Hello,

For most of banking history, depositors have had no leverage. You’d park your money, which the banks would then lend out for a return that would be multiple times what they would pass on to you. Depositors accepted this arrangement because the alternative was worse; try saving your money from its worst enemy - time.

The national average savings account in America pays 0.6% interest, while the money parked in US Treasuries and money market funds earns at least 4%. This model survived so long because depositors didn’t have an easy alternative. Except, every once in a few decades, they do have one.

Stablecoins offer a dollar that moves 24/7 on the blockchain, settles in seconds, and costs a fraction of a cent to transfer. Although the law prevents stablecoin issuers from passing interest on directly to holders, DeFi composability allows a stablecoin holder to route funds into a lending protocol and earn 5-8% APY. This has given depositors an exit that doesn’t require them to trade off convenience for something new.

In today’s deep dive, we explore what banks are doing to stop the flight of deposits and how this will change the way world banks and moves their money.

Onto the story,

Prathik

How Depositors Behave

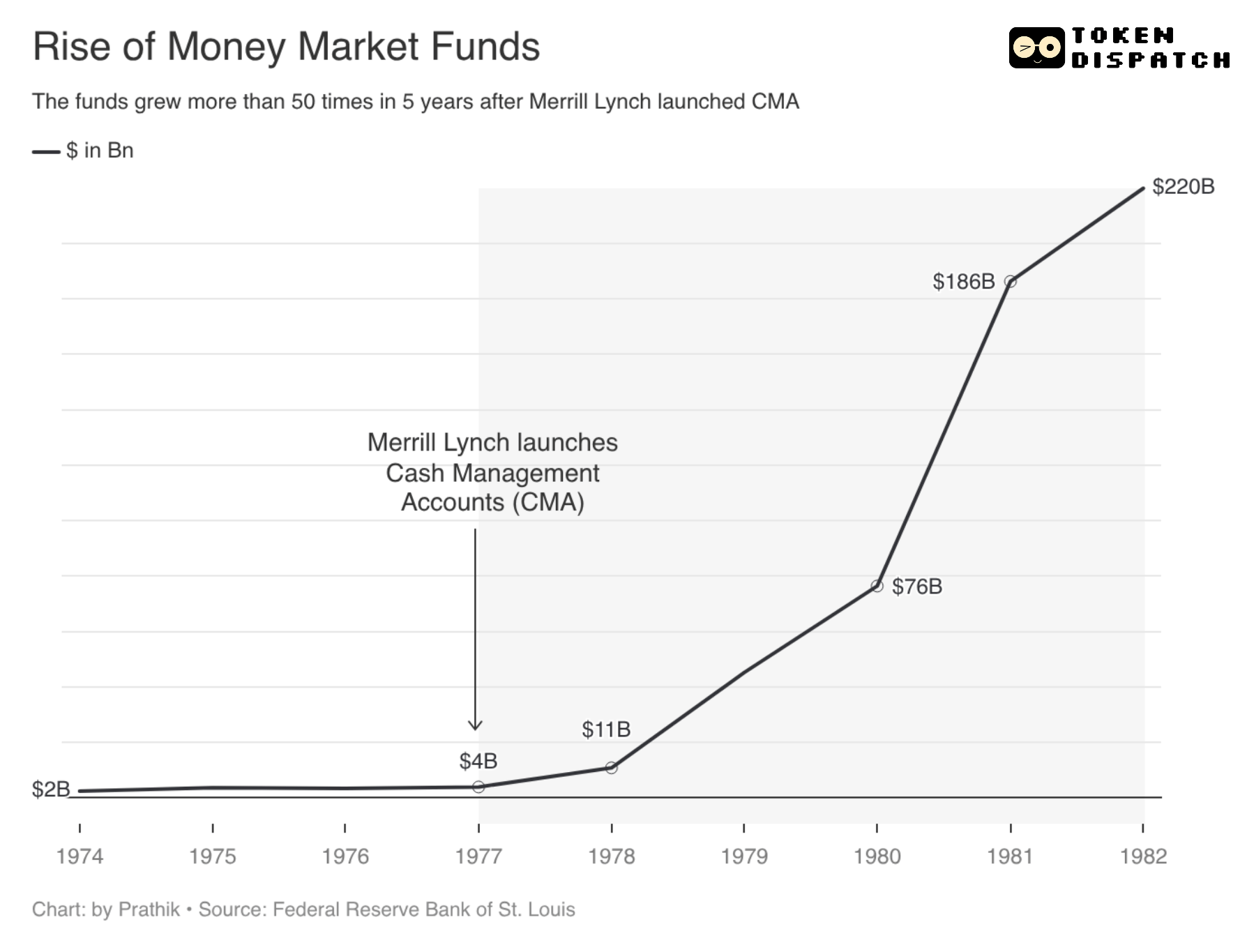

In 1977, wealth management and investment firm Merrill Lynch launched the Cash Management Account (CMA). At that time, Regulation Q had capped the interest US banks could pay on deposits at 5.25%. The US Treasuries yielded over 7%. Merrill found the loophole and used the CMA feature to sweep its users’ idle brokerage cash into money market funds every night. It also gave its clients check-writing and debit card access. Combined together, this let its clients earn interest at superior market rates while being able to use it as a checking account to withdraw money whenever they need.

Money market funds grew 55 times from ~$4 billion in 1977 to $220 billion in 1982, mostly at the expense of bank deposits.

The banks revolted. Eventually, Congress repealed the rate caps set by Regulation Q. Banks regained deposits by creating Money Market Deposit Accounts that offered higher yields. But it took nine years for this to happen, from the CMA’s launch to the repeal of the interest rate caps.

Depositors don’t wait as long anymore, especially with the evolution of technology that allows them to move money in minutes, if not faster.

When Silicon Valley Bank collapsed on March 8, 2023, customers initiated withdrawal requests worth $42 billion in less than eight hours. That’s roughly $1.5 million per second. More than 85% of the SVB deposits were uninsured. That explains the flight of deposits.

A prudent depositor will always move their money to a safer place, where it is likely to at least retain its value if not grow further.

Two Kinds of Digital Dollar

The response to this problem has led to two competing digital-dollar instruments. One sucks dollars out of the banking system, while the other retains them, albeit in a different form.

First is the stablecoin route.

When Circle issues USDC, it takes a customer’s dollar and parks it in US Treasuries. This dollar leaves the bank’s balance sheet. That’s one less dollar for the bank to loan out and earn interest income on. On the flip side, that dollar is no longer insured by the FDIC. If the stablecoin issuer shuts shop, the holder can no longer claim the dollar back.

The GENIUS Act, signed in July 2025 to regulate the issuance and use of stablecoins, bans stablecoin issuers from paying interest to holders. That’s similar to what Regulation Q did by capping deposit rates. But just as Merrill circumvented Reg Q through money market funds, issuers circumvent the yield ban by offering rewards. This is still being debated in the proposed CLARITY Act. A holder can also deposit their stablecoins into a lending protocol and earn yield.

This is an existential threat to the banking industry, which saw billions of dollars in deposits withdrawn within hours of the SVB collapse. Standard Chartered estimates that $500 billion in deposits could migrate to stablecoins by 2028, with US regional banks bearing the brunt due to their excessive dependence on net interest margin.

Although these projections may or may not materialise, the direction cannot be argued with. This is clear from the fact that the four largest US banks have joined hands for the first time in decades to tackle this problem in a different way.

Enter tokenised deposits.

One of the biggest USPs of stablecoins is the low-cost transfers and sub-second settlements. So, the banks decided to solve this.

Using tokenised deposits, a bank can issue a tokenised form of user deposits that can be moved on the blockchain at low cost and high speed. At the same time, the original dollar deposits remain on the bank’s balance sheet, allowing it to lend and earn interest income. These tokenised deposits still carry FDIC insurance.

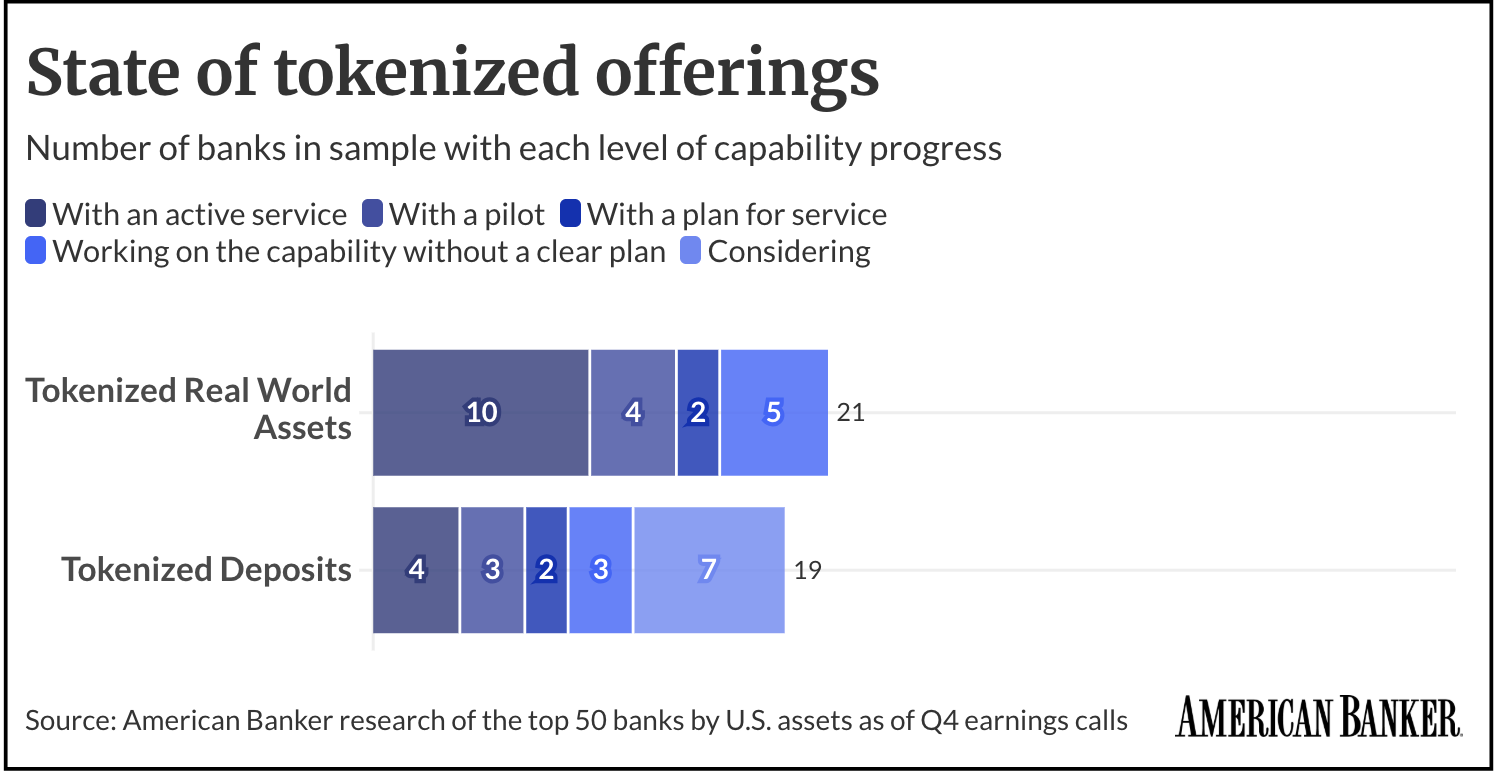

Two banking consortia have emerged to operate using this approach.

First is the Clearing House network, where JPMorgan, Citi, Bank of America, Wells Fargo and more than a dozen other banks are building a shared tokenised deposit platform targeting H1 2027. This consortium will be wholesale-focused and offer 24/7 settlement, programmable treasury settlement, and cross-border payments.

This tackles what the competition from stablecoins head-on.

The second is the Cari Network, formed by five regional banks including Huntington, M&T, KeyCorp, First Horizon, and Old National. Collectively holding about $780 billion in assets, this network is building a retail-facing tokenised deposit platform on ZKsync’s Prividium stack and plans to launch in Q4 2026. This move by regional banks explains the intensity of the risk they face from the flight of deposits to stablecoins and their disproportionate dependence on net interest margin to keep the lights on.

But what will depositors prefer?

In theory, depositors rarely choose the best product. Instead, they pick the product that offers them the least painful escape from the constraint they face at that moment.

In the late 1970s, that constraint was yield maximisation. Regulation Q made deposits safe but uncompetitive once market rates moved beyond what banks were allowed to pay. Merrill’s edge was that it unbundled the bank account into two things people wanted: market yield and everyday access. Banks eventually copied the bundle through MMDAs once regulation allowed them to pay market rates.

Stablecoins have the same edge as Merrill. They sit outside the traditional deposit stack, move money globally, plug into crypto venues, and make idle dollars more programmable. Their weakness is also similar to the weakness that money funds had relative to bank deposits. They are not insured bank liabilities. Trust depends on the issuer, the reserve stack, the redemption venue and the broader regulatory perimeter around them.

Tokenised deposits have the same edge as banks had in the 1980s. They keep the dollar inside the regulated banking system, preserve the bank’s lending economics, and attach the familiar comfort of deposit protection. But, the same guardrails that make tokenised deposits bank-like also make them less open, less portable and less composable than stablecoins. A bank deposit can become faster and more programmable. But the moment it becomes as open as stablecoins, the bank loses the control that made it a bank deposit in the first place.

This makes the competition more about who controls convertibility.

So, a third route has emerged, something that gives us a sneak peek into what the future of banking and money could look like.

The Bridge

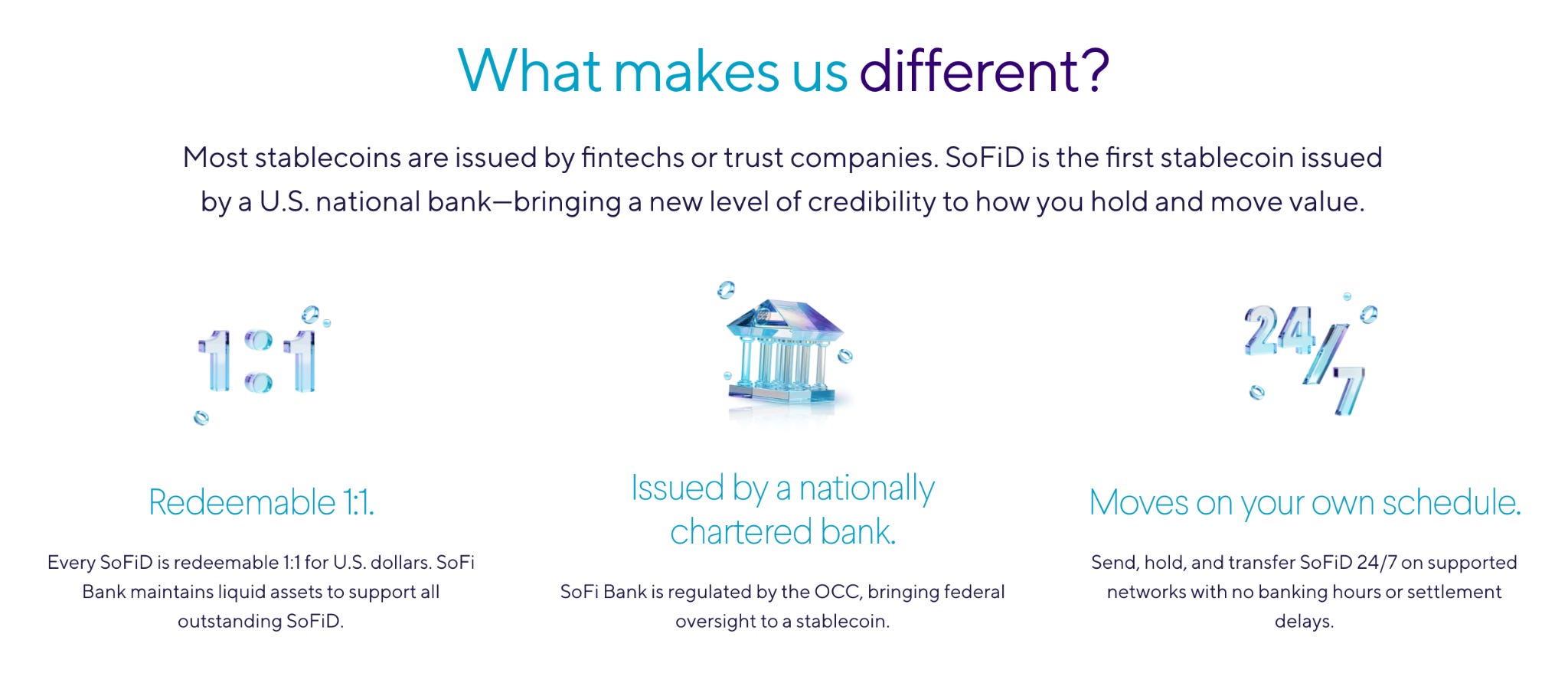

On May 27, SoFi Bank launched SoFiUSD, the first stablecoin issued by a US national bank. SoFiUSD is available on Ethereum and Solana and is issued via a mobile application to its 15 million members. It moves like any stablecoin around the clock and enables cross-border and sub-second settlements at a few cents in fees.

At the same time, SoFi also plans to let members convert SoFiUSD into tokenised deposits that earn interest and carry FDIC insurance within the same app. So users can choose to move their money as a stablecoin while holding it as tokenised deposits to get the best of both worlds. If they are not happy with the yields offered by banks, they can switch their tokenised deposits back to a stablecoin and deploy them across lending protocols to earn a higher yield.

SoFi may never become more decentralised than Circle or systematically more important than JPMorgan. But it has an edge in that it can collapse three user choices into one interface: a bank account, a stablecoin wallet, and, eventually, a tokenised deposit wrapper.

That is closer to what Merrill did than what a pure stablecoin issuer or a pure bank consortium is doing. SoFi is trying to get customers to stop choosing between the convenience of blockchain technology and the interest-earning potential of bank deposits.

The evolution of these products tells us why, when it comes to holding and moving money, the form of the product matters less than the convertibility it offers.

When stablecoins gave the depositors an alternative way to hold and move their money, banks first responded by lobbying to ban stablecoin yield and rewards. But I don’t see the banks winning this battle by lobbying. The only way they win this is by evolving to offer what crypto products deliver. Offer what stablecoins promise, but better. Let users move their money at the same lightning speed, with the same programmability, plus interest and insurance. Interestingly, the path to that evolution runs through blockchains.

This is the beauty of markets. They force incumbents to keep evolving until the system is optimised for its participants. Merrill’s CMA forced banks to repeal Reg Q and create Money Market Deposit Accounts. Stablecoins are forcing banks to tokenise deposits and build 24/7 settlement. In both cases, the incumbent didn’t die. It had to pick lessons from the innovators and evolve to stay relevant.

This evolution will have the sharpest impact on regional banks. They depend more heavily on net interest margin and have less room to absorb deposit flight than the largest banks. If they offer only a better bank account, they lose the dollars that want mobility. If they offer only crypto-like speed, they give up the protection and lending economics that made them banks in the first place. Cari is their attempt to defend both. The Clearing House consortium is the large-bank version of the same defence. SoFi is the more aggressive version: turn the bank into the bridge before someone else builds a bridge around it.

In the past financial cycles, the first entrant usually wins by exposing an inefficiency. The incumbent survives by absorbing the feature once the inefficiency becomes too important to ignore. Merrill exposed the gap between capped deposit rates and market yield. Banks eventually absorbed that feature through MMDAs. Stablecoins exposed the gap between banking-hour settlement and internet-hour money movement. Banks are now absorbing that feature through tokenised deposits and 24/7 settlement.

The edge keeps moving from the product that first reveals the problem to the institution that can bundle, regulate and distribute the solution at scale.

We have been writing lately about how crypto, or blockchain, if I were to be more politically correct, is emerging as fintech infrastructure.

Read: Every Exchange is an ‘Everything Exchange’

That thesis holds here, too. Crypto is not replacing bank deposits as much as it is forcing them to reveal what each part of the product is worth. Yield is one layer. Settlement is another. Insurance is another. Convertibility may be the most valuable layer of all.

Either way, the deposit won’t die. It will just get unbundled and rebuilt. The winner will be the one who lets money move between safety, yield and speed with the least friction.

That’s it for today. I will be back with the next one.

Until next time, stay curious,

Prathik

Token Dispatch is a daily crypto newsletter handpicked and crafted with love by human bots. If you want to reach out to 170,000+ subscriber community of the Token Dispatch, you can explore the partnership opportunities with us 🙌

📩 Fill out this form to submit your details and book a meeting with us directly.

Disclaimer: This newsletter contains analysis and opinions of the author. Content is for informational purposes only, not financial advice. Trading crypto involves substantial risk - your capital is at risk. Do your own research.