When we think about competition, we think about “survival of the fittest.”

I hear that phrase and imagine a relentless war of all against all, where the fiercest predator wins by crowding out everyone else.

But now I doubt that is how lasting ecosystems actually form. At the turn of the twentieth century, the naturalist and philosopher Peter Kropotkin challenged this view in his evolutionary essays on mutual aid. Kropotkin saw that species surviving severe climate shifts succeeded through sophisticated patterns of collective cooperation. Mutual support is infinitely more powerful than individual warfare in long-term evolutionary progress. The truly “fittest” are those that learn to cooperate and build stable, shared frameworks to handle an unpredictable environment.

The principle spans everywhere.

Every crypto project is figuring out what it actually is right now, and the protocols that survived are each making a defining call about what comes next.

Some development teams are retreating to original ideological principles like absolute censorship resistance and pure decentralisation. Others are integrating centralised overrides to maintain basic solvency. A few are focusing entirely on proprietary ecosystems, pulling their internal liquidity into isolated rollups.

ZKsync made a different call, a mutually aided one. It’s building for banks.

BCG projects the tokenised asset market moving onto blockchain rails, hitting $10-16 trillion by 2030. Every major bank is running pilots. Some have moved past pilots into live production. The infrastructure decisions being made right now will determine how that money moves and who controls the rails it moves through.

ZKsync is currently a serious public blockchain candidate for those rails. That’s why it matters even if you haven’t thought about L2s since the last bull run.

Why are banks even here? Why ZKsync specifically?

Deutsche Bank isn’t on the same ZKSync as regular crypto users. They’re on the Memento ZK Chain, a private, permissioned Layer 2 that Memento built using ZKsync’s Prividium stack.

Prividium is ZKsync’s institutional product. This offers private transactions, controlled access, built-in compliance tools, and final proof that everything settles on Ethereum. After testing five different blockchain ecosystems, Memento picked ZKsync. Fund deployment now takes 2-3 weeks instead of 2-3 months.

Banks love zero-knowledge tech because it proves a statement is true without revealing the private details behind it. A bank verifies a transaction without showing the public the names, the dollar amounts, or the assets involved. This private setup gives the bank total control over who sees what, providing privacy for corporate strategy and clarity for regulators. It fits how Wall Street actually operates.

Tradable has $1.7 billion in private credit sitting on ZKsync. Nearly 30 institutional positions targeting yields between 8% and 15.5%. And in October 2024, Buenos Aires quietly moved its entire digital identity system onto ZKsync Era. 3.6 million residents got cryptographically secured government credentials overnight. Local government can’t track that. The city became the first in the world to do this.

The global private credit market reached $3.5 trillion by late 2025. Tradable’s share is under 0.05% of that pie. Tokenised credit could grow into a meaningful share, or stay marginal, though the current situation says it is growing. Either way, the difference between the on-chain money today and the total available market cap is gigantic.

Think about the choice a corporate risk team faces here. They must decide between an isolated network that they completely control, a corporate group bound by contracts, or a public network managed by an online community.

JPMorgan is a private network under absolute internal control. It has run its own internal blockchain setup through its Kinexys unit since 2019. They handle repo trades and cross-border payments, as well as asset settlements, with partners such as BlackRock and Siemens. JPMorgan hosts the machines and manages the ledger while maintaining zero exposure to public online forums. Fees never change because a token holder voted, and system upgrades follow internal calendars. JPMorgan is the governance.

The catch is in their own numbers. Kinexys processes around $5 billion daily. JPMorgan’s payments division processes $10 trillion a day. Their own blockchain unit handles about 0.05% of their own payment flows, five years in. The bank that has the most control over its blockchain infrastructure also has the least adoption of it. Full control didn’t solve the hard part.

Then you have R3 Corda, which cleared $10 billion in tokenised real-world assets. It processes a million transactions daily. Corda functions as a consortium of over 200 financial institutions that built their rules upfront through contracts. When a feature changes, it changes because the members collectively signed off on it. The banks secured a seat at the table before the first transaction ever settled.

These platforms are ZKsync’s competitors. Yet ZKsync delivers a specific benefit that proprietary or consortium networks cannot replicate. Public verifiability without data exposure, paired with a settlement layer independent of any single corporation’s survival. If a single institution terminates its internal blockchain unit, the assets hosted on that network face immediate operational danger. Assets anchored via ZKsync settle to the Ethereum mainnet, which lacks a chief executive to order a shutdown. This separation remains the primary differentiator, and balancing it against governance exposure is a live debate.

Before ZKsync committed fully to the institutional strategy, it ran an incentive program called Ignite, paying DeFi protocols to stay active on the network. When the strategy shifted, they ended Ignite, citing a shift to enterprise. The activity followed the incentives.

Around the same time, ZKsync Lite, the original network from 2020, shut down permanently. Matter Labs had been signalling this since December 2025 and gave a confirmed date in late February. Funds remained claimable indefinitely, and none of the institutional deployments was on Lite anyway.

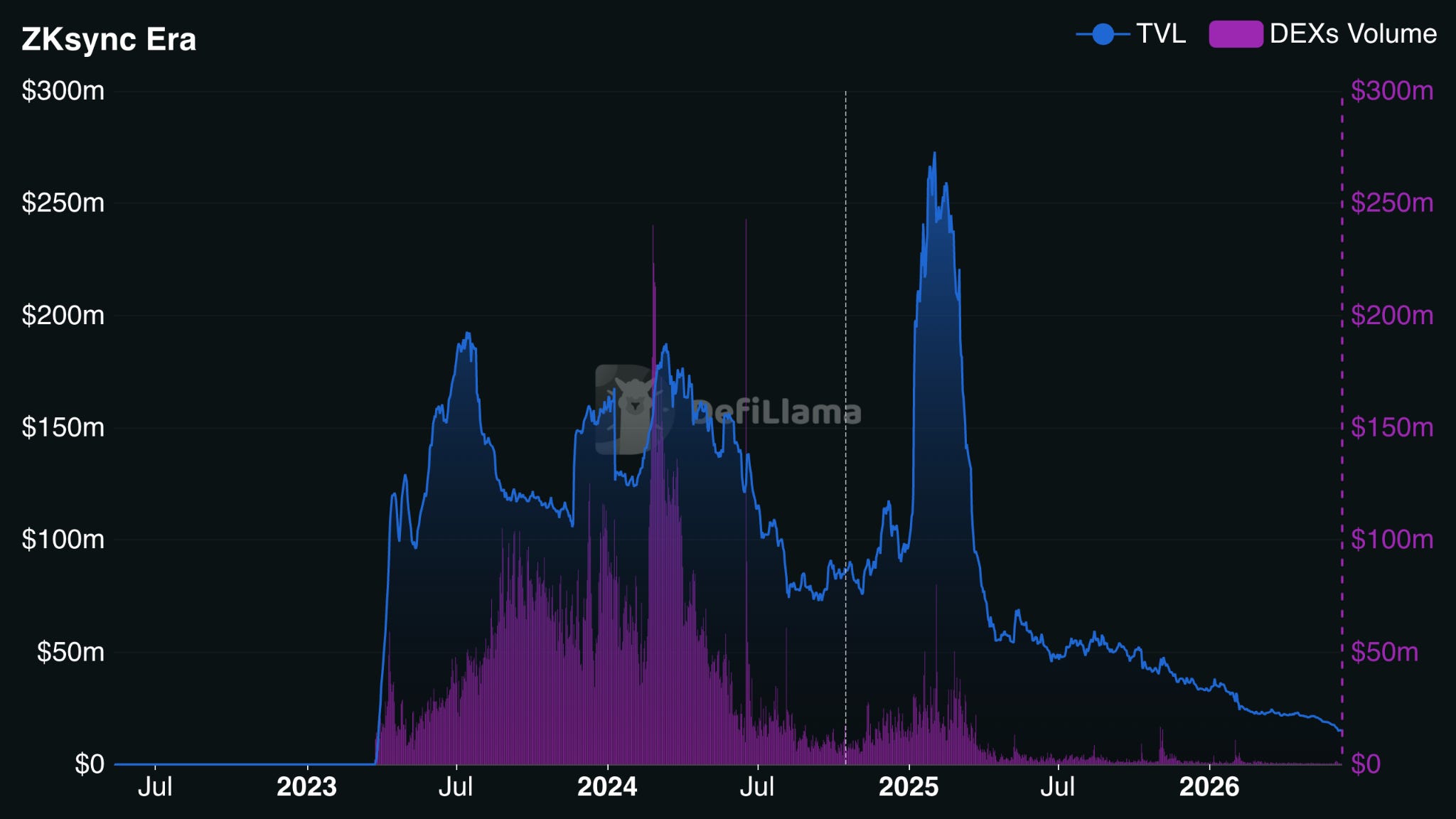

Aave, the massive DeFi lending protocol, voted to pull the plug on its ZKsync Era market. The motivation came down to raw numbers. ZKsync generated just $714 in fee revenue for Aave over a 30-day window. Compare that to Base, which brought in $300,000, or the Ethereum mainnet at $7.7 million. The voting forum concluded the chain lacked true product-market fit, proposing that any future deployment on any network must hit a $2 million annual revenue floor before Aave even considers launching there.

At the height of the retail layer-rollup boom, ZKsync Era regularly held hundreds of millions of dollars in locked DeFi value. Today, the total value locked across its public DeFi ecosystem is roughly $15 million. For context, top-tier retail networks maintain billions.

If this stalls, the ecosystem depends entirely on your thesis. Are L2S supposed to be consumer-crypto havens that banks are co-opting, or just corporate rails that happen to settle on Ethereum?

Matter Labs explained this to you earlier this year. CEO Alex Gluchowski released a roadmap that shifts the focus to building heavy-duty financial infrastructure for traditional markets.

Look at the product releases themselves. They rolled out Prividium to give banks an isolated space where transactions stay locked away from public view. Then they introduced the Bank Stack, partnering with entities such as the Cari Network to onboard regional banks that manage billions in traditional deposits. So, Aave’s departure did not shock the developers.

Talking about the Cari Network deployment. It was started by a former US Comptroller of the Currency, and they are planning a pilot next quarter with five regional banks. These banks hold over 600 billion dollars in total deposits.

If that pilot works out, nobody will care that retail DeFi apps left the chain. The transaction volume from banks at that scale replaces the loss. But if it fails, ZKsync is a good piece of tech with no users, running a few corporate experiments.

The v31 protocol upgrade, passed through ZKsync’s governance forum, went live in early May.

Under v31, every cross-chain call between ZKsync chains costs a flat 10 $ZK. That number was set by a DAO vote. Banks deal with volatile costs all the time, such as gas fees, cloud compute, and FX spreads. That is part of doing business.

The fee structure itself, not just the price, but the entire mechanism of how fees work, can be rewritten by the same forum. There’s no obligation to tell the institutions running on top of it.

The ZK Nation forum is already working on what comes next. They are debating node operator transaction fees, staking rules, and custom pricing for checking proofs. Each one of those is a live research thread that could become a vote that changes the economics of every cross-chain operation Deutsche Bank or Tradable runs. Anyone can read this on forum.zknation.io, publicly available.

Compare that to Kinexys, where JPMorgan holds the absolute keys to the system. Or Corda, where a formal contract dictates how adjustments happen and under what circumstances.

So, why would a bank ever choose ZKsync over JPMorgan? Because ZKsync gives you public proof that your transactions are valid without revealing your private data.

If JPMorgan decides to shut down its blockchain unit tomorrow, any assets on it are stuck. If Matter Labs (the company behind ZKsync) goes out of business, ZKsync keeps running because it settles on the public Ethereum network. But to get that, you have to accept that the network isn’t owned by anyone. A network that isn’t owned by anyone is governed by whoever shows up to vote.

$ZK is currently trading around $0.01. At its all-time high in June 2024, it was $0.3285. That’s a 96% drop. At 10 $ZK per interop call, that same cross-chain transaction costs roughly $3.28 at peak. Today it costs $0.10. The asset price volatility can be managed, but relying on an online community vote makes long-term budgeting entirely unpredictable for corporate planners.

L2Beat categorises ZKsync Era as a Stage 0 network, meaning an independent Security Council can pause or modify smart contracts without waiting for a full DAO vote. Mature Stage 1 networks, such as Arbitrum, lack this type of central intervention mechanism. Corporate risk managers often value emergency stop buttons to reduce the damage from smart contract exploits. However, this particular control belongs to a Web3 Security Council that functions outside traditional corporate structures.

Sygnum tokenised $50 million of Matter Labs’ corporate treasury into a Fidelity liquidity fund on ZKsync. Fidelity subsequently launched an institutional money market fund on the network. The builders kick-started ecosystem volume by placing their own capital into the product, establishing the core enterprise case study. The application processes live assets smoothly, yet the arrangement directly serves the founding team.

The core infrastructure remains tethered to an independent Security Council holding the keys to the system. During an emergency, this entity can bypass the standard delay mechanism completely, modifying smart contract parameters or freezing functions with zero advance notice. Control of the live system rests with this council and the active token forum, meaning participating banks operate under an organic, shifting governance structure rather than a fixed enterprise agreement.

ZKsync is betting its survival on a group that has never kept a crypto project alive before, that is, regulated financial institutions. Banks don’t care about tokens or post on governance forums.

Banks do, occasionally, build their core infrastructure on something and then never leave. That way of survival is lower to arrive, harder to dislodge.

ZKsync is either the first crypto project to achieve that, or the most expensive proof that banks will always eventually build their own version and walk away. The difference between those two outcomes is probably decided in the next 18 months.

The graveyard is full of projects that were right about the technology and wrong about the governance and the sustainability. The ZKsync governance test is still running.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.