Hello,

If you live outside the United States and want to buy a share of SpaceX or Nvidia, it’s not easy. You need a brokerage account that accepts residents of your country, a compliant bank transfer route, and often an investor accreditation. Most people cannot buy a US stock directly.

Blockchain is building workarounds. You can now get exposure to US companies through tokenised stocks. But “tokenised stock” is often used as an umbrella term for three different products.

First is the on-chain equity registered with the company’s share issuer. Second, it could mean tokens that are backed 1:1 by real shares, often held by an offshore company on your behalf. Lastly, there are perpetual futures contracts that hold no underlying shares. Each of these could mean different things for the holder in terms of ownership, voting rights and price exposure.

Right now, all three exist for Nvidia. Over 650,000 real Nvidia shares back the first two types of tokens. Yet the perpetual futures version, which has no underlying shares backing the token, trades at 4-5 times the volume of the other two types.

Last week, Vaidik traced how most stock ownership, tokenised or otherwise, has been built around the same nominee structure since 1973. He explained how almost nobody who “owns” a stock actually owns the share.

Read: Who Actually Owns Your Stocks?

In today’s piece, I explore how ownership of tokenised shares is structured across different on-chain instruments and what drives the market to trade them even when ownership is completely abstracted.

On to the story…

Tokenising Stocks

Tokenised stocks are digital representations of company shares on the blockchain. These tokens are programmable instruments that can move between wallets, trade around the clock, and integrate with decentralised financial protocols. The share’s economic properties, like price exposure, dividends and corporate actions, are embedded in the token.

The market for these tokenised stocks is no longer small. Over the last year, the total market value of tokenised stocks has shot up almost five times from $327 million to $1.5 billion.

This wave of tokenised stocks is interesting because of who is leading the experiments. The DTCC, the centralised body that clears, settles, and custodies the vast majority of US and global securities transactions, announced last month that it’d launch a tokenised securities pilot in October 2026. Earlier this year, the NYSE said it was developing a platform for 24x7 tokenised stock trading. These are incumbent institutional giants that are reconsidering the infrastructure that has facilitated stock trading for decades.

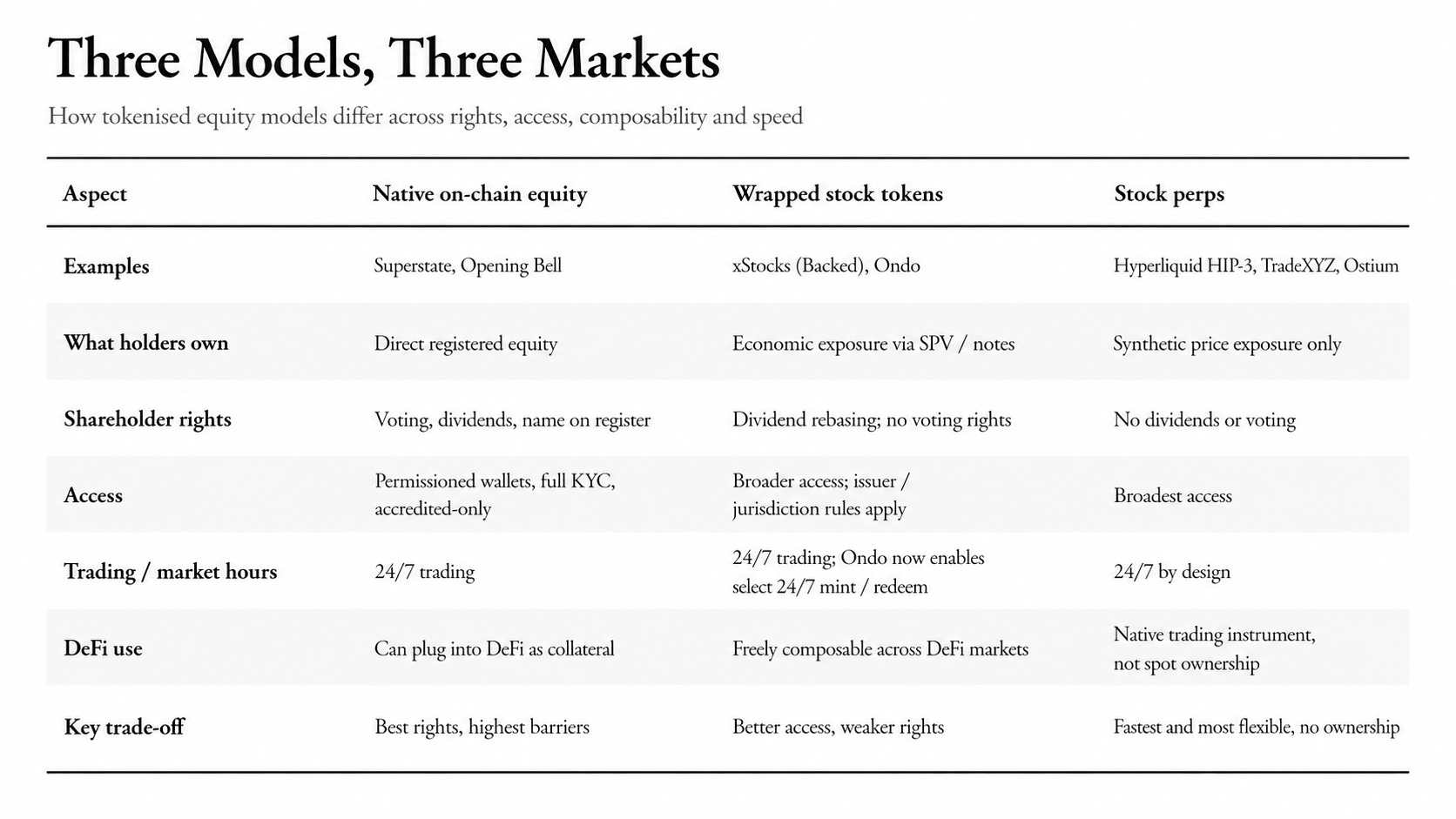

Many protocols are tokenising stocks in different ways. Each of these on-chain instruments offers a different level of ownership, redemption, composability and price exposure.

Let’s dive in.

The Tokenisation Trade-Offs

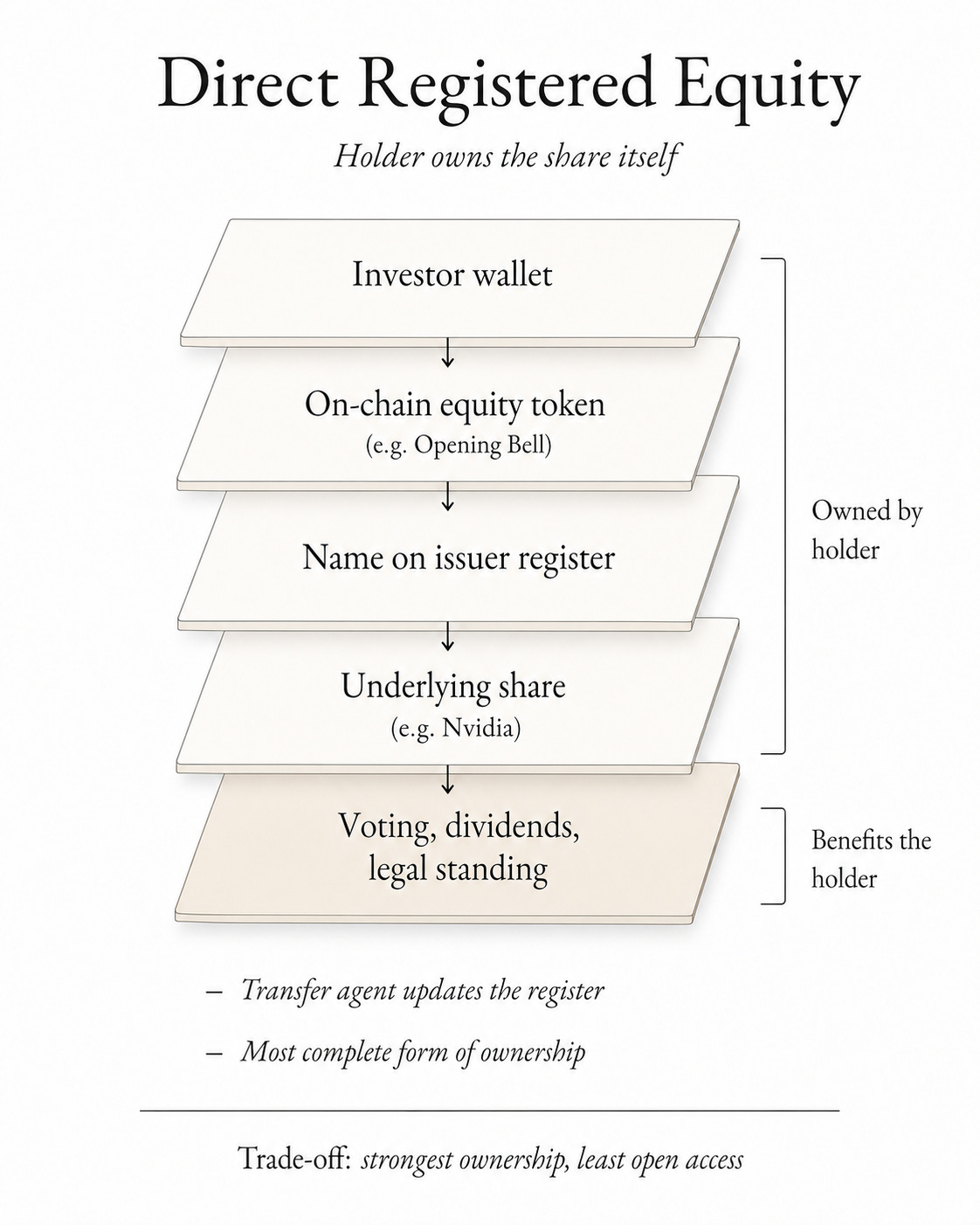

The first model gives you real ownership.

Superstate, an SEC-registered transfer agent, records ownership directly on Solana, and the holder’s name appears on the company’s shareholder register with full voting rights, dividend eligibility, and legal standing.

Galaxy tokenised its registered equity this way and ran on-chain proxy voting through Broadridge in May 2026. In December 2025, Superstate equities went live as collateral on Kamino, the first regulated equity usable inside a DeFi protocol.

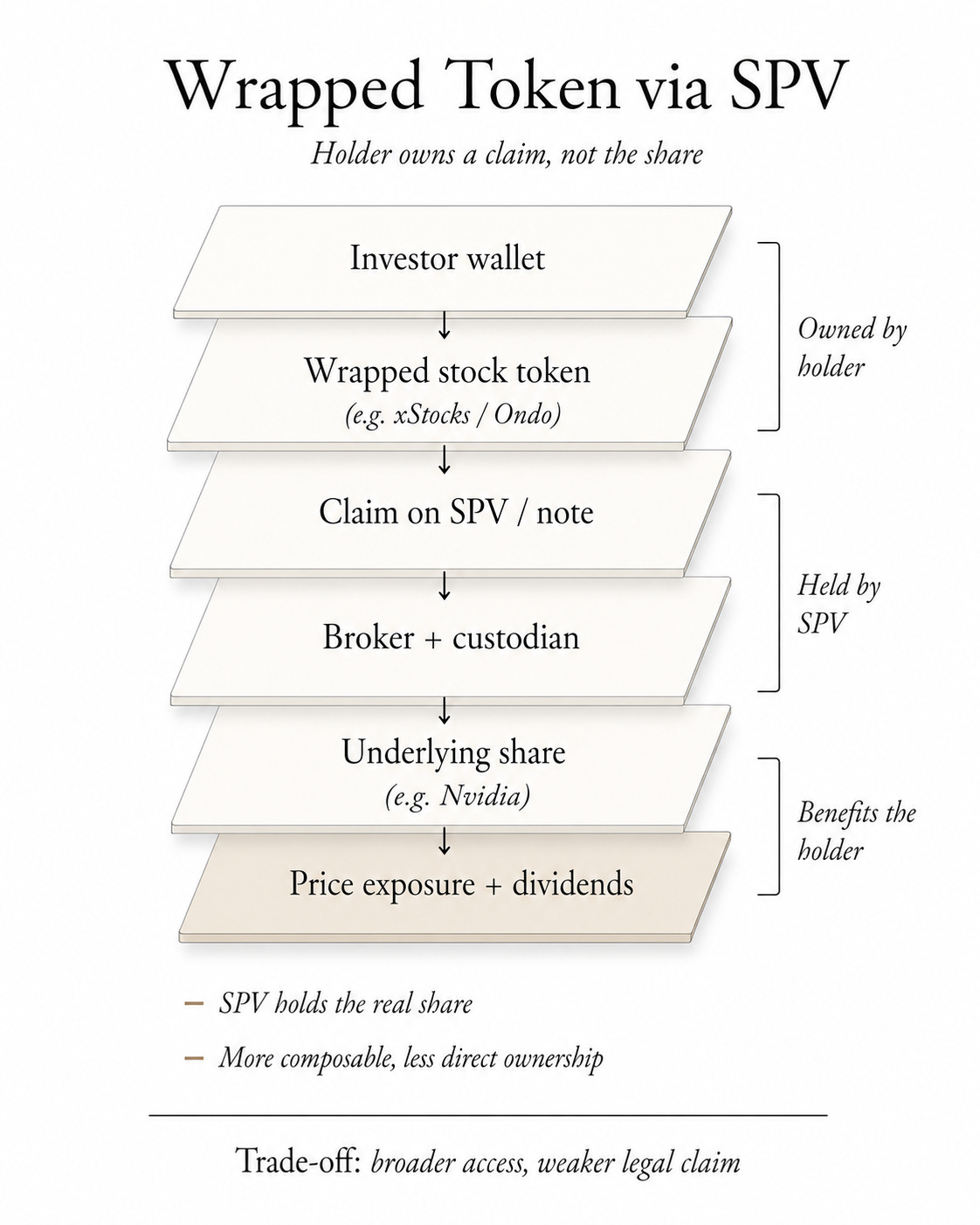

The second model trades some ownership for access.

xStocks by Backed issues tracker certificates for 160+ equities through a Jersey-based SPV (Special Purpose Vehicle), backed by 1:1 real shares. Ondo issues total-return notes for over 200 tokenised stocks through a British Virgin Islands-based SPV and has crossed $1 billion in TVL within eight months of its launch. Both offer economic exposure and dividend rebasing, in which dividends increase the holder’s token balance rather than being paid in cash.

The value of this model is in its composability. xStocks are collateral on Kamino and Morpho, and less than 24 hours ago, Ondo enabled 24x7 minting and redemption for its most popular tokenised stocks, making the primary market always-on.

The risk here is that you own only a claim on an SPV, not the shares. PreStocks showed what happens when that breaks. Its pre-IPO tokens collapsed in May 2026 after the underlying share transfers were called void, with $23 million backing over $1.3 trillion in implied valuation. Although Backed and Ondo mitigate this with segregated custody and proof of reserves, the risk does not disappear. It just shifts from the company to the wrapper.

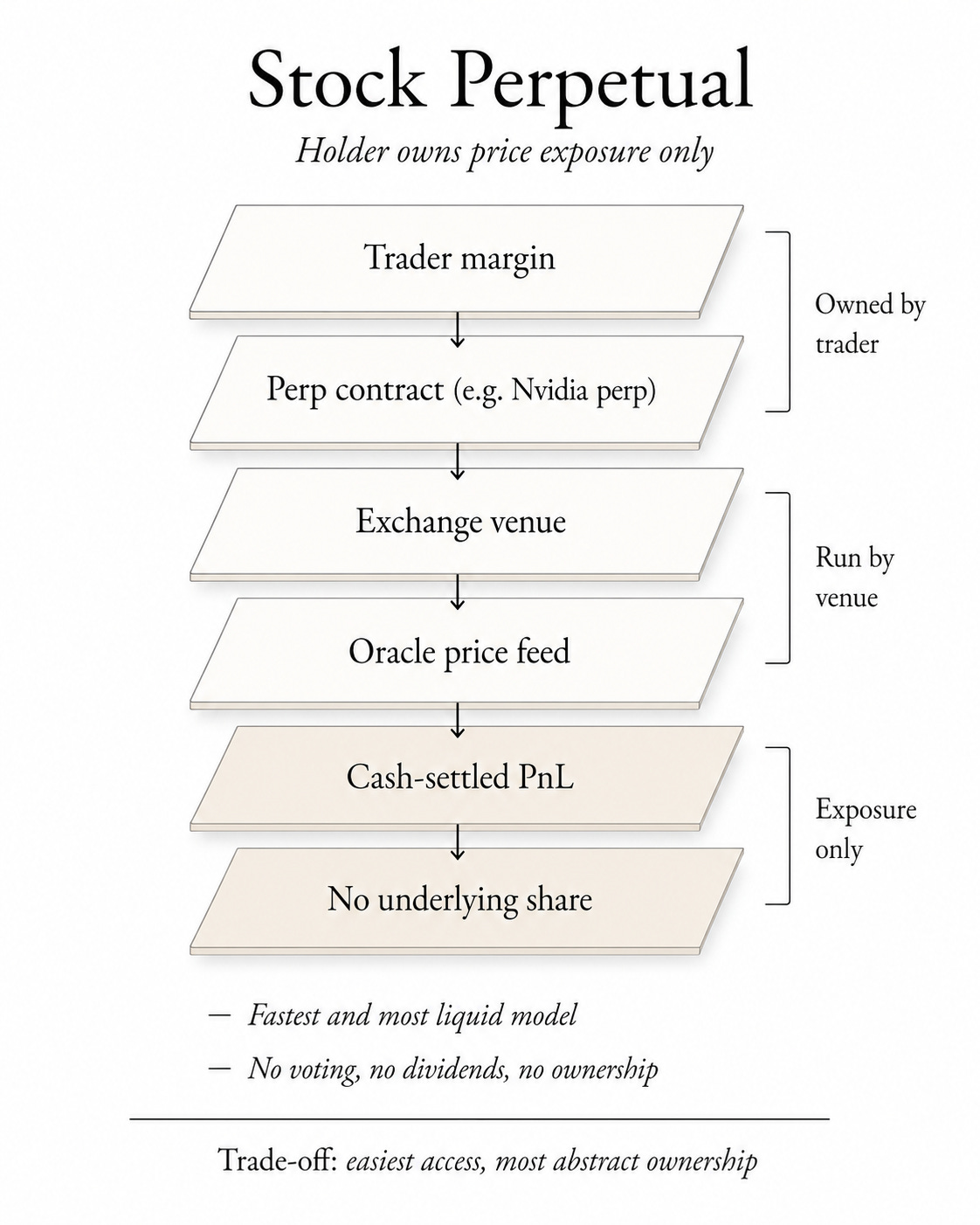

The third model abandons ownership entirely.

Hyperliquid’s HIP-3 framework lets anyone deploy a perpetual futures market with an oracle and a funding pool. TradeXYZ, the leading deployer with over 90% of HIP-3 open interest, runs perps on Nvidia, Tesla, Google, Amazon, and a Nasdaq-100-style index. Ostium on Arbitrum does the same.

The funding rate, which is paid hourly to balance long and short positions, keeps the price of the perp contract tethered to the spot price.

There’s a reason why perp trading outperforms spot trading by volume multiple times. Building a spot market for a stock requires an SPV, a broker-dealer, a custodian, and a proof-of-reserves regime. Building a perp market just needs an oracle to feed the price. TradeXYZ launched a SpaceX perp that hit $50 million in open interest before the company filed its S-1.

A wrapped tokenised product cannot move that fast because an SPV cannot source shares that fast.

The Role of a Token

Most retail shareholders never exercise the voting right that tokenised wrappers trade away. Research by the Harvard Law School Forum found that only 12% of the average firm’s retail accounts vote. For global traders who want exposure to blue-chip stocks like Nvidia, Google, SpaceX and Tesla, giving up a vote they would never cast is not a matter of concern.

The value of holding a tokenised stock on a blockchain is what you can do with the stock while you hold it. You can deposit your NVDAx or Superstate equity as collateral to borrow stablecoins on Kamino and Morpho. On Raydium, you can provide liquidity with xStocks in an automated market maker pool. A traditional brokerage account cannot offer any of these. The same stock, as a token on a blockchain, becomes a productive financial instrument. It can collateralise loans, earn trading fees, and compose with other DeFi protocols simultaneously.

For the perp trader, the value is different. There is no underlying asset to use as collateral, but leverage allows you to take a position with multiple times the capital deployed. Perps trade around the clock. When news breaks about Nvidia’s next-gen chip while the NYSE is closed, the perp market prices it in immediately. For directional traders, the always-on pricing is the main product.

The benefits of blockchain-enabled stock instruments come not as substitutes but as additions to what traditional, off-chain stock holding offers.

This is how the best financial assets have always behaved. They let the holder do more with them than just holding them. A treasury bond not only earns a coupon rate but also serves as collateral in the repo market. A share of stock is worth more than its price appreciation because it can be lent, margined, or used in a structured product. Blockchain does the same for tokenised stocks.

A tokenised stock is more than just a new kind of wrapper. Historically, the financial markets have evolved by creating layers of access to the same underlying value. Bonds, stocks, options, futures, and ETFs were all invented for different kinds of investors who wanted a different kind of exposure to the same economy. A pension fund sought a conservative yield. A retail investor wants price appreciation, while a hedge fund seeks leverage.

Tokenisation is another fintech evolution that changes who can access stocks and what they can do with them while they hold them.

Blockchain now allows fund houses, retail investors, and perp traders to gain exposure to the same Nvidia stock for different reasons. One might want to hold a registered share for governance, the other might want a wrapped token for composability, and the third might want a perp contract for leverage. But all three are valid expressions of their respective financial opinions.

The token can be the asset. It does not need to be the share.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.