Hello,

Over the past year, we have spent a lot of time at Token Dispatch writing about perpetual futures (perps) venues. Their rise to fame made it impossible to ignore them. Perps allow participants to price events close to their occurrence, with high leverage and deep liquidity available around the clock. Existing exchanges never offered that because of their constrained trading time and days. An 11-member team rode on this 24/7 trading pitch and made Hyperliquid the fastest-growing crypto exchange, with almost a billion dollars in annualised revenue.

Throughout 2025, perp trading volume averaged seven times that of spot trading. It seemed like a guaranteed way to build a sustainable business. So the inevitable happened: others jumped on the bandwagon.

Last week, the two largest prediction markets, Polymarket and Kalshi, announced perpetual futures and crypto trading within hours of each other. This comes just months after Hyperliquid said it’d launch event contracts. The convergence of perps and prediction market venues is a no-brainer. Everyone wants to be the everything exchange, and offer a one-stop shop that brings together attention, capital and leverage.

Three weeks ago, Saurabh wrote in a note on X about why Hyperliquid’s expansion into prediction markets will help the exchange take over finance. But is that true the other way round too? Can Polymarket and Kalshi’s moves be similarly rewarding?

Today, I will tell you all about it.

Why Perps Matter for PMs

Prediction markets have a stickiness problem. They are often cyclical and see record-level trading volumes when there are events to bet on. Just like we saw it during a U.S. Presidential election, a Super Bowl season, or an FOMC meeting.

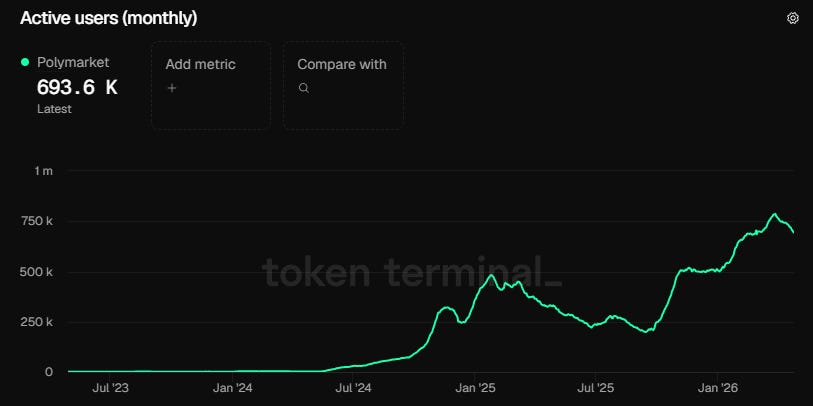

Polymarket’s monthly active users peaked at 321,500 in November 2024 during the U.S. Presidential Elections. Three weeks later, the number had dropped by 25% to 245,000.

However, with seasonal events, the monthly user count kept swinging in both directions.

In January 2025, it peaked at 500,000 users, then dropped below 200,000 in September. This tells us about Polymarket’s user-retention rate.

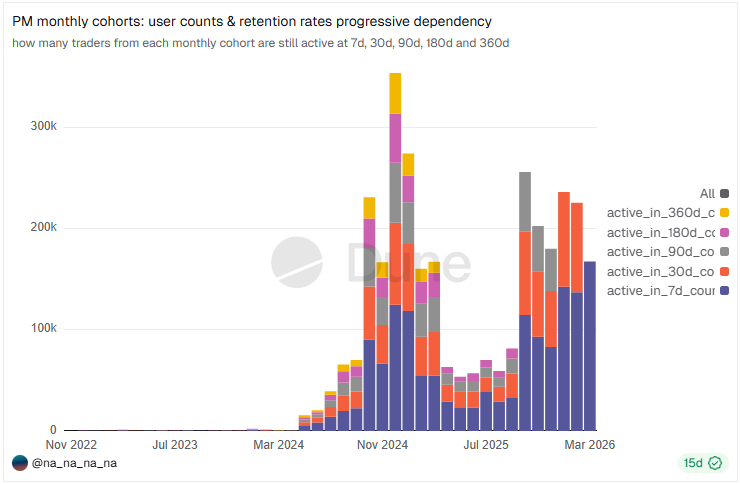

Dune’s cohort data shows that across every monthly cohort since 2024, only 8-11% of users are still trading a year after joining. About 75% of them vanish within 90 days. Users return for events and don’t necessarily find the platform sticky.

But that’s just part of the problem.

PMs also block capital until the issue is resolved. Perps are different. They price the event every second. It captures attention for extended periods and builds sustained engagement. It also makes economic sense for the PMs, since perps record far more trading volume and proportionally higher fee income.

In 2025, perps recorded over $60 trillion in notional trading volume, compared with $28 billion for PMs.

So, this adjacency expansion for PMs becomes a natural evolution. Platforms that capture one form of speculative intent often extend their reach to the next. They either build the capability or buy another player with that capability. We’ve seen this happen multiple times: Robinhood went from stocks to options to crypto to prediction markets (PMs). Coinbase acquired Deribit for a record $ 2.9 billion to venture into derivatives trading. Binance expanded from offering spot to futures to creating its native blockchain.

We see this often in the traditional world. A company expands the breadth of its services and hopes to cross-sell the new offerings to the same customers. It does two things: increases the average revenue per user (ARPU) and insulates the business from market cycles by diversifying reliance across multiple revenue streams.

In the early 1970s, the Chicago Board of Trade’s (CBOT) revenue from its commodity futures was dwindling. So they launched the Chicago Board Options Exchange (now known as Cboe) in what used to be a 4,000-square-foot smoking lounge of its parent company, CBOT. Both the products worked in sync because they needed a common infrastructure: risk management, clearing and a network of professionals who understood derivatives pricing.

But there’s a wide strait between wanting to run a perps venue and actually being able to execute one.

The Perps Stack

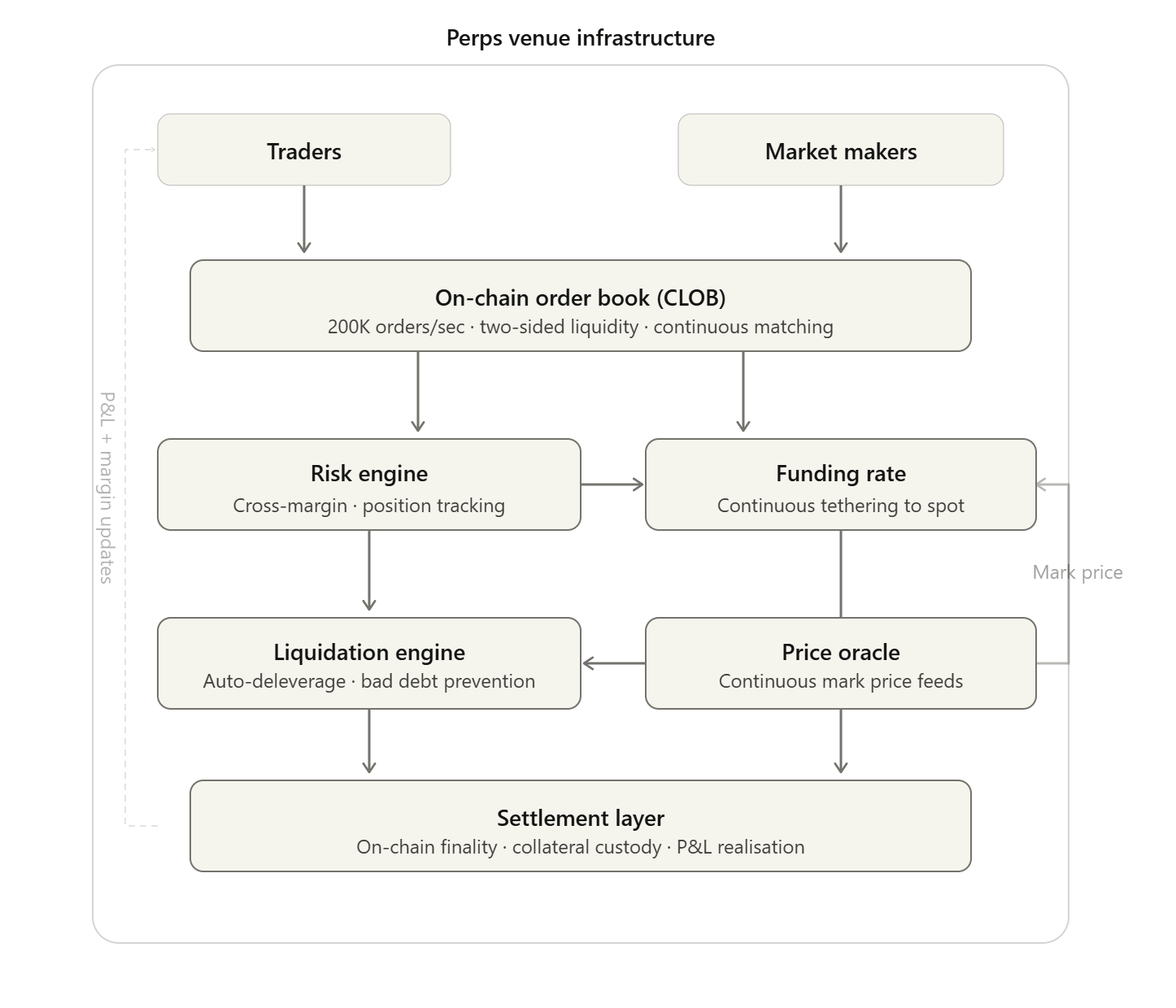

Running a perps exchange has too many moving parts. Let’s start with liquidity.

Hyperliquid processes over 200,000 orders per second through a fully on-chain order book. The perps venue clears over $6-7 billion in daily volume with two-sided market making. Lack of liquidity would lead to extreme volatility, wide bid-ask spreads, and high slippage. This makes it easy for whales to manipulate prices.

Second is the risk engine - the heart of any derivatives platform. It tracks every position and checks margin requirements on every order. When $19 billion were wiped out of the crypto market in October 2025, Hyperliquid processed billions in liquidations without downtime.

Then there’s the funding rate mechanism that keeps perps tethered to the spot price of the underlying asset. It runs continuously by settling small payments between long and short positions every few hours.

Building this entire stack isn’t the main problem. That I’m sure the prediction markets will manage to put together. The bigger problem is stress-testing that stack.

Hyperliquid built all this and stress-tested it in real-world scenarios, like the 10/10 crypto liquidation event and the U.S.-Israel-Iran war. It then launched event contracts via HIP-4 once the entire stack was in place to support that. Kalshi and Polymarket are trying to go the other way round. They have been running successful prediction markets that required none of the above stack in the first place. They are now going to fight for a share of the pie by not only competing alongside a highly successful Hyperliquid but also with an infrastructure that has not been stress-tested for the high-frequency activity seen in perpetual trading.

There’s a lot more stacked against PMs that makes the expansion to perps more difficult than the other way around.

The Hedging Synergy

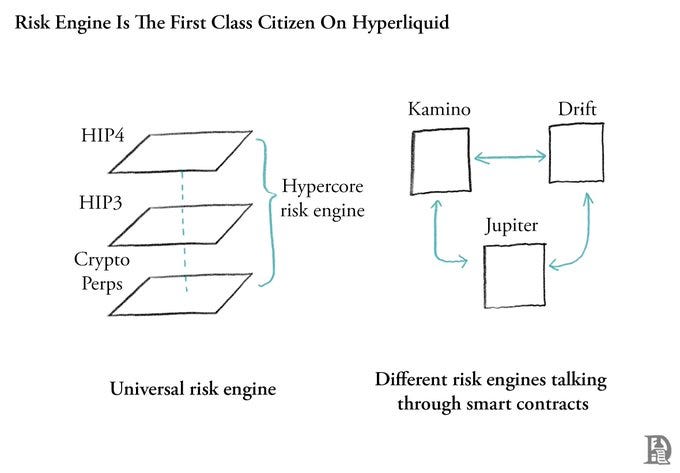

On Hyperliquid, the risk engine sees all your positions across perps, spot and, soon, event contracts. Saurabh explained this in his note on HIP-4.

It sees all your positions without differentiating between them. At the end of the day, the leverage you use and the margin you keep as cross-collateral determine at what point you get liquidated. A combination of positions across spot, perps, prediction markets or anything else determines how much margin you need to keep.

But Saurabh, aren’t other blockchains like Ethereum or Solana composable too? Of course, they are. On a general-purpose chain, every application runs its own risk engine inside its own smart contract. They cannot see each other’s state atomically. So, Kamino doesn’t understand what’s happening on Pacifica. Aave doesn’t understand what’s happening on Lighter. All applications are smart contracts on respective chains. Each app or smart contract has a separate risk engine, and making them all aware of each other, i.e., creating a universal risk engine, would require a massive collaborative effort.

This common risk engine solves a core money problem by optimising the same capital across multiple trades a trader makes on the venue.

Consider a trader on Hyperliquid who is long ETH at 5x leverage. The trader is worried about the Fed decision next week, so she buys an outcome contract that says “Fed holds rates steady” at $0.65. With a common risk engine, both positions are held in the same margin account. If the Fed surprises with a cut, ETH rallies, her perp profits and the outcome contract loses only what she paid. If the Fed holds the rates, the PM contract pays out and partially offsets any drawdown on her perp.

This is why a PM platform or a perp venue cannot be a mere add-on feature. This hedging possibility is what makes HIP-4 valuable on Hyperliquid. An average trader on the platform sees PMs as insurance cover in case their existing perps position flips over.

Currently, the collateral on Polymarket and Kalshi is locked until the event resolves. So, unless they offer a common risk engine across their perps and prediction markets venues, it loses a crucial catalyst that keeps traders on the platform. Right now, neither platform has announced cross-margining between their PM and perps venues.

The category breakdown and average trader profile on PMs raise further concerns about their ability to replicate their success in perps trading.

Over 80% of Kalshi’s total monthly trading volume occurs in the sports category. For Polymarket, that share was over 40% in 2025. Now, how would you create a continuous pricing mechanism for a perps venue around these sporting events? That takes away a big chunk of its traders out of the perps equation.

Additionally, an average Kalshi trader is a retail user who has never touched crypto and funds their PM account via ACH transfers from their bank account. So, even if I assume the theoretical possibility of cross-margining on Kalshi, I doubt that these traders have the sophistication required to double down on their positions on the platform and use perps as a hedging strategy.

What Could Work for PMs

There’s one scenario where I expect the bets to work if Kalshi and Polymarket do announce cross-margining. Their institutional partnership with prime brokerages and clearing firms can encourage high-value, frequent trading activity across event contracts and perpetual futures.

It would let institutional desks treat PMs as part of a broader risk management toolkit.

Both Kalshi and Polymarket can boast about partnerships that will give them access to institutional clients.

Kalshi’s tie-up with FIS and Tradeweb data, and Polymarket’s deals with Intercontinental Exchange (ICE) could help retain institutional clients who value hedging their prediction market positions with perpetual contracts on the same platform.

That’s still a far-fetched wedge that rests on many things going right for both the prediction markets. They need to set up stress-tested infrastructure, ink partnerships and show their clients that their platforms can help optimise capital.

But this is what it takes for them to survive a cut-throat competition. With the distribution wedge already with Hyperliquid, they have no other choice but to maximise their chances elsewhere.

That’s it for today. I will be back with another deep dive.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.