operations, because the big telcos that could do it have no reason to.

They sell wholesale bandwidth to these small operators, and that’s a good business for them. If they built out the last mile and started selling directly to households, they’d be killing the wholesale contracts that pay them today. A single bulk deal with an ISP brings in steady revenue with almost no support cost. Replacing that with retail means billing millions of people one at a time, running customer support, and competing door-to-door with ten thousand operators who already have the relationships. No telco wants that trade.

Kenya is the easiest place to look at. The regulatory environment is stable, Safaricom runs one of the best mobile money systems in the world through M-Pesa, and multiple submarine cables land right at Mombasa. If any African country should have cheap internet by now, it’s Kenya.

The Communications Authority of Kenya has over 400 registered ISPs on its books. But the real number is much higher. Once you count the neighborhood-level operators who run a single router in a building and resell to a few dozen customers, the total is probably north of 10,000. That’s ten thousand separate internet businesses in a country of 55 million people, most of them serving a handful of users each.

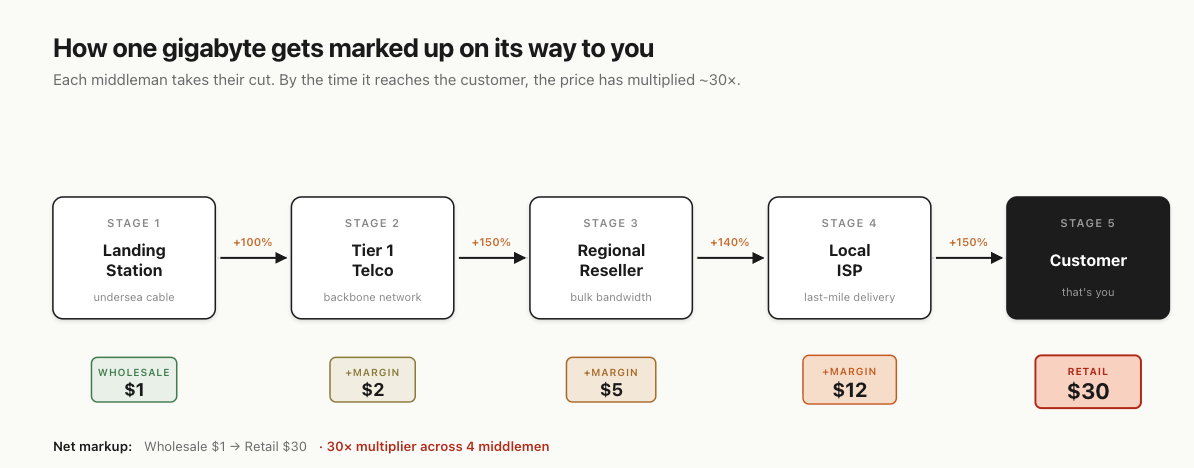

As a result, when someone in Nairobi goes online, their traffic typically passes through three to five of these small networks before it reaches the open internet. Every handoff between them adds cost and adds latency. By the time the signal reaches the end user, the price per gigabyte has multiplied several times over from what it costs at the Mombasa landing station. The bandwidth starts cheap, but it gets expensive on the way to the customer.

Running one of these small ISPs is a terrible business. You buy bandwidth in fixed bundles from an upstream provider and pay upfront before your customers pay you. Every month, you’re guessing how much capacity you’ll need. Buy too little and your service is unusable by evening. Buy too much, and that money is locked up in bandwidth nobody’s using, and you won’t see it back for weeks. There’s no room to invest in better equipment or a backup connection. You run one upstream link, oversell it, and hope the congestion doesn’t get bad enough that your customers switch to a different service.

This is one of the biggest reasons India’s Jio strategy will never work here. Jio walked into a market with a handful of national telcos and undercut them all at once. That only works when there’s a concentrated market to disrupt, and when you can spend $30 billion building your own last-mile infrastructure across a country of 1.4 billion people, losing money for years before seeing a dollar back. Kenya doesn’t have that. It has 55 million people. No Kenyan telco has $30 billion, and even if they did, the market isn’t large enough to justify that kind of spend. So the last mile stays with ten thousand small operators, and nobody above them has the reason or the resources to replace them.

In fact, you can see how fragile the whole arrangement is when something goes wrong. Four subsea cables off West Africa failed in March 2024. Eight countries went offline for days, and repairs took weeks to months. Two months later, SEACOM and EASSY were damaged off the South African coast, and most of East Africa lost access to cloud services. There were plenty of cables. The problem was that nobody inland had built local caching, proper routing, or any backup path. Most of the traffic was being routed through a single upstream link to Europe, even when other cables were still working. When that one path broke, there was no way to reroute and nothing locally cached to fall back on.

What Share Built

So that’s the problem. Thousands of small ISPs with no scale, no bargaining power, buying overpriced bandwidth through chains of middlemen, running on thin margins with no backup infrastructure. And on top of all that, the big telcos have zero incentive to fix any of it.

Share is a DEPIN project that is solving this exact problem by building the missing layer between the landing station and the last mile. The company is based in Kenya and started in Mombasa, and what they’ve put together touches three parts of the stack.

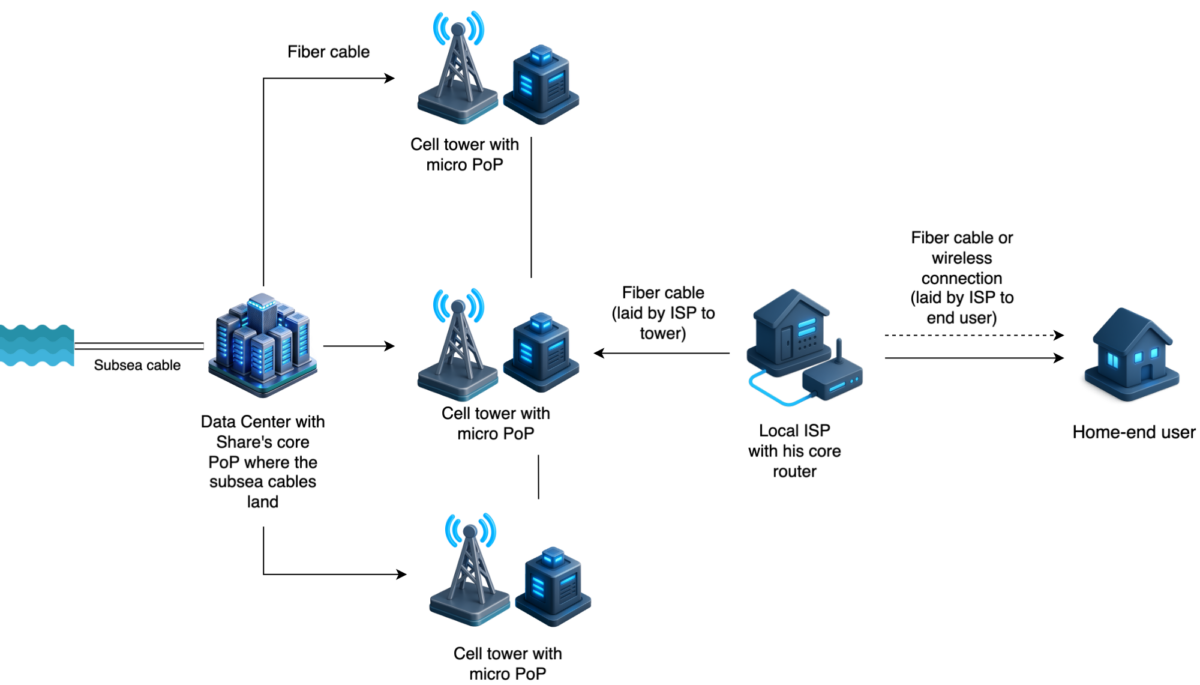

The first thing Share did was set up its own points of presence inside Kenya’s major data centers and connect directly to Meta, Google, Akamai, and Cloudflare. These are the content delivery networks that serve most of what people actually do online. YouTube, WhatsApp, Instagram, Netflix. Depending on the market, that’s 70-80% of all internet traffic. When an ISP connects to Share, that traffic no longer has to travel through three to five upstream middlemen to reach a European exchange point and come back. It terminates locally, inside Share’s own network. For the ISP, the cost per gigabyte drops on day one. For the end user, the video they’re streaming now comes from a cache in Kenya instead of being routed through Frankfurt, so it’s faster, too.

The second thing is physical fiber. Share laid a 40-kilometer fiber ring around Mombasa. It’s a loop, which means if any one segment gets cut, traffic automatically reroutes in the opposite direction. That ring alone can reach about 1.5 million people without anyone having to rebuild last-mile connections. Along the ring, Share places what it calls micro-PoPs. These are small, standardized network boxes at tower sites and rooftops, where nearby ISPs can plug in and connect to the backbone. Through its own fiber and infrastructure-sharing deals with tower companies and utilities, Share now has access to over 1,000 kilometers of fiber across Kenya. They just moved to Nairobi.

The third part is software. Every ISP that connects to Share gets access to a single system that handles routing, billing, customer onboarding, plan management, and revenue sharing. For a small operator who was managing everything on a spreadsheet and a handshake deal with an upstream provider last month, Share entirely changed their business operations. They go from reselling someone else’s marked-up bandwidth to operating as a last-mile partner on a real network with a real backend. Their costs drop, their service gets better, and they keep their customers. Share takes a minority cut of the revenue.

What makes all of this work together and scalable is how Share grows. When a small ISP joins Share, it doesn’t just get better infrastructure; its existing subscriber base immediately migrates to Share’s backbone, meaning Share inherits those customers without having to acquire them. That’s how they went from a test network in Mombasa to covering 8 million people in 15 months.

This is a model where everyone wins. The ISPs get lower costs and better service without losing their customers. The telcos and tower companies that own fiber and tower sites become suppliers to Share, which is a more predictable business than competing against 10,000 small competitors. Share gets a growing network with recurring revenue. Nobody in the arrangement is worse off than they were before, which is probably why it’s held together in a market where nothing else has.

Where Crypto Earns its Place

Most DePIN projects launched between 2020 and 2024 were pretty much the same. Launch a token; use it to pay people to set up hardware, to pay early users to show up, and to fund whatever activity generates a decentralised network. Helium did it. Render did it. A dozen WiFi hotspot projects did it. Most of them never shipped any real infrastructure. Even the ones that did were paying for hardware deployment with token incentives, and the moment the token lost value, the people running the hardware walked away.

Share doesn’t do any of that. The physical network already generates recurring revenue in Kenyan shillings. The company is profitable at the infrastructure level before crypto enters the picture. Crypto is only used in two places, and only because those two places have real problems that traditional finance hasn’t solved.

The first is settlement. Share’s ISPs collect revenue in Kenyan shillings. As the network expands into Uganda, Nigeria, and Ghana, they’ll be collecting in a different local currency in every market. But hardware and wholesale bandwidth are priced in dollars. So you have revenue in a dozen African currencies and costs in USD, and the financial infrastructure to move money between African countries barely exists.

Cross-border B2B payments between African companies today still route through correspondent banks in Europe and New York. The IMF’s numbers put the share of intra-African transactions that actually settle on the continent at roughly 12%. The other 88% takes a detour through Frankfurt or London, takes days to clear, and loses 3 to 5% to FX spreads and bank fees. A Kenyan ISP paying a Nigerian equipment supplier is sending money through Europe to reach the country next door.

The second is financing, and this is the part I think is sharpest.

Each micro-PoP unit is built to the same spec, so you can model what it will earn before you deploy it. All traffic flows through Share’s billing system, so revenue is verifiable on-chain in real time. No bank is going to write a $5,000 loan for a networking box at a Mombasa tower. The deal is too small, the borrower too thin, and the lender would need a local office just to do diligence. But an on-chain structure can underwrite the device itself: a buyer takes a claim on a specific micro-PoP through a smart contract and gets paid based on actual traffic. If the device goes down or users drop off, it shows up in the data immediately. The lender doesn’t need to trust the borrower. They need to trust the data coming off the device, and that data is verifiable.

If this works at scale, and I believe it will, small-ticket African internet infrastructure can be financed with global capital for the first time, one device at a time, without going through a development bank or waiting for a government guarantee.

Markets like Kenya exist all over the developing world. Indonesia’s archipelago has the same problems. Thousands of small operators, deep gaps between coast and interior, upstream pricing controlled by a few large wholesalers. You see it in rural South Asia and parts of Latin America, where submarine cables landed years ago, and nobody built the inland distribution. In each of these places, there is demand and coastal bandwidth, but nobody builds the middle layer because no single company has the incentive to do so.

If the model keeps working in Kenya, and 8 million people over 15 months say it is, this might be the template for how internet infrastructure gets built in fragmented emerging markets over the next decade. I think we’ll look back at Share as proof that DePIN was always supposed to be an infrastructure business that uses crypto to move money and finance hardware, and nothing more than that.

That’s all for today.

Until then, stay curious,

Vaidik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.