Hello,

In the late 1960s, Wall Street had an unsexy problem. Trading activity surged as securities became more popular, but the infrastructure supporting it remained outdated. Brokers settled trades by physically swapping share certificates. Messengers ran around Manhattan with envelopes. Back offices drowned in forms. The volume surge got so bad at one point that U.S. markets had to stop trading on Wednesdays for six months just to allow firms to catch up on their paperwork.

All this culminated in the infamous Paperwork Crisis.

Better “runners” or more papers was not the solution. So they replaced all the moving things with the Depository Trust Company (DTC) in 1973. The corporation immobilised securities and made ownership a ledger update rather than a physical handoff of share certificates. The modern U.S. market we see and trade in today is the result of multiple iterations that evolved over time from that decision.

Today, DTC holds custody of more than 1.4 million security issues valued at $87.1 trillion, including securities issued in the U.S. and over 130 other countries and territories.

We see a similar narrative playing out in the history of finance. When an asset class becomes big and popular enough, what helped manage it wasn’t merely a book-entry strategy. The underlying force behind it has always been trust. After the DTC was launched, an average investor no longer had to worry about ownership, as trust in the centralised body’s ability to maintain records replaced the need for a physical certificate.

The same problem has surfaced with crypto, as its appeal as a mainstream asset rose in the U.S., driven by exchange-traded funds (ETFs) and other forms of exposure (think Digital Asset Treasuries) over the past two years.

This development has caused back offices to spring into action, just as the 1960s’ paperwork crisis did for the DTC.

The “paper” in crypto is the private key, which is more like a bearer instrument - whoever controls the key, controls the asset. This creates a familiar set of problems for institutions to address: operational controls, segregation, auditability, insolvency questions, governance, and the fact that losing a key is a permanent loss.

Now, a new trust layer is being built around these challenges through a trust bank charter. In today’s story, I will explain why firms are lining up for bank charters to custody crypto.

The Charter Rush

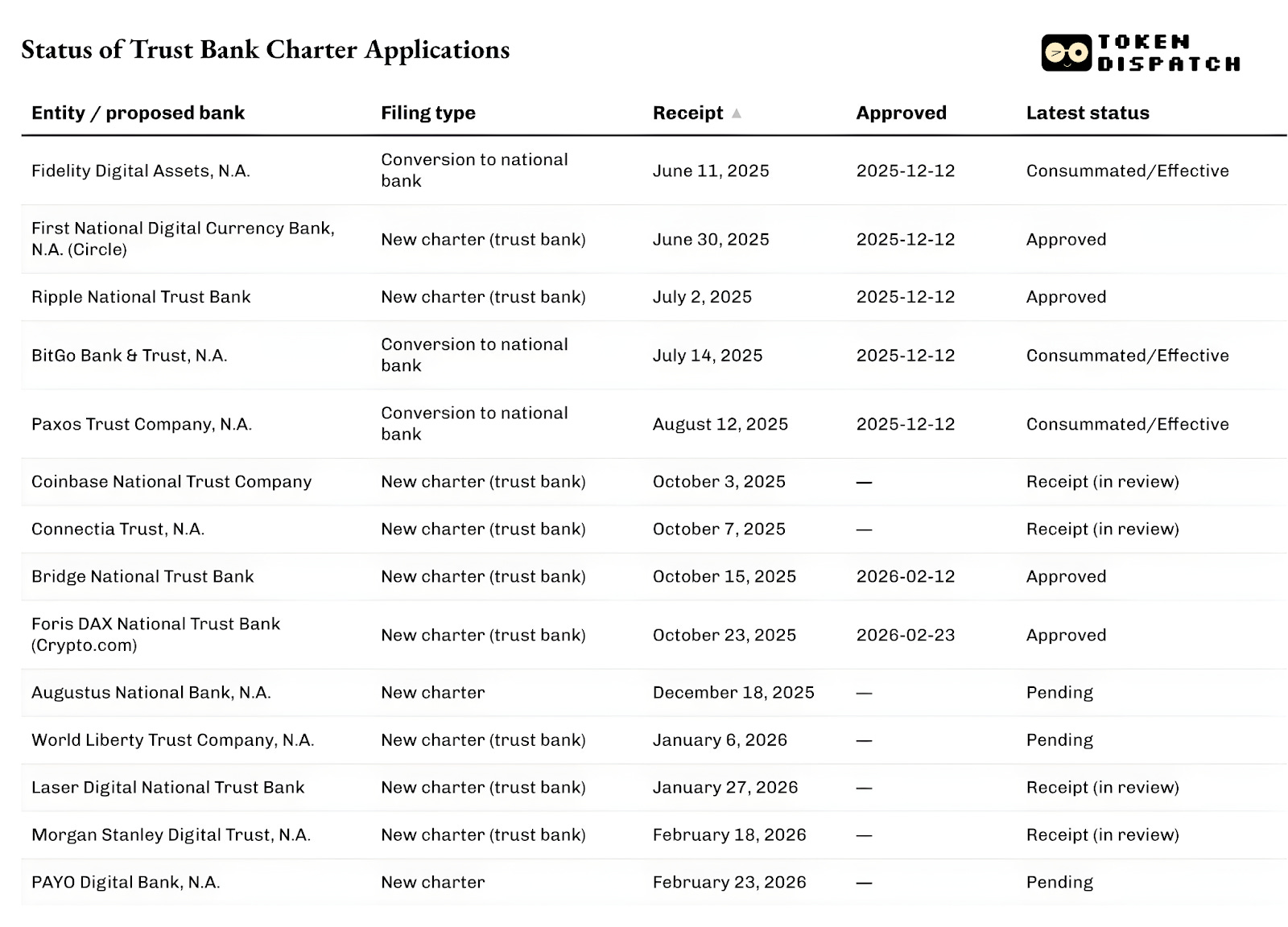

In recent months, the U.S. Office of the Comptroller of the Currency (OCC) has been approving and processing a growing number of applications to become national trust banks tied to digital asset custody and stablecoin infrastructure.

On December 12, 2025, the OCC conditionally approved five such applications, including Circle’s First National Digital Currency Bank, Ripple National Trust Bank, and conversions for BitGo, Fidelity Digital Assets and Paxos. This was followed by Stripe’s crypto unit, Bridge, and Crypto.com getting the initial nods from the OCC in February 2026.

The queue isn’t just limited to crypto natives.

Last week, the world’s largest wealth management firm, Morgan Stanley, applied for a trust bank charter called Morgan Stanley Digital Trust, National Association.

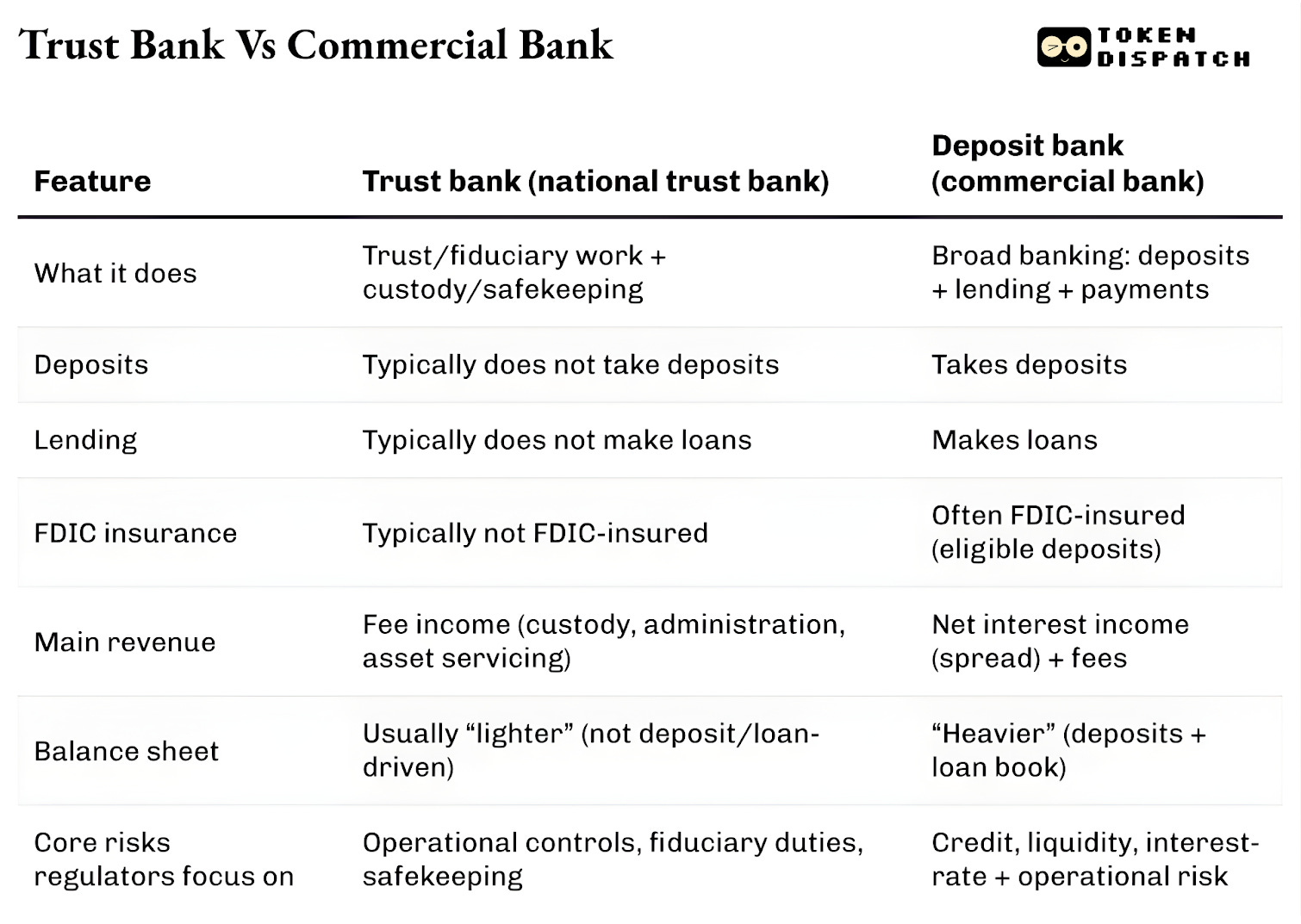

Know what’s common in these applications? They weren’t queuing up to become a normal bank, running deposit and lending activities. Unlike normal banks, these national trust banks cannot accept deposits or make loans and do not have FDIC insurance. They all had applied to offer custodial, safekeeping and fiduciary administration services. Think of bookkeeping, but specifically for crypto assets.

I find this to be one of the most pronounced signs that crypto is changing how traditional financial institutions function, while the rest of the world is busy focusing on the sideways movement of cryptocurrency prices.

Banking charters may sound boring, but like many other financial infrastructure innovations, they bring our attention back to the lesson the financial world learnt from the paperwork crisis. It also emphasises that, at its core, the mainstreaming of crypto is a custody-and-controls story.

Why Now?

The rush to apply for charters is linked to recent clarifications from the OCC about what national banks can do in crypto-related custody. In May 2025, it confirmed that national banks and federal savings associations may buy and sell assets held in custody at a customer’s direction.

In December 2025, it also confirmed that banks can conduct “riskless principal” crypto transactions by acting as intermediaries without holding inventory.

Last week, on February 27, 2026, the OCC clarified that national trust banks can engage in non-fiduciary activities beyond their narrow fiduciary role, starting April 1, 2026.

Why does this matter? It is critical if you are a firm building custody, settlement, reserve management, and related services.

We have seen it happen before in the world of finance.

In the early 2010s, neobanks emerged when a crop of fintechs built apps on top of partner banks. While these apps made banking more accessible, they had their problems. Although the apps owned the interface, partner banks still owned the deposits, infrastructure, and regulatory attention. It became messy when something went wrong because accountability was split across multiple entities.

The response was the same that we see now with crypto: take control of the risk and reward.

In 2016, the OCC began exploring special-purpose national bank charters for fintech firms. Two years later, it started accepting charter applications from non-depository fintechs engaged in core banking functions.

While courts struck down the possibility of issuing charters to non-depository institutions, fintechs nevertheless went ahead to reduce their reliance on partner banks. What followed was a handful of fintechs becoming full-service banks through the traditional, heavier route, which sometimes included acquisitions.

Varo, which started as a fintech, received its full-service national bank charter in 2020. Jiko became a bank by acquiring a small national bank. SoFi received conditional approval in 2022 to become a full-service national bank by acquiring an existing national bank.

The national trust bank charter rush we see today follows a similar pattern, except this time, Washington is also laying a fresh set of guardrails for digital assets.

The legislative backdrop to all these developments makes it clearer why firms are pursuing more than just custodial services within the digital asset landscape under their national trust bank charter applications.

In July 2025, U.S. President Donald Trump signed the GENIUS Act, establishing a federal framework for payment stablecoins. Several firms pursuing trust bank structures have explicitly stated their intention to operate stablecoin and reserve-related activities within a federal oversight regime aligned with that law.

Both Bridge and Circle mentioned this in their announcements.

This addresses the first layer of ‘why now’. The regulatory clarity opens new value chains for incumbents, both traditional and crypto-native, enabling them to expand their business lines.

The second layer involves the market structure.

Institutional crypto exposure has shifted toward wrappers that resemble legacy finance. Think of ETFs, funds, and managed accounts. These wrappers demand custodians who clear legal and operational thresholds.

You’d be mistaken to think centralised crypto exposure is no longer in demand. This is evident in the developments within the current crypto ETF infrastructure.

In April 2025, the world’s largest asset and crypto fund manager, BlackRock, added Anchorage Digital Bank as an additional Bitcoin custodian alongside their existing partnership with Coinbase for its iShares Bitcoin Trust. BlackRock framed it as part of “ongoing risk management” to address the growing retail and institutional demand.

What value do financial giants, such as the $9-trillion Morgan Stanley, see in these charters?

One of the most recent signs came less than two weeks ago in a fireside chat at the Bitcoin For Corporations conference. When Phong Le, Strategy’s (fka MicroStrategy) chief executive officer, said, “If there’s somebody that could help ‘orange pill’ the world, it would be Morgan Stanley,” Amy Oldenburg, Morgan Stanley’s head of digital assets strategy, replied, “That would probably be accurate.”

What Changes?

Once you string these developments together, the trust charter rush no longer looks like a crypto story and resembles the evolution we saw with the DTC.

As crypto evolves as a financial asset, both retail and institutional investors need a place to store their keys, one that lawyers, auditors, and regulators can approve. A national trust bank charter is one way to address that at scale.

Then there is the question of the business line’s economics. Custody may seem like a small-fee business. Starting Q1 2025, Coinbase stopped disclosing custodial fee revenue as a separate line item and has rolled it into “Other subscription and services revenue.” Yet, there’s more to the custody business than meets the eye.

Whoever has custody controls collateral, which in turn addresses financing for these institutions. Financing controls leverage, which controls volume. Ultimately, volume decides how much one gets paid.

In 2025, EquiLend’s Data & Analytics said global securities lending revenue hit $15.3 billion, with loan balances topping $4 trillion. State Street, a giant in custody, reported $13.94 billion in total revenue in 2025. Of that, its servicing revenue accounted for ~40% ($5.32 billion), which included custody, accounting and fund administration, recordkeeping, and client reporting.

So, while custody alone may not translate into a material revenue line, the ancillary services around custody could generate repeatable revenue pools.

The DTC became irreplaceable because it allowed the market to scale without drowning in paperwork. Today, DTC has evolved to become more than just safekeeping; it offers settlement services, processes corporate actions and supports underwriting. This has become a whole ecosystem built around updating ownership records.

A licence to crypto custody can unlock something similar for these applicants. Beyond becoming a vault, they can provide an authorised ledger interface.

The charter allows these institutions to lend credibility to their clients in how they record, segregate, transfer, and audit the ownership of digital assets. They can do so with a lighter balance sheet and a more focused approach without becoming a deposit-accepting bank.

But trust charters have their share of critics.

Traditional banking advocates have argued that these charters can serve as a “backdoor” into the banking system without taking deposits or incurring the same broad public obligations. Banks are fighting over where the line should be drawn.

While the debate continues, the regulatory shift is well underway. The OCC’s conditional approvals may not equate to a final nod, but they signal one thing. It’s that crypto, despite its self-custody ideology, has now grown large enough to make the back-office role indispensable.

I think it would be a misreading if the industry looked at the trust bank charter rush and called it a crypto industry phenomenon. It is more of a natural evolution of market players who are always on the lookout for ways to create value by solving industry inefficiencies.

That’s it for today. I will be back with another analysis.

Until then, stay curious!

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 200,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.