Your Bitcoin Can Buy a House. Don’t Sell it

A small change that could reshape how people use their crypto wealth.

Hello,

If you own Bitcoin in America and want to buy a house, you only have two options, and both of them are bad.

Option one: sell your Bitcoin, pay the capital gains tax on every dollar of appreciation, use the cash for a down payment, and lose your position entirely. Option two: keep your Bitcoin. But when you apply for a mortgage, the system treats you as if that wealth does not exist. Until recently, it officially did not.

Around 52 million Americans own crypto. 53% of millennials under 35 hold some form of it. But the median age of first-time homebuyers in America just hit 40, the oldest on record. So you’ve got a whole generation building wealth in crypto and then being asked to sell it just to qualify for a home loan.

But that’s finally changing…

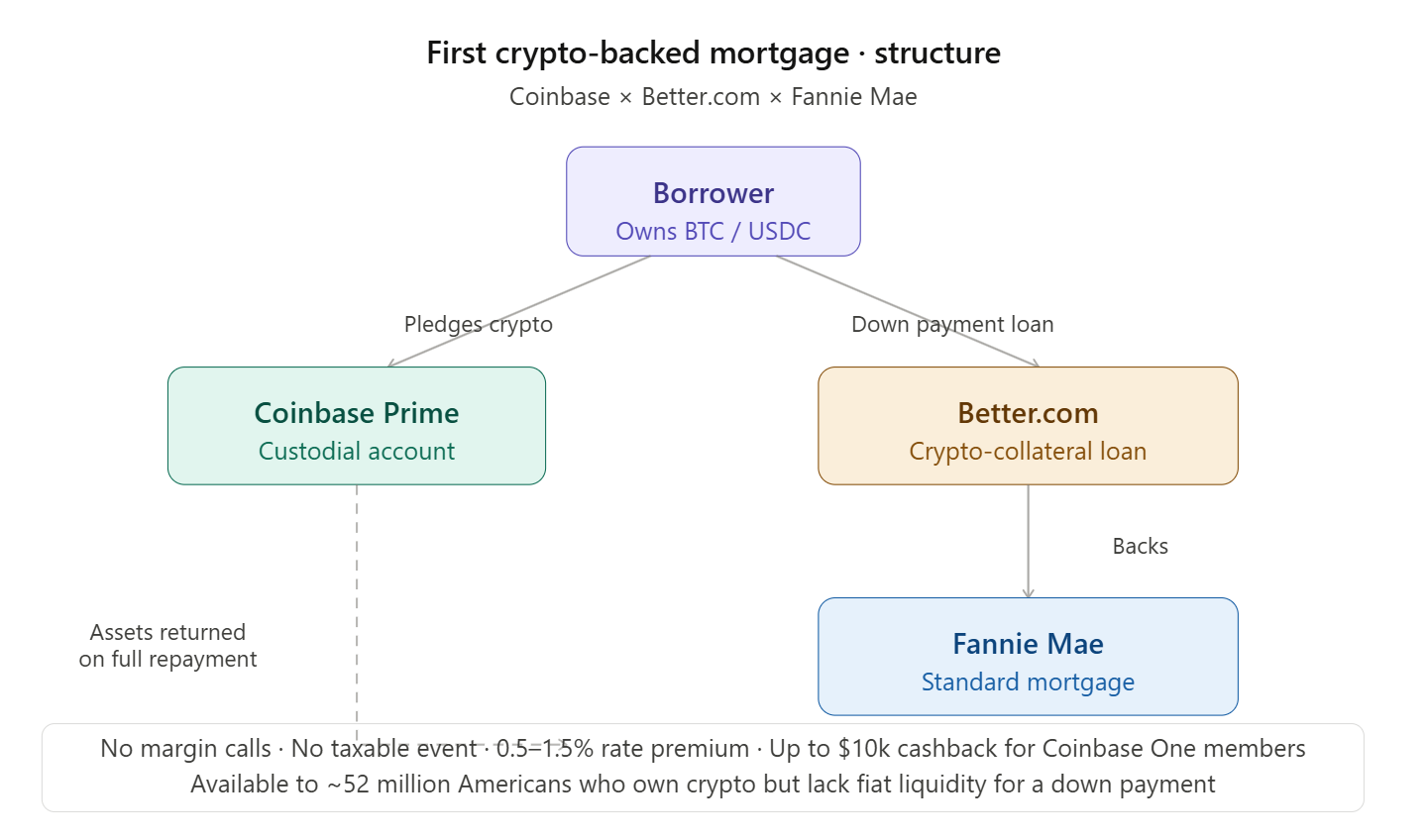

Better Home & Finance and Coinabse launched a mortgage product last week where you pledge your Bitcoin or USDC as collateral for the down payment. You get a Fannie Mae-backed loan. You keep your crypto, you do not need to sell it, you do not trigger a capital gains event. And the most important part, even if Bitcoin’s price drops, you don’t lose your home.

That’s the key part. Here’s how it actually works.

Lessons From Every Crypto Lending Failure

In 2021, a wave of companies figured out how to offer something that sounded impossible – interest rates of 6 to 10% on your Bitcoin or Ethereum, when a bank savings account was paying close to zero. BlockFi, Celsius, and Voyager were the biggest names. The model was simple. You deposited your crypto with them, and they lent it out to institutional traders and hedge funds who would pay high rates to borrow it, and they passed some of that yield back to you. At their peak, Celsius had $12 billion in customer funds. BlockFi was valued at $3 billion. Voyager had $5.9 billion on the platform.

Then crypto prices crashed in 2022. The hedge funds and traders who had borrowed crypto to run their strategies started getting margin called. They could not repay. The collateral backing their loans lost value faster than anyone could liquidate it. Celsius froze all customer withdrawals in June 2022. BlockFi filed for bankruptcy in November with $3 billion in liabilities against barely $150 million in assets. Voyager went down right after. All obituaries were now saying the same thing: Crypto lending is too risky.

What they actually meant was that particular model of crypto lending is too risky. The problem was that the collateral and the loan were in the same asset class. When crypto prices fell, the collateral lost value at the same time as the borrowers’ losses mounted. Margin calls were fired, forcing people to sell. That selling pushed prices down, which triggered even more margin calls. The whole system was wired to accelerate its own collapse.

The Fannie Mae product is something very different. Here, your collateral is Bitcoin, your loan is a fixed-rate dollar mortgage, and your monthly payment is a dollar amount that does not change, regardless of what Bitcoin does. And the trigger for losing your collateral is not price. It is 60 consecutive days of missed payments. The same standard practice, applied to every conventional mortgage in America.

That means, if Bitcoin drops 70% right after you take the loan, your mortgage doesn’t change. The collateral simply stays with Coinbase, and your loan continues as usual. You keep making the same monthly payments, and that’s all that’s required. The price volatility of your collateral is entirely absorbed by you as the borrower. The lender is not exposed to it at all.

This became possible in June 2025, when the FHFA issued a directive ordering Fannie Mae and Freddie Mac to start accepting crypto as financial reserves without requiring conversion to dollars. That reversed a 2022 policy that had locked digital assets out of the mortgage underwriting system entirely.

There is also a tax angle to this, pleading crypto as collateral is not a taxable event. You have not sold the asset, so no capital gains liability is triggered. The only scenario where taxes enter the picture is if the collateral gets liquidated, and this product is specifically designed so that price drops never cause that to happen. So the only path to liquidation is for a borrower who stops paying for 60 days.

Of course, this isn’t free; the rate premium is 0.5-1.5% above a standard 30-year mortgage, depending on borrower profile. But for a homebuyer sitting on Bitcoin that has appreciated 300% and does not want to sell, paying a slightly higher rate to preserve the position and avoid a tax hit is the better deal.

The Real Risk

The mortgage product itself is pretty conservative, but the real question is what happens when it scales.

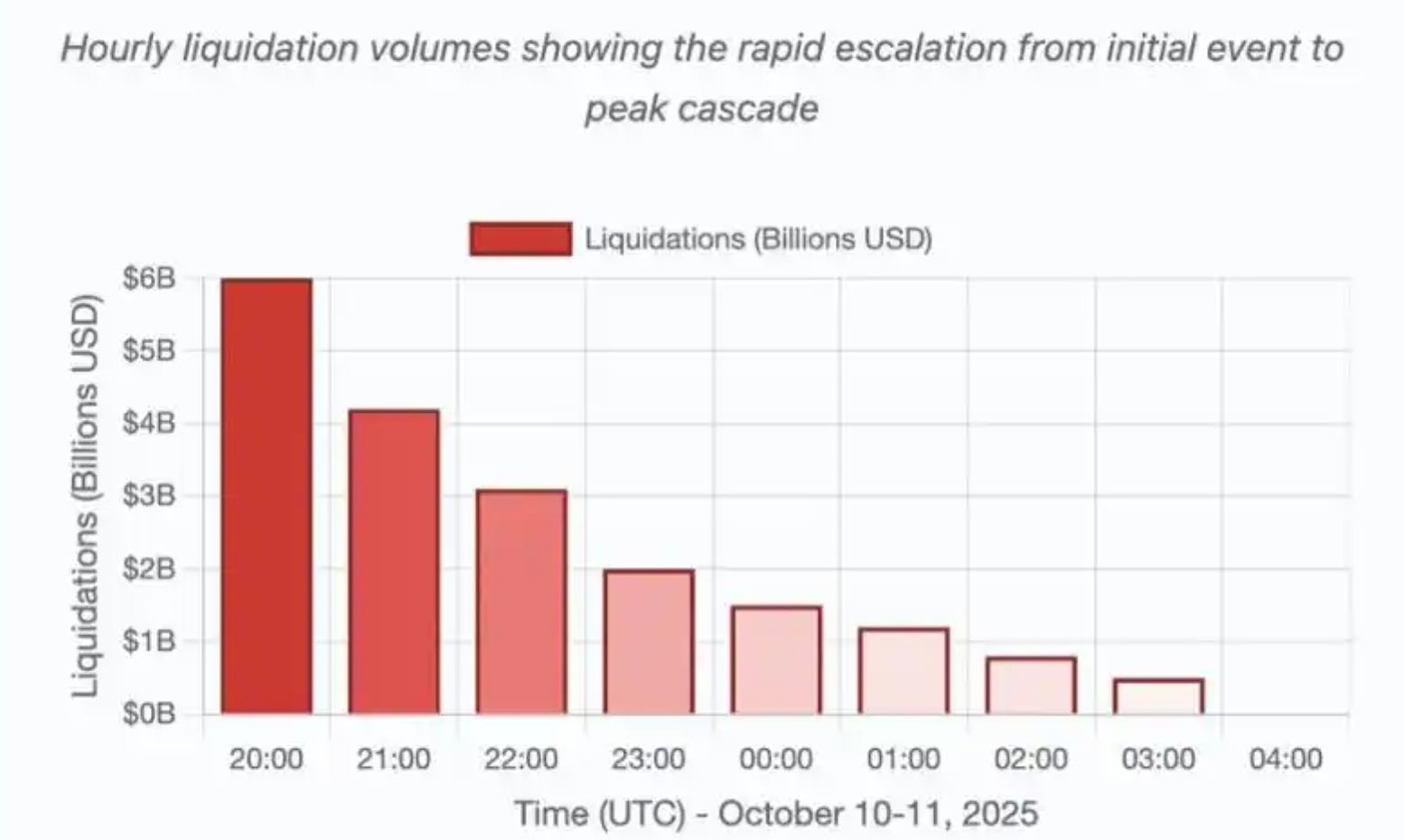

On October 10, 2025, crypto markets saw $19.16 billion in liquidations in a single day, one of the largest to date, wiping out 1.6 million trading accounts. At this point, we know how these cascades work. When leveraged positions cluster at similar liquidation prices, each forced sale pushes the market down enough to trigger the next position’s liquidation threshold, which triggers the next, and so on.

The Fannie Mae product doesn’t create that kind of cascade because there are no price-based liquidations. But as this scales, a different kind of risk comes in, which is, what will happen if a market crash hits at the same time people start defaulting on their loans?

Consider the scenario where a severe crypto crash coincides with an economic downturn. Bitcoin falls 60%, layoffs rise, and some borrowers lose income while also watching their portfolios fall, which leads them to start defaulting on their mortgage payments. At 60 days, liquidation begins, and Coinbase starts selling the bitcoin collateral into a market that is already distressed. If this happens at scale across thousands of mortgages simultaneously, you have introduced a new vector for crypto selling pressure that is correlated with economic stress. It’s not a doom loop, but definitely a feedback mechanism worth watching as the product scales.

Ledn’s example is useful here. It is a crypto lender that has been making Bitcoin-backed loans since 2018, and by most measures, it is one of the most conservative operators in the space. It has originated hundreds of millions in loans without a single loss on record.

In early 2026, it was in the middle of closing a $188 million bond deal, essentially packing a pool of its Bitcoin-backed loans into a security that institutional investors could buy, the same way banks bundle mortgages into mortgage-backed securities. Before the deal could close, Bitcoin dropped 27% in a short window. Because Ledn’s loans had price-based margin call triggers built in, the collateral backing roughly 25% of loans in that pool fell below the required threshold, and those positions had to be liquidated. The bond deal survived, but a quarter of it has to be unwound before it even reached investors.

Ledn’s product and the Fannie Mae mortgage are structurally different. But the episode shows that even well-run, conservative crypto lenders operating at a relatively modest scale had to face liquidations due to one price move.

Beyond The Mortgage

Fannie Mae’s product is only a few days old. There are no stress test results because there has been no stress. We will get those answers over time, most likely when it is no longer hypothetical. What we do know is that it is the first crypto-backed mortgage in America, and it will not be the last.

Companies like Figure Technologies have been offering Bitcoin-backed mortgages up to $20 million with 30-year terms since 2022, without Fannie Mae backing. SoFi, a U.S.-regulated bank, is expanding into crypto-collateralized products and launching a native stablecoin in 2026. The idea of “putting your bitcoin to work without selling it” is expanding and moving beyond just homeownership into auto loans, business loans, and margin facilities for investors. Anywhere that collateral currently has to be converted to cash before a bank will accept it represents a potential expansion of this model.

The mechanism is the same in every case. You hold an asset. The system accepts that as proof of your creditworthiness, and you borrow against it. The asset stays on your balance sheet. You do not pay capital gains tax because you never sold it.

For the past decade, one of the biggest inefficiencies in crypto has been that it sat outside the productive capital system. You could hold bitcoin, watch it appreciate, and then do exactly the one thing you could: sell it, pay taxes on it, and re-enter the dollar economy. There was no way to let it function the way a stock portfolio functions for a wealthy investor, as something you borrow against while keeping the underlying asset intact.

Regulators are moving in the same direction. When FHFA reversed its 2022 policy to accept crypto as a financial reserve, it was a change in how they classify crypto. When CTFC launched a pilot in December 2025, allowing Bitcoin and USDC as collateral in derivatives markets, that was another one. They are signaling that crypto belongs in the same bucket as other assets the financial system uses to function.

Today, US Treasuries are the world’s default collateral because they are liquid, predictable, and backed by something everyone has agreed to trust. That took decades. Bitcoin is earlier in that same process, with more institutional infrastructure already in place than Treasuries had at a comparable stage.

That’s it for today. See you next week.

Until then, stay curious!

Vaidik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.