Hello,

Meta is building a data centre in Louisiana to run its AI workloads. To finance its costs, they set up a subsidiary and loaded it with debt. Pimco took on that debt, repackaging it into $30 billion in bonds that will mature in 2049 and placing them with pension funds, insurance companies, and retirement advisors. But the problem now is that the GPUs inside these data centres become e-waste within four years. People’s retirement money is being used to back hardware that will be obsolete even before the bonds mature.

In last week’s piece, I showed how GPU compute is becoming a tradable commodity with its own pricing indices and futures contracts. Companies are borrowing billions of dollars to build GPU clusters and selling capacity in advance to lock in revenue. Still, there is no public way to verify whether the same rack has been pledged to multiple lenders or to check its real utilisation.

Today, I will dig deeper into the financial layer, and how computing is actually being financed, and how they are pricing the risk and lending against it.

")

The Compute Lending Structure

So the question is, how do you lend against hardware that will be obsolete in four years?

The Meta deal is a good example of how the structure works. A data centre is built and then filled with GPUs worth approximately $27 billion. A lender puts most of the capital; in Meta’s case, it was Blue Owl. After this, Meta signs a take-or-pay contract, meaning it commits to pay a fixed rate for the compute capacity the facility produces over the full term of the financing, whether or not it actually uses the GPUs.

The lender here is betting entirely that Meta will continue making those payments, and as long as it does, the lender gets repaid regardless of what happens to the chips underneath. Pimco then takes that $27 billion in loans, repackages them into $30 billion in bonds, and places them with pension funds and insurance companies.

Every major GPU financing deal is structured the same way: the credit decision sits on the customer’s balance sheet, and the hardware comes second. CoreWeave, which builds GPU clusters that companies like Microsoft and Meta rent for AI workloads, has used this approach eight times now. Their latest facility raised $8.5 billion on this model.

And this approach isn’t new. Wall Street used this trick for mortgages twenty years ago, and it ended in one of the worst financial crises since the Depression. For the CDO machines of the 2000s, rating agencies did not examine the individual mortgages within a CDO; instead, they focused on the legal wrapper, assuming the mortgages would fail independently of one another.

Think of it like insuring a hundred houses spread across the country; each of them looks fine individually because a fire in Texas would not cause a fire in Maine. But what if all one hundred houses are in the same flood zone? When the flood comes, every single one will file a claim at the same time, and the insurer will be wiped out. The agencies assumed the mortgages were spread out across neighbourhoods. But when the housing crash occurred in 2008, prices dropped everywhere at once, and the safe layers that pension funds had been buying turned out to be the most exposed.

This is exactly what these GPU-backed SPVs are doing: lenders take a complex, rapidly depreciating physical asset that nobody can reliably price, wrap it in a legal structure from an investment-grade counterparty, and produce a debt instrument that pension funds and insurance companies can buy.

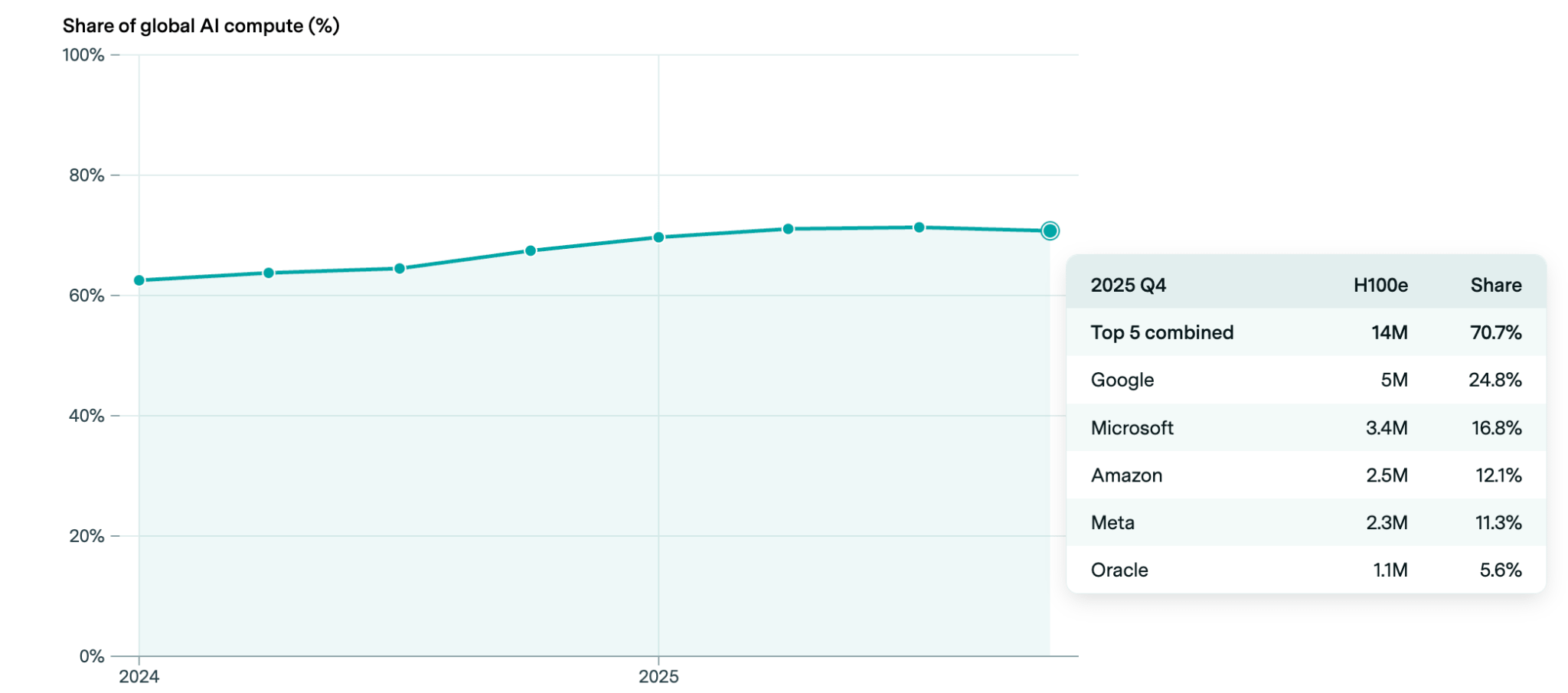

But GPUs are worse than mortgages because every single GPU in these financing vehicles depreciates with Nvidia’s product release cycle. When Nvidia ships a new generation, every chip from the previous one loses value on the same day. And every one of these deals depends on a handful of buyers. Five hyperscalers account for 70% of all AI compute demand, and their capex budgets are the only variable that determines whether these contracts will be renewed.

Mortgage defaults at least had geographical variation — a housing crash in Florida didn’t automatically trigger one in Oregon; GPUs have no such cushioning, and yet lenders are still underwriting every one of these deals as if the risks are independent of each other.

The biggest counterargument to this is that depreciation doesn’t matter as long as the customer’s contract repays the full loan amount before the GPU becomes obsolete, which might be true at the individual-deal level. But that also puts the operator on a non-stop treadmill, where every new GPU generation that makes the current lending ‘safe’ also forces the operator to raise fresh debt for the next one. Nvidia has recently moved to a one-year product cycle, which only makes the treadmill faster. The whole market is making the same bets, just through separate legal entities that need to be renewed every year.

The rating agencies understand this well. Estimates on such new hardware are meaningless, which is why they price the contract rather than the chip.

But Can You Verify & Price the Chips?

Pricing the contract solves the lender’s immediate problem, but the underlying problems remain untouched. If no one is checking the chips, does that mean no one can tell whether those chips actually exist? If yes, are the chips running? What’s the utilisation so far? And what if the same chips have been pledged to multiple lenders?

None of these questions can be answered without verifying the underlying asset. The verification problem has a long history in commodity markets. In 1963, a vegetable oil trader in Bayonne, New Jersey, convinced banks he had 900K tons of salad oil stored in tanks in his facility. When the inspectors checked the tanks, they found them full, but with water at the bottom and only a thin layer of oil on the surface. Banks had lent this trader $180 million against warehouse receipts for oil that did not even exist. The shortage turned out to be 1.8 billion pounds, causing two brokerage firms to collapse and nearly bringing down American Express.

Fifty years later, it happened again in Qingdao, when a Chinese trading firm used duplicate warehouse receipts to pledge the same metal to multiple banks simultaneously. A single batch was pledged an average of ten times. And it was only discovered when a Communist Party corruption probe caught the company’s chairman.

Nearly every physical-asset market that scales fast enough eventually produces this kind of fraud. The documents suggest that the collateral exists, but because no one verifies its physical reality, companies misuse it to make multiple claims against the same asset. The current verification infrastructure for GPU-backed lending has the same leaks. In traditional lending, when a bank finances a physical asset, it files a public notice claiming the asset as collateral so other banks can verify it before lending against the same asset again.

In the US, this runs through UCC filings, but these filings often contain errors. A study of the Florida system found that nearly a third of all filings there were legally void because of typos in the borrower’s name. A single wrong character can easily erase the lender’s entire claim.

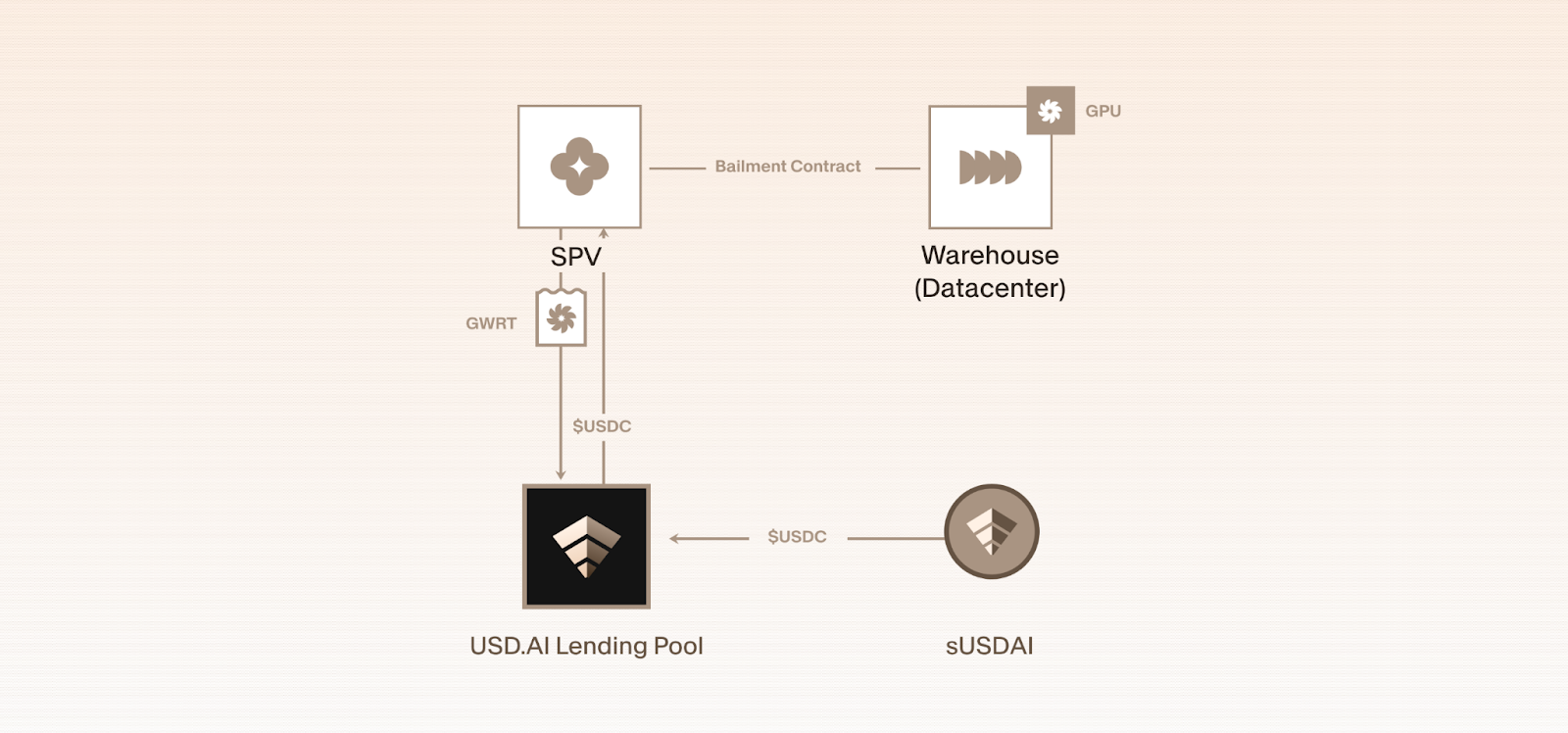

Now imagine an on-chain version of this registry, which is immutable and resistant to those errors, designed specifically for GPU financing. USD.AI, for example, has built a system that turns any physical GPU into a tokenised financial instrument with real legal enforceability.

The borrower can sell the hardware to a tokenising agent, who creates an NFT that functions as a digital deed of ownership under UCC Article 7, the same law that governs warehouse receipts for physical commodities such as oil and copper. This NFT gives the holder a legally enforceable claim to the physical GPU, just as a warehouse receipt gives its holder a claim to metal in a vault.

The borrower gets the NFT back under a bailment agreement that lets them operate the hardware while it serves as collateral for an on-chain loan. These loans are set up inside bankruptcy-remote Delaware SPVs with perfected liens. The hardware is also monitored in real-time, and the default triggers are hardcoded into the smart contract itself. This means if telemetry ever goes dark for more than 24 hours or if a hardware attestation check fails, the contract freezes the position and routes it into a liquidation waterfall.

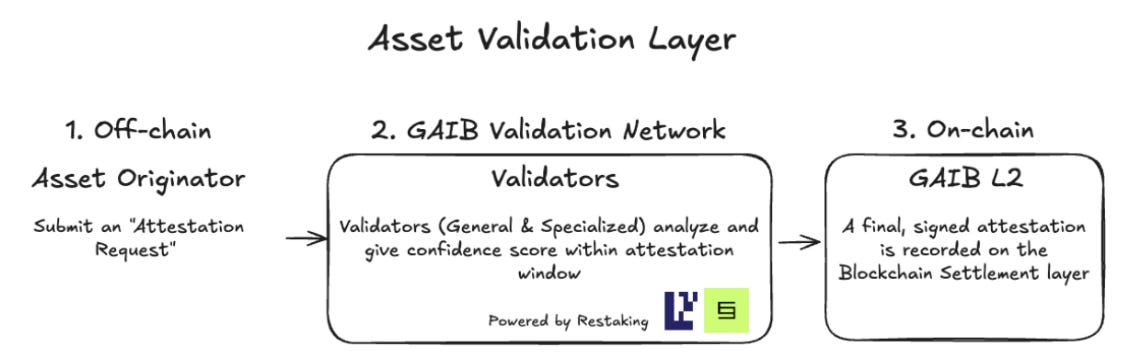

Another protocol, GAIB, takes verification even further by continuously running several cryptographic proofs. It verifies that the hardware is where the borrower says it is, confirms whether it has been moved or swapped, and checks that the GPU is actually running compute jobs and generating revenue.

Validators can stake tokens to participate in this verification, and if they attest to something false, their stake is slashed. This is the same security model that secures hundreds of billions of dollars in value across Ethereum and its restaking ecosystem.

The verification with GAIB is also embedded at the hardware level. Every H100 chip that ships from Nvidia’s factory has a unique cryptographic key physically burned into its silicon, serving as a fingerprint that cannot be changed or forged. So when a lender or a protocol wants to verify that a specific GPU is genuine, they just have to send a challenge to the chip, and the chip signs a response with that key. The signature is then checked against Nvidia’s certificate authority, which verifies that it is a real H100 chip, that it is running authentic firmware, and that it has not been tampered with.

Researchers have further pushed this to software-only fingerprinting that can measure the entire latency profile of a chip’s processing units and produce a physical signature unique to each individual die, much like a human fingerprint is unique to each person. This can distinguish individual GPUs with 100% accuracy and pin their physical location to within 44 kilometres of a claimed datacenter.

Last week, I argued that the compute market needs a settlement layer in which collateral is verifiable by anyone so that the forward curve becomes a public good. That layer is now being built, and it runs on crypto rails because no existing financial infrastructure can settle a compute credit between a lender in Tokyo and a GPU rack in Virginia in under a second. No paper-based filing systems can provide cryptographic proof that a GPU exists, is operational, and is not already pledged to someone else.

The question is whether it will be adopted fast enough. Over $200 billion in private credit has already been deployed for AI hardware, and that debt does not remain with the original lenders. It flows through insurance companies and target-date retirement products until it reaches the savings of people who have no idea their 401(k) is just four layers of intermediation away from a rack of GPUs.

Nvidia sits at the epicentre of all this. Their standing offer to buy back compute at pre-agreed levels is what makes these clusters bankable in the first place. But the floor is set by the same company whose next chip release lowers it.

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.