Hello,

When Warren Buffett took over Berkshire Hathaway in 1965, he began writing letters to the shareholders of a dying textile mill. In them, he explained in detail where the cash from the mill was being redeployed and why.

Capital allocation became a public affair in a true sense. Despite being owners of a company, shareholders generally trust the management to carry out operations as their fiduciary agents. Buffett’s letters made shareholders feel heard in annual discussions around what the business should become.

Most public companies do capital budgeting in closed boardrooms. Corporate law mandates the disclosure of audited numbers, not the reasoning behind the decisions. But Berkshire’s transparency with reasoning was timely and crucial. Sixty years of letters read like a continuous conversation about where to put the money next.

A version of this practice is now showing up on-chain.

DeFi protocols have their own versions of these boardrooms: backchannels, founder calls, and delegate huddles. Yet the vote, the proposal text, the dissent, the amendments, and the final proposal all rest on the public record.

On April 12, Aave’s token holders voted on a $25 million capital allocation proposal. The vote, which passed with a landslide majority, allows Aave’s token holders to vote on governance, protocol upgrades, and risk parameters.

Beyond Aave, this move helps crypto evolve from debating whether a token has a claim on protocol cash flow to allowing token holders to decide which project to fund next and how much capital to allocate.

In today’s analysis, I will tell you how.

What’s in the Vote?

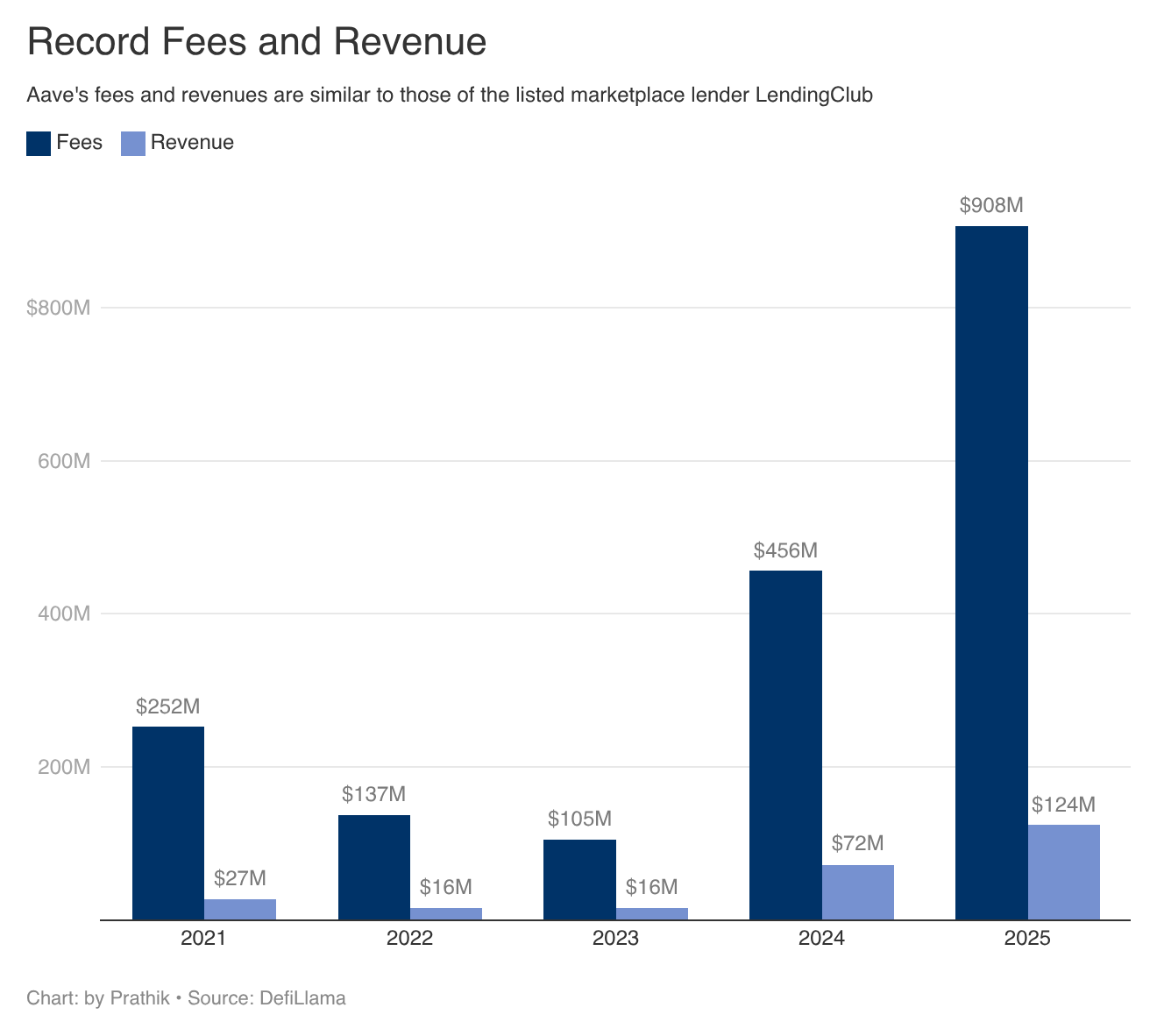

Aave’s vote matters because of its relevance in the lending marketplace. Aave currently has over $26 billion in total value locked (TVL) and generated about $907 million in fees last year. Most of that flows to suppliers who earn interest on deposits, leaving around $125 million in annual revenue with the protocol. That’s what accrues to the DAO treasury.

As of December 31, 2025, Aave held over $21 billion worth of active loans on its books.

That’s a larger borrow book than Robinhood’s $16.8 billion margin book at the end of 2025, and nearly twice the size of LendingClub’s $11.8 billion in total assets. The latter is a NYSE-listed marketplace lender whose business model most resembles Aave’s.

In 2025, LendingClub, an NYSE-listed marketplace lender with which Aave’s economic model resembles the most, recorded $136 million in net income on a revenue base of a billion dollars. The two-decade-old company closed 2025 with $11.8 billion in total assets. This is a business competing with well-known traditional fintech peers.

LendingClub made $136 million in net income on a $1 billion revenue base in 2025. Aave’s $125 million accrues to the DAO on a loan book nearly twice as large, which means LendingClub earns roughly twice as much per dollar lent.

That’s because Aave is just a protocol. It can’t charge more interest without breaking its own market since it doesn’t own the deposits. Raising the reserve factor would push suppliers to a rival protocol with better yields. LendingClub can charge more because it owns the loans, takes the credit risk, and funds a full bank of underwriters and default provisions to do so.

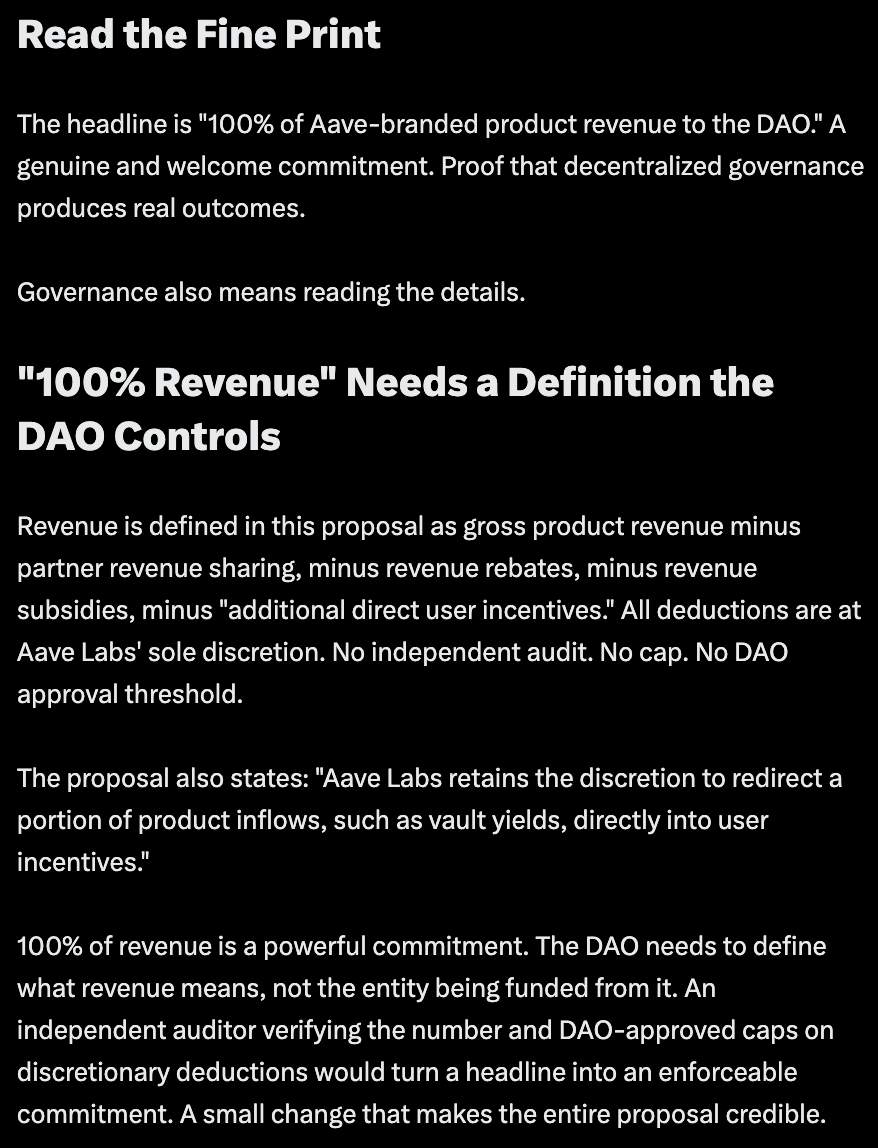

Aave’s proposal is to route all revenue from Aave-branded products, including the App, the Card, and the Pro institutional tier, to Aave DAO’s treasury. In return, the DAO will pay Aave Labs $25 million plus 75,000 AAVE, to be vested over four years, to keep building.

Aave Labs, which is the development entity behind the Aave protocol, had been keeping a share of product revenue to fund itself. The Cowswap integration on Aave.com applied a 15-25 basis point fee on swaps and sent proceeds totalling roughly $10 million a year, or about 10% of the DAO’s potential revenue, to a private Labs address. ACI's Marc Zeller called it the "stealth privatisation" of the DAO's earnings. Under the new structure, it will be paid by its token holders, on terms they set and against milestones they can withhold disbursements against.

Token holders didn’t approve the ‘Temp Check’ version that was initially proposed in early March. They split the bundle involving the V4, brand, funding, and growth grants into separate votes and stretched vesting from two years to four. They also tied disbursements to milestones instead of writing a single cheque.

Not everyone supported the initial version. Some agreed to the negotiated version, others walked away after a long association.

In the past two months, three of Aave’s most embedded contributor organisations ended their partnership with the protocol. BGD Labs left in February. Aave Chan Initiative (ACI) announced its exit from Aave in March after contributing 61% of governance actions and 48% of protocol income during its three-year tenure. Chaos Labs stepped down from risk management on April 6, after helping scale TVL from $5.2 billion to over $26 billion without material bad debt.

The bigger shift is that large protocols with product-market fit and surplus are now enabling token holders do what public markets typically confine to boardrooms.

Uniswap is moving in the same direction from a different angle. Its UNIfication proposal hinges on protocol fees, routes them into UNI burns, disables Labs-level interface and wallet fees, and funds Labs from the treasury.

In 2025, Uniswap recorded $1 billion in fees, nearly identical to Aave. But almost all of it has historically gone to liquidity providers. Its current annualised protocol revenue stands at $42 million. UNI holders got nothing.

In March alone, Uniswap processed $42 billion in DEX volume. Meanwhile, Robinhood’s app recorded $34 billion in crypto notional volume throughout Q4 2025. Uniswap is doing slightly more than that in just a month.

Two of DeFi’s most-watched protocols are moving toward the same structural move, albeit with different mechanisms. Both of them want to route revenue up to the token layer and then publicly decide where to redeploy it.

The new treasury strategies change who decides how revenue is redistributed once it reaches a treasury. Should the funds be deployed to buy back and burn the tokens? Or deploy them for operating budgets and growth grants? Maybe fund new product lines or save it for a longer runway? All these are capital allocation questions. The same thing that Buffett was answering in his letters for decades.

For years, DeFi has argued whether the token deserves a claim on protocol cash flows. We saw Hyperliquid and pump.fun settle that conversation through their extensive planned buyback programmes.

Read: Burn, Baby, Burn 🔥

What Public Capital Budgeting Requires

Buffett’s letters were voluntary. What makes his act seem more than just a goodwill gesture is the audited financials that back the letters. He had a fiduciary duty that’s enforceable in court. Berkshire shareholders have rights that don’t depend on Buffett’s goodwill; they can sue the company, vote out the board and demand records.

A corporate regulator mandates baseline disclosure regardless of how nice Buffett’s letters might sound.

With DeFi, transparency takes the front seat. On-chain architecture forces every transaction, treasury movement and vote to be public. But that’s not enough to make crypto protocols transparent to the public. Token holders need a collective understanding of the business to make capital budgeting decisions.

The financial statements and filings of publicly listed companies are accessible and legible to the public because of standardised accounting requirements. What Nvidia means by gross revenue is about the same as what Apple might mean. If you can make sense of Nvidia’s balance sheet, you will likely understand the line items in the iPhone-maker’s financial statements, too.

But this standardisation of financial terms is mostly absent in crypto protocols. Terms like revenue and fees are often used interchangeably, while they may mean different things.

Token holders may still read the Aave treasury balance sheet to the cent. But they cannot separate what counts as “Aave-branded product revenue” unless the definitions are standardised. They still need to know what happens if Aave Labs and the DAO disagree on the number.

This isn’t hypothetical. One of the biggest criticisms of Aave’s proposal was on what “100% of revenue” actually meant. Is it gross or net of operational costs? Who verifies it? How do you enforce it?

Even Marc Zeller, the founder of the now-exited ACI, raised these concerns in his X post after acknowledging Aave DAO’s win.

As token holders, you simply cannot allocate what you cannot define.

Checks and Balances

Although the vote signals a transfer of power to the token holders, those who left Aave argue that the transfer is incomplete.

The two teams closest to Aave’s governance machinery, one that coordinated 61% of all governance actions (ACI) and one that wrote the production codebase (BGD Labs), complained about similar things. The entity asking for the money, Aave Labs, was also the one voting to approve it. That’s a conflict of interest.

A budget recipient cannot vote on its own funding.

This is a structural problem in every on-chain capital budget in which founders or core teams hold large token positions. Although theoretically, it’s the token holders who get to decide where the surplus goes, it’s often the largest tokenholder who drafts the proposal.

You may argue that a larger stake brings a larger say in how the company is operated. But if DeFi protocols want to emulate the capital budgeting practices of public companies, they need to ensure similar checks and balances. For instance, minority shareholders are protected against abuse by majority shareholders through legal frameworks.

DeFi needs similar checks and balances. Revenue numbers must be independently verified, including those off-chain. When Venice AI said it would burn VVV using Stripe subscription revenue, DefiLlama’s 0xngmi asked for read-only Stripe access so the off-chain numbers feeding an on-chain claim could actually be audited.

There must be on-chain milestones that trigger capital releases in tranches and reverse them if the milestones aren’t met. Protocols must standardise the disclosure of voting power held by entities that will receive the DAO funds. None of this is hard to achieve. It’s just not desirable because the people who have to agree to be constrained are the same ones writing these proposals.

One team had specifically requested safeguards to ensure on-chain milestone tracking and self-voting limits before supporting the Aave proposal. Those recommendations were ignored, and the proposal was passed anyway.

What Aave’s ‘Win’ Means

The vote itself is not the achievement. Passing a $25 million funding proposal on-chain is not hard when the largest token holder supports it. But there’s a lesson to be learned here.

Token holders rejected the first version. They broke a single mega-proposal into smaller decisions. They doubled the vesting period. They forced a founder-led entity to negotiate terms in public, revise them in public, and accept constraints it didn’t volunteer. This is a step toward achieving capital budgeting in public.

If Aave’s proposal becomes a template, the fact that token holders can reshape a proposal before it passes must become the part that every other protocol copies. Just like in a democracy, a policy isn’t sound enough if it can’t see the light through all dissent and disagreements. Pushback in DAOs is not a dysfunction. It’s what makes DAOs more transparent and stand the test of time.

Uniswap’s UNIfication proposal is going through a similar journey. It needs to address similar questions, such as “Who decides where to allocate the treasury funds?” What is the recourse if something doesn’t work?” These are the questions many other blue-chip DeFi protocols will face. They must understand that the DAO community will not remember buybacks or token burns if the policy decisions are not justified and grounded in reason.

Buffett and Berkshire came to be respected not right after the first letter. Shareholders read years of letters before they gradually trusted the entrepreneur to judiciously apply their funds to profitable use.

That’s it for today. I will be back with another deep dive.

Until then, stay curious!

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.